VLO - Marathon Petroleum Q2 Earnings: Why This Stock Is An Attractive Investment

2023-08-01 16:10:20 ET

Summary

- Marathon Petroleum's Q2 earnings show strong refinery demand despite economic weakness, leading to aggressive buybacks and dividend growth.

- MPC benefits from favorable refining margins and expansion into renewable fuels, supporting its earnings and growth prospects.

- Marathon's healthy balance sheet, low debt, and upbeat outlook make it an attractive investment, with the potential for a 32% stock price increase.

Introduction

Marathon Petroleum Corporation ( MPC ) is one of the refinery stocks that has been on my radar for many years and the biggest peer of my own refinery investment, Valero Energy ( VLO ).

The company just reported its quarterly earnings , which confirmed that refinery demand is surprisingly strong. Despite the economic weakness, MPC has tremendous earnings power and the ability to turn these tailwinds into aggressive buybacks and consistent dividend growth.

Furthermore, the company is expanding its business as it captures opportunities related to renewable fuel and its superior network of assets.

In this article, we'll discuss all of this and assess the risk/reward after the stock's 50% rally off its 52-week lows.

So, let's get to it!

Marathon Petroleum Is Doing Very Well

Marathon's second quarter was a success. The company reported $36.8 billion in revenue, which was $2.94 billion higher than expected. It helped the company to beat GAAP EPS expectations, which came in at $5.32, by $0.74.

That said, sales were down 32.1% year-on-year, which might seem like a stunning number - it is. However, it's caused by last year's unusual developments. The war in Ukraine and refinery shortages caused gasoline prices to explode, leaving companies like MPC with favorable margins.

Now, the environment is still strong, but not as strong as it was in 2022, which is a good thing for the economy.

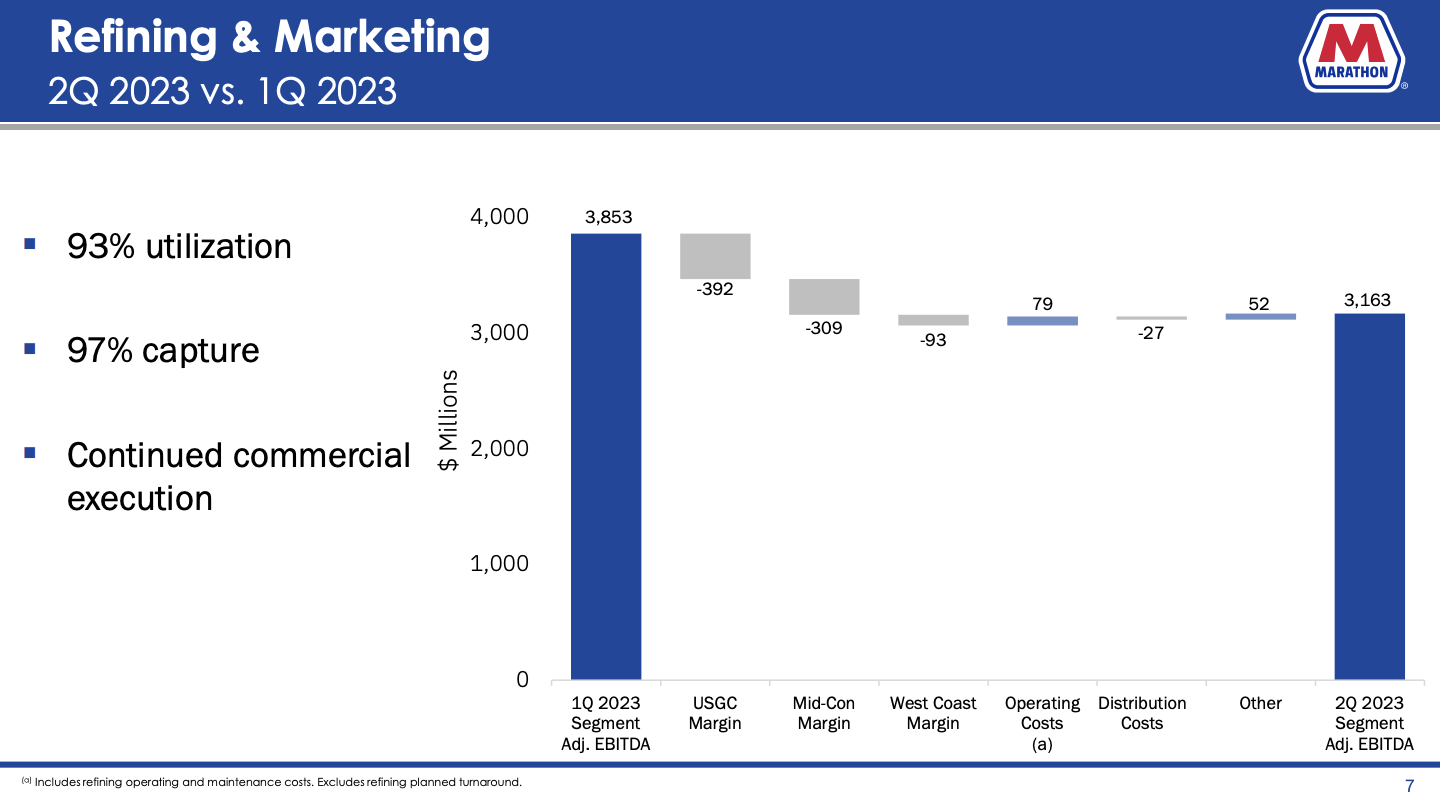

Having said that, in the Refining & Marketing segment, refining utilization increased by 4% to 93%, despite significant turnaround activity.

