MPC - Marathon Petroleum Should Benefit From Europe's Net-Zero Strategy

2023-03-20 04:38:56 ET

Summary

- LNG demand from Europe continues to drive revenue.

- Net-Zero strategy and global demand continue to drive LNG demand.

- Fundamentals remain cheap for now.

Investment Thesis:

Marathon Petroleum (NYSE: MPC) is set to benefit from Europe's Net-Zero strategy well into 2023, as demand continues to increase. Marathon trades relatively cheaply and has a reasonable upside considering the valuation.

Overview

Marathon Petroleum currently has 2898 MB PCD of capacity, and in 2022 it averaged 2761 in refining capacity, and this should see a slow but steady increase in 2023, as the company looks to take advantage of increased natural gas demand. The company currently has a total refining capacity, of 2.9 million barrels per day and 852,000 BOE/d capacity for LNG, and 12 billion standard cubic feet of natural gas.

{kind=link}

Capex Schedule (Investor Presentation 23')

Outlook for LNG and Oil

Global oil inventories continue to rise, but global production continues to fall to a seven-month low , which could lead to oil prices once again rising to above $100 a barrel, as the trend is likely to continue in February, as oil producers continue to remain tight. A number of oil-producing countries have been slow to cut their total production, and therefore, oil prices remain below where they should be. Furthermore, as we head into 2023, interest rates continue to rise, which has meant that the dollar remains elevated. The combination of the higher dollar has kept oil prices down for now, but questions remain about whether or not they will remain lower for longer. The increasing prices, along with increasing interest rates could see operations affected negatively.

How the Global LNG market is shaping up.

The global LNG market continues to face pressures from a number of different sources, including Russia, which has been cutting production. LNG demand continues to remain robust outside of major economies, and countries in Asia, especially Europe, continue to see an increase in demand due to climate strategy that calls for the replacement of energy sources such as coal. This could mean Marathon Petroleum continues to see strong demand for its refined products throughout the year, despite pressures that are stemming from global macro headwinds.

Europe continues to focus on a net-zero strategy , and that means transitioning from traditional forms of power such as coal and moving to other sources of energy, but doing so means overcoming structural issues, which currently natural gas is fulfilling. This has left European countries with no choice but to turn to the U.S. natural gas producers and natural gas refiners, including the likes of Marathon Petroleum, and other US-based producers will continue to see strong demand. Germany, Italy, and the Netherlands remain the biggest consumers of Russian natural gas, and all of these countries have been trying to replace Russia’s natural gas, and co-investments into increasing liquefication facilities should help increase the total capacity to 70 billion cubic feet , some of which should help Marathon Petroleum.

Oil demand continues to remain strong globally, with GDP largely positive, while there is an expectation that Chinese GDP slows down despite a reopening, overall demand for energy will likely continue to rise.

Valuation & Risks to Cash Flow

Marathon Petroleum's revenue surged in 2022, as LNG demand, and crude demand continued to rise. This increase in revenue led to a record level of cash flow and a record level of operating net income, considering there is very few headwinds to speak of that will see energy demand reduce significantly, we should see continued growth for the year. The biggest factor remains capacity and considering Marathon Petroleum continued to run at high capacity and marginal profitability will depend on capital expenditure and the company’s ability to increase refining capacity.

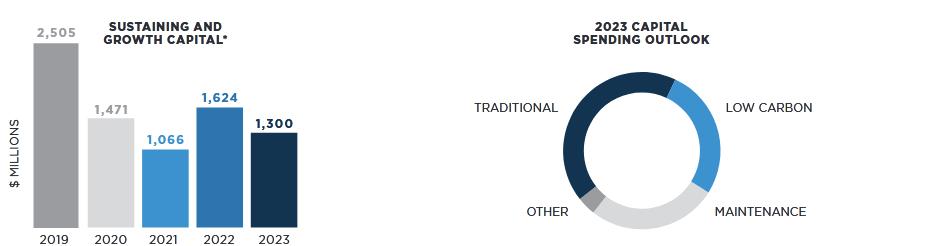

Management has projected that capital spend will fall to $1.3 billion in 2023, which should help it, improve cash flow during the year, management has made numerous attempts to reduce capital spend but continues to see strong demand for its products. Therefore, it remains to be seen how it will overcome these issues, and ensure that LNG supply remains high, especially considering that the company is already running at 95%+ capacity .

Marathon’s management would do well to increase its capital expenditure despite the fact that there are clear global headwinds going into the next few years. Management might clearly be worried that demand will start to wane especially if there is a recession, which will affect Europe’s ability to import natural gas.

Marathon currently trades at around 5x earnings, and forward earnings should fall to 4.5x, with EPS coming in around $25-27, making the stock quite cheap, despite a dividend that is still quite low. Investors have been driving MPC stock to new highs over the past year, and the technicals currently point to the market expecting a correction in the stock, with a put-to-call ratio of 2.5, this would mean there is a significant bet against Marathon Petroleum stock to correct.

Unless Marathon witnesses a significant adverse event, investors would be happy with the fact that the stock trades so cheaply, despite investor sentiment clearly on the side of being negative. Meanwhile, there is little indication that there is a significant reduction in revenue or a revaluation which would make the stock trade sideways.

According to analysts' estimates and their 12-month forecast Marathon Petroleum, currently, has a 20% upside , but in my estimate could easily increase by 50%, making the stock very attractive on a fundamental basis. This is based on an expectation that growth continues into 2023, and 2024, refined LNG, and demand continue to increase from Europe, as they continue to replace their current energy sources with LNG, both as a replacement to Russian gas and as a replacement for traditional energy.

In terms of net income, I expect net income to come in around 4-5% high, both in organic revenue growth, and due to replacement by Europe of traditional suppliers. Revenue for the fiscal year 23' should be around $15 billion, and with margins remaining steady around 8% (similar to FY22'), net income to be around $1.2 billion. At a current P/E of around 5x, a 50% increase would take the stock to around 7.5x in terms of P/E and that would not be expensive for a stock that continues to grow, and has multiple tailwinds.

All in all, Marathon Petroleum trades at a low valuation, has the necessary positives from the market, to consider a stock that has 'value', and could see some upside in the medium term, as earnings continue to come positively.

For further details see:

Marathon Petroleum Should Benefit From Europe's Net-Zero Strategy