MRRTY - Marfrig Global Foods Could Recover But Some Headwinds Are Still Ahead

Summary

- Marfrig Global Foods has been overly penalized by market reactions to inflation and the aftermath of the war in Ukraine.

- Perhaps the market is underestimating this company, which instead is performing well despite tough macroeconomic conditions.

- Profit margins fell in North America, but this should only be temporary.

- However, it would be wise not to go beyond a Hold rating as the outlook for the share price remains uncertain due to the potential looming recession.

Marfrig Global Foods S.A. in the Packaged Foods Industry

Marfrig Global Foods S.A. (MRRTY), based in São Paulo, Brazil, is a global producer of beef patties and beef, claiming to be one of the largest in the world.

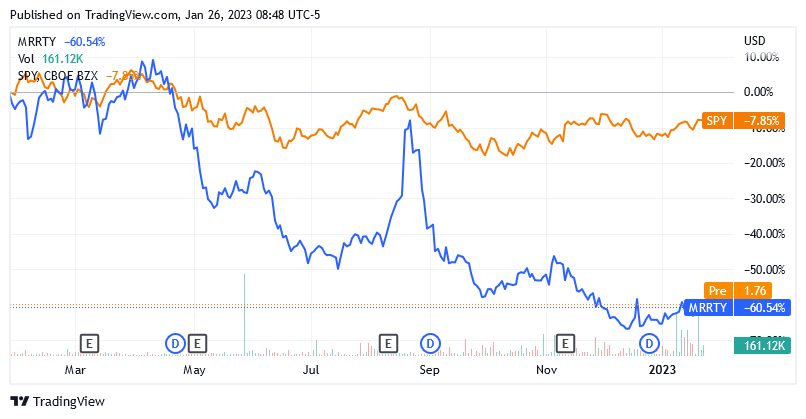

The share price of Marfrig Global Foods collapsed last year with a loss of more than 60% and showed, among other things, quite some volatility compared to the US stock market as a whole.

{kind=link}

But it looks like headwinds from increased inflation in 2022 and the aftermath of the war in Ukraine have put this stock at an unfair disadvantage, as the company is performing well despite some signs of a slight slowdown in North American profit margins.

However, instead of a Buy recommendation, which the stock might deserve from my point of view, investors should probably stick with a Hold recommendation for the time being, due to possible further headwinds on the market.

As the recession and inflation could still squeeze the company's profit margins a little bit, this could push the stock a little further below its current levels. Marfrig Global Foods' 14-day Relative Strength Index of 55.18 suggests there is still a possibility for lower stock prices as the stock is far from oversold despite falling sharply over the past year.

Relevant Figures on the Composition of the Activities of Marfrig Global Foods S.A

Marfrig Global Foods S.A. sells its beef products in mainland Brazil, as well as in Argentina and Uruguay, North America, and some other regions around the world.

Marfrig Global Foods S.A. finances the continuation and expansion of its economic activities, broken down by geographic area, as follows. Marfrig Global Foods S.A. has a business unit in North America, another business unit in South America, and a third business unit recently added to the portfolio called BRF S.A.

BRF S.A., one of the world's largest food companies and operating for more than 85 years, has been part of Marfrig since the second quarter of 2022, when Marfrig officially became the largest shareholder of BRF S.A. on April 1, 2022.

As measured by Q3 2022 US dollar sales, the North American business segment accounts for 41% of total consolidated sales, while the South American business segment accounts for 20% and BRF the remaining 39%.

By currency, the US dollar accounted for approximately 72% of total consolidated sales, the Brazilian real [BRL] for 25%, while other currencies accounted for the remaining 3% of total consolidated sales.

The North American business segment consists of 88% domestic market and 12% export, the South American business segment consists of 35% domestic market and 65% export, while BRF consists of 53% domestic market and 47% export.

As measured by Q3 2022 BRL adjusted EBITDA, the North American business segment accounts for 46% of total consolidated BRL adjusted EBITDA, while the South American business segment accounts for 18% and BRF S.A. the remaining 36%.

How Marfrig Global Foods S.A. Is Performing

In the third quarter of 2022, Marfrig delivered net revenue of BRL 36.4 billion (or about $6.75 billion), Adjusted EBITDA of BRL 3.8 billion (or about $705 million) which both determined an Adjusted EBITDA margin of 10.4%, while the net income was BRL 431 million (or about $82.2 million).

Net sales for Q3 2022 increased 5.6% sequentially, were up 63% compared to Q1 2022 and 54.1% year-on-year.

Adjusted EBITDA for Q3 2022 decreased 4.8% sequentially, increased 38% compared to Q1 2022 but decreased 19.9% year-on-year.