An incident at one of the refineries' catalytic reformers in Galveston Bay reduced crude throughput by approximately 2.5 million barrels and its capture by about 1%.

Marathon Petroleum Corporation

{kind=link}

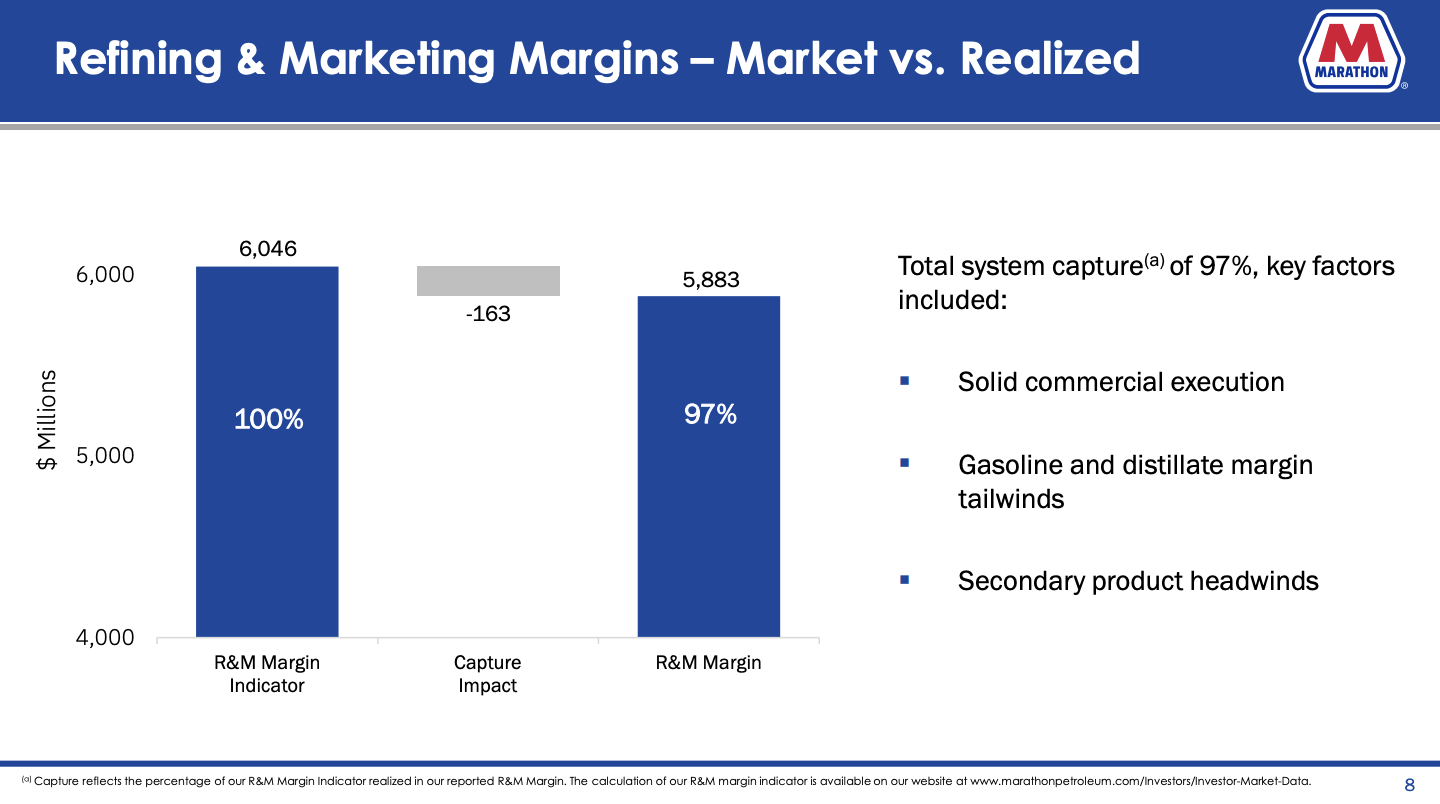

Please note that margin capture refers to the actual realized margin compared to a market-based benchmark margin.

Marathon Petroleum Corporation

{kind=link}

Sequentially, per barrel margins, were lower in the Gulf Coast and Mid-Con regions due to lower crack spreads and sour crude differentials.

Refining operating costs decreased to $5.15 per barrel in the second quarter, primarily due to higher throughput and lower energy costs.

As the overview above shows, the refining and marketing margin capture for the quarter was 97%, with the company's commercial team performing well despite planned and unplanned refinery downtime.

The company expects fluctuating capture results based on market dynamics but believes its capabilities will provide a sustainable advantage.

I have to agree with that, as fundamentals remain favorable.

