CSLLY - Market Is Still Not Pricing In The FDA And EU EMA Approvals For uniQure

2023-05-22 17:38:02 ET

Summary

- uniQure secured FDA approval late last year and EMA approval in Q1 2023 for its AMT-061 Hemophilia B treatment. This paves the way for its commercialization in the US and EU.

- It also has a healthy R&D pipeline, with its Huntington’s disease treatment in Phase I/II trials and several others in preclinical trials.

- uniQure is valued here as a pre-revenue company assessing its liquidation value, value of potential cash flows from AMT-061 commercialization and estimating the worth of its future R&D efforts.

- The value I get for uniQure is close to $39/share, which is close to 2X the current price.

- The market seems to be pricing uniQure as if it was still in the approval process for AMT-061. When a catalyst event corrects this mispricing, the patient investor will be rewarded handsomely.

Company Overview and R&D Pipeline

uniQure N.V. ( QURE ) is a Netherlands-based small pharma company focusing on research and development of new gene therapy treatments. It is primarily involved in developing single treatment gene therapies for genetic diseases of the nervous system. uniQure was founded in 1998 and in 2012, it got incorporated as the gene therapy business of AMT.

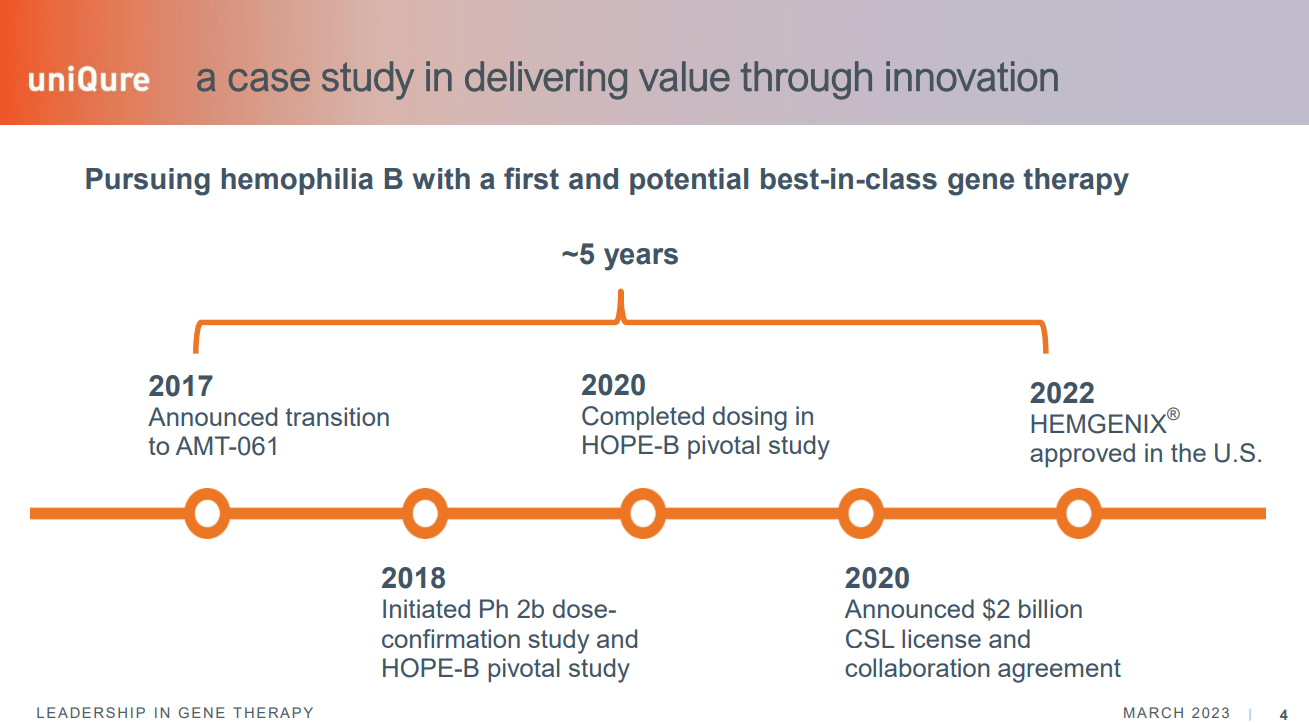

From a product pipeline perspective, it has 1 program (AMT-061 or HEMGENIX for treatment of Hemophilia B) that just received approval for commercialization in the US and the EU. For this program, uniQure entered into a commercial licensing agreement in 2020 with CSL Behring, a unit of CSL Limited ( CSLLY ), who is responsible for commercialization of HEMGENIX. As part of this agreement, uniQure received some upfront payments from CSL Behring and is entitled to specific milestone payments and royalties on net sales of HEMGENIX (more on this later).

