MPX - Marine Products Corporation: Still Strong Trends And Upside Potential

2023-06-22 12:43:16 ET

Summary

- Marine Products Corporation shares may rise further due to strong trading trends, robust margins, and favorable demand for boats.

- The company's customers, who mostly belong to the middle class and above, are less sensitive to price increases and higher interest rates.

- Normalization in supply chains and a potential slowdown in inflation in the second half of 2023 may support the company's growth.

Introduction

Shares of Marine Products Corporation (MPX) have risen 41% YTD, however, I believe its financial results in the coming quarters could be a catalyst for MPX stock's upside as the start of the season lies ahead while prices for new boats and demand is generally at a favorable level.

Investment thesis

In my personal opinion, strong trading trends and robust margins could drive prices higher throughout 2023. Firstly, based on management comments, we see that the demand for boats during the winter shows remains favorable, while the start of the season is ahead of us. Secondly, the company notes a normalization in the supply chain, transportation costs and a favorable product mix (increased demand for more expensive equipment), which may support operating margins. Thirdly, despite the increase in boat prices due to high inflation, demand remains at a stable level due to the fact that customers belong to the middle class and above, which is less sensitive to higher interest rates, since most customers buy the company's products using cash, and not through the use of credit. As per Ben Palmer (President & CEO) commenting on consumer trends during the Earnings call following Q1 2023 results .

We have not with our model mix it continues to be kind of higher end boats and most of those purchasers are cash-only buyers are not as sensitive to rates.

Company overview

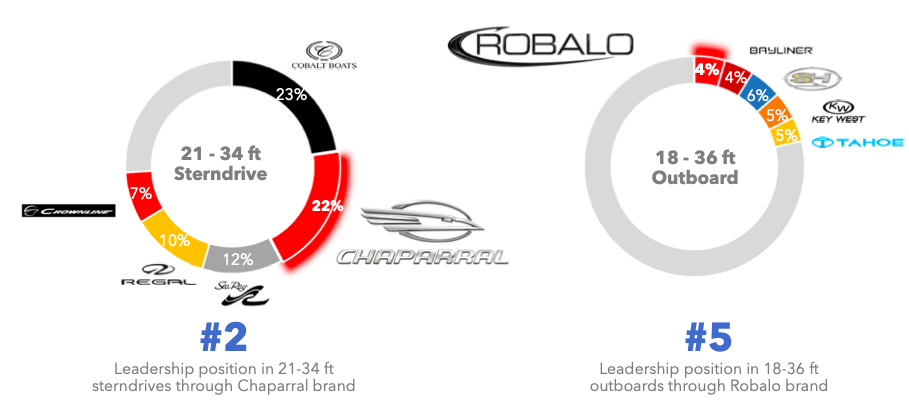

Marine Products manufactures high-quality fiberglass powerboats and is one of the market leaders. The main brands of the company are Chaparral and Robalo, which are focused on the recreational and coastal fishing categories. Dealers are the main sales channel (210 domestic and 88 international) . The company's headquarters is located in Atlanta.

Market share (Company's information)

{kind=link}

1Q 2023 Earnings review

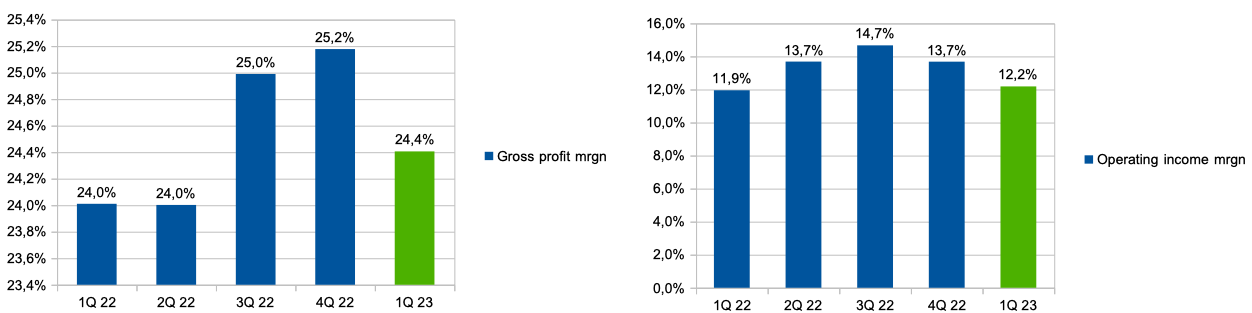

The company's revenue showed growth of 55% YoY and reached $118.9 million , which is a record figure for the company. The main drivers of revenue growth are a 40% YoY increase in sales volume due to a recovery in demand and a 12% YoY increase in the average price due to a favorable product mix.

Gross margin increased from 24% in Q1 2022 to 24.4% in Q1 2023. SGA expenses (% of revenue) remained at the same level and amounted to 12%. Operating margin increased from 11.9% in 1Q 2022 to 12.2% in 1Q 2023. You can see the details in the chart below.

Margin trends (Company's information)

{kind=link}

We are seeing a recovery in boat sales in 2023 as demand was under pressure throughout 2021 and 2022 as we saw extreme demand and price increases during the pandemic in 2020 due to high inflation and rising prices for materials and parts.

Market trends (Company's information)

I would also like to note the extremely low level of debt on the company's balance sheet, while the amount of cash is more than $43 million in the first quarter of 2023.