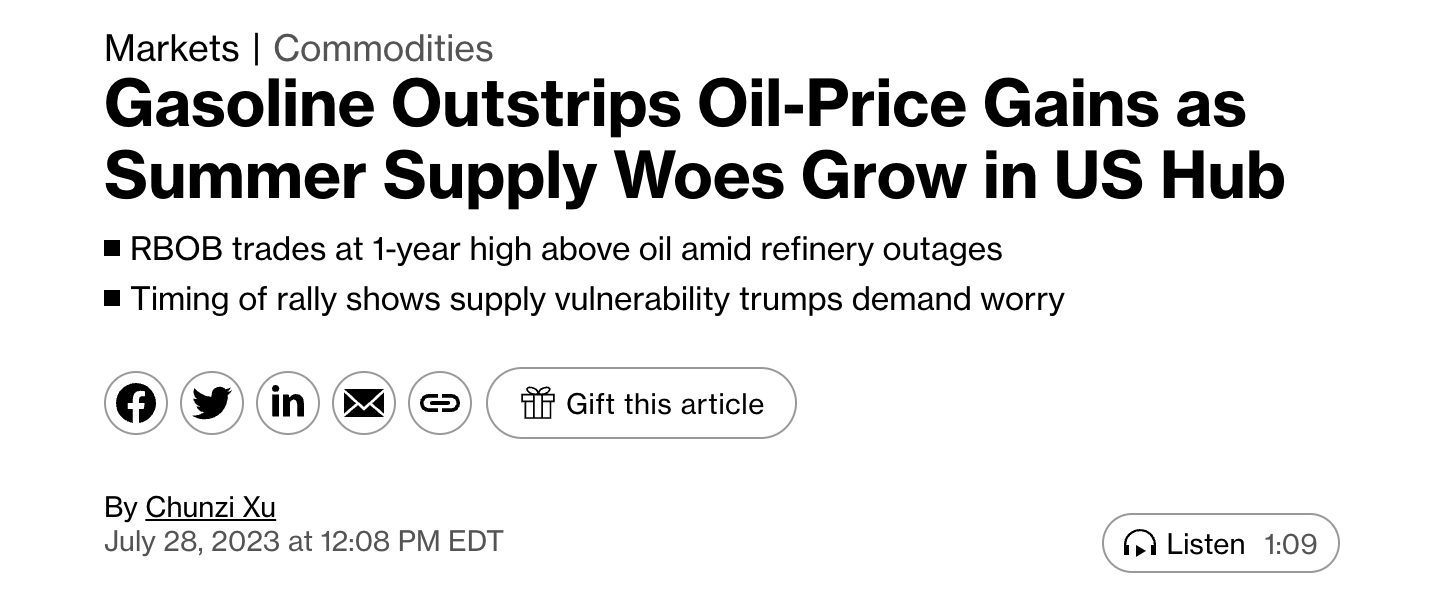

For example, at the end of July, Bloomberg reported that gasoline prices are having a strong revival, causing refinery margins to jump.

{kind=link}

According to Bloomberg (emphasis added):

Benchmark gasoline futures in New York surged to the biggest premium over WTI futures in more than a year . The latest jump is triggered by an extended shutdown at a Louisiana refinery, among others. The outages threaten to drain stockpiles in the Gulf Coast region, which are already 6% below the five-year average for this time of year.

[...] The timing of the gasoline rally also shows market participants are more worried about supplies than demand, even as refining capacity has grown with new projects coming online . Prices hit their highs only weeks after demand peaked ahead of the busy July 4th holiday.

