MPX - Marine Products: Quiet Compounder And Potential M&A Target

2024-01-08 01:37:47 ET

Summary

- Marine Products has achieved impressive growth, with revenue growing +10% and EBITDA +20% during the last decade.

- The company has benefited from a market-leading brand, as well as strong technological development to ensure a highly competitive suite of boats. These factors are underpinned by an extensive dealership.

- We believe its growth trajectory is sustainable in the medium term, owing to international growth opportunities, economic improvement, and increased interest in recreational boating.

- MPX appears incredibly undervalued, trading at a >100% discount. Although we are likely early with our buy rating, a 11% FCF yield is too tempting given the quality of the company.

Investment thesis

Our current investment thesis is that Marine Products Corp. ( MPX ) is a niche compounder with the potential to maintain its current trajectory, particularly as Management increasingly needs to focus on growth, unlocking international expansion, and potentially M&A. We also see an opportunity for margin appreciation, compounding its scope to generate alpha for shareholders.

This is underpinned by a solid business model, differentiation, and a quality management team. Even if growth does slow, cash accumulation and optimization should ensure a strong cash return.

Businesses of this quality are never trading at such as high FCF yield. Assuming market conditions improve in the back end of 2024 and growth returns, we see scope for significant capital appreciation to close its >100% discount.

Company description

Marine Products is a leading manufacturer of fiberglass motorized boats, primarily under the brand name Chaparral. The company, headquartered in Atlanta, Georgia, has been a key player in the recreational boating industry for several decades. Marine Products is recognized for its commitment to quality, innovation, and a diverse product line catering to various segments of the boating market.

Share price

MPX’s share price performance during the last decade has been disappointing, significantly underperforming the wider market and broadly trading flat since 2018. This is despite positive financial development, partially due to the impact of the pandemic, and also hesitancy around the long-term trajectory of the company.

