TSN - Marfrig: Financial Discipline Expected To Yield Long-Term Benefits

2024-01-10 23:13:15 ET

Summary

- Marfrig's Q3 2023 success drove year-end share gains, fueled by strategic financial discipline and leverage reduction efforts.

- Despite U.S. cattle cycle challenges, Marfrig foresees gradual recovery and enhanced EBITDA, especially in South America.

- Initiatives like selling 16 plants to Minerva and capital increases led to a substantial rise in Marfrig's shares since October 2023.

- Marfrig's attractive forward EV/EBITDA of 7.1x positions it favorably compared to competitors, remaining 37% below industry average.

- Despite potential challenges, the positive long-term outlook for Marfrig persists, anticipating continued deleveraging and improved results.

In my previous articles on Marfrig ( MRRTY ), my investment thesis centers around the company's efforts to reduce leverage, unlocking significant value for the stock. Despite the challenges posed by the U.S. cattle cycle, I maintain a long-term perspective, anticipating a gradual recovery and stronger EBITDA for the company.

{kind=link}

In the latest reported quarter, Marfrig exceeded market consensus, with North America facing pressure on margins due to the negative cattle cycle. At the same time, South America, particularly Brazil, experienced positive results with expanding margins.

The primary concern in the investment thesis remains leverage, but selling 16 plants to domestic peer Minerva ( MRVSY ) has alleviated some of these concerns. Since October 2023, Marfrig's shares have seen a substantial increase, attributed to a capital increase, a rise in the controlling shareholder's stake, and a progressive increase in its BRF ( BRFS ) stake. While short-term appreciation potential may be limited, I view the company as highly promising for the long term, considering it is undervalued compared to global industry peers.

I affirm my optimistic stance on the company, expecting that as deleveraging continues in 2024 and results demonstrate improvement, a more significant influx of investors should align with the buy thesis.

Latest Results and Outlook for 2024

In the third quarter of 2023, reported in November of the previous year, Marfrig disclosed a net revenue of R$21.8 billion, excluding BRF's operations, indicating a year-on-year decrease of 2.5%. The EBITDA was R$1.3 billion, representing a 44.3% decline year-on-year. The EBITDA margin stood at 6.2%, primarily reflecting elevated cattle costs in North America as the main contributing factor. The reported net profit was R$150 million, resulting in a net margin of 0.7%, down 0.6 percentage points compared to the previous year's period.

Breaking down the main segments, North America experienced an increase in demand despite high costs, while South America saw the opposite trend in costs.

North America:

In the domestic market, demand for beef remained resilient, with volumes growing by 10.5% in the quarter and 6.9% in the year. This growth was driven by demand and the higher number of weeks in the quarter (14 weeks vs. 13 weeks in 3Q22). Selling prices also increased by 12.9% year-on-year, contributing to the growth in net revenue, which reached R$3.4 billion, up 14.9% quarter-on-quarter and 18.6% year-on-year. However, costs remained high, with the cost of cattle rising by 29.3% year-on-year, resulting in a tight EBITDA margin of 4.4%, signaling a quarterly drop of 0.8p.p. and a sharp annual drop of 7.4p.p.

The outlook for the fourth quarter indicates weak margins for the U.S. operation, mainly due to the negative cycle and typical seasonalities, highlighted by the winter season and the low trend in meat consumption. The expectation is that 2024 will continue to be challenging for Marfrig in the U.S., primarily due to low cattle availability, which is predicted to persist until mid-2025.

Examining estimated cattle prices in the five major cattle-producing regions in the United States, the outlook 2024 has decreased from $190 per hundredweight to $180 per hundredweight. Although this remains considerably higher than the historical average of $130 per hundredweight, which would be optimal for Marfrig, it is now more likely to envision a scenario approaching $150-$160 per hundredweight for 2025 and beyond.

USDA, Economic Research Service

{kind=link}

South America:

In this region, the scenario is opposite to that seen in North America regarding costs, guided by a more favorable cattle cycle in Brazil. This made it possible to expand the EBITDA margin, which ended the quarter at 11.6%, up 1.6 p.p. quarter-on-quarter and +2.1 p.p. year-on-year.