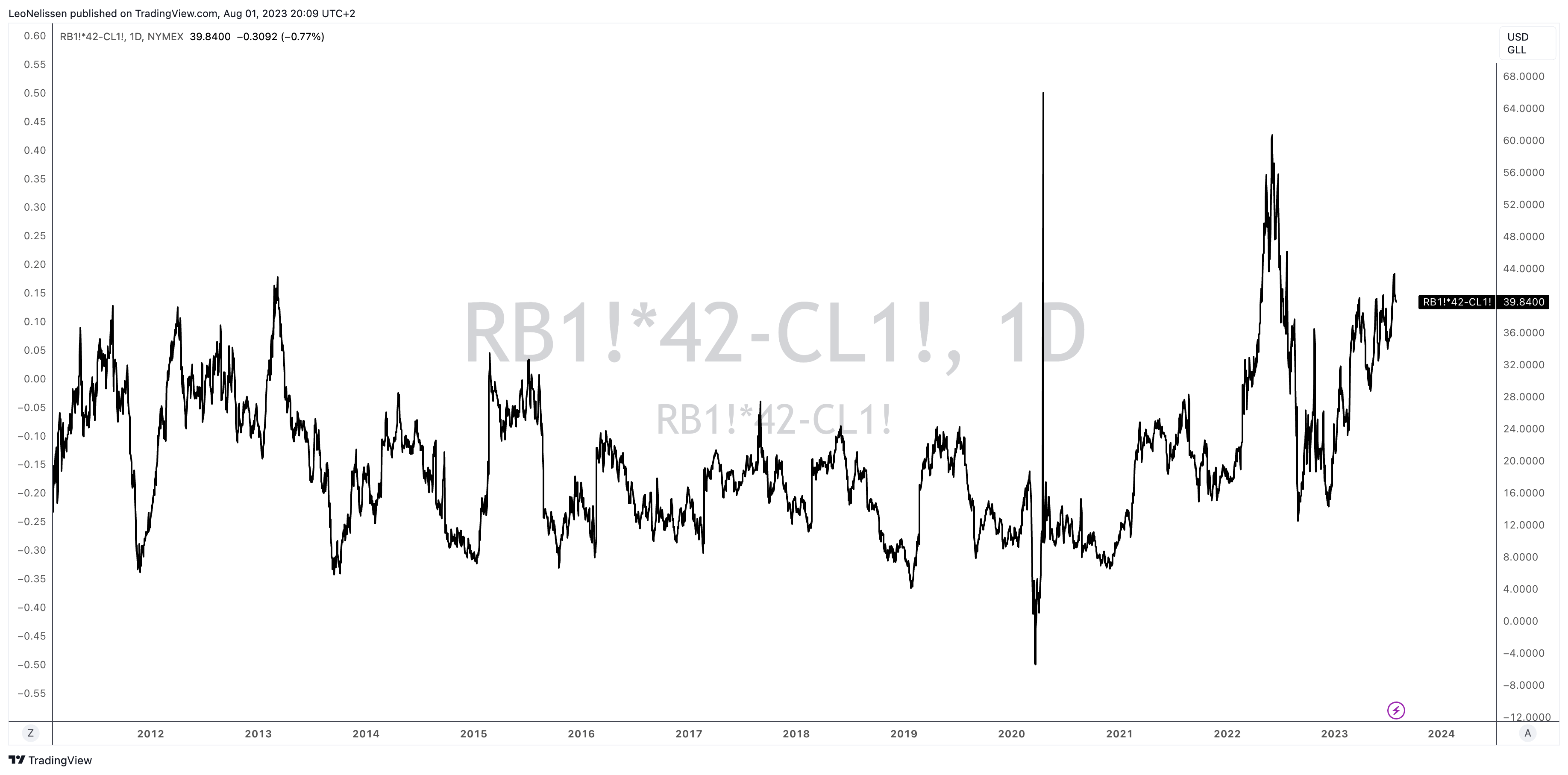

This is the chart Bloomberg used:

Bloomberg

When zooming out - using my chart - we see two things.

- Margins are well below their 2022 highs, which explains the year-on-year decline in revenue.

- Margins remain historically elevated, confirming that MPC remains in a good spot and Bloomberg's comments regarding the supply situation.

TradingView (RBOB Gasoline vs. NYMEX Crude Spread)

{kind=link}

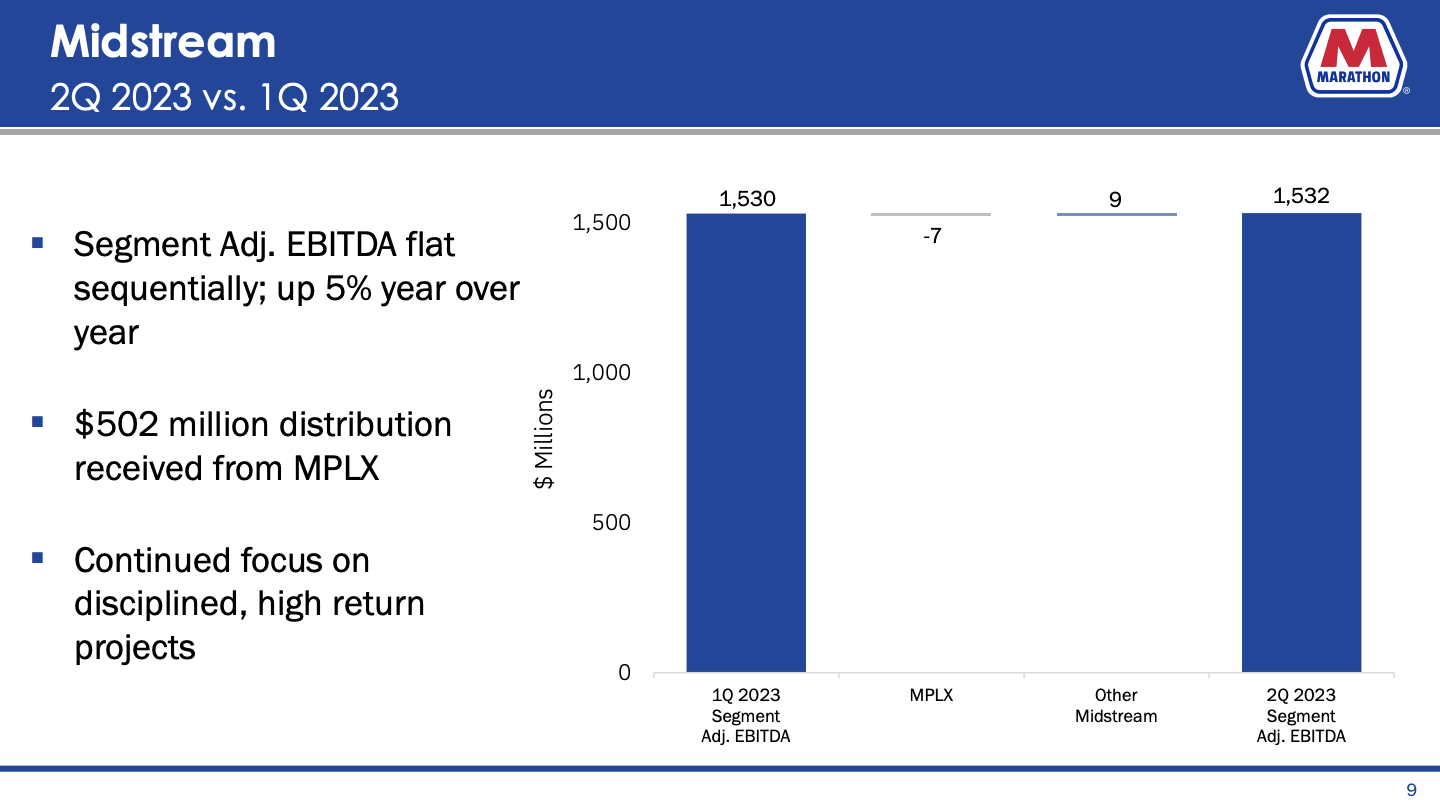

Furthermore, Marathon Petroleum has a Midstream segment, which is its majority ownership of midstream giant MPLX LP ( MPLX ).