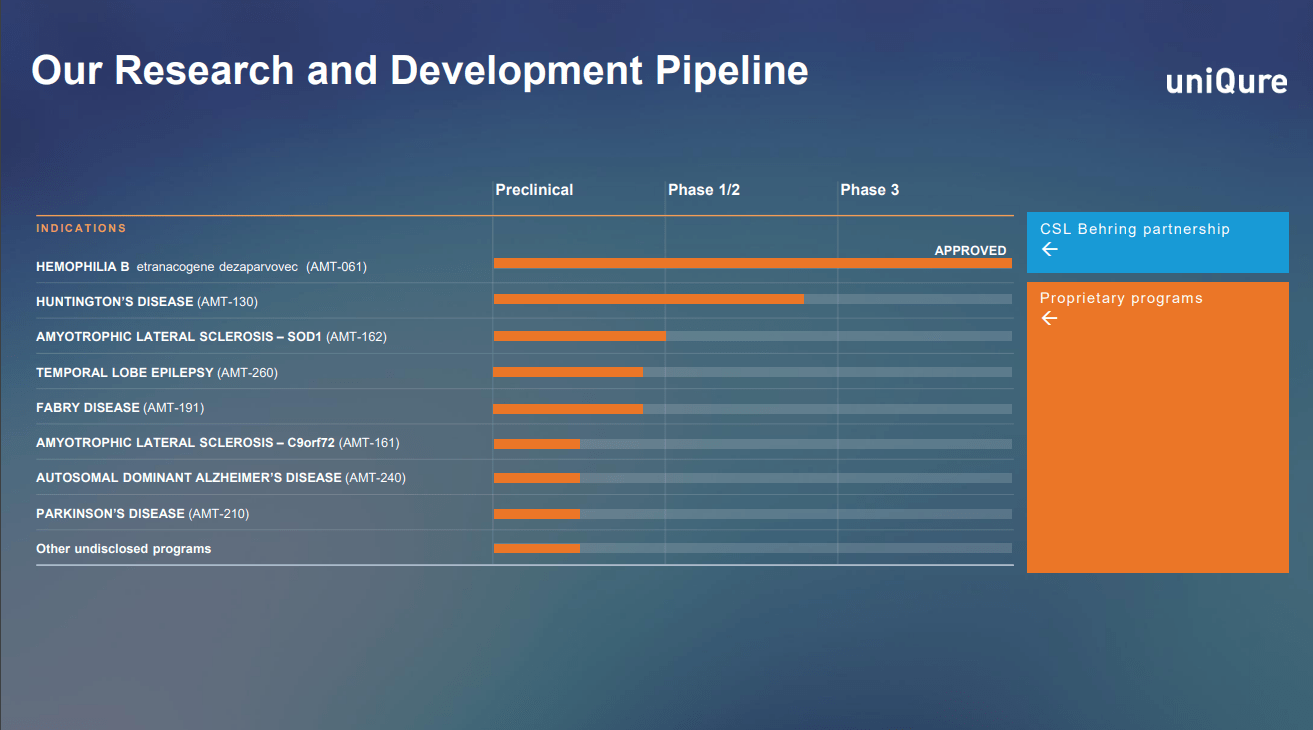

The 2nd program is AMT-130 for the treatment of Huntington's disease. It's currently undergoing Phase I/II clinical trials in the US and the EU. In addition, uniQure has a number of programs in the Preclinical trial phase, for which it intends to file Investigational New Drug ((IND)) applications with the FDA. The chart below shows the entire R&D pipeline for uniQure.