Adjusted EBITDA margin for Q3 2022 decreased 114 basis points sequentially, decreased 192 basis points compared to Q1 2022 and decreased 962 basis points year-on-year.

The net income for Q3 2022 decreased 89.9% sequentially, increased by 295.4% compared to Q1 2022 but decreased 74.3% year-on-year.

Regarding the beef segment, the company had excellent performances in the South American business in the third quarter of 2022 as this segment delivered record net sales of more than BRL 7.4 billion (about $1.4 billion) and a record Adjusted EBITDA of BRL 710 million (about $131.7 million).

While the adjusted EBITDA margin of 9.5% was flat sequentially but improved by 310 basis points compared to the first quarter of 2022.

The South American branch also performed exceptionally well in the second quarter of 2022 , posting its highest-ever sales of BRL 7.1 billion (about $1.4 billion), while exports set a record at 70% of total quarterly sales.

Recurring investments to expand and maintain beef operations totaled BRL 498 million in Q3 2022, of which 55% was spent on growth projects, most notably the beef patty line capacity expansion projects in Brazil, Argentina and Uruguay.

A Strong Financial Position and a High Level of Creditworthiness Are Essential to Support the Company's Goal of Creating Shareholder Value

Marfrig Global Foods S.A. intends to continue to allocate financial resources to expansion projects in beef operations, provided that a highly disciplined attitude is maintained in resource allocation.

The company likely does not want to lose sight of the creditworthiness obtained from the rating agencies. This aspect will be fundamental in determining the terms on which Marfrig can access debt, the purpose of which is not limited to funding ongoing operations and expansion projects, but also maintaining an easy repayment schedule over time.

Following recent updates to its credit rating from S&P and Fitch, Marfrig says it now just needs to add one more notch to reach an investment grade. An investment grade rating indicates that there is a low risk that the company will not be able to repay the capital it has raised and meet all other financial obligations. For rating agencies, it appears Marfrig is currently demonstrating the ability to meet its debt payment obligations in international markets, although it could still be a little vulnerable if economic conditions change sharply. Marfrig is highly capable of repaying loans in the domestic market in my view.

Credit agencies typically use the ratio of net debt to adjusted EBITDA [TTM], among other metrics and aspects, to determine a company's probability of default on its debt obligations. This leverage ratio helps determine how many years it will take the company to pay off all outstanding debt through EBITDA. As of September 30, 2022, Marfrig Global Foods S.A.'s ratio of TTM Net Debt to Adjusted EBITDA was 2.38 times in BRL terms or 2.32 times in US dollar terms.

Typically, this financial leverage metric does not trigger red flags as long as it stays below the value of 3. In addition, for a correct interpretation of the Marfrig leverage ratio, the inclusion of the liabilities of BRF in the Marfrig balance sheet after Marfrig became a major shareholder of BRF must also be taken into account. This explains why the LTM ratio increased 1.25x - 1.28x year-on-year in Q3 2022.

The leverage ratio is expected to decrease over time as the North American business regains some of the profitability lost last year, supported by an expected improvement in macroeconomic conditions in the second half of 2023. While the other segments should continue to perform well as the trends in the third quarter of 2022 suggest.

As of September 30, 2022, the balance sheet stood on solid pillars, as the following key figures show. Net debt position was about $8.02 billion , but the trailing 12-month [TTM] interest coverage ratio of 2.72x suggests the company has no trouble paying interest costs on the outstanding debt. Investors typically welcome an interest coverage ratio of 1.5x or higher.

The TTM Interest Coverage Ratio as of Q3 2022 is calculated as a TTM operating income of $1.79 billion divided by the TTM interest expense of $657 million .

In addition, the relationship between Marfrig Global Foods' weighted average cost of capital of 6.15% and Marfrig Global Foods' return on capital employed of 19.41% contributes to the company's sound financial condition. Marfrig generates returns that go beyond the cost of the capital raised to fund the investment, thereby creating value.

What to Expect in the Coming Quarters

Exports, which represent at least 35% of the total consolidated beef sales volume of Marfrig Global Foods S.A., are likely to have been impacted by the appreciation of the US dollar against other international currencies, particularly in the third quarter of 2022.

So this kind of pressure should ease as the US dollar loses some of its accumulated purchasing power, and in that regard, A US trade deficit, which analysts are forecasting to narrow further, could suggest just this kind of desired move in the US dollar. Analysts see the US trade deficit fall from $78.2 billion in October.

In addition to expectations for a less strong US dollar, exports should benefit from policies in many European countries, notably The Netherlands, to reduce cattle breeding areas to reduce CO2 emissions into the atmosphere.

Strong demand is also expected from Asian countries, particularly from the People's Republic of China due to the full reopening of activities such as hotels, restaurants and catering as the government abandoned the zero-tolerance policy towards the COVID-19 virus. Due to this policy of strict lockdown and restrictions, Chinese demand and production came to a standstill for a while.

The decline in sales volume in the North American domestic market to 437,000 tons of beef in the third quarter of 2022, a decrease of 1% from the first quarter of 2022 and a decrease of 3.3% from the second quarter of 2022, undoubtedly weighed on earnings and profit margins amid higher costs and expenses through the first 3 quarters of 2022.

The North American domestic market accounts for 32% of the total consolidated domestic sales volume or approximately 21% of the total consolidated sales volume (domestic markets and exports).

The significant inflation was most likely responsible for lower sales volumes in the North American domestic market. However, the negative trend is also impacted by an unusual increase in beef demand in 2021 as key food service networks and retailers had to replenish stocks in anticipation of restaurants reopening and fears of supply chain issues.

In addition, more expensive livestock supplies impacted profit margins in North America. While North American livestock declined, demand for beef from the packaged food industry remained quite strong, putting strong upward pressure on beef purchase prices. In the packaged food industry, capacity utilization was still too high despite the stabilization in consumption.

However, the company's North American segment should rebound over the next months as adverse factors fade and consist of a slowing down in inflation due to monetary tightening and the adjustment of utilization rates in the packaged food industry to consumption levels.

The South American segment benefits from stable livestock costs in Brazil, better export price conditions and a positive development of sales volumes in the domestic markets.

Brazil is a very important consumer market for Marfrig Global Foods S.A. as at least 25% of the company's total revenues in Q3 2022 depended on Brazilian demand, up sharply from 7% in Q3 2021.

Argentina's consumer market should benefit from analysts' expectations of rising consumer spending , supported by continued improvements in sales activity in food halls and restaurants and an expected rise in consumer confidence despite inflation.

For the Latin American segment, the Uruguayan consumer market should also be supported by an expected recovery in consumer spending .

The Stock Valuation

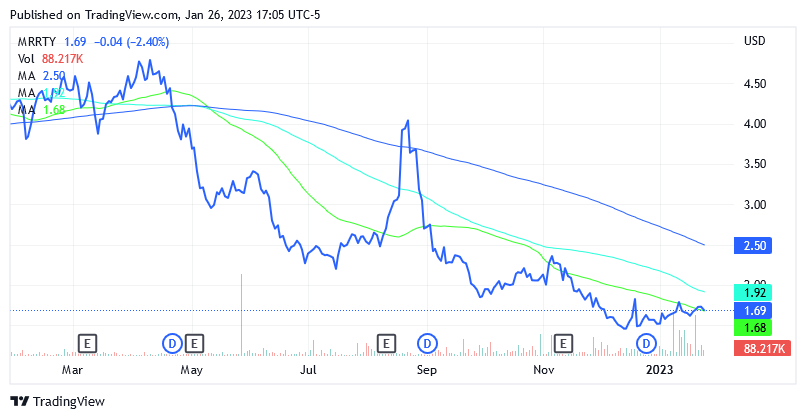

As of this writing, the shares are trading at $1.69 a share, giving it a market cap of $1.09 billion. The stock price plummeted over the past 12 months and is now below the long-term trend of the 200-day and 100-day simple moving average lines.

{kind=link}

The stock trades along the 50-day simple moving average line and is only slightly above the lower bound of the 52-week range of $1.36 to $4.72.

Price/Sales [FWD] is 0.05 versus the sector median of 1.13, while the EV/EBITDA [FWD] is 6.22 versus the sector median of 11.58.

Undoubtedly, the stock is very low and likely cheap given the prospects for an improvement in the business. However, the next headwinds from recession and inflation, which have not yet been completely overcome, could lead to slightly lower profit margins, which could put the share price under downward pressure again for the time being.

So, the stock has a Hold rating for now.

The stock pays a semi-annual dividend of $0.17 per common share, yielding a forward dividend yield of 18.15% as of this writing. The company has resumed the payment of dividends for about a year .

Conclusion

This stock has suffered tremendously from market reactions to inflation and the aftermath of the war in Ukraine. The market may be underestimating this company, which instead appears to be doing well despite difficult macroeconomic conditions worldwide.

However, with headwinds from the recession potentially delaying the share price recovery, it would be prudent not to go beyond a Hold rating for now, at least until central banks provide more insight into the looming recession.

For further details see:

Marfrig Global Foods Could Recover, But Some Headwinds Are Still Ahead