Financial analysis

{kind=link}

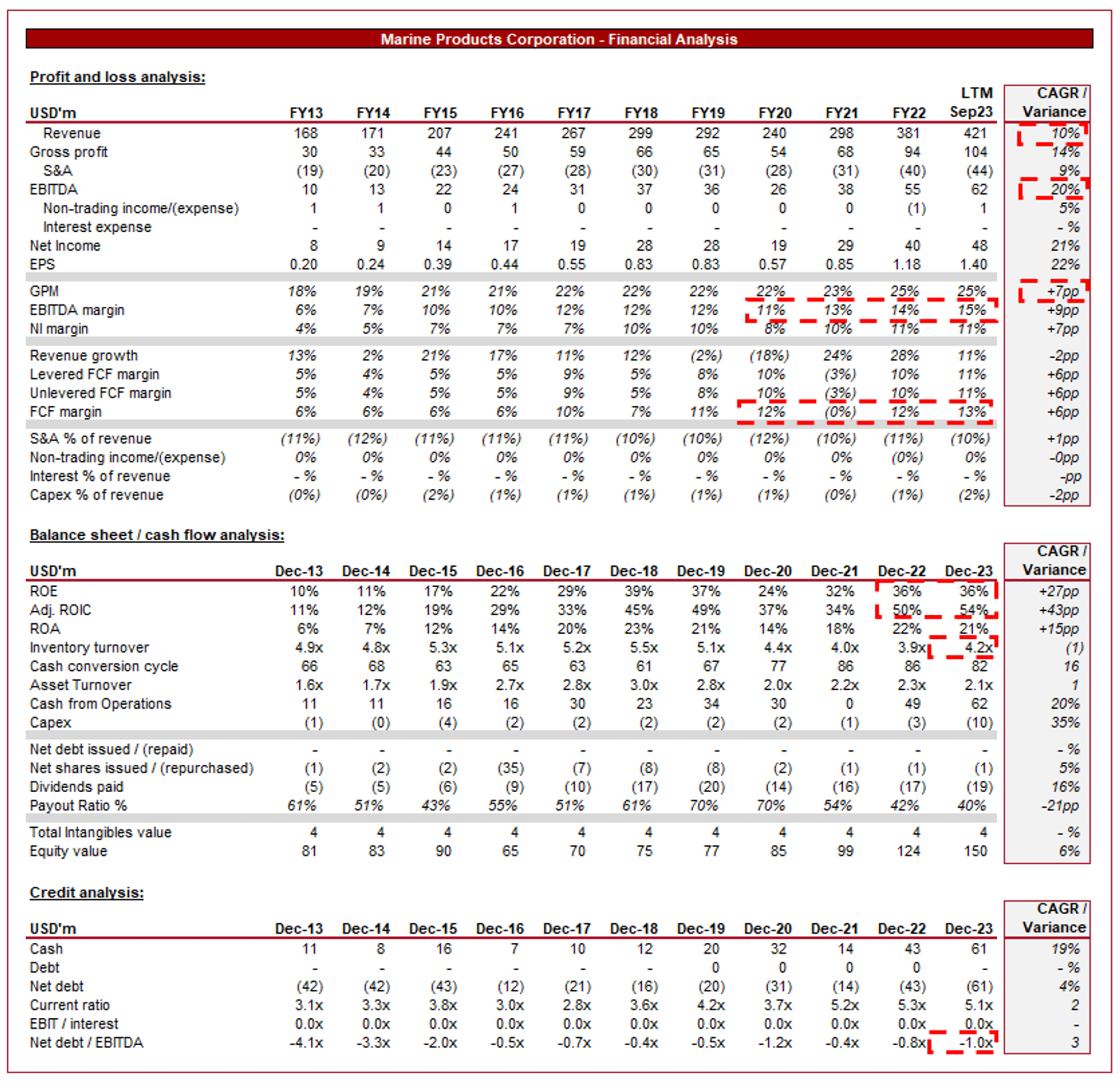

Presented above are MPX’s financial results.

Revenue & Commercial Factors

MPX’s revenue has grown at a CAGR of +10% during the last decade, with broadly consistent YoY gains, while EBITDA has impressively outperformed at +20%.

Business Model

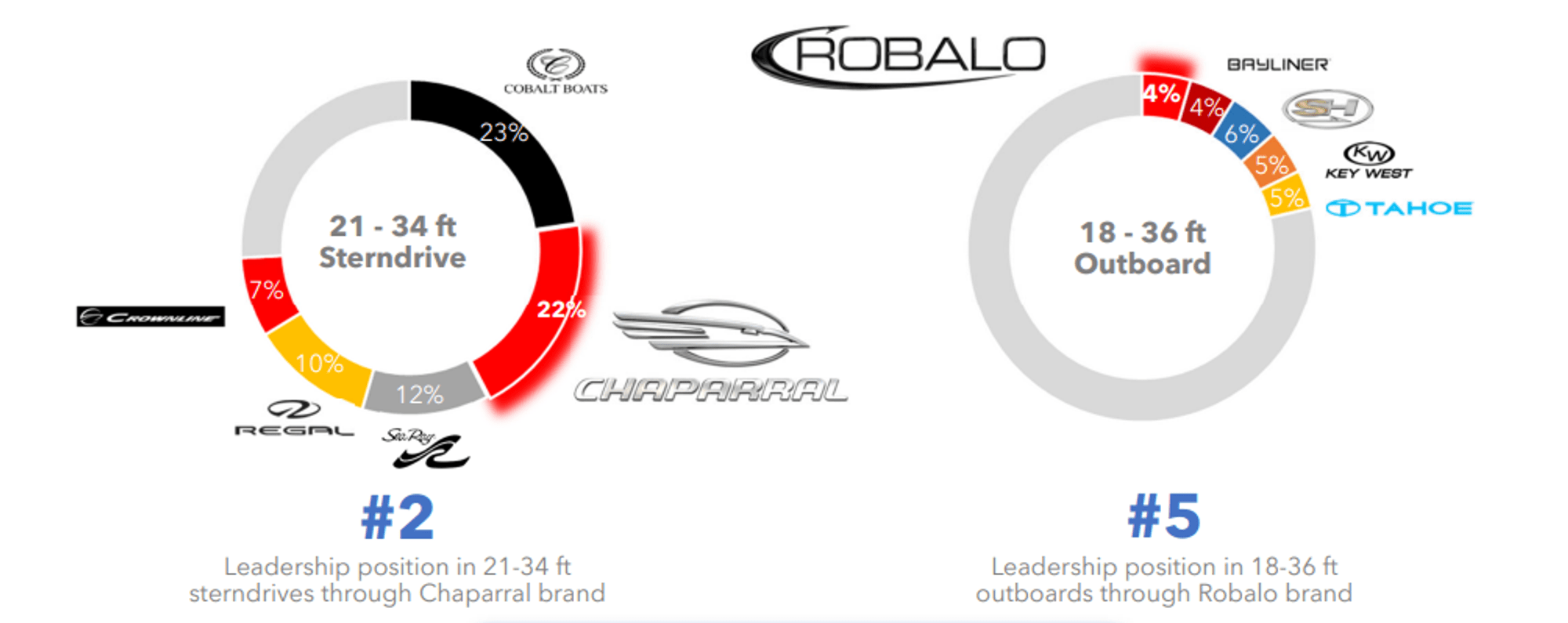

MPX specializes in fiberglass motorized boats, particularly under the brand name "Chaparral" and “Robalo”. The company has ~39 boat models, with Chaparral positioned as a premium and high-quality option in the boating market.

This focused product line allows the company to concentrate its efforts on a specific niche within the marine industry, capturing strong market share in the outboard and sterndrive segments (estimated #3). The company is primarily targeted toward the recreational and coastal fishing categories.

{kind=link}

The company handles both the design and manufacturing processes in-house. This vertical integration provides greater control over the production quality, customization options, and innovation in boat design. From an operational perspective, it allows MPX to minimize costs given its niche nature.

Continuous innovation in boat design and features is a key aspect of MPX's strategy. This ensures that its boats stay competitive in the market and appeal to current preferences. Through decades of experience, MPX has created a market-leading suite of Boats that very few competitors can rival. This technology is incrementally improved upon, ensuring its brand remains a leader. For example, in 2010, ~95% of sales were Sterndrive powered, compared to ~37% today, reflecting agility in the face of changing consumer preferences.