This Midstream segment delivered strong second-quarter results, with adjusted EBITDA remaining flat sequentially but 5% higher year-over-year.

Marathon Petroleum Corporation

{kind=link}

The business continues to grow and generate strong cash flows, with high-return growth projects progressing in the Marcellus and Permian basins.

Focusing in on the Marcellus, by far our largest basin of G&P operations, we saw year-over-year volume increases of 3% for gathering and 5% for processing, driven by increased customer demand . Fractionation volumes grew 10% primarily due to recent increases to our fractionation capacity to meet in-basin demand for ethane.

[...] In the Permian, our production outlook is unchanged as crude prices remain strong and prices for associated gas do not significantly impact producer activity. Our integrated footprints in these resilient basins position the partnership with a steady source of earnings and growth opportunities. This quarter, we advanced our natural gas and NGL value chain strategies with the announcement of new projects in the Permian. - MPLX 2Q23 Earnings Call (emphasis added).

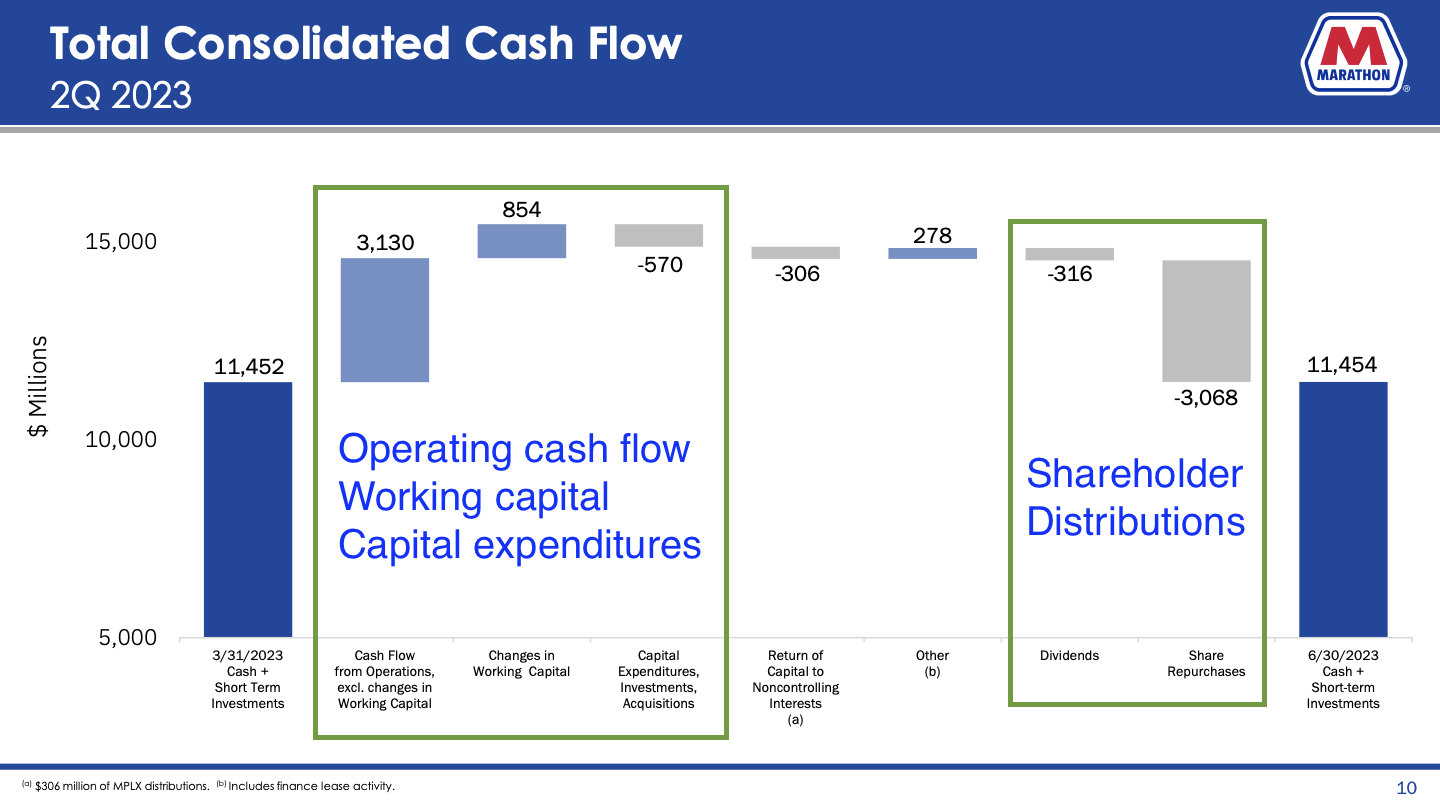

As a result of these tailwinds, MPC returned nearly $3.4 billion via share repurchases and dividends during the quarter, representing a 100% payout of operating cash flow, excluding changes in working capital.

Marathon Petroleum Corporation

{kind=link}

The company had approximately $6.3 billion remaining under its current share repurchase authorization and held roughly $11.5 billion in consolidated cash and short-term investments at the end of the second quarter.