uniQure Corporate Presentation, March 2023

{kind=link}

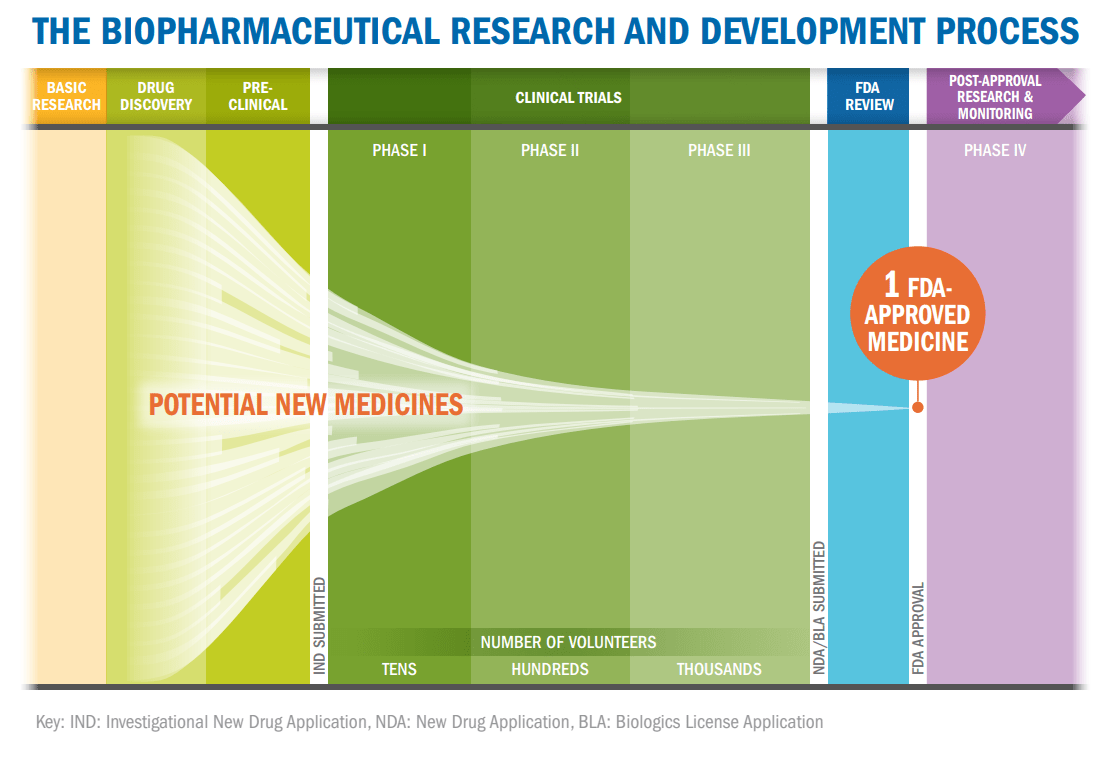

The new drug discovery, development and approval process is a lengthy and costly process. According to Phrma.org , it takes 12-15 years on average for an experimental drug to travel from the lab to US patients. Only 5 in 5,000 compounds that enter preclinical testing make it to human testing and one 1 of these 5 tested is approved.

phrma.org Chi Heem Wong, Kien Wi Siah, Andrew W Lo. "Estimation of clinical trial success rates and related parameters". Biostatistics 20(2): April 2019