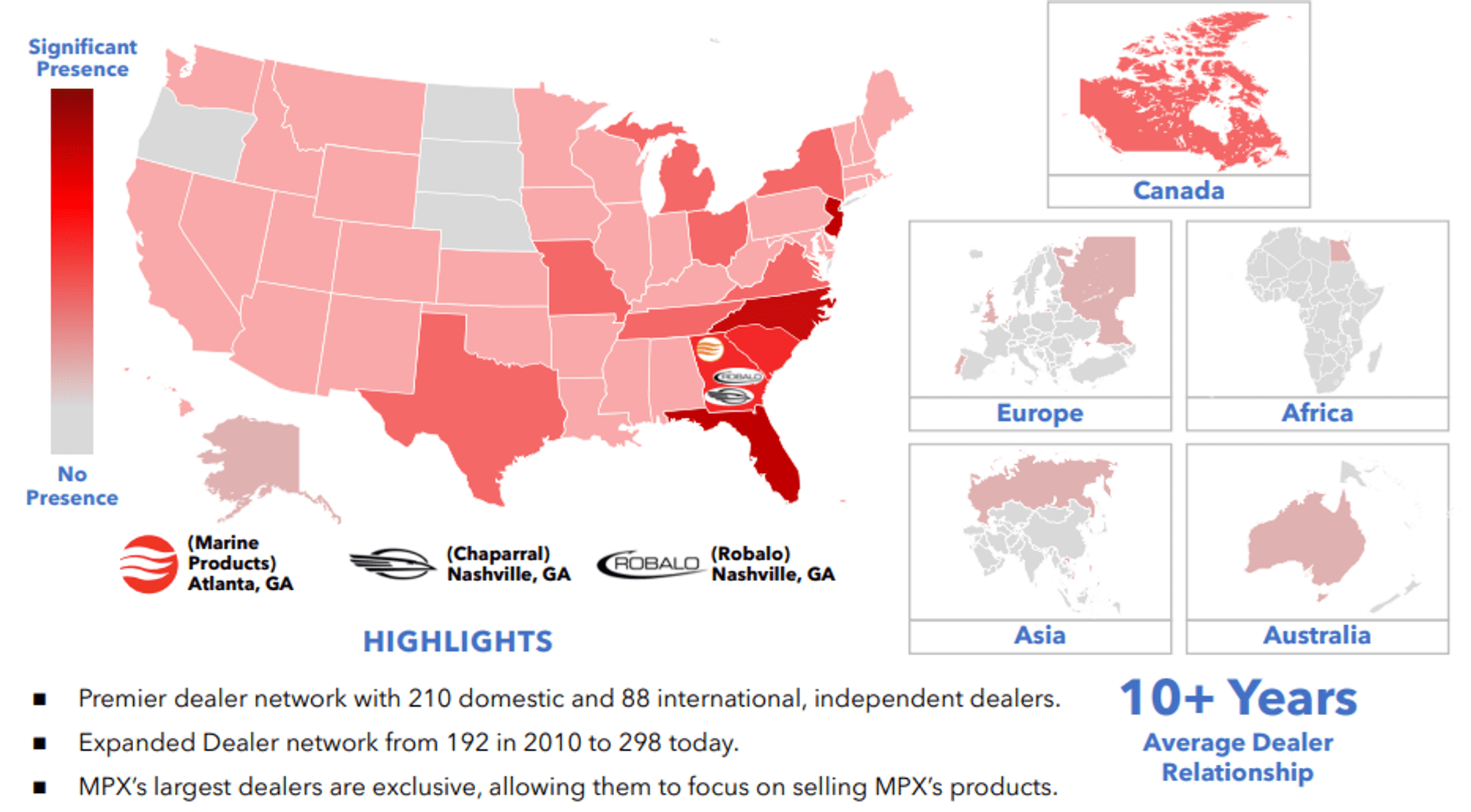

Given its niche, MPX relies on an extensive network of dealers to distribute its boats (300+ globally), many of which are exclusive. These dealers serve as crucial touchpoints for customers, providing sales, service, and support. A robust dealer network is absolutely critical to ensuring brand accessibility.

{kind=link}

Competitive Positioning

In addition to its strong business model, which is underpinned by a strong brand and technical capabilities, we believe the following factors have been critical to its competitive position:

- Effective Marketing and Branding - Successful marketing campaigns and effective branding efforts have contributed to heightened brand visibility and customer engagement. The company is actively associated with Magazines, roadshows, and other traditional media, as well as on social media.

- Economic Conditions - Favorable economic conditions, namely a decade of record low interest rates, have contributed to luxury investments and purchases, including within the Boating industry. This has increased the number of lifelong customers who will make multiple purchases over time.

- Competitive Pricing - The company’s scale and expertise allow it to target a wide price bracket, with boats starting at ~$50k and going up to ~$600k.

