HZO - MarineMax: Extensive Acquisitions Could Prove Themselves Promising

2023-10-18 02:53:56 ET

Summary

- MarineMax has had a spree of acquisitions in the past years to strategically grow its bottom line, resulting in a significant amount of debt but promising revenue growth.

- The company's EBIT margin has been growing as MarineMax's operations have scaled up organically and through acquisitions.

- At the current price, I believe that MarineMax is extensively cheap - as my DCF model estimates a good upside, I have a buy-rating for the stock.

MarineMax ( HZO ) sells recreational boats. The company has had an aggressive spree of acquisitions in the past few years to strategically grow the company’s bottom line. Although the acquisitions have resulted in MarineMax drawing a significant amount of debt, I believe the strategy is mostly promising – the company’s revenues have climbed significantly in the past few years. As MarineMax is currently priced quite low compared to the company’s probable sustainable earnings level, I have a buy-rating for the stock.

The Company & Stock

MarineMax owns numerous boat brands as well as boat dealers. The company’s boat brands include names such as Azimut, Aquila, Galeon Yachts, and MasterCraft – the company has a wide portfolio of premium boat brands. In addition, the company has a wide network of boat dealers that help MarineMax in selling the brands as well as in selling parts and services for boats. In total, the new boat sales are still the company’s clearly largest segment with around 73.2% of total sales in FY2022:

MarineMax Q3/FY23 Presentation

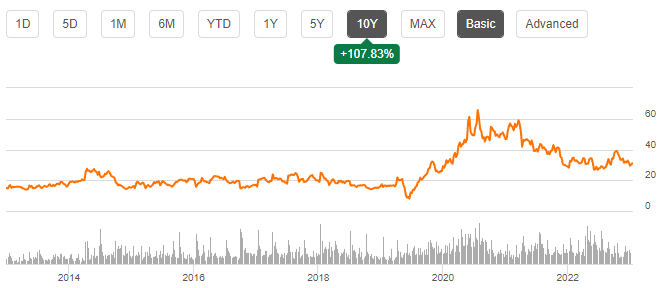

MarineMax’s stock price has had a decent run on the stock market – in the past ten years, the stock’s GAGR has been 7.6%:

{kind=link}

Ten-Year Stock Chart (Seeking Alpha)

Financials

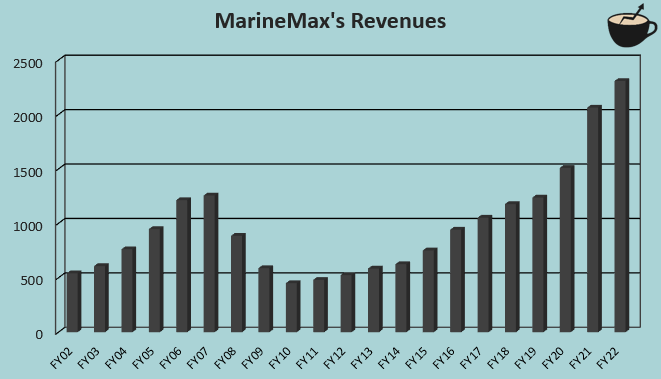

MarineMax’s revenues have had a turbulent history with clear trends – the company’s revenues have mainly climbed, with the financial crisis being a large exception in FY2008 to FY2010:

{kind=link}

Author's Calculation Using TIKR Data

The company has still kept a good long-term growth rate despite the financial crisis’ impact – from FY2002 to FY2022, MarineMax’s compounded annual growth rate has been 7.5%. The growth hasn’t been organic, especially in the recent years, though – MarineMax’s strategy revolves around acquiring and optimizing new parts of the business.

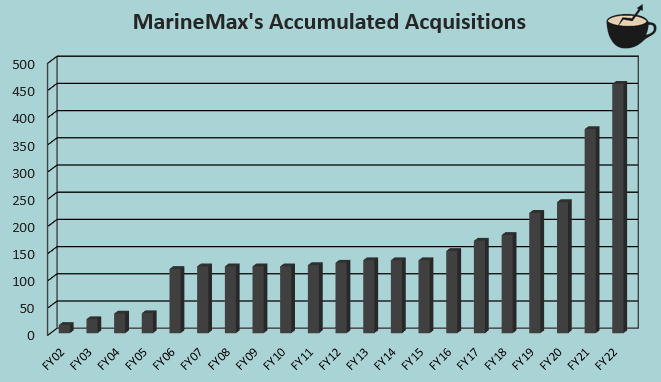

MarineMax doesn’t pay out a dividend, as the company has a large focus on acquisitions – from FY2002 to FY2022, the boat retailer has had cash acquisitions totalling to an amount of $458 million with an acceleration in the most recent years:

{kind=link}

Author's Calculation Using TIKR Data

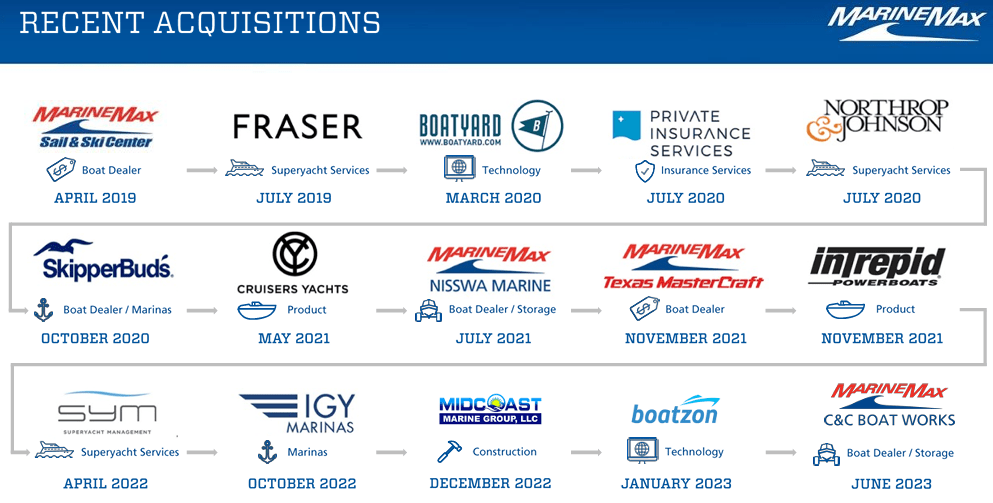

The company’s pace of acquisitions in the past years has been very frequent – the revenue CAGR of 17.4% from FY2015 to FY2022 is clearly higher than the mentioned longer-term average of 7.5%. From April of 2019 to June 2023, the company has completed 15 acquisitions, with a recently finished large acquisition of IGY Marinas that was bought for around $480 million in cash. Other recent acquisitions include Sym, Midcoast Marine Group, boatzon, and C&C Boat Works:

{kind=link}

Recent Acquisitions (MarineMax Q3/FY23 Presentation)

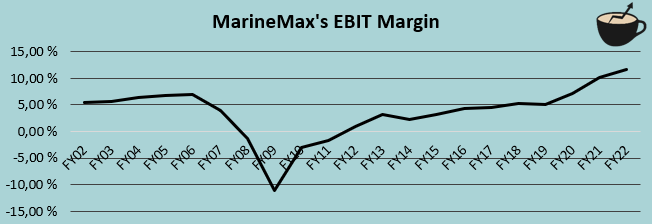

A larger scale of operations has clearly improved MarineMax’s bottom line in the long term – the company’s EBIT margin has been on a mostly constant rise after the financial crisis. From FY2002 to FY2022, the company’s average EBIT margin is 3.6%, with the current trailing figure standing at a clearly better level of 9.7%.

{kind=link}

Author's Calculation Using TIKR Data

As MarineMax has had an extensive amount of acquisitions in the recent past, the company hasn’t been able to finance the acquisitions from its own cash flows – MarineMax’s balance sheet has seen a significantly growing debt balance. At the moment, the company has long-term debts totalling $432 million of which $32 million is in the current portion. Moreover, the company has a significant amount of short-term borrowings at $514 million – in total, the debts of $946 million are very large compared to MarineMax’s market capitalization of around $670 million.

Valuation

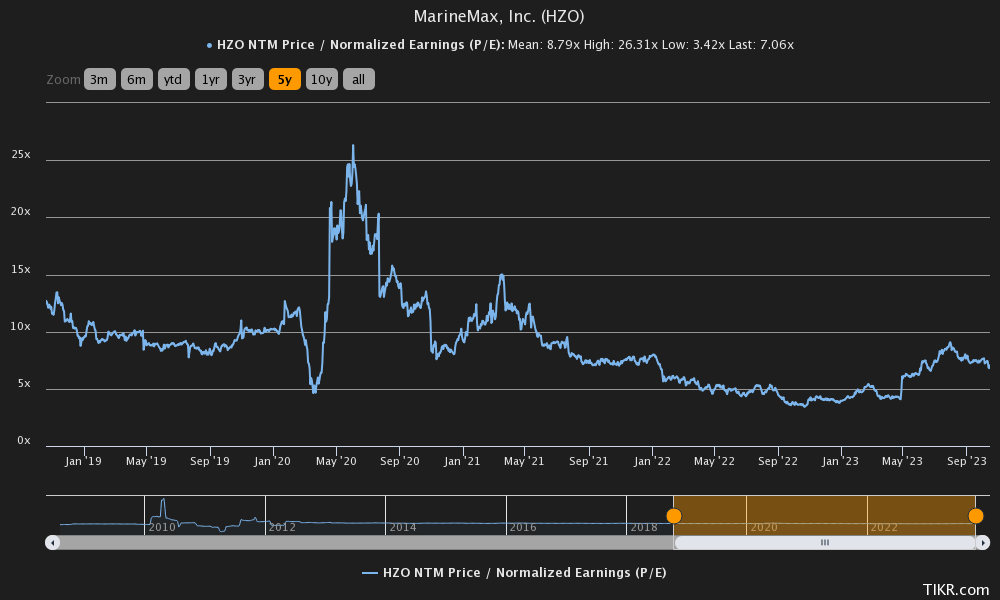

Currently MarineMax’s forward P/E ratio stands at 7.1, well below the five-year average of 8.8 and high of 26.3:

{kind=link}

Historical Forward P/E (TIKR)

The P/E ratio of 7.1 seems very low as the company’s forward earnings shouldn’t be extraordinarily high in the next twelve months. Although MarineMax does invest heavily to keep up the mostly growing earnings, I believe the P/E ratio is mostly representative of MarineMax’s cash flows. To analyze the valuation further, I constructed a discounted cash flow model as usual.

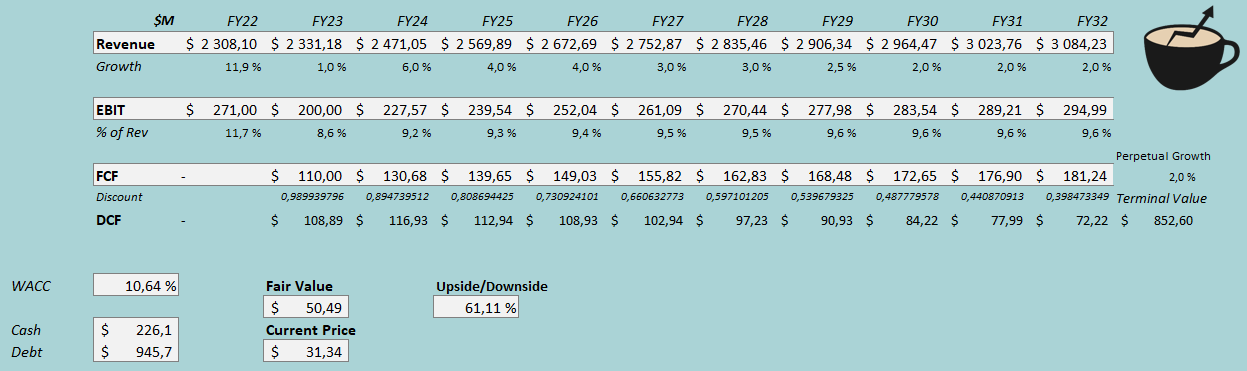

I estimate a very small growth of 1% for the current fiscal year, as MarineMax is facing tougher demand. After the year, I estimate a growth of 6% for FY2024 as the IGY Marinas acquisition’s revenues are accounted for, and the company’s demand could start to slowly recover. After FY2024, I estimate the company’s organic growth to slow down in steps into a perpetual growth of 2% - from FY2024 to FY2032, I estimate an organic CAGR of 2.8%.

For MarineMax’s EBIT margin, I estimate a decrease of 3.1 percentage points into an EBIT margin of 8.6% and an EBIT figure of $200 million. After the year, I estimate the industry’s demand situation to become slightly better as I do with revenues – I estimate the EBIT margin to rise into 9.2% in FY2024. After the year, I estimate very slight operating leverage that’s mostly in line with MarineMax’s long-term history – I estimate the margin to rise into a level of 9.6%. The company should have a moderately good cash flow conversion, although the growth should require a good amount of investments.

The mentioned estimates along with a cost of capital of 10.64% craft the following DCF model with a fair value estimate of $50.49, around 61% above the stock’s price at the time of writing:

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, MarineMax had around $15 million in interest payments. With the company’s current outstanding interest-bearing debt balance, MarineMax’s interest comes up to 6.26%, used in the CAPM. The company hasn’t recently shied away from drawing debt – I estimate that the company’s long-term debt-to-equity ratio is a high figure of 40%.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.82% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate . Yahoo Finance estimates MarineMax’s beta at 1.57 , as boat sales are quite cyclical in nature. Finally, I add a small liquidity premium of 0.5% into the cost of equity, crafting the figure at 14.60% and the used WACC at 10.64%.

Takeaway

At the current price, MarineMax seems to be an interesting investment opportunity. The company does operate on quite a cyclical industry and has drawn an excessive amount of debt to finance acquisitions, but if the company manages to ride through the rough tide smoothly, the current price seems promising – as my DCF model estimates an upside of 61%, the stock has significant potential. Although there are prevalent risks, in my opinion the risk-to-reward seems good – I have a buy-rating for the stock.

For further details see:

MarineMax: Extensive Acquisitions Could Prove Themselves Promising