MPC - Marathon Petroleum: Low Natural Gas Provides Support

Summary

- Marathon Petroleum is a refiner of oil products. Demand for refined products was abnormally strong in 2022. What's the outlook for 2023 like?

- A discussion of Marathon Petroleum's operating leverage.

- The impact of natural gas on Marathon Petroleum's operating expenses and how this could be a tailwind in H1 2023.

Investment Thesis

Marathon Petroleum ( MPC ) is one of the largest refiners in the US. Even though MPC has seen its stock take a breather in the past several weeks, I believe that this story is far from over.

I lay out the bull case, and highlight the impact that natural gas has on MPC's cost structure, as well as remark on MPC's attractive valuation.

I conservatively estimate that MPC is priced at 7x this year's free cash flow.

For 2023, despite the highly anticipated recession, I believe that demand will remain high. Why? Because this recession has been so well-telegraphed, that I believe this is already more than factored into MPC's share price.

Natural Gas Prices Could Provide a Tailwind

Feedstock costs, predominantly natural gas prices, have a substantial impact on MPC's bottom line. More specifically, 15% of MPC's operating costs are derived from natural gas.

Here's how MPC explained this on the earnings call :

We are expecting operating cost per barrel in the fourth quarter to be lower projected to be $5.30 per barrel for the quarter. This is primarily driven by expected lower natural gas and energy costs. As a reminder, natural gas has historically represented approximately 15% of operating costs.

Our natural gas sensitivity is approximately $330 million of annual EBITDA for every dollar change per MMBtu.

That means that if natural gas prices were to come down by approximately $2.5 to $3 MMBtu from Q3 2022 when natural gas prices hovered around $7 to $8 MMBtu, this would mean that on an annualized basis, from lower energy costs alone, MPC's EBITDA could be boosted annually by approximately $900 million.

If one was concerned that MPC's EBITDA could, in 2023, return to approximately $10 to $12 billion, lower natural gas prices could provide a welcome boost and support around 10% of MPC's annual EBITDA.

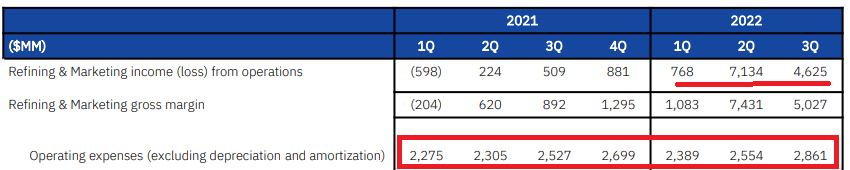

The Power of Operating Leverage

The graphic that follows is a stark reminder of the power of operating leverage.

{kind=link}

What you see highlighted above is that MPC's Refining & Marketing operating expenses are high and fixed, reaching approximately $2.3 to $2.9 billion.

In other words, small changes in MPC's revenues (not shown above), due to MPC's significant operating expenses, can have a weighty impact on MPC's bottom line prospects and cash flows.

Put another way, I believe that if we assume that 2023 is not likely to be as strong as 2023, MPC's considerable operating leverage could see MPC's net income cut by 50% in 2023, including the benefit from lower natural gas prices.

MPC Stock Valuation - 7x 2023 Free Cash Flow

Nobody doubts that 2022 was a record year for MPC. I suspect that Marathon's free cash flows could reach $15-$16 billion.

Now, the big question is how is 2023 going to fare. Let's assume that 2022 was an anomaly, driven in part by abnormal conditions earlier in 2022.

Let's work off the assumption that for 2023 MPC's free cash flow is cut by 50%. That would see MPC's cash flows at approximately $8 billion.

This implies that the stock is priced at approximately 7x this year's conservative estimates. Note, this 50% reduction in free cash flow estimate, is echoed in analysts' EPS estimates for 2023.

MPC analysts estimates

As you can see in the red arrows above, once we get further into 2023, analysts assume that MPC's EPS figures will get cut in half relative to 2022.

Put another way, 7x free cash flow is not only a more than attractive valuation, but on top of that, there is a 2.6% yield. Again, as I noted in my prior article , I don't believe that anyone is getting involved with MPC only due to its dividend yield, but at the end of the day, it's better to have some yield than none at all.

The Bottom Line

The one-line summary is this, Marathon Petroleum is well positioned to benefit from a strong refining market, particularly given its cheap valuation of 7x free cash flow.

In the analysis, I describe the potential tailwind from low natural gas prices, and how this could cut operating expenses by around $900 million annualized.

Finally, while the 2.6% dividend yield isn't a thesis needle mover, it's better to have it than not.

For further details see:

Marathon Petroleum: Low Natural Gas Provides Support