- Positive Customer Reviews - Positive reviews and testimonials from satisfied customers contribute to the company's reputation. Word-of-mouth marketing is absolutely critical in a niche industry where relative marketing spend cannot be significant.

Recreational Boating Industry

The recreational boating industry has experienced strong growth trends, with many of the leading players growing at low-single digits. The industry has experienced a degree of consolidation, owing to a degree of fragmentation.

MPX’s competitors include Brunswick Corporation ( BC ), Malibu Boats ( MBUU ), and MasterCraft Boat Holdings ( MCFT ).

These businesses compete on:

- Differentiation in design and features.

- Marketing strategies and brand positioning.

- Dealer network and customer engagement.

Opportunities

We believe the following factors, partnered with the company’s strong business model and competitive advantage, will drive growth in the coming years in line with historically achieved:

- After-Sales Service - Offering robust after-sales services, including warranty support and maintenance, contributes to customer satisfaction and loyalty. From a financial perspective, this allows for more consistent revenue generation and usually higher-margin income.

- Market Expansion Strategies - Pursuing a strategy of entering new markets and/or acquiring smaller peers in existing markets will contribute to greater overall business growth. With a growing middle and upper class in Asia, and limited exposure to this market thus far, MPX has high potential for growth in these markets.

- Pandemic impact - The pandemic contributed to record sales of new fiberglass boats (+15% growth in 2020 vs. 2.2% the year prior). Although this may restrict near-term demand, we believe the long-term benefits of new entrants into the market and the potential for upgrades, etc. are net beneficial.

- Interest rates declining - Central banks have indicated the current levels are not “the new normal” so financing of boats, which is an important factor for demand, should improve in the coming 12-24 months.

- Eco-Friendly Boats - With a number of industries transitioning to clean-energy motors, this represents a more longer trend factor that will impact growth.

