MPC - Marathon Petroleum: In It For The Long Run

2023-12-19 01:12:55 ET

Summary

- Marathon Petroleum is the largest refining system in the US, with a dominant position in gasoline and distillates wholesaling.

- The company focuses on capital returns, utilizing surplus cash flow for buybacks and maintaining a competitive dividend yield.

- MPC has made progress in reducing costs and is exploring cost-effective capital projects to improve reliability and margins.

Marathon Petroleum ( MPC ), holds the distinction of operating the largest refining system in the U.S., boasting an oil refining capacity of 2.9 million barrels per day (MMBbl/d). It stands out as a dominant wholesaler of gasoline and distillates. The company's operations encompass an integrated midstream business, facilitating the transportation, distribution, and marketing of oil and refined products, alongside the management of natural gas and natural gas liquids (NGLs). Anticipating a positive trajectory, I foresee Marathon's shares continuing to gain strength due to several key factors. These include the company's peer-leading free cash flow ((FCF)) and capital return yield, bolstered by its substantial presence in the PADD 2 and 3 refining regions. Marathon presents an appealing value proposition as well as a sum-of-the-parts value.

Capital Returns Are the Main Focus of the Management Team

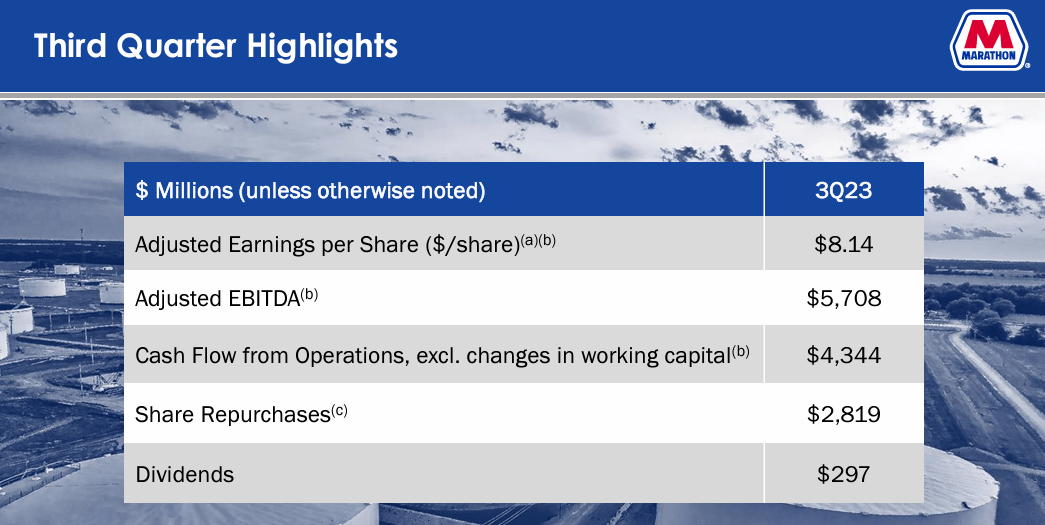

Marathon's dedication to utilizing surplus cash flow through buybacks has significantly slashed its share count by 40% since its inception. As part of its third quarter reporting, the company announced that there's an $8.3 billion allocation for buybacks from the recently augmented authorization, whereas the third-quarter cash/investment stood at $13 billion (inclusive of $1 billion in MPLX) alongside a targeted cash balance of $1 billion at MPC. Projections indicate an approximate $5 billion post-dividend free cash flow for 2024, sustaining the momentum for buybacks into the upcoming year, exemplified by around $1 billion in October buybacks. The company recently upped its dividend by 10% last quarter, yielding 2%, and has pledged to maintain an evolving and competitive yield, although buybacks continue to be the favored avenue for capital returns.

{kind=link}

There Remains Room For Further Cost Efficiencies

Management at Marathon has made considerable headway in reducing costs, yet they acknowledge there's more to be done despite achieving competitive cost levels akin to the industry's best performers. Asset reliability has been maintained amid these efforts. While progress has been made on the commercial front, specifics are deliberately withheld for competitive reasons. According to analyst estimates, MPC has sector leading EBITDA and cash margin per barrel among its industry peers. Projects like the Martinez Renewable Fuels initiative are progressing as scheduled, anticipated to hit full capacity by year-end, while the Galveston Bay reformer is slated to resume operations this quarter. MPC intends to disclose separate results for RD now that Martinez is operational in the coming quarters. Looking ahead, Marathon is exploring cost-effective capital projects that could bolster reliability and margins. Yet, they haven't highlighted any significant impending ventures, mentioning that the economic viability of Sustainable Aviation Fuel ((SAF)) doesn't currently meet their expected return thresholds. I expect some visibility around these items during either the upcoming fourth quarter call or early in the new year.