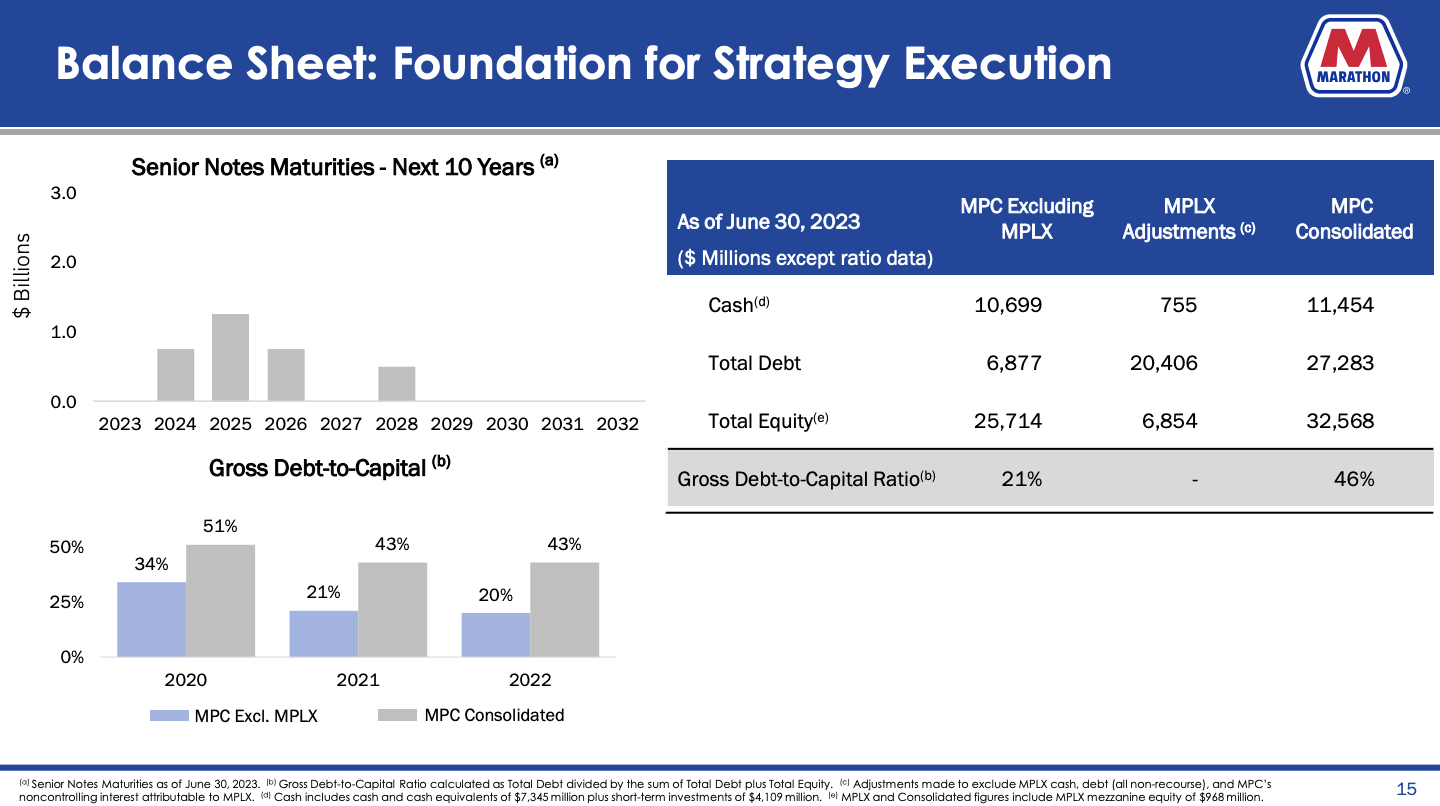

After all, one of the key reasons why the company is so aggressive when it comes to buybacks and dividends is its healthy balance sheet . Not only did the company have roughly $11.5 billion in cash ($10.7 billion excluding MPLX), but its gross debt-to-capital ratio is just 21%. Even including MPLX's $20.4 billion in debt, that number is below 50%.

It also has no maturities in 2023.

Marathon Petroleum Corporation

{kind=link}

Since May 2021, MPC has repurchased 264 million shares, accounting for approximately 40% of the shares outstanding.

The current dividend yield is 2.3%, which enjoys a payout ratio of just 9% and 10.5% average annual dividend growth over the past five years.

Like Valero, Marathon Petroleum did not cut its dividend during the pandemic but used its balance sheet to take on more debt. Luckily, the years after the pandemic allowed the company to quickly reduce debt again.

Having said all of this, the company is upbeat as it looks into the future.