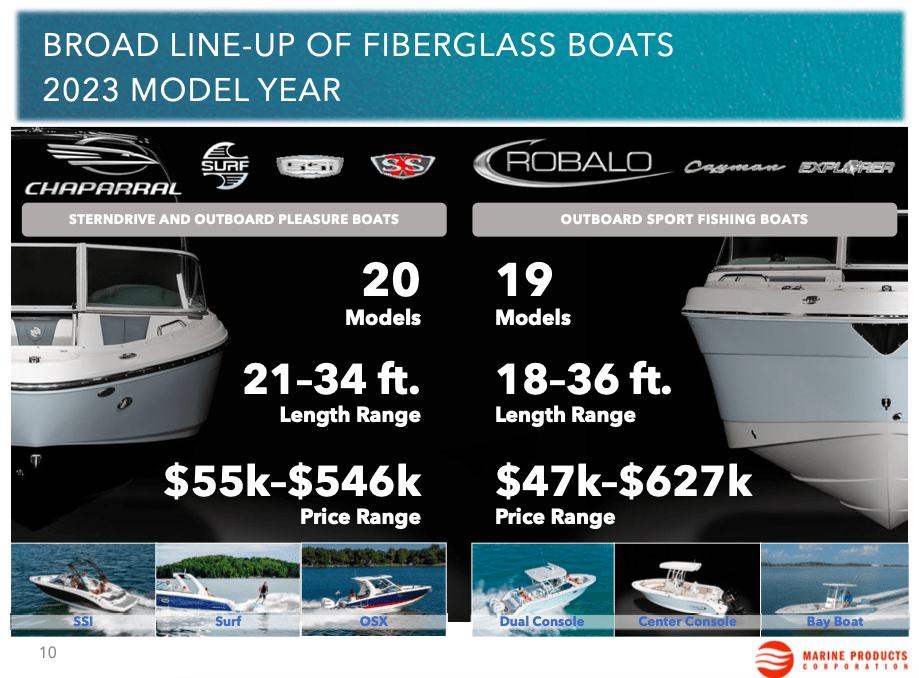

Broad line-up 2023 (Company's information)

{kind=link}

My expectations

In line with management comments , dealers (the main sales channel) continue to call for inventory, expecting strong trading trends to continue as the results of the winter show were favorable (more boats were sold than last year). At the moment, dealer stocks remain below pre-pandemic levels.

Also, I'd like to note management's comments that customers prefer to use cash to buy company products. In my opinion, this is a positive factor, since it may indicate that the client is less sensitive to rising interest rates, which, in my opinion, reduces the risk of a change in demand in a negative direction.

Normalization in supply chains can also have a positive impact, as it reduces the necessary investment in working capital, which can support the free cash flow of a business.

In addition, based on management comments, macro data and trends in other industries, I believe that we may see a slowdown in inflation in the second half of 2023, thus boat price growth will slow down, which may reduce the potential risk of pressure on demand from for relatively high prices.

Drivers

Supply chain & margin: normalization of supply chains, reduction of transport and logistics restrictions, as well as a favored product mix can help reduce operating costs, reduce investment in working capital and thus maintain the operating profitability of a business.

Fuel price: a decline in oil prices and, consequently, a normalization of fuel prices could support demand for the company's products in terms of lower cost of ownership.

Price: the ability to raise product prices and effectively pass on price increases to the end consumer can help boost the company's revenue in the future, as the company's customers are in the middle class and above, so they are less sensitive to price changes.

Risks

Macro: continued growth in inflation, lower real incomes, lower consumer confidence, or fear of a recession could put pressure on demand for a company's products and therefore put pressure on the business's growth rate. In addition, the relatively high prices of the company's products may also lead to a reduction in demand.

Supply chain: lack of parts (engines) or logistical difficulties can lead to slower production, increased operating costs and additional investment in working capital, which is negative for both revenue and business profitability.

Valuation

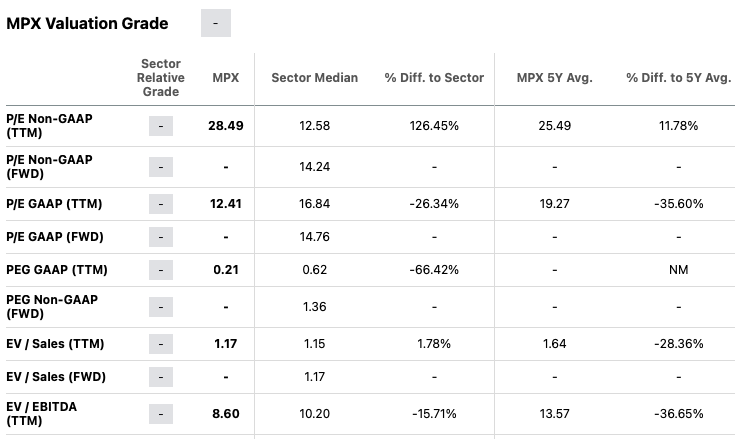

In my personal opinion, the company's shares are still undervalued relative to historical data and peers. On an EV/EBITDA ((TTM)) multiple, the company is valued at 8.6x, which I think is favorable for a company with >50% YoY revenue growth and an EBITDA margin of over 12%. You can see the details of the assessment in the chart below.

{kind=link}

Conclusion

So, in my personal opinion, Q2 and Q3 2023 financial results could help boost the share price as the start of the season lies ahead of us, while based on management comments, the winter show results were favorable and dealers continue to increase demand for the company's products, as inventories are still at relatively low levels. In addition, we see both supply chains normalizing and transportation costs normalizing, which could support production and sales volumes.

For further details see:

Marine Products Corporation: Still Strong Trends And Upside Potential