MRRTY - Marfrig: Q2 Weakness Offset By Easing Leverage Concerns

2023-09-06 00:29:11 ET

Summary

- Marfrig reported weak Q2 results influenced by regional dynamics, with challenges in North America and positive trends in South America.

- Despite the challenges, Marfrig has strengthened its financial position, including a strategic agreement with Minerva to reduce leverage.

- The resurgence in Chinese beef demand and Marfrig's attractive valuation position the company more favorably for the second half of the year, supporting a cautiously bullish outlook.

Marfrig ( MRRTY ) reported weak second-quarter results characterized by various regional dynamics.

The situation is challenging in North America due to an unfavorable cattle cycle, leading to higher costs and tight margins. Conversely, South America is experiencing a more positive trend with Brazil's favorable cattle cycle and early signs of improvement in Uruguay. Meanwhile, BRF ( BRFS ) (partially owned by Marfrig) showed a slight margin recovery but delivered sluggish results.

Nevertheless, despite these less impressive results, Marfrig has undertaken substantial measures to bolster its financial position. The company reached an agreement with its Brazilian peer, Minerva, to generate $7.5 billion in proceeds by selling 16 plants. This strategic move is poised to reduce the company's leverage to more manageable levels significantly. Furthermore, the resurgence of Chinese demand for beef is expected to enhance future financial performance further.

In my previous article on the company, I maintained a cautiously bullish stance for the long term. I anticipated that reducing its leverage could unlock significant value for Marfrig, especially compared to some of its peers trading at less attractive multiples.

I believe that investors who choose to go long on Marfrig shares at their current levels, even amid the headwinds posed by the U.S. cattle cycle, stand to reap substantial rewards in the long term as the company regains its footing and delivers a more robust EBITDA.

Therefore, despite the weakness in the Q2 results, I hold the same position as Marfrig, which retains considerable long-term upside potential.

Marfrig's Q2 Results

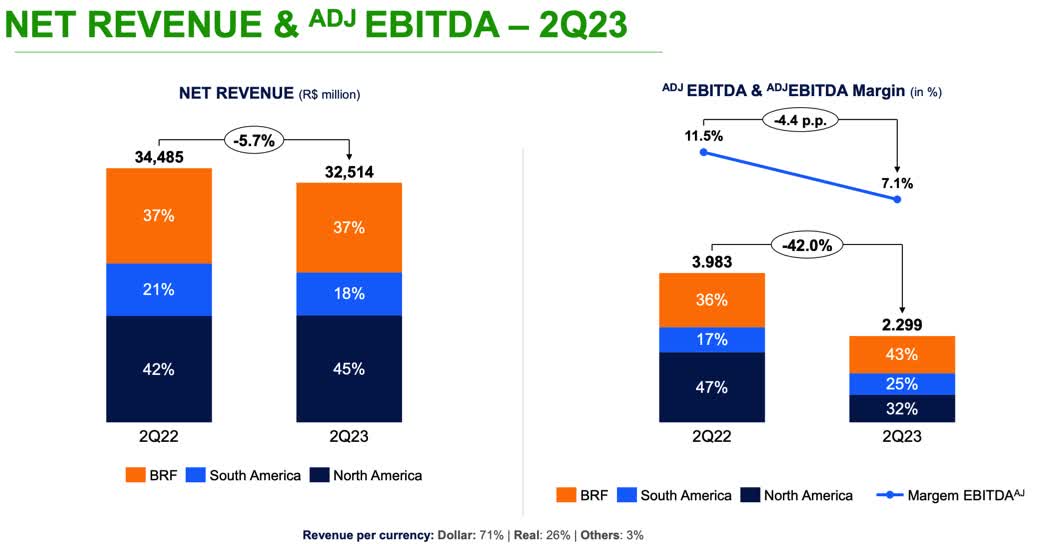

The consolidated results for Marfrig in Q2 were less than impressive. Revenues amounted to R$20.3 billion, marking a 5.7% year-over-year (YoY) decline, while EBITDA dropped significantly by 48.8% YoY to R$1.6 billion. Consequently, the company achieved an EBITDA margin of 6.4%, representing a decrease of 5.3 percentage points compared to the previous year. The net margin was 2.7%, an increase of 0.5 percentage points YoY.