The Outlook & Growth Projects

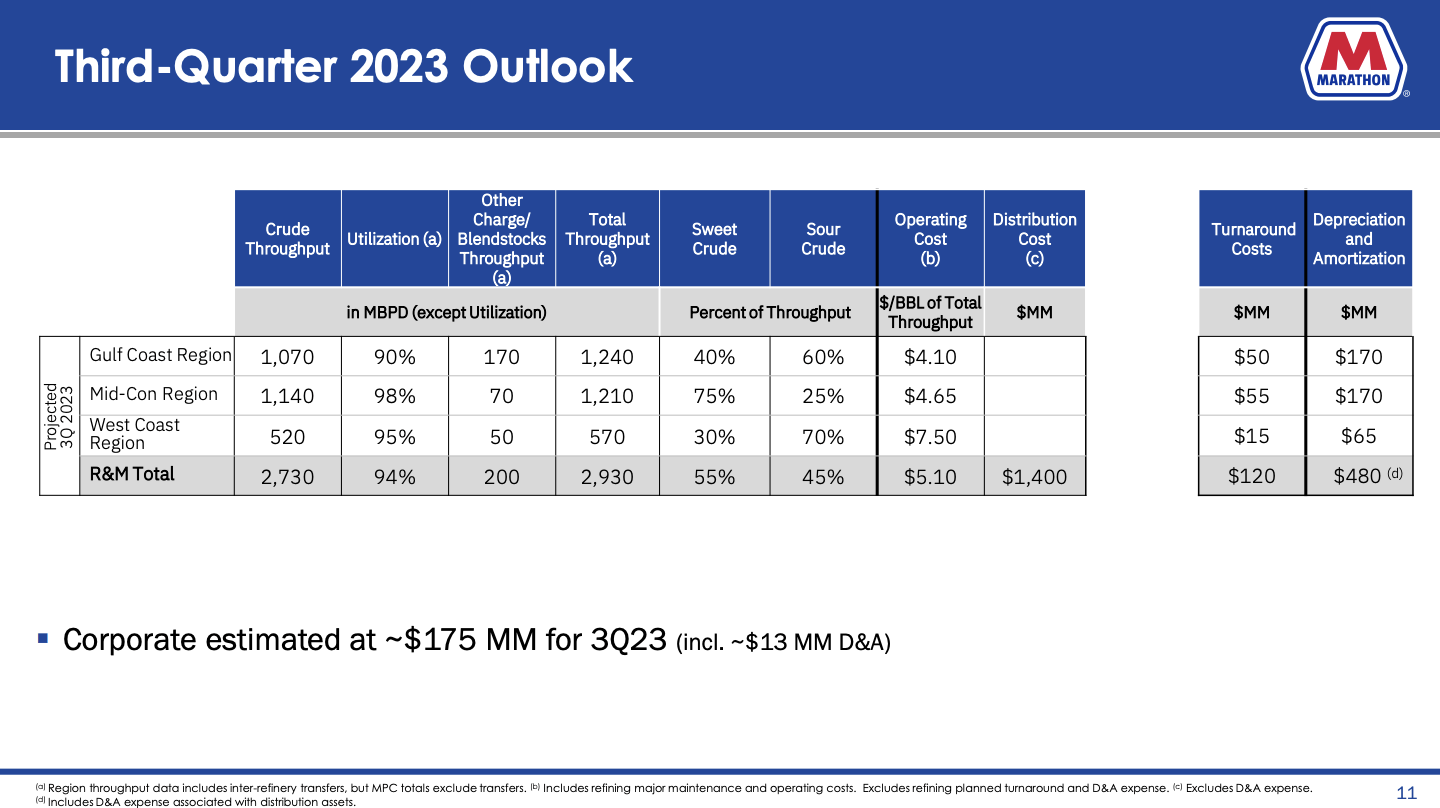

For the third quarter of 2023, MPC expects crude throughput volumes of approximately 2.7 million barrels per day, which would translate to a utilization rate of 94%.

Marathon Petroleum Corporation

{kind=link}

The utilization rate is expected to be higher sequentially due to lower planned turnaround activity in the third quarter, incentivizing high refining utilization.

The company's guidance also assumes the reformer at the Galveston Bay refinery will be down for the entire quarter.

Operating cost per barrel in the third quarter is expected to be $5.10, benefiting from higher throughput and lower costs due to completed turnaround and project activities.

Distribution costs are expected to be approximately $1.4 billion, and corporate costs are expected to be $175 million, reflecting sustained reductions.

Additionally, the company is investing in growth.

For example, MPC completed the STAR project at its Galveston Bay refinery, which enhanced the competitive position of the refinery. The project increased residual fuel and heavy crude processing capacity and improved distillate recovery.

MPC boasts two premier 600,000 barrel-per-day refineries on the US Gulf Coast with significant logistics and export capacity, supporting its global commercial strategy.

Additionally, construction activities at the Martinez renewable fuels facility are ongoing, with pretreatment capabilities set to come online in the second half of 2023.

This facility is expected to reach its full capacity of producing 730 million gallons per year by the end of 2023.

According to MPC, the Martinez facility will become one of the largest, most competitive renewable diesel facilities with a strong operating profile, logistics flexibility, and advantaged feedstock slate, supported by a strategic relationship with Finish refinery giant Neste.

Marathon Petroleum Corporation

{kind=link}

With that said, let's look into the valuation.