The cattle cycle in Uruguay is showing signs of improvement, with a significant drop in the cost of the animal by 29.4% per year. The region is benefiting from the negative cycle in North America, exporting more beef to the U.S., both from Brazil (commodity meat, processed) and Uruguay (premium cuts). Sales prices to the foreign market continue to weaken due to weaker short-term Chinese demand, impacting revenues annually, which reached R$377 million, a quarterly increase of 24.5% and an annual drop of 1.6%.

Looking ahead to the fourth quarter, the trend is for slightly stronger margins driven by the favorable cattle cycle and the high availability of animals in the slaughter phase. Positive seasonality is expected compared to the holiday season. The 2024 outlook for Marfrig in South America is optimistic, as the year should be marked by greater availability of cattle, enabling good margins that are expected to continue until 2025. The biggest challenge to face, however, is weaker Chinese demand in the short term, although, in the medium to long time, it should become more optimistic and contribute to a higher average selling price than in 2022 and 2023.

Deleveraging and Focus on the Processed Portfolio

The sale of 16 plants in South America to Minerva, completed in August last year, represents a significant step in Marfrig's deleveraging strategy, although debt remains a point of caution. The deal amounted to R$7.5 billion, with R$1.5 billion paid as a down payment in August and the remaining R$6 billion scheduled for payment at closing, supported by Minerva's financing commitment from a bank. Marfrig utilized the funds from the initial payment to increase its stake in BRF from 33.27% to 50.06%.

Despite the reduction, Marfrig's leverage closed the last quarter at 3.9x LTM Net Debt/EBITDA. Adjusting for the pending amount from the South American asset sale, leverage drops to 3.2x. With the expectation of improved cattle trends in South America, it is reasonable to anticipate Marfrig reaching a Net Debt/EBITDA level close to 3.0x by the end of 2024. Although healthier than the previous 4.0x, the level remains relatively high.

The conclusion of the sale to Minerva in the first half of 2024 will position Marfrig to concentrate more on processed product production, retaining the regional industrial units and factoring in BRF's share in the consolidated result. This strategic shift underscores Marfrig's commitment to focusing on the processed products portfolio and achieving financial deleveraging.

Marfrig's Controller Aumanta Posicao na empresa

One significant bullish aspect of my Marfrig investment thesis is its shareholding structure. In October of the previous year, the company's controller, MMS Participacoes, controlled by the Molina family who founded Marfrig, infused R$1.6 billion in capital, increasing its stake from 54% to 60%.

Marfrig conducted a private capital increase in July of the same year to avoid decapitalization after the BRF follow-on. Controlling shareholders committed to subscribing 240 million Marfrig shares (MFRG3) on the Brazilian stock exchange, raising R$2.1 billion by issuing 300 million new shares. Controlling shareholders took 77% of these new shares, amounting to 232 million.

Chairman of the board and controlling shareholder Marcos Molina expressed Marfrig's comfort with its current stake in BRF, holding 47% until November of the previous year. While not ruling out future share purchases, Molina, considering BRF's shares attractive, increased Marfrig's shareholding in BRF in December, surpassing a 50% stake in total voting capital.

The move by a controlling shareholder, especially a founder, to increase their stake typically signals confidence in the business outlook and alignment of interests with other shareholders. It may indicate the perception of an opportunity to buy at attractive prices, strengthen control over strategic decisions, and convey optimism about the company's future.

These actions have driven Marfrig's shares on the Brazilian stock exchange to surge up to 60% in the subsequent months, a trend also reflected in the company's ADR since mid-October.

The Bottom Line

Marfrig reported positive numbers in the third quarter of 2023, contributing to a year-end share appreciation of 60%, which naturally reduces the attractiveness for the short term.

The increase in the controlling shareholder's stake, coupled with Marfrig's strategic financial discipline, including capital increases, the decision not to distribute dividends, and selling South American plants to Minerva for deleveraging, underscore the company's focused approach amid the BRF acquisition.

Anticipating a gradual improvement in South American results and with these initiatives, I believe Marfrig could achieve a net debt/EBITDA of 3x by the end of 2024, a favorable prospect that might attract more buyers to the stock.

