MRRTY - Marfrig Stock: A Cautiously Bullish Outlook For The Long-Term

2023-07-03 14:56:15 ET

Summary

- Marfrig, one of the world's largest beef companies, has seen its shares drop by 70% since April 2022 due to fluctuating cattle prices, rising inflation, and interest rates.

- The company plans to reduce its significant debt through a capital injection from Saudi Arabian company SALIC, which could improve its risk profile and financial stability.

- Despite potential short-term downward pressure on the stock, Marfrig's high free cash flow yield compared to its peers may indicate an undervaluation of the stock.

Marfrig Global Foods S.A. ( MRRTY ) is one of the largest beef companies in the world by capacity and is a world leader in the production of hamburgers. Marfrig divides its activities into production, processing, industrialization, and commercialization.

The company focuses on producing high-value-added animal protein-based foods. It also maintains a portfolio of other protein options, such as beef, fish, and plant-based protein. Marfrig serves wholesalers and restaurants and operates in over 100 countries. However, its beef operations in North America are responsible for more than half of its revenue.

BRF S.A. ('BRF'), also one of the world's largest food companies, has been part of Marfrig since the second quarter of 2022 when Marfrig officially became the largest shareholder of BRF. Since then, Marfrig's stake in BRF has risen from 24.23% to 33.25%, and Marcos Antonio Molina dos Santos, chairman of Marfrig, was also elected as the chairman of BRF.

At least, Marfrig has suffered from a strong bear market in the last year. Shares have plummeted about 70% since April 2022 as the company's results have been heavily hurt by fluctuating cattle head prices, rising inflation, and interest rates, leaving the company with significant debt.

Although there are reasonable indications that Marfrig's leverage, excluding BRF, will remain stable and that the company should reduce consolidated leverage, this could improve its risk profile. Thus, my investment thesis in Marfrig is cautiously bullish as I am willing to invest in a minimal portfolio position in the asset.