Margins

{kind=link}

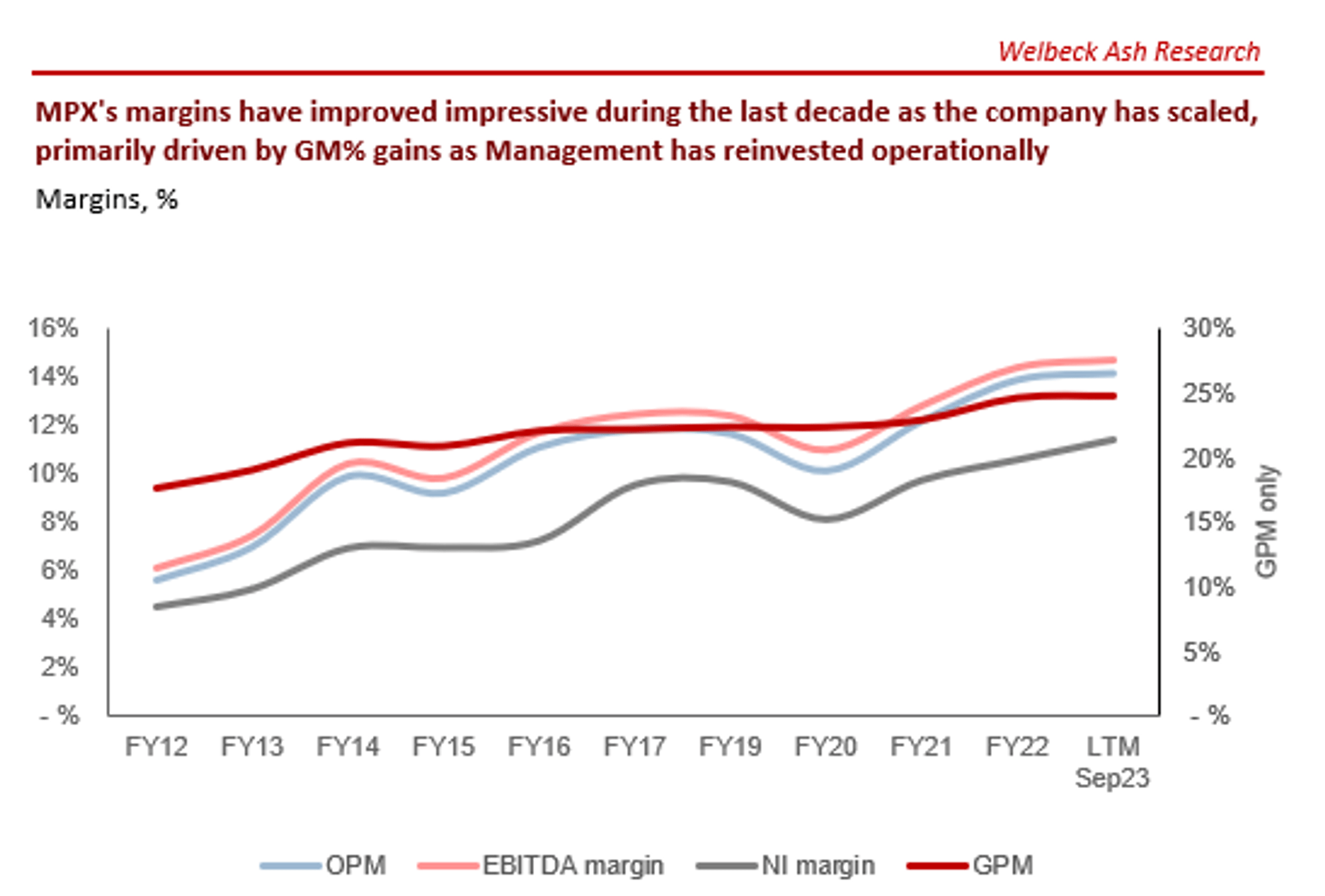

MPX’s margin development has been impressive, with EBITDA-M increasing from 6% in FY13 to 15% in LTM23 (+7ppts). The company’s trajectory was not materially derailed by the pandemic or the current economic conditions, suggesting a strong upward pressure that is likely sustainable going forward.

Margin improvement is a reflection of the company’s success, with an incremental step-up in pricing, combined with operational excellence limiting marginal costs of production. This cannot continue in perpetuity, although we suspect an EBITDA-M of ~17-18% is a reasonable 5-year target.

Quarterly results

MPX’s recent performance has ground to a halt, with top-line revenue growth of +41.8%, +55.2%, +21.2%, and (22.3)% in its last four quarters. In conjunction with this, margin improvement has slowed, likely stabilizing in response to the slowdown in revenue.

This decline in revenue is a reflection of economic conditions finally catching up. Retailers are far more careful with inventory levels, while consumer interest is normalizing. With elevated interest rates and inflation contributing to a cost of living crisis, this is an unexpected development.