MPC Stock Valuation

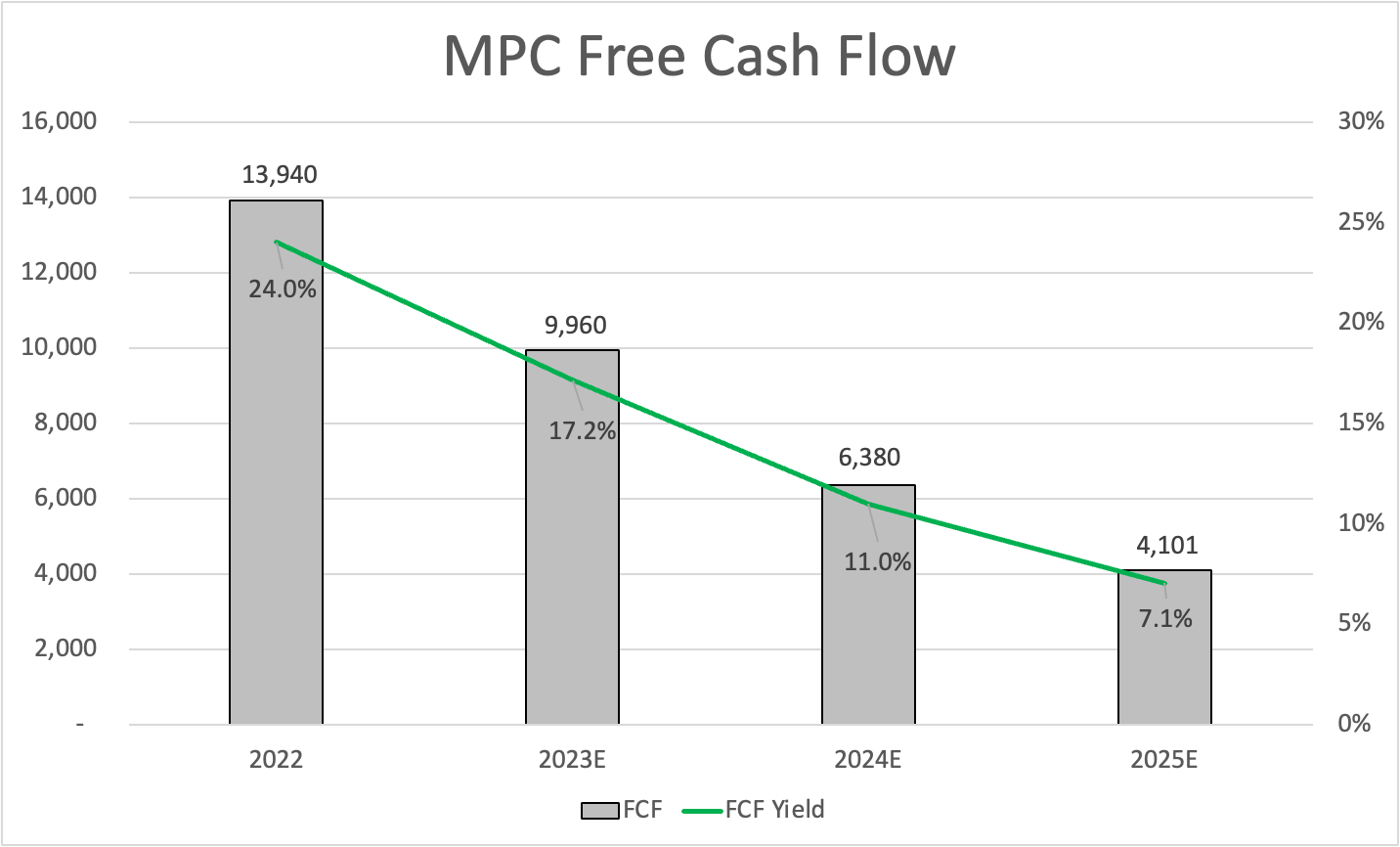

When looking at the analysts' free cash flow estimates, we see a steep downtrend. However, it's not as bad as it looks. Essentially, what we're seeing is an expected long-term normalization in margins. 2022 was truly exceptional. Unless a miracle happens, we will continue to see normalization.

However, bear in mind that in 2019, the company generated $3.3 billion in free cash flow. Even the expected result of $4.1 billion in 2025 would be far above that.

{kind=link}

Having said that, I do not believe that the decline will be this steep. Analysts continue to underestimate the earnings power of this company and its peers, which was confirmed by 2Q23 numbers.

Nonetheless, sticking to analyst numbers and using 2024 estimates, the company is trading at 9.1x 2024E free cash flow.

Not only does an 11.0% free cash flow imply a lot of room to maintain aggressive dividend growth and buybacks it also indicates a favorable valuation.

Given the health of MPC's business and ability to capture long-term growth, I would make the case that the company should not trade below 12x free cash flow.

This would indicate a fair price 32% above the current price.

The current consensus price target is $144, which is 7% above the current price.

Based on this context, I still do not urge anyone to jump into MPC. The economy is not in a good spot, and given the recent uptrend in the market and MPC, I would only buy this company after a 10-15% correction.

My rating is bullish to reflect the fact that my longer-term target is well above the current stock price.

Takeaway

In conclusion, Marathon Petroleum has shown impressive resilience and earnings power, despite economic weakness.

The company's recent quarterly earnings report revealed strong refinery demand, setting the stage for aggressive buybacks and consistent dividend growth.

With MPC's expansion into renewable fuels and its superior network of assets, the company is well-positioned for future growth. Despite a dip in sales compared to the exceptional numbers of the previous year, the company remains in a favorable spot.

Furthermore, MPC's Midstream segment, through its ownership of MPLX, continues to generate strong cash flows and offers high-return growth opportunities.

The company's healthy balance sheet allows for aggressive buybacks and dividends, making it a sound long-term investment with an attractive valuation.

Overall, I rate MPC as bullish for the long term, considering its ability to weather market fluctuations and deliver sustained growth.

However, given the prevailing economic conditions, it may be prudent to wait for a 10-15% correction before considering an entry into this promising refinery stock.

For further details see:

Marathon Petroleum Q2 Earnings: Why This Stock Is An Attractive Investment