MPC - Marathon Petroleum Is A Buyback Monster

2023-11-09 11:05:56 ET

Summary

- Marathon Petroleum is America's largest pure-play refinery and has outperformed its peers in the energy industry over the past decade.

- Despite challenges such as subdued gasoline demand, MPC's strategic positioning and global market presence contribute to its success.

- MPC's recent financial performance, strong dividend growth, and attractive valuation make it a promising investment, although potential volatility should be considered.

Introduction

The energy industry consists of three major segments.

- Upstream - companies that produce oil and gas.

- Downstream - companies that turn oil and gas into value-added products like gasoline and diesel.

- Midstream - companies that connect upstream to downstream and any buyer to a seller. In other words, operators of pipelines and storage.

Eland Cables

In this article, I'll focus on downstream. Marathon Petroleum ( MPC ) is America's largest pure-play refinery and part of what used to be the integrated Marathon Oil ( MRO ) company.

After 2011, Marathon Oil spun off Marathon Petroleum, which formed MPLX ( MPLX ), a midstream giant that owns its pipelines.

I have covered both Marathon Oil and MPLX in the past few months as well.

Over the past ten years, all of these companies have outperformed their peers, as shown in the chart below, offering the best in upstream, midstream, and downstream.

Having said that, MPC had the best performance, returning 240% since the end of 2013.

The company, which owns 13 major refineries with the capability of producing close to three million barrels of product per day, is a superstar that not only benefits from a healthy balance sheet and efficient operations but also its focus on share buybacks.

On top of that, it pays a 2.3% dividend that comes with a low payout ratio and strong dividend growth.

In this article, I'll dive into the risk/reward of this company, using its just-released earnings, industry fundamentals, and its valuation.

So, let's get to it!

Weathering The Storm

The economy isn't in a good place. While we're not in a recession, it's not a favorable environment for cyclical demand.

For example, the ISM Manufacturing Index, which is a leading indicator, is back below 47, which is more than three points below the neutral 50 level. It's now close to levels seen during the 2011 debt crisis, the 2015 manufacturing recession, and the pandemic.