Balance sheet & Cash Flows

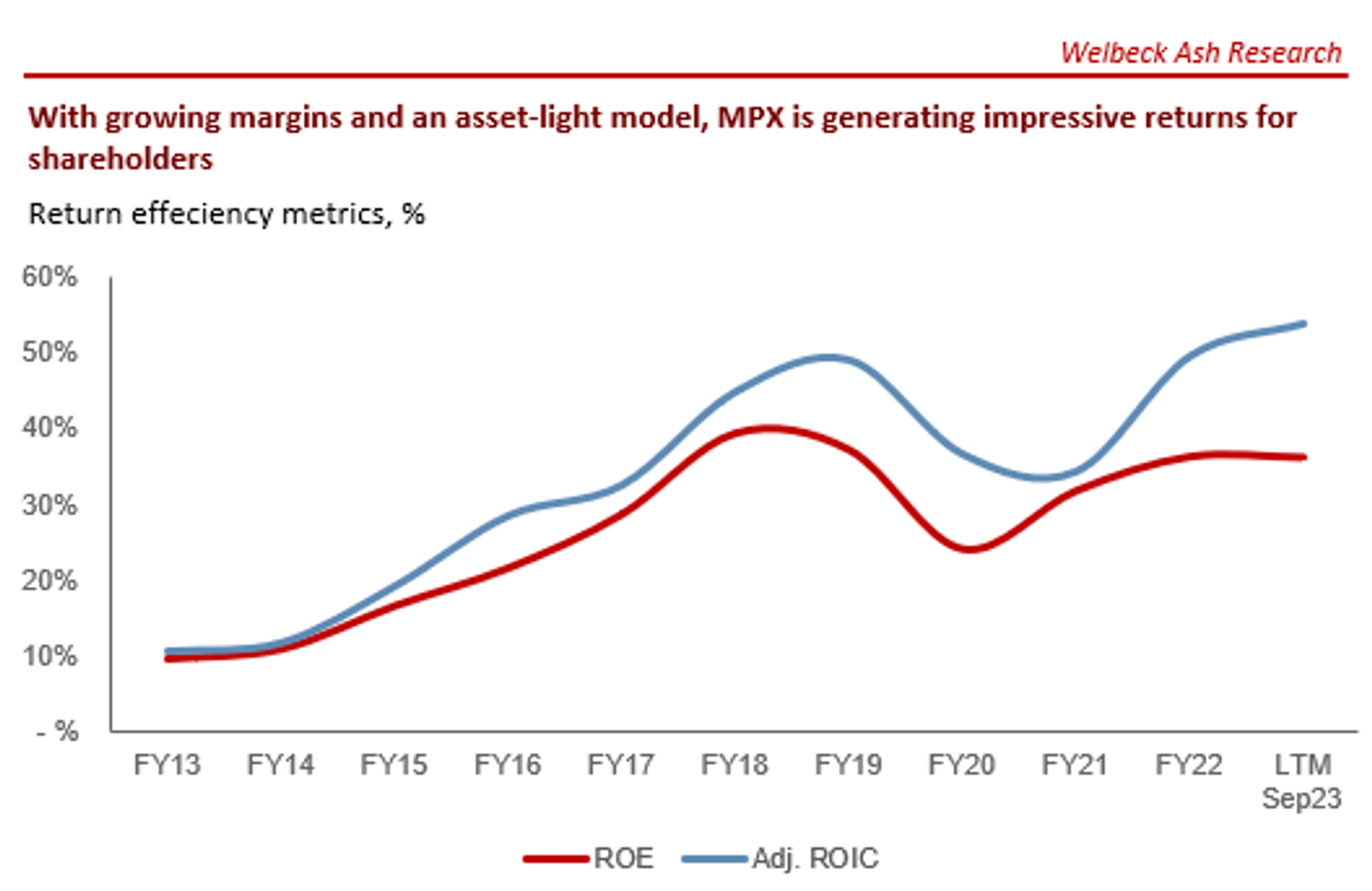

MPX’s cash generation has been incredibly consistent and on an upward trend in line with margins, allowing the company to be debt-free. This has allowed capital allocation to focus on reinvestment and shareholder returns, with ROE increasing by +27ppts and dividends growing by +16%. Management’s allocation of capital has been impressive and is showing no evidence of slowing down.

We suspect that if MPX’s growth rate does tick down, Management can reallocate cash from reinvestment to share buybacks, supporting EPS and ROE growth further.

{kind=link}

Outlook

Looking ahead, we suspect much of 2024 will be difficult for MPX, particularly due to higher comparable given the slowdown has only now set in. We see limited scope to offset this given the reliance on retailers, who will naturally be spooked by the recent downturn in demand.

We would initially target high single-digit negative growth for FY24, although it is difficult to form a concrete view until Q4 results are published. We are not overly concerned by this, however, given the signals that rates should start declining in 2024.

Industry analysis

{kind=link}

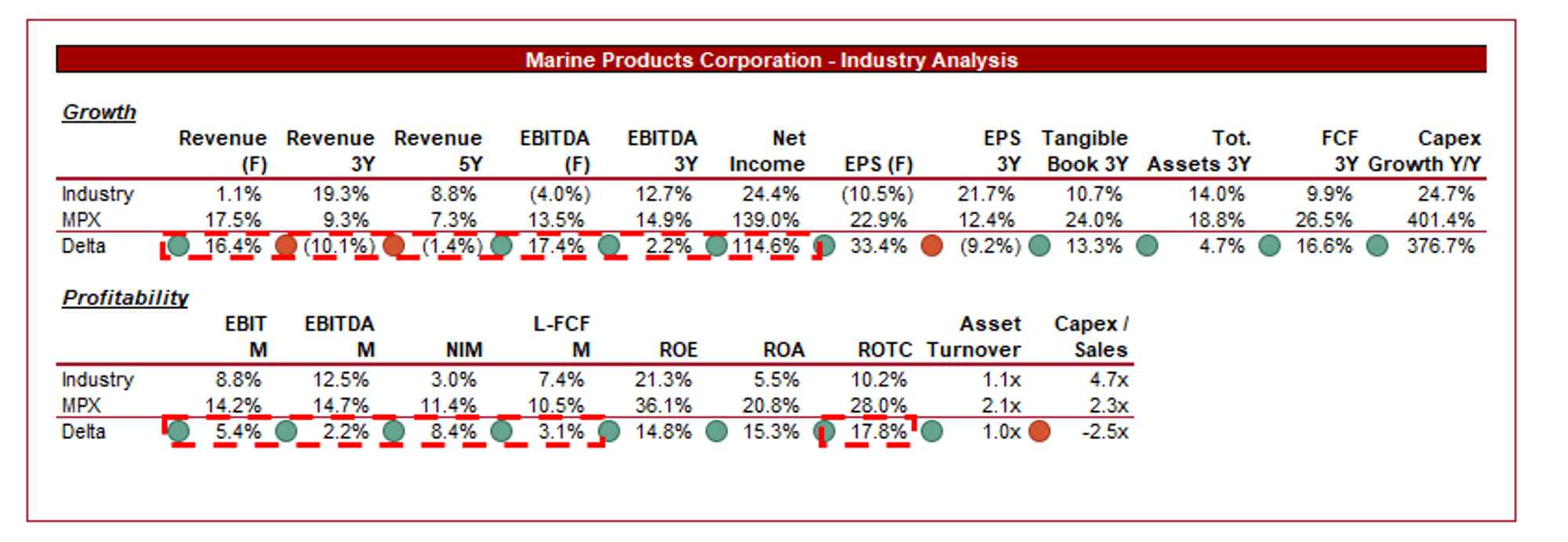

Presented above is a comparison of MPX's growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

MPX is performing incredibly well relative to its peers. Its revenue growth has slightly lagged behind on a 5Y timeframe, but this is almost wholly offset by superior profitability and FCF growth, suggesting its margin expansion is sufficient to offset the inherent weakness of its niche focus.

Further, its margins are comfortably above the average of its industry, translating to superior FCF and ROTC. This is a reflection of MPX successfully cornering this niche industry.