{kind=link}

-

North America operation

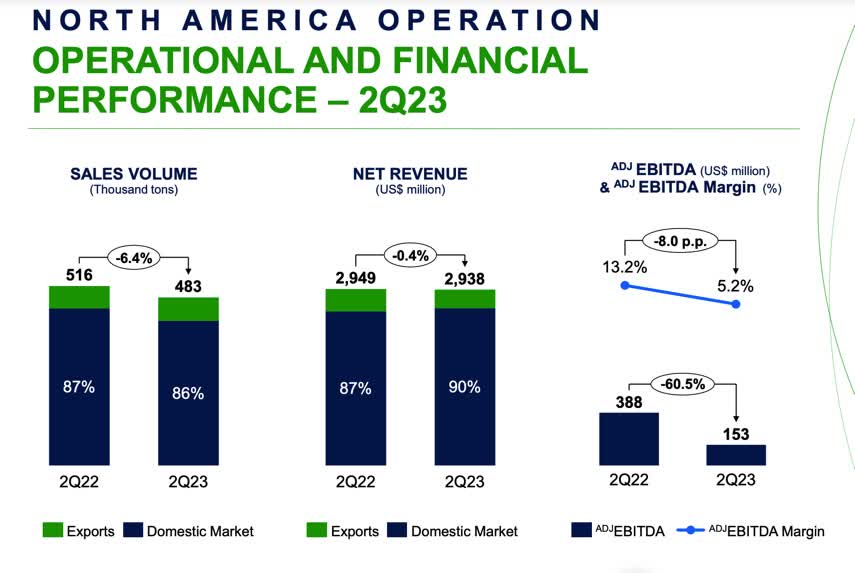

Demand has shown resilience, helping to prevent a further decline in revenue. However, inflationary pressures in the US still challenge increasing beef consumption. In North American operations, the business division's net revenue increased by 0.6% year-over-year (YoY), reaching R$14.6 billion. Furthermore, the cutout price has risen, and there has been an increase in demand from foreign markets, particularly from countries that were weak points in the previous quarter, such as Japan and South Korea.

{kind=link}

As a result of these factors, we observed reasonable volumes (a 3.8% increase quarter-over-quarter and a 6.4% decrease YoY), contributing to a sequential improvement in revenue (an 8.5% increase quarter-over-quarter). However, on the cost side, the cattle cycle in the region remains highly unfavorable, with a limited supply of cattle and consequently elevated costs that exert pressure on operational margins. Therefore, there was only a marginal sequential improvement in the EBITDA margin compared to Q1 2023 (a 1.3 percentage point increase quarter-over-quarter) and a slightly sharper decline year-over-year (an 8.0 percentage point decrease YoY).

Looking ahead to the next few quarters, Q3 2023 is expected to be more robust than Q2 2023, while Q4 2023 will shrink again, following the usual seasonality patterns. In 2024, the livestock cycle is anticipated to remain negative in the region, potentially leading to an additional 50 basis points YoY compression in Marfrig's EBITDA margin.

-

South America operation

In this region, the situation has been quite the opposite. In Q2, there was a gradual improvement in the segment's EBITDA margin, expanding by +300 basis points quarter-over-quarter and +270 basis points year-over-year. Revenues, on the other hand, declined by -18.6% year-over-year to R$5.8 billion.

Brazilian operations turned out to be the most noteworthy positive highlight. This trend is expected to continue in the second half of this year, thanks to the favorable cycle and the recovering demand from China. Operations in Uruguay also demonstrated improvement, driven by Chinese and European demand, with the cattle cycle approaching a reversal.

These figures lead us to anticipate that South America's second half of this year will be stronger than the first in revenue and margin. However, it's worth noting that although we anticipate an increase in the average selling price of beef in the second half of the year, it is expected to remain below the levels observed in 2022.

Fewer Concerns About Leverage

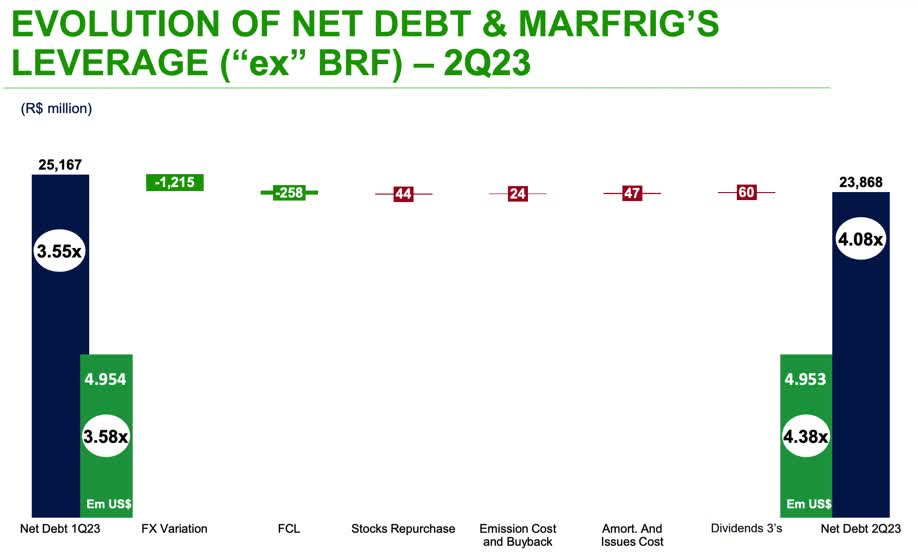

The challenging situation in North America resulted in significantly weaker EBITDA, causing Marfrig's leverage to reach 4.1x net debt/EBITDA by the end of the second quarter, a relatively high level. When factoring in the impact of BRF's results, the leverage decreases to 3.5x, still above the historical average for the meatpacking sector.

{kind=link}

However, recent news involving Minerva, one of the significant competitors in Brazil, brings some relief at a time when liquidity and leverage have become concerns for Marfrig. Minerva announced the purchase of 16 Marfrig plants for R$7.5 billion ($1.5 billion), a move that will make Minerva the second-largest player in beef slaughter in Brazil, trailing only JBS ( JBSAY ).

Following this deal, Marfrig's leverage is expected to decrease from 4.1 times to 3.1 times, which appears timely considering the rapid deterioration in profitability expectations for US beef due to the slowdown in the region's cattle cycle.

It's also important to note that in Q2 2023, Marfrig ended the quarter with a free cash flow burn of R$374 million. Excluding the effect of BRF's operations, it would have increased by R$258 million. Despite the cash consumption, BRF is no longer a margin detractor for Marfrig. BRF's EBITDA margin within the results was 8.2% in Q2 2023, relatively higher than Marfrig's margin of 6.4% in the ex-BRF consolidated figures. This can be attributed more to operational challenges in Marfrig's North America segment than to a significant improvement in BRF's performance.

With the agreement with Minerva, Marfrig now has the opportunity for immediate deleveraging. This will lead to a better risk perception of the company's balance sheet, reduce the cost of equity, and increase the potential for converting EBITDA into Free Cash Flow to Equity for shareholders.

China's demand should improve

A resurgence in Chinese demand for beef will likely contribute to improved results for Marfrig. Although Chinese demand for beef fell short of expectations from March onward, a gradual improvement should be seen in the coming quarters. This expectation is based on the appreciation of the CNY against the USD and the implementation of new government stimulus packages to boost the Chinese economy, which should, in turn, drive up demand for beef.

Furthermore, the average export price to China is approaching normal levels, which will likely result in higher prices in the year's second half compared to the first. This is particularly relevant because China remains the primary growth driver for Marfrig's exports despite its efforts to diversify its export destinations.

Additionally, the second half of the year is expected to benefit from seasonal factors related to cultural events in China, which typically lead to increased consumption and stockpiling around Chinese New Year.

Other risks to keep an eye on

Exchange Rate: Due to Brazil's bleak economic outlook, the exchange rate has gained increased relevance for companies' financial results, given that exports have become one of the most profitable avenues. For some companies, notably JBS and Marfrig, which have expanded their industrial presence into North America, the USD has become even more significant. This is especially pertinent as Brazilian-listed companies generate a substantial portion of their revenue in dollars.

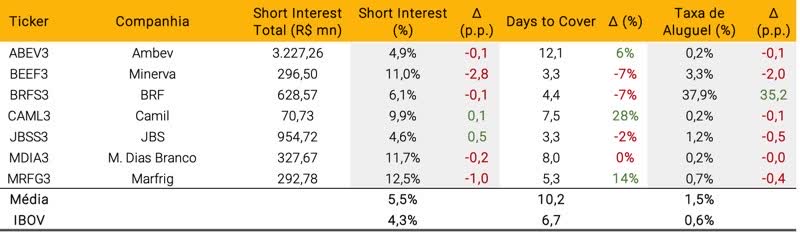

Short Interest: According to a report by XP, Marfrig's shares traded on the Brazilian stock exchange have the highest short interest compared to their industry peers. Approximately 12.5% of the float is shorted, with a 5.3-day coverage ratio. While this selling pressure may continue to weigh on the company's shares and potentially result in underperformance this year, the improved risk perception stemming from reduced leverage may also introduce volatility to the stock, prompting short sellers to cover their positions.

Short Interest in Food Companies Listed on IBOVESPA (XP Inc)

{kind=link}

Environmental Pressure: I see ESG (Environmental, Social, and Governance) factors as a potential discounting element for Marfrig due to their growing significance among investors, although it remains a sensitive issue for meatpackers. However, the Environmental aspect requires investor support to validate the companies' ambitious commitments.

The bottom line

Marfrig faces significant challenges in the short term, including headwinds from the negative cattle cycle in North America, operational difficulties at BRF, and its high level of leverage. Although selling plants to Minerva has provided some relief, the company's leverage remains elevated.

However, when considering the multiples the company has been trading, I maintain a bullish outlook for Marfrig in the second half of the year. Evaluating Marfrig and its peers JBS and Tyson Foods ( TSN ) through the lens of free cash flow yield, which stands at 122%, indicates that the company is generating a substantial amount of cash relative to its market value.

In other words, for every dollar of market capitalization (the company's total market value based on its stock price), it generates $1.22 in free cash flow.

Consequently, despite the weakness in Q2, the signs of a recovery in Chinese demand for beef and the agreement with Minerva have prevented me from downgrading Marfrig to a "hold" position. Therefore, I hold a cautiously bullish stance on its long-term prospects.

For further details see:

Marfrig: Q2 Weakness Offset By Easing Leverage Concerns