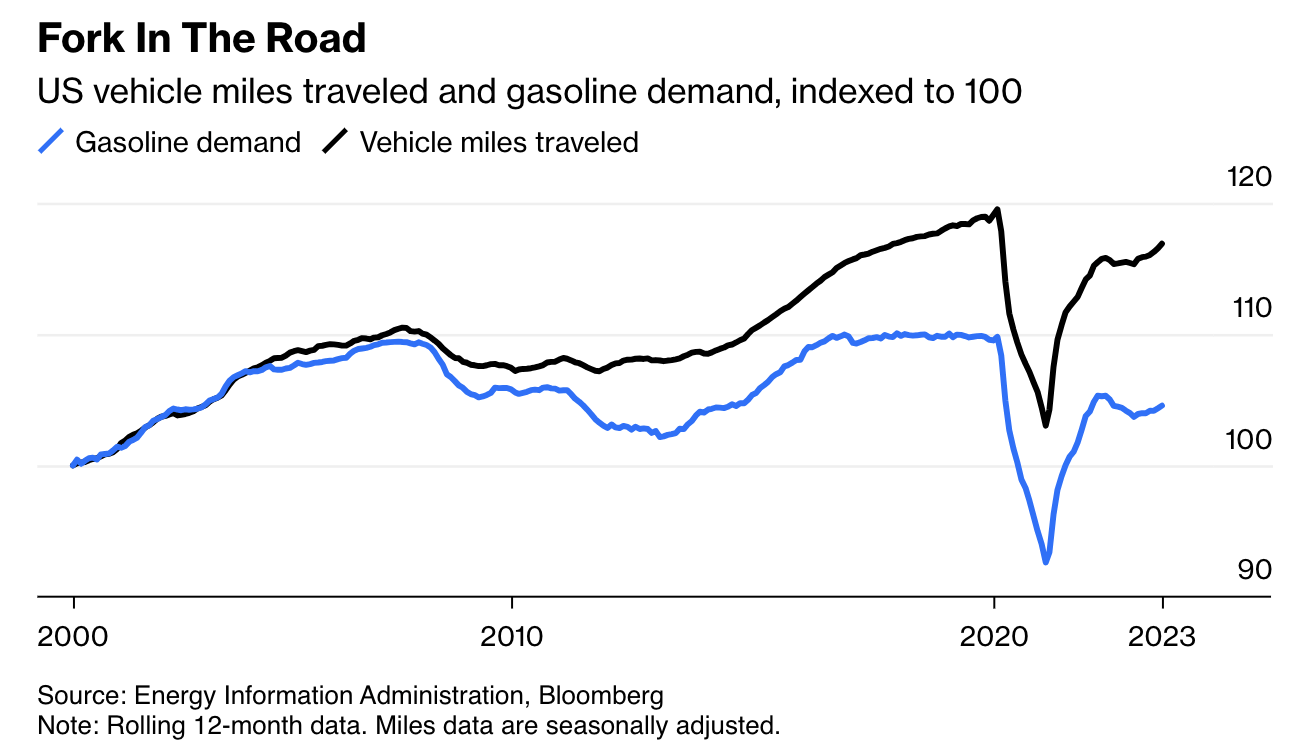

Meanwhile, gasoline demand in the U.S. is well below pre-pandemic levels.

As reported by Bloomberg at the end of last month (emphasis added):

US gasoline demand accounts for roughly one-in-ten of every barrel of crude oil refined. A shock report in late September indicated demand had slumped to a 25-year seasonal low (barring the pandemic). Such weekly estimates are subject to revision, but even the more robust monthly data indicate structural change. While Americans are back to driving almost as much as before the pandemic, gasoline demand remains stubbornly subdued .

{kind=link}

Bloomberg

While better fuel economy vehicles and more EV sales have something to do with it, it doesn't help that a big driver of gasoline demand is economic growth.

Nonetheless, MPC has been a superstar since the pandemic, benefitting from higher margins on each barrel of finished products and its ability to buy back stock, artificially enhancing the per-share value of its business.

Furthermore, during its 3Q23 earnings call, the company noted that, globally, oil demand reached a record high, reflecting the increasing need for affordable and reliable energy worldwide.

Steady demand was observed in both domestic and export markets, with growth in gasoline, diesel, and jet fuel demand. Global supply constraints persisted, and capacity additions progressed slowly.

See, the thing is that it's a global market, which means that export markets are just as important as domestic markets. After all, shortages in other markets "suck" supply out of other markets.

As the U.S. is one of the world's largest oil producers, it's a great market for refinery companies that want to service domestic demand and benefit from exports. Marathon Petroleum is one of these companies.

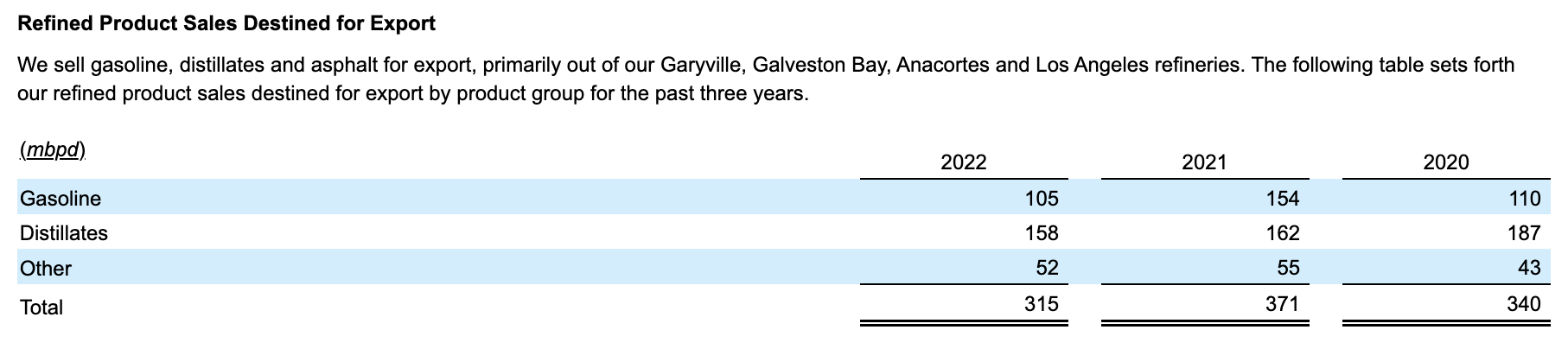

Some of the company's largest refineries have great export access, allowing the company to export more than 300 thousand barrels of product per day.

{kind=link}

Marathon Petroleum Corporation

The company is also very efficient.

When OPEC+ production reductions added pressure to medium-sour differentials.

While crude differentials generally narrowed, WCS widened. As a result, the company strategically positioned itself to run heavy Canadian crude at refineries across PADDs 2, 3, and 5.

These are the five PADDs:

U.S. Energy Information Administration

Even better, the company continues to benefit from lasting demand, tight global supply, and elevated refinery margins. Favorable diesel margins in Europe are helping export and pricing demand.