Valuation

{kind=link}

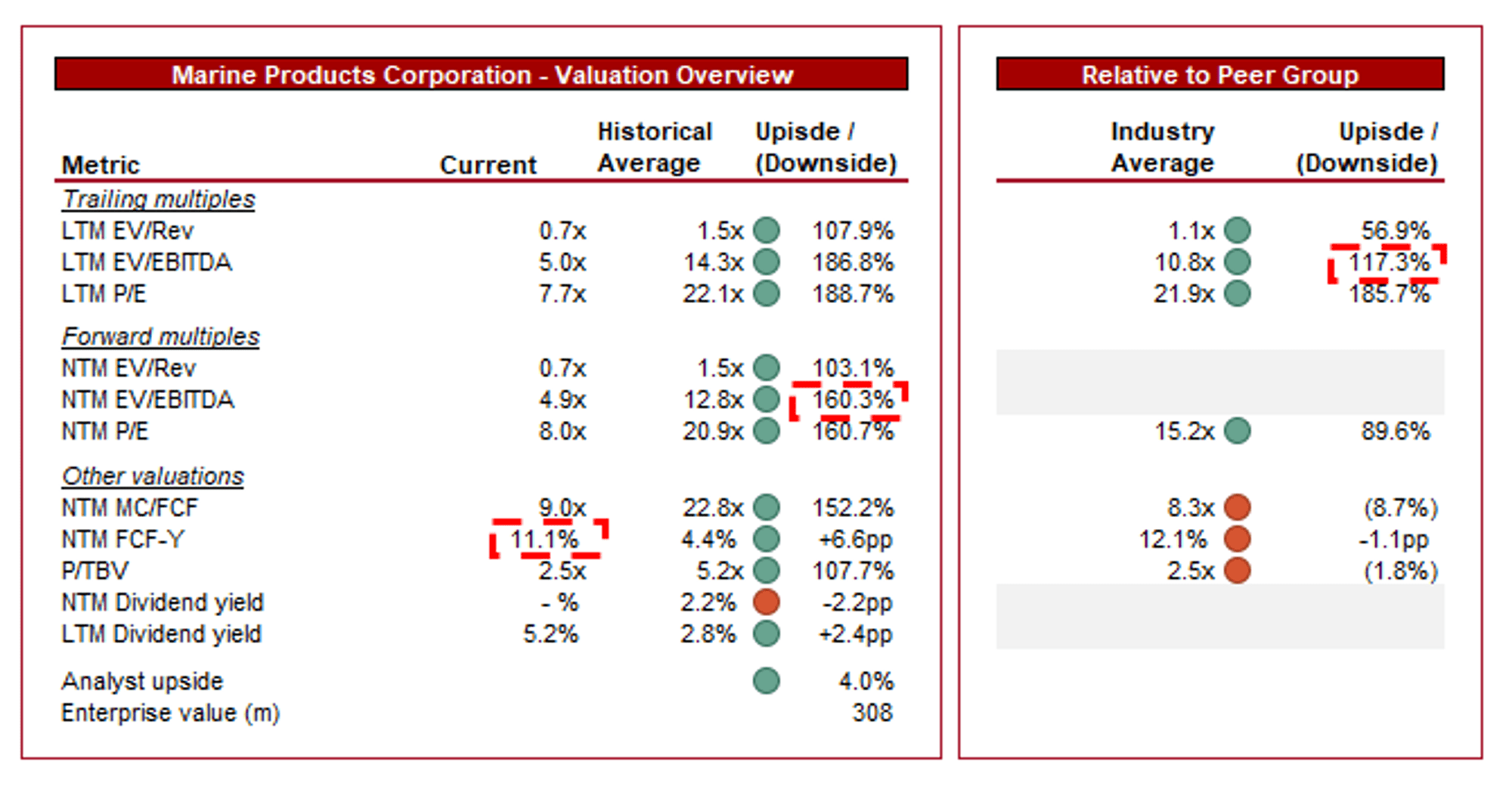

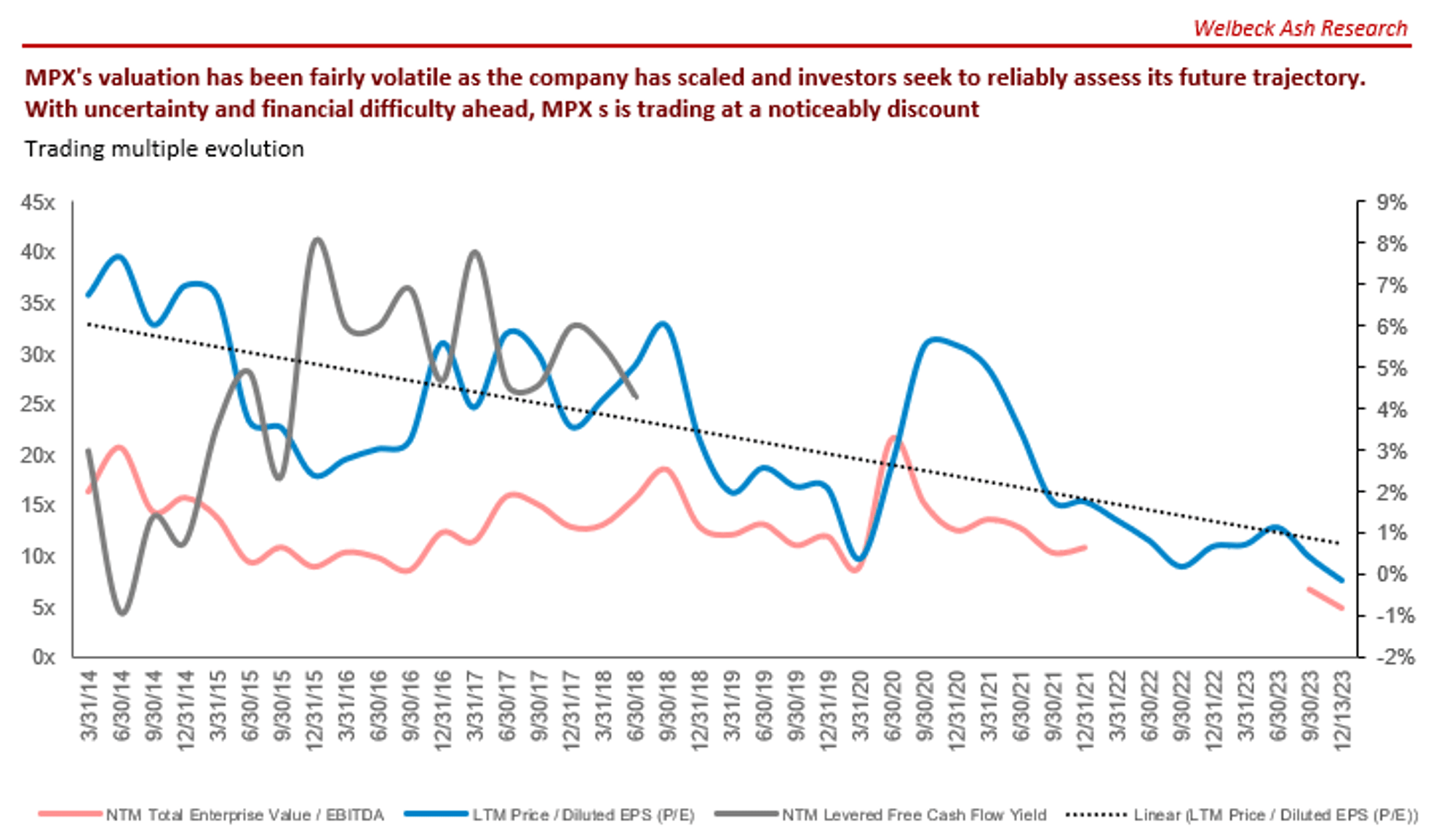

MPX is currently trading at 5x LTM EBITDA and 5x NTM EBITDA. This is a deep discount to its historical average.

The deep discount to its historical average reflects investor fear of the year to come. The company is facing macroeconomic headwinds and an inevitable slowdown in growth. This said, a discount in excess of 100% appears extreme, although likely suggests historical mispricing, also. At a 5x multiple of EBITDA, the company has an implied FCF yield of 11.1%, with a payout ratio of 40% and a growing ROE. Even with the potential pain ahead, we think the stock is clearly undervalued.

Further, MPX is trading at a ~120% discount to its peers on an LTM EBITDA basis and ~90% on a NTM P/E basis. As a member of the leisure segment, many of its peers are also suffering from post-pandemic normalization and macroeconomic headwinds. We concede that it is more greatly exposed, however, once again we struggle to reconcile the depth of the delta.

Confirming our position is MasterCraft. We covered the stock in Nov23 and rated it a hold based on the pain ahead and a ~6x NTM EBITDA valuation. Since then, the share price has appreciated ~14%, implying an appetite for a valuation in the region of ~7x based on the current outlook. MasterCraft is outperforming MPX but not sufficiently for a ~2x EBITDA multiple delta.