{kind=link}

{kind=link}

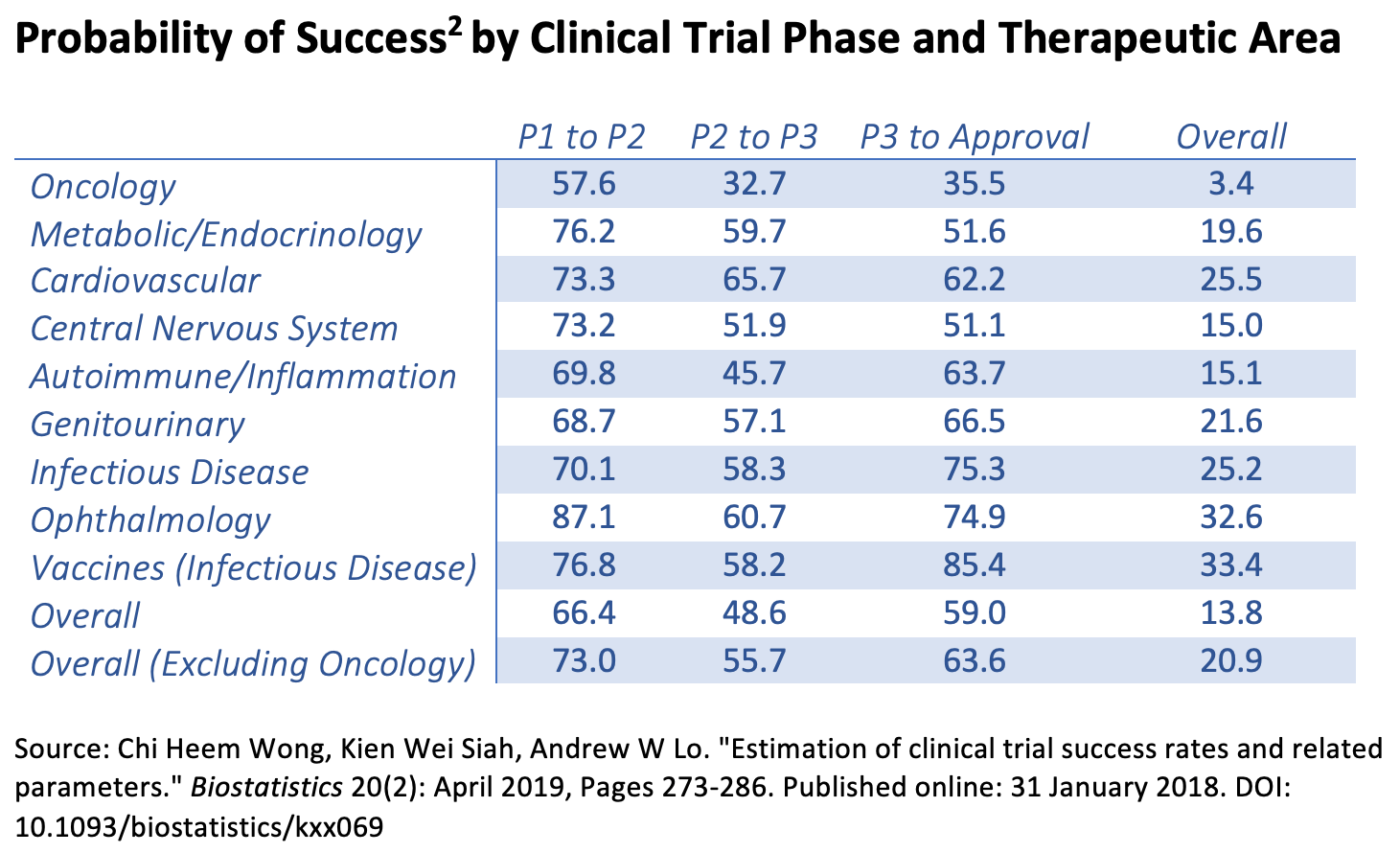

Considering these facts, uniQure is in a strong position with its 1st drug approved for commercialization both by the FDA and the European EMA.

uniQure Corporate Presentation, March 2023

{kind=link}

Valuing a Pre-Revenue Company…

From an intrinsic valuation perspective, I treat uniQure as a pre-revenue company though it has started to earn some revenues in the past 2 years. The reason for this choice is that the revenue stream thus far has been driven by the upfront payments and subsequent milestone payments from CSL Behring on the licensing agreement for AMT-061 and the treatment is not yet commercialized. Therefore, past revenues are quite volatile and should be the basis to project future revenues. Instead, the approach I use here is more akin to a "sum of the parts" valuation. For uniQure, this amounted to assessing the value of its current assets in the form of its liquidation value, evaluating potential cash flows from AMT-061 commercialization and assessing the value of its future R&D efforts. The sum of these 3 components, which are mutually exclusive and cumulatively exhaustive, provides an assessment of the value of the entire firm. Needless to say, along the way, I made some assumptions, which may not hold true and could have a material impact on the valuation. I would welcome any and all feedback on the overarching valuation approach and these implicit or explicit assumptions.

Value of current assets - Here, I consider the book value of tangible assets and all liabilities for the company and assess the liquidation value based on the difference in these. I think the use of book value does not cause any major aberrations in estimation as their assets are largely in cash and receivables. Also, I ignore the value of intangible assets like goodwill, operating lease right of use assets and other intangible assets to get a conservative estimate. As seen below, the liquidating value I get is $311MM or $137MM excluding debt and cash & equivalents .

Author's estimate & analysis

Value of potential cash flows from AMT-061 - I first look at the licensing agreement for AMT-061 from the perspective of CSL Behring to ensure to validate the assumptions I use. When the licensing agreement was consummated, AMT-061 was still in clinical studies. Therefore, CSL Behring was bearing part of the risk of the treatment not getting FDA or EMA approvals. With this increased risk, the NPV value still has to be positive for CSL Behring to sign the deal.

The global hemophilia treatment market size was estimated at $12.8 billion in 2021, and is projected to grow at a CAGR of 7.5% until 2031 . CDC estimates hemophilia B represents about 20% of all hemophilia cases in the US. Assuming the treatment cost does not vary much between various types of hemophilia, the market size of hemophilia treatment comes out to be $3.2B in 2024 (when it is likely for meaningful sales of AMT-061 to begin). I further assume that being the first of its kind treatment, AMT-061 would capture a 15% market share in 2024 which would grow to 30% by 2030. Beyond 2030, I assume that sales would start decreasing substantially as the patent protection ends.