Currently trading at a forward EV/EBITDA of 7.1x, compared to 8.15x for JBS ( JBSAY ), its main U.S.-focused competitor, Marfrig, appears poised to be more attractive, still 37% below the industry average, considering U.S. peers like Tyson Foods ( TSN ).

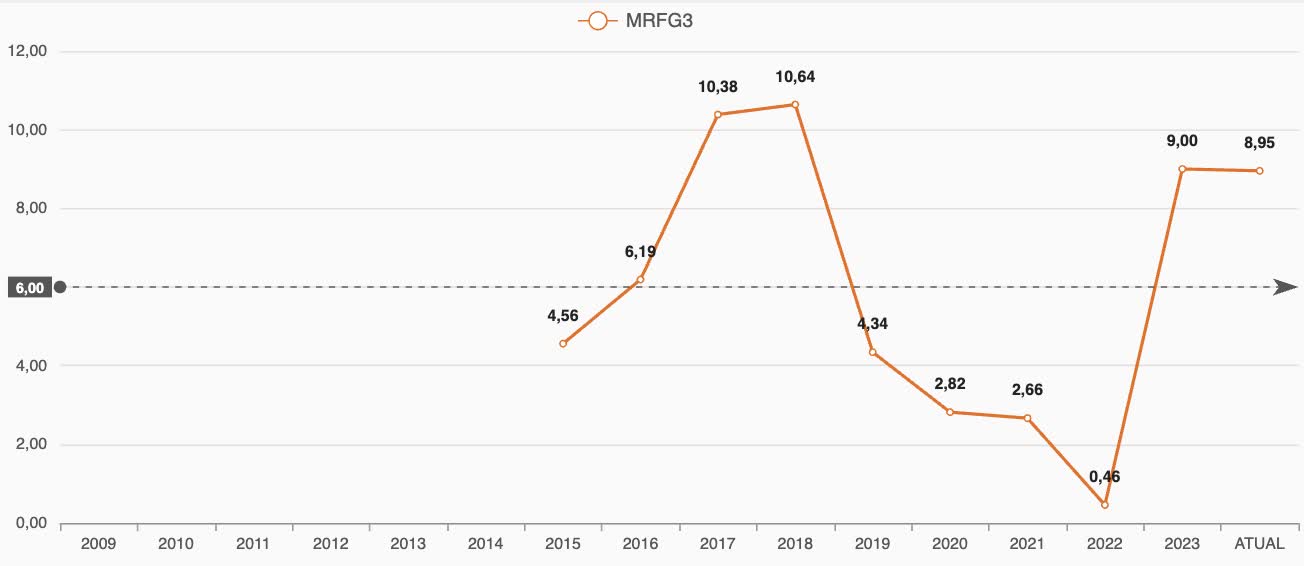

Considering Marfrig's valuation between 2017 and 2018, when the company reached a peak with an EV/EBITDA exceeding 10x amid a robust US cattle cycle, I believe there is potential for the company to achieve or even surpass the same multiple by 2025, potentially reaching an enterprise value above $15 billion. This optimism is driven by the anticipated improvement in the US cattle cycle and its financial discipline, resulting in deleveraging.

Marfrig's historical EV/EBITDA on Ibovespa (Status Invest)

{kind=link}

However, the primary risk to the thesis continues to be associated with the fluctuation of cattle prices, especially in the U.S., which directly impacts Marfrig's costs and puts pressure on the EBITDA margin (currently at 3.3% compared to 16.6% in 2021), as well as on the execution of the company's financial discipline. These are risks that will need to be monitored in Q4, as it is expected to be a quarter where improvements in margins, mainly from operations in South America, may be reported.

While acknowledging that leverage levels may remain high and the Brazilian interest rate (Selic) may hover around 9% in 2024, coupled with persistent challenges in the U.S. market, I maintain a positive outlook on Marfrig as a long-term investment. However, considering the recent surge in share prices from late 2023 to early 2024, the short-term attractiveness may be less pronounced.

For further details see:

Marfrig: Financial Discipline Expected To Yield Long-Term Benefits