Although we are clearly leaning toward a buy, we see one key issue. The industry average FCF yield is 12.1%, which suggests either ~21 other stocks are also mispriced, or markets inherently value these stocks as highly risky in 2024. This suggests to us markets will need a lot of convincing to consider these stocks a buy in 2024. We will likely be early with a buy rating currently.

{kind=link}

M&A

Downside risk is somewhat covered due to the potential for M&A. The company’s ROE is 36%, its EBITDA-M is pushing toward 20%, and its business model is solid. MPX will be accretive for almost any business and it is trading at a record-low valuation.

In an ideal world, we would be highly supportive of a combination of MasterCraft and MPX, which conveniently are trading at identical market caps. Realistically, debt markets are not in a position to make this a reality but the potential is there.

Key risks with our thesis

The risks to our current thesis are:

- Greater than anticipated economic challenges affecting the luxury boating market.

- Inventory misstep contributing to cash squeeze.

Final thoughts

MPX is an incredibly well-managed company that has carved out a competitive niche. We expect healthy growth and high margins to continue, allowing distribution to increase and shareholder returns to be maximized. At an FCF yield of ~11%, this is a never-before-seen opportunity to acquire this asset cheaply. We are likely early with a buy rating but our coverage of MasterCraft implies the market still has some appetite and is slowly adjusting its expectations.

For further details see:

Marine Products: Quiet Compounder And Potential M&A Target