The Macro Outlook Remains Constructive

Marathon maintains its anticipation of an improved mid-cycle margin setting in 2024, driven by fundamental supply/demand dynamics, the reduced investment and closures of refining capabilities following the COVID era, and inherent advantages for U.S. refiners stemming from feedstock, energy expenses, and refinery intricacies. Management perceives demand as stable throughout its network, yet they advise against relying solely on weekly DOE trends. The TMX (Trans Mountain Expansion) is predicted to constrict Western Canadian Select (WCS) once operational, although MPC (Marathon Petroleum Corporation) foresees some counterbalancing effects from its West Coast system. The pipeline capacity is expected to gradually replenish in the medium term.

Major drivers for the company include finalizing the ongoing $15 billion share buyback plan, considering further expansion of the capital return initiative due to the company's robust free cash flow performance, the amplification of discrepancies in heavy-sour differentials, and advancement toward finishing the conversion of the Martinez refinery into renewable diesel production.

What Can Go Wrong?

The biggest risk for any refiner is spreads and this is true in the case of Marathon as well. To a smaller extent, there is risk associated with execution of its business strategy which is currently focused on extracting increased efficiencies in its operations. A misstep in the latter could result in a decline in MPC trading multiples.

Valuation Will Normalize Alongside the EBITDA:

{kind=link}

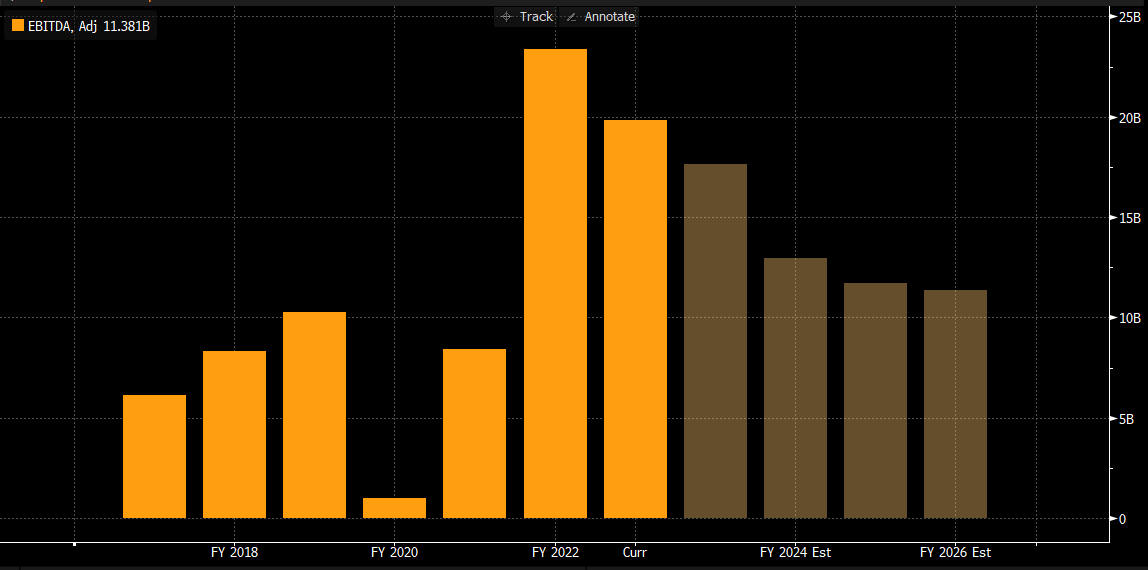

There is value in holding MPC shares today for getting exposure to a robust refining business, however, the upside isn't terribly exciting given strong move the shares of MPC have experienced through 2023, rising 30.4% through 2023 and returning 33.5% including dividends. Following an exceptional 2022, the sell-side expects for the EBITDA to begin normalizing towards a run-rate of ~$12B annually. This number is well above the levels we saw before COVID and the strength is partially a result of industry-wide changes as well as a focus on efficiencies at MPC. Upside to these numbers can come from positive changes to the crack differentials. We are already seeing some widening of the heavy-sour differentials which had reached very tight levels during the middle of 2023. For investors seeking a dividend linked return, it should be noted that MPLX ( MPLX ) which is the master limited partnership formed by MPC carries a more hefty 9.4% dividend yield. Almost 64% of MPLX shares are currently held by Marathon. Applying a 7.5x multiple to its 2024 estimate gets us to a target price of ~$168/share, which is ~12% higher than today's levels. Backstopping the current value of the shares are the aforementioned levels of dry powder left for more buybacks as well as the modest 2.2% dividend yield on the MPC shares. At today's levels, MPC is a hold and becomes more attractive if valuations approach 5.5-6x EBITDA, or approximately 15% lower on a per share basis.

For further details see:

Marathon Petroleum: In It For The Long Run