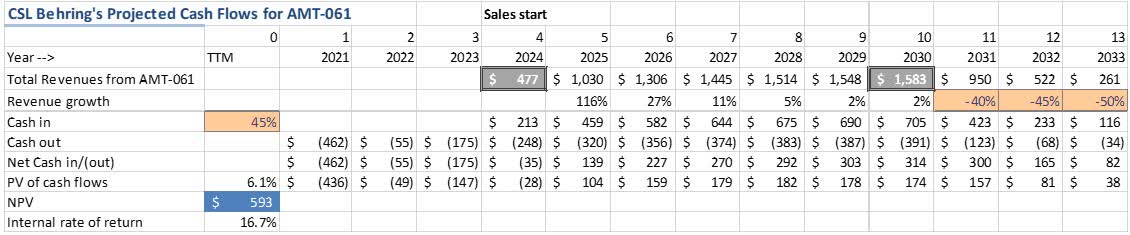

This licensing deal can be viewed as CSL Behring buying the R&D for this project. Therefore, to estimate the NPV of the deal from CSL's perspective, I took the median of free cash flows of all pharma companies on a pre-R&D basis, which comes out to be 45%. The contractual milestone and royalty payments to uniQure are its outgoing cash flows. Though the exact terms of the deal are not publicly available, uniQure has stated that it has received $462.4MM in cash payments in 2021, $55MM in 2022 and is expected to receive $100MM for US drug launch and $75MM for EU drug launch in 2023. Beyond that, it expects to receive $1.3B in various commercial milestone payments and tiered double-digit royalties of up to a low-twenties percentage of net product sales. I assume a 13% average royalty payment. The WACC for CSL in May 2020, when the deal with signed, was estimated to be 6.1%. Based on these assumptions, the cash flows for AMT-061 for CSL Behring are presented below.

{kind=link}

The project has an NPV of about $600MM and an internal rate of return of 16.7% if the treatment were to get approved. On the other hand, if the treatment was not approved, CSL's potential loss would have been ($485MM). FDA Phase 3 approval rate for Central Nervous System treatments is 51%. Using this probability of success, the NPV for the project at the time of signing would have been around $68MM, which is still positive. This lends some credibility to the assumptions made around these cash flows.

Next, I used the same cash flows to assess the value of this deal from uniQure's perspective. However, in this exercise, I used a conservative approach and made a couple of changes. First, instead of the $175MM in launch payments due in 2023, I only assumed $100MM. This was based on uniQure's latest 10-K report in which they have hinted at the EU launch payment of $75MM may not materialize. Secondly, I assumed that only 50% of the remaining milestone payment of $1.3B would be realized. With these modifications, the present value of cash flows for uniQure comes out to be $1.3B. Further, I assume uniQure will bear some commercialization costs, which I estimate as being 2/3 of its projected R&D spend for 2023, or $168MM. This brings the NPV for this project to $1,135MM .

{kind=link}

Value of future R&D - To estimate the value of their future R&D efforts, I assume that uniQure would keep investing in R&D at a CAGR of 27% for the next 5 years (which has been their CAGR for the past 4 years) and thereafter, gradually decline to 10% over the following 5 years. Furthermore, I assume that every $ of R&D investment produces a $1.25 return for the next 5 years, which gradually declines to $1 by the end of 10 years. Since there is more uncertainty in these cash flows, I also assume a higher discount rate of 15%. With these assumptions, the value I get for future R&D is $545MM .

{kind=link}

Summing these 3 components of value, the total value of operating assets for uniQure comes out to be $1.8B. After accounting for cash, outstanding debt and outstanding employee stock options, it yields an equity value of $1.93B for the company or $39/share, which is approximately 2X the current market price.

Valuation Model ($ million)

Author's estimates & analysis

Elusive Catalysts

When I first valued this stock back in June of 2022, the major catalysts I foresaw were the US FDA approval and the EU EMA approval for AMT-061. The company's value was highly dependent on whether their Phase 3 trials would succeed in winning these approvals. Using the 51% probability of FDA approval, I computed the value of AMT-061 cash flows at $579MM. Combined with the liquidation and the future R&D components, this yielded a total equity value of about $1.4B or $28/share. The stock was trading at a discount to this value as well, hovering typically around the $18 range.

In November 2022, the FDA approved the marketing application for the US, and in February 2023, the EMA approved the marketing application for EU. In November 2022 when the company announced the FDA approval, the stock price did jump from around $21 to around $27. However, in 2 months, it gave back all of the gains. The EU approval announcement in February 2023 did not have any material impact on the stock price. Both these major milestones have so far proven elusive for the market to realize the true value of uniQure. Notwithstanding the fact that the stock traded at an all-time high of ~$80 in the summer of 2019 when the Phase IIb/3 trials were still ongoing for AMT-061, it seems odd that the stock failed to react on these approvals.