Latest Financial Results

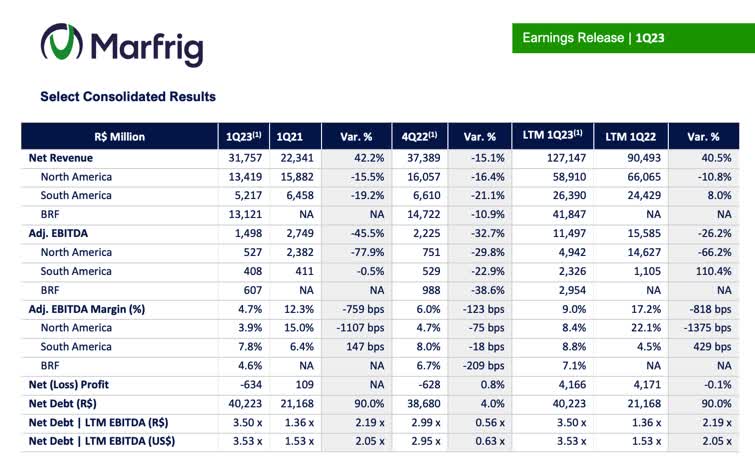

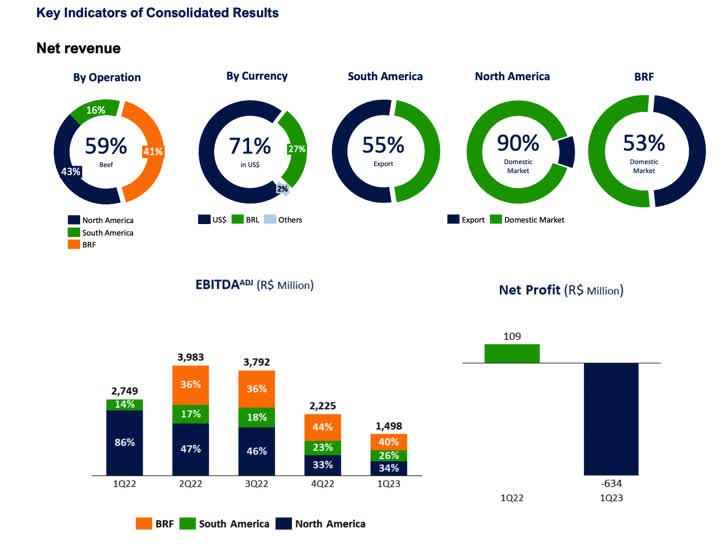

Marfrig's latest earnings results were at least short of impressive. The company reported consolidated net revenue of R$31.8 billion, meaning a 42% year-on-year increase and a 15% quarter-on-quarter drop due to BRF's results. However, when analyzing purely Marfrig's North American and South American businesses, there was a decline in revenues of 15.5% and 19.2%, respectively.

{kind=link}

The company's operating cash flow came in positive figures totaling R$673 million. The North American operations accounted for 43% of consolidated revenues, while South America represented 16% and BRF 41%.

Considering this significant diversification of Marfrig's revenues, the dollar played an essential role in the company's results, accounting for 71% of the consolidated revenues in the first quarter of 2023.

Marfrig's Adjusted EBITDA totaled R$1.451 billion, indicating a 47% year-over-year drop, 2% below the specialists' consensus. Consolidated leverage was 3.5x, both measured in BRL and USD. At the end of Q1 2023, the net debt, without considering the effects of BRF consolidation, totaled $4.9 billion, mainly explained by the seasonal cash flow effect. Leverage of this magnitude indicates that the food company may have a moderate financial risk, as it has a significant debt burden to manage.

{kind=link}

In summary, excluding the consolidation of BRF, Marfrig reported a weak first quarter of 2023 with margin pressure in North America due to higher cattle costs and lower beef prices. In South America, Brazil's export ban to China negatively impacted volumes and average prices sequentially, leading to lower revenues and margins.

Better Ahead Days for Marfrig

Marfrig is seeking a capital infusion considering the company's high leverage. This fact has been harming the company's competitive capacity and the focus of its operations. Therefore, the company's management announced a capital injection to reduce the net leverage by up to a quarter.

This plan involves bringing a significant shareholder to its base , SALIC , a Saudi Arabian company that invests in livestock. However, This support has a symbolic bias as the Saudi market is one of the most important revenue generators for BRF, opening a potential space for Marfrig to penetrate this market.

The deal with SALIC consists of an issue of around 46% outstanding shares through a primary offering, where Marfrig and SALIC have the commitment to subscribe half each at an amount equivalent to R$9 per share – converging in a capital injection of up to R$4.5 billion, which is not bad at all in my opinion. The agreement with SALIC also states that the company receives at least two-thirds of the shares it proposes to acquire, putting it in a relevant position in BRF.

Should the injection of R$4.5 billion from the SALIC deal materialize, this should give more stability in the leverage ratio as the company estimates a target of 3.5 times by the end of the year.

Although there are risks, such as avian influenza impacting BRF's revenues and the first quarter of the year coming in weaker than expected, I still see it as feasible that Marfrig can achieve the goal of reporting an EBITDA above R$ 5 billion and can significantly reduce leverage to levels similar to the first quarter of 2022 of around three times.

Mind the Risks

Marfrig also plans to increase its number of shares as it prepares to sell between 240 million and 360 million shares at a market price corresponding to about $1.35 per share. This stock offering tends to be positive for the company's long-term leverage, as debt levels do not increase as Marfrig injects more cash into BRF.

On the other hand, even if this offer will help Marfrig have a better financial condition, this movement has dilutive effects on shareholders. It should likely pressure the performance of the company's shares in the short to medium term.