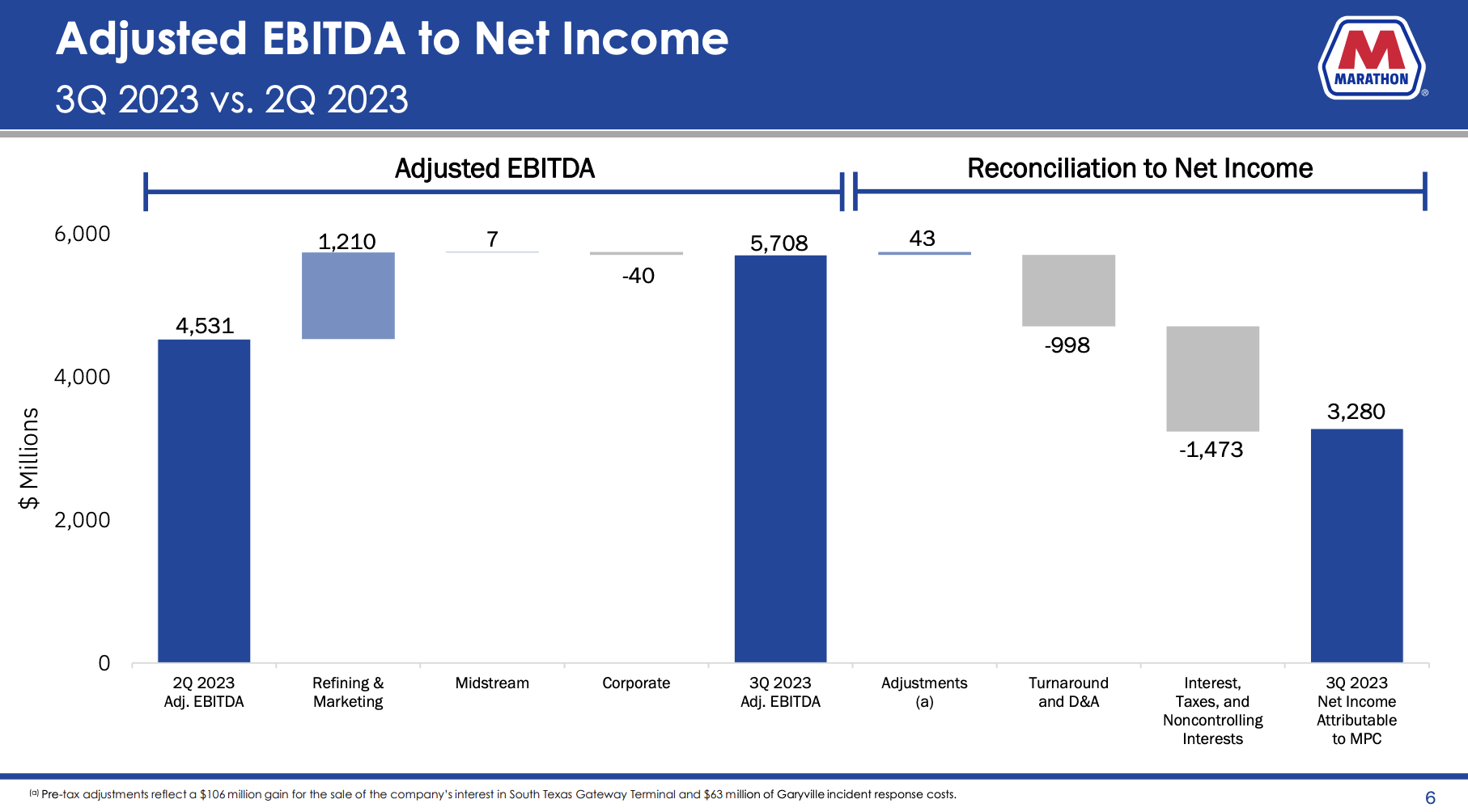

Due to these developments, the company reported adjusted earnings per share of $8.14 in the third quarter. This number excludes a $106 million gain on the sale of MPC's 25% interest in the South Texas Gateway Terminal and $63 million in response costs related to an unplanned outage at Garyville.

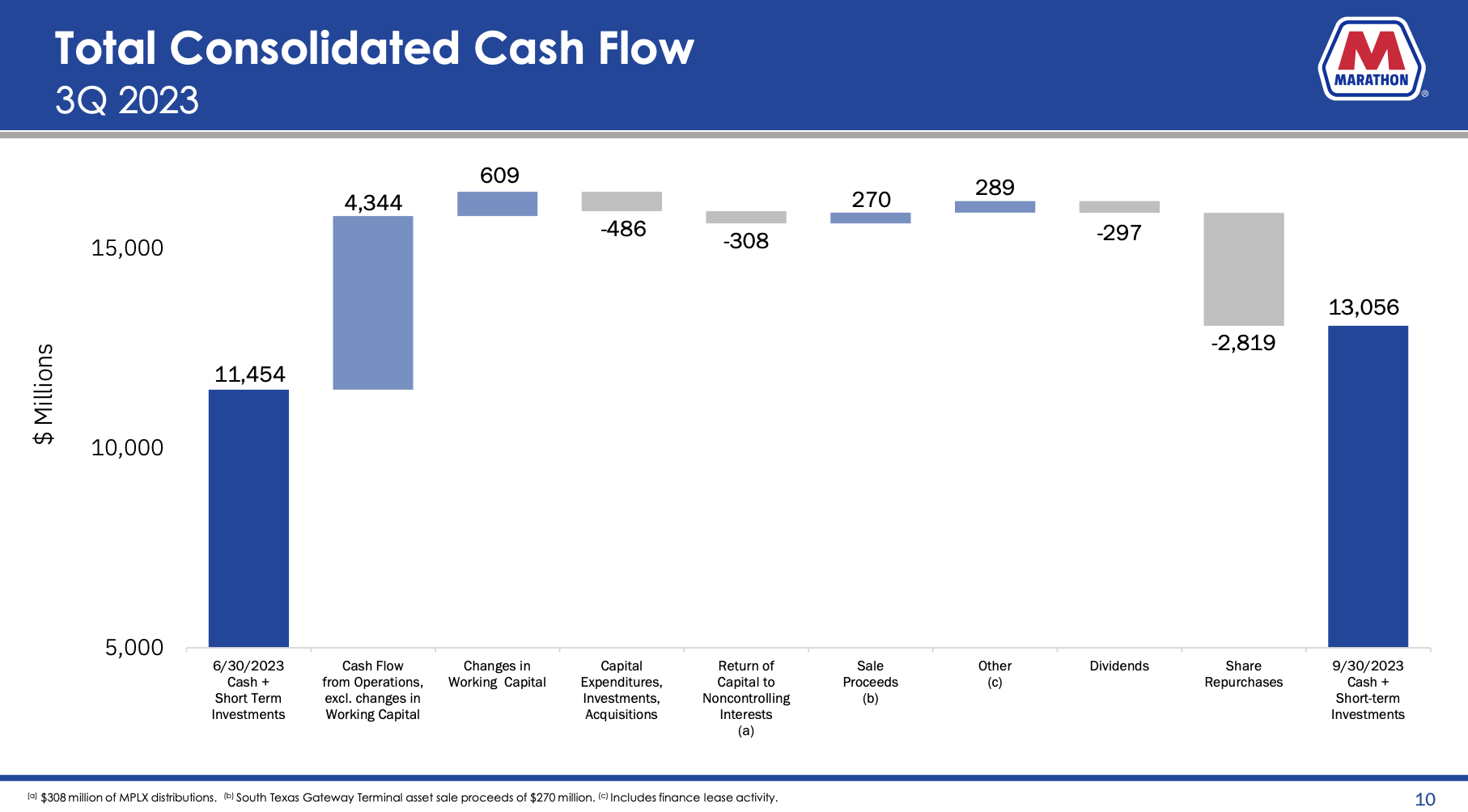

Adjusted EBITDA for the quarter was $5.7 billion, and cash flow from operations, excluding working capital changes, exceeded $4.3 billion.

{kind=link}

Marathon Petroleum Corporation

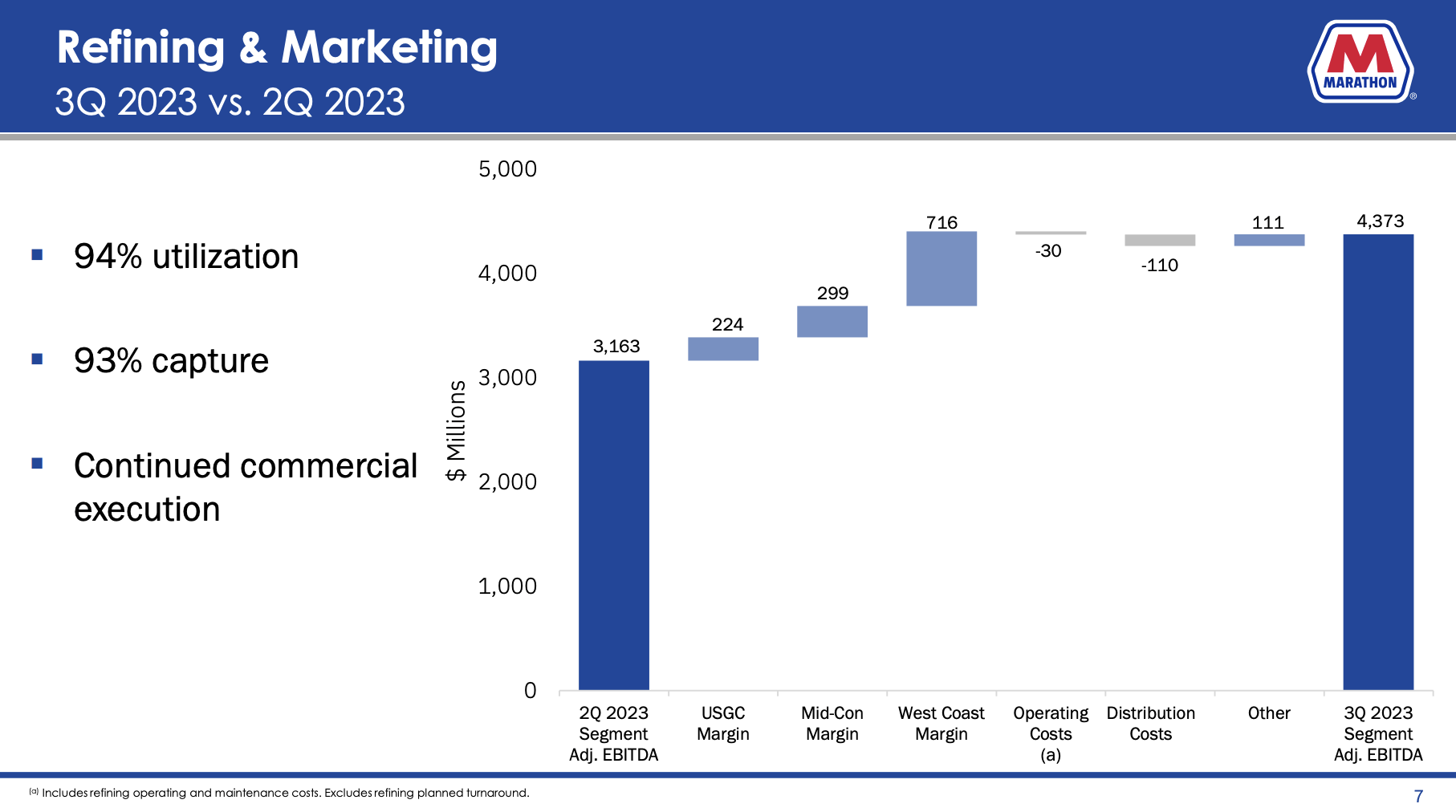

The Refining & Marketing segment ran at 94% utilization, processing nearly 2.8 million barrels of crude per day.

Sequentially, per-barrel margins were higher across all regions, driven by higher crack spreads.

However, unplanned downtime impacted the two largest refineries, resulting in lost crude throughput, which is also visible in the overview above.

{kind=link}

Marathon Petroleum Corporation

The Midstream segment delivered strong third-quarter results, with adjusted EBITDA flat sequentially and 3% higher year-over-year. MPLX, the Midstream business, increased its quarterly distribution by 10%, and MPC expects to receive $2.2 billion in cash from MPLX annually.

On a side note, I discuss the MPC/MPLX relationship and MPLX dividend hike in detail in the article I mentioned at the start of this article.

Outlook & Shareholder Returns

Thanks to strong demand, the company generated sufficient cash to handsomely reward shareholders.

Operating cash flow, excluding changes in working capital, was over $4.3 billion in the quarter. Working capital provided a $609 million tailwind, driven primarily by increases in crude oil prices.

Capital expenditures and investments totaled $486 million, and MPC returned nearly $3.1 billion to shareholders via share repurchases and dividends during the quarter.

As usual, the biggest chunk of shareholder returns consisted of buybacks, its favorite way of returning cash. Note that the same goes for its former parent, Marathon Oil.

{kind=link}

Marathon Petroleum Corporation

The company isn't just buying back stock because of its healthy balance sheet (a sub-1.5x 2024E net leverage ratio and a BBB credit rating), but also because it is upbeat about its future.

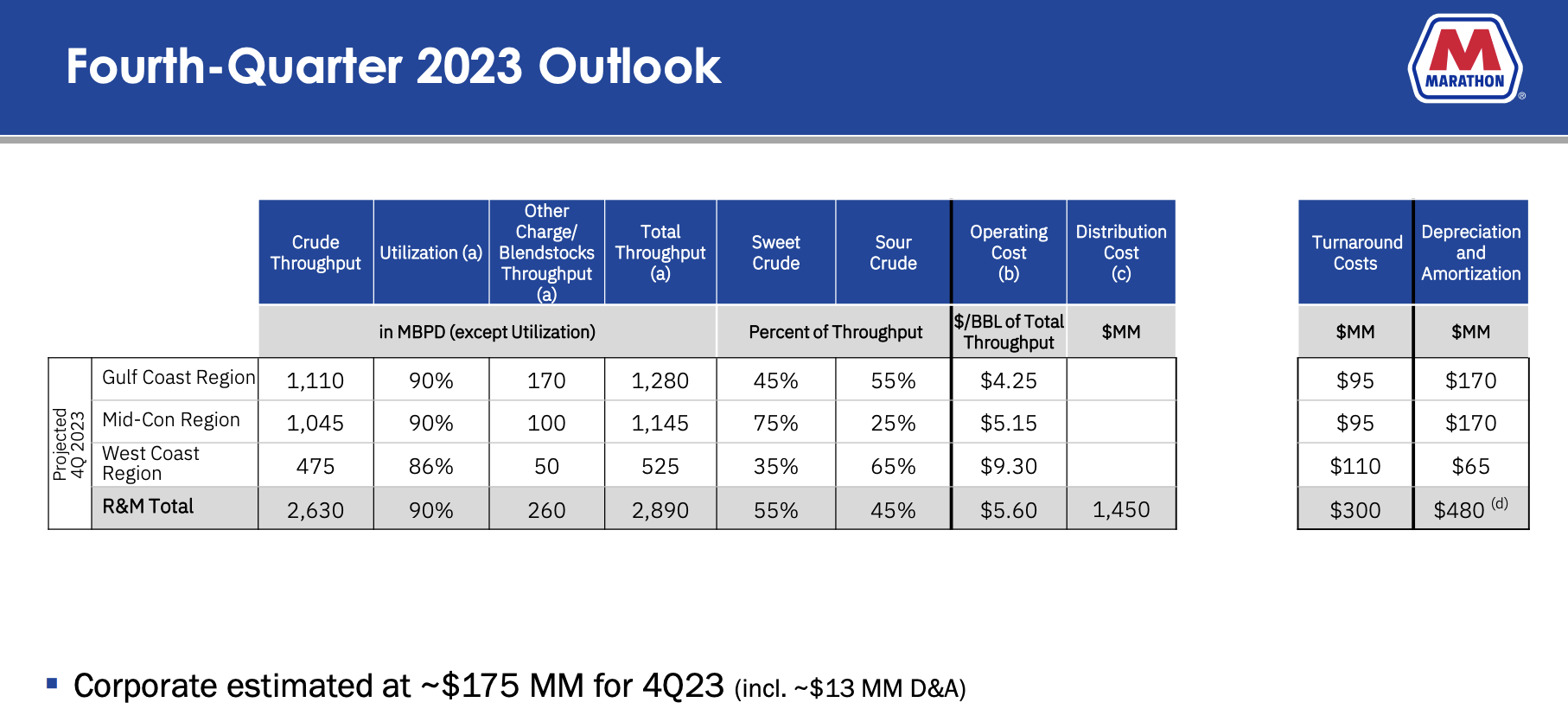

Operating costs per barrel in the fourth quarter are expected to be $5.60, higher sequentially due to higher energy costs, particularly on the West Coast, and higher project-related expenses associated with planned turnaround activity.

Distribution costs are expected to be approximately $1.4 billion, and corporate costs are expected to be $175 million in the fourth quarter.

The company has approximately $8.3 billion remaining under its current share repurchase authorization. This translates to 15% of its market cap!

Over the past five years, MPC has bought back more than 40% of its shares, making it the most aggressive buyback corporation on my radar.

Furthermore, with regard to its fourth quarter, the company expects crude throughput volumes of over 2.6 million barrels per day in the fourth quarter, representing utilization of 90%.

Turnaround activity is expected to have a higher impact on units in the fourth quarter, leading to lower utilization.

{kind=link}

Marathon Petroleum Corporation

Adding to that, and with regard to financial health, the company highlighted an interesting metric during the Q&A session of the 3Q23 earnings call.

With $13 billion in cash, the company is comfortable with $1 billion on the balance sheet. Everything beyond that will likely be used to repurchase shares and grow the dividend.

{kind=link}

Seeking Alpha (MPC Dividend Scorecard)

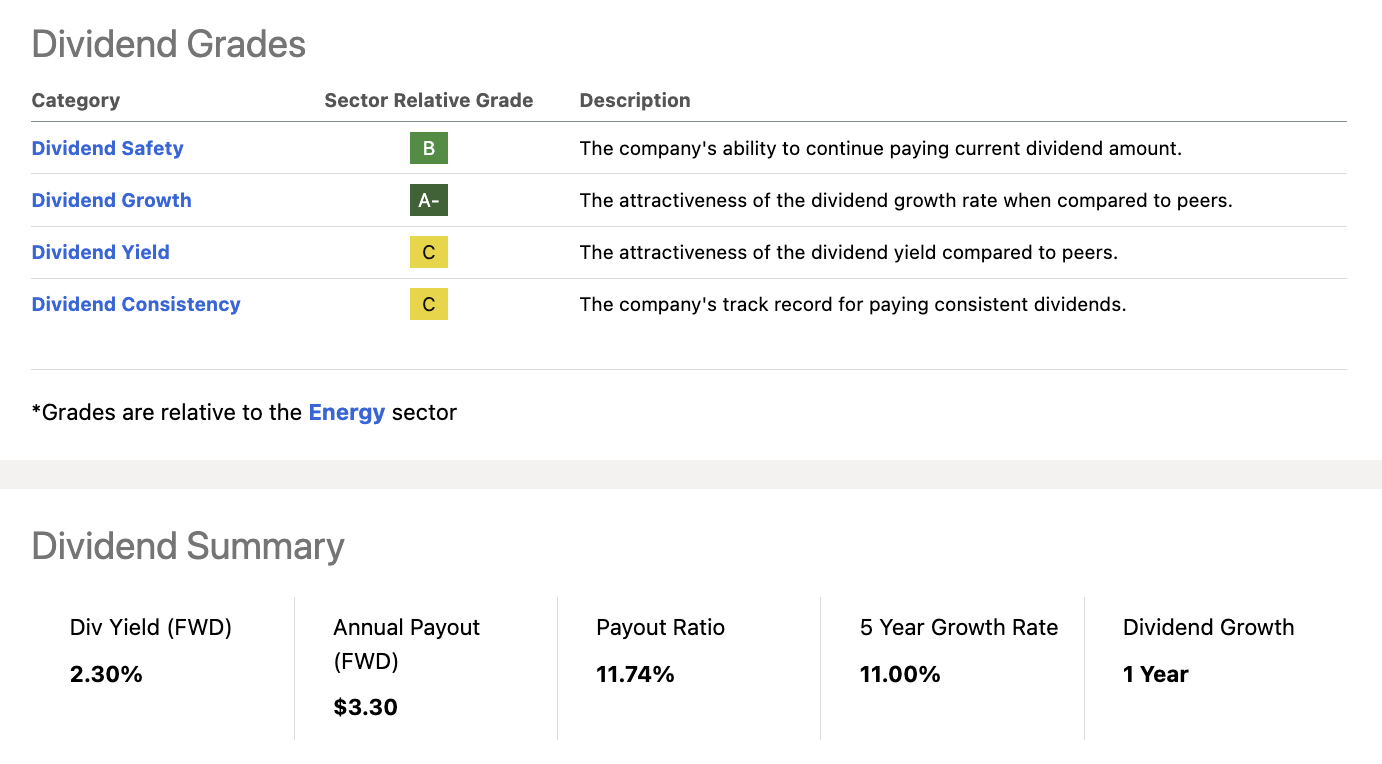

The current yield is 2.3%, protected by a sub-12% payout ratio and a five-year dividend CAGR of 11.0%.

Last month, the company boosted its dividend by 10%.

The company, which was spun off after the Great Financial Crisis, has never cut its dividend. During the pandemic, it kept its dividend unchanged. While this caused its debt load to jump, it is now in great financial shape and in a great spot to maintain strong dividend growth, even if economic growth slows further.

With that said, what about the valuation?

Valuation

This is the tricky part - and has been for a while.

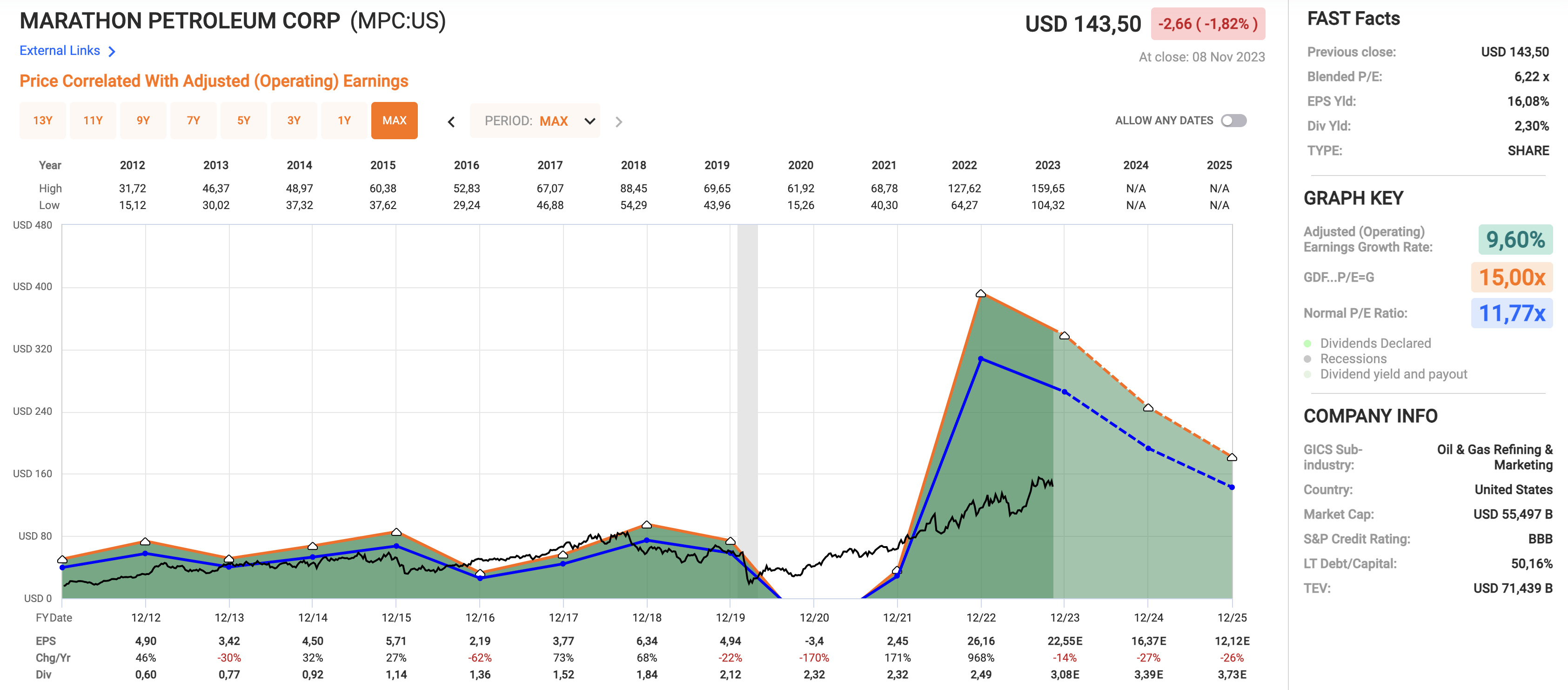

Since its spin-off, MPC has traded close to a normalized P/E ratio of 12x. That's a fair valuation for a company as cyclical as MPC. As we can see at the bottom of the chart below, MPC barely has any "normal" years. It either sees steep contractions due to economic challenges or high growth when demand improves.

Currently, MPC trades at a blended P/E ratio of just 6.2x!

Looking at the chart below, a return to its fair valuation would indicate a fair stock price of more than $240. That would be $100 above its current ~$140 stock price.

{kind=link}

FAST Graphs

The only reason why MPC isn't taking off is the fact that analysts believe that the company will see three consecutive years of steep EPS contraction caused by normalization in global refinery margins.

Although this assessment makes sense, I do not expect the decline to be this steep.

I believe that MPC could see a $190 stock price by the end of 2025.

However, I do not expect that to happen without mid-term volatility, as I still believe that we're in for a recession in 2024.

I will stick to a Buy rating, given my favorable outlook, but I would not be buying after surges.

An entry price close to 1Q23 levels ($120-$130) presents an attractive buying point, with the ability to average down if the economy continues to weaken.

Buying on weakness is how I'm currently treating all of my investments - especially dividend growth investments.

On a long-term basis, I have little doubt that MPC can keep growing its dividend, aggressively buying back stock, and outperforming its peers.

However, please do not buy MPC if you want to avoid buying volatile stocks. MPC is much more volatile than most of the blue-chip stocks you may be familiar with. Please keep that in mind!

Takeaway

With a focus on share buybacks and a healthy balance sheet, MPC has returned 240% since 2013, offering investors a compelling proposition.

Despite challenges like subdued gasoline demand, MPC's strategic positioning, efficiency, and global market presence contribute to its success.

The company's recent financial performance, strong dividend growth, and attractive valuation make it a promising investment.

While we could see potential mid-term volatility, I believe a long-term Buy rating is justified, with an eye on entry points during market weakness for a better risk/reward.

For further details see:

Marathon Petroleum Is A Buyback Monster