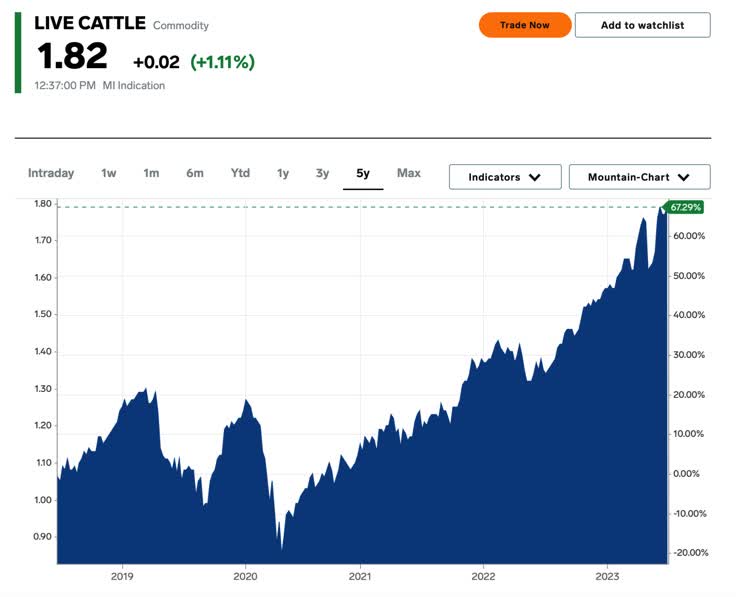

Regarding Marfrig's business, I see as a primary risk the significant reduction in U.S. beef margins, considering 60% of revenues come from North America.

Recently, live cattle prices have been at historic highs, and prices per ground beef have been 20% higher since 2020 due to years of drought conditions , mainly in the southwestern U.S., keeping cattle numbers in the U.S. at their lowest level in almost a decade.

{kind=link}

ESG has also been a high-risk factor since countries' obligations regarding global warming have reduced cattle herds, which may influence the maintenance of high live cattle prices.

Another significant risk is related to sanitary barriers in the Brazilian market. In case of embargoes on exports, Marfrig should lose revenue and simultaneously reduce its products in the domestic market due to the expansion of supply.

Valuation, Looking at Cash Flows

To value Marfrig, I will prioritize the company's cash flow generation. As the company operates in a super cyclical business as it is highly influenced by commodity prices, different life cycle stages may have varying earnings levels due to factors such as investments in growth, market penetration, or restructuring efforts.

Therefore, looking solely at earnings and the P/E ratio may not provide a complete picture of the company's value. The free cash flow yield, which considers the company's cash generation, can provide a better understanding of its financial strength and potential.

Marfrig trades at a free cash flow yield of 79.58%, considering its cash from operations of $1.737 billion in the last twelve trailing months, CAPEX of $965.2 million in the same period, and its current market cap of $978.16 million at the previous check. This multiple indicates that the company is generating a proportion of cash well above its market value.

By comparison, JBS Foods ( JBS ), the world's largest meat producer, and Tyson Foods ( TSN ), which has a significant presence in the U.S. market, have a cash flow yield of negative 3.05% and 0.52%, respectively.

Thus, I see Marfrig's high cash flow yield compared to its major peers as an indication that the market has yet to fully recognize the company's cash flow-generating potential, which could indicate that the stock trades at a discount.

The Bottom Line

In conclusion, Marfrig is a large company in the beef and hamburger industry, with a global presence and product diversification. The company counts as a competitive advantage against domestic peers in its high market exposure in North America compared to Latin America shielding itself from the country's risk.

Although it has faced recent challenges due to fluctuating meat prices and significant debt, I see good prospects for reducing its leverage through a capital injection from the Saudi company SALIC.

If this injection materializes, investors should expect Marfrig to improve its financial stability and reduce leverage to levels similar to the previous year. However, the stock may face downward pressure in the short and medium term due to the potential realization of plans to sell more stock, the reduction of beef margins in the U.S., and the presence of sanitary barriers to the Brazilian market.

Evaluating the company based on cash generation, Marfrig presents a high free cash flow yield compared to its peers. The increased free cash flow yield may indicate an undervaluation of the stock, especially considering the sharp decline in recent years.

Considering these factors, the investment thesis in Marfrig is cautiously optimistic for investors who have set their expectations right by focusing on the long term based on the company's valuation and better deleveraging prospects.

For further details see:

Marfrig Stock: A Cautiously Bullish Outlook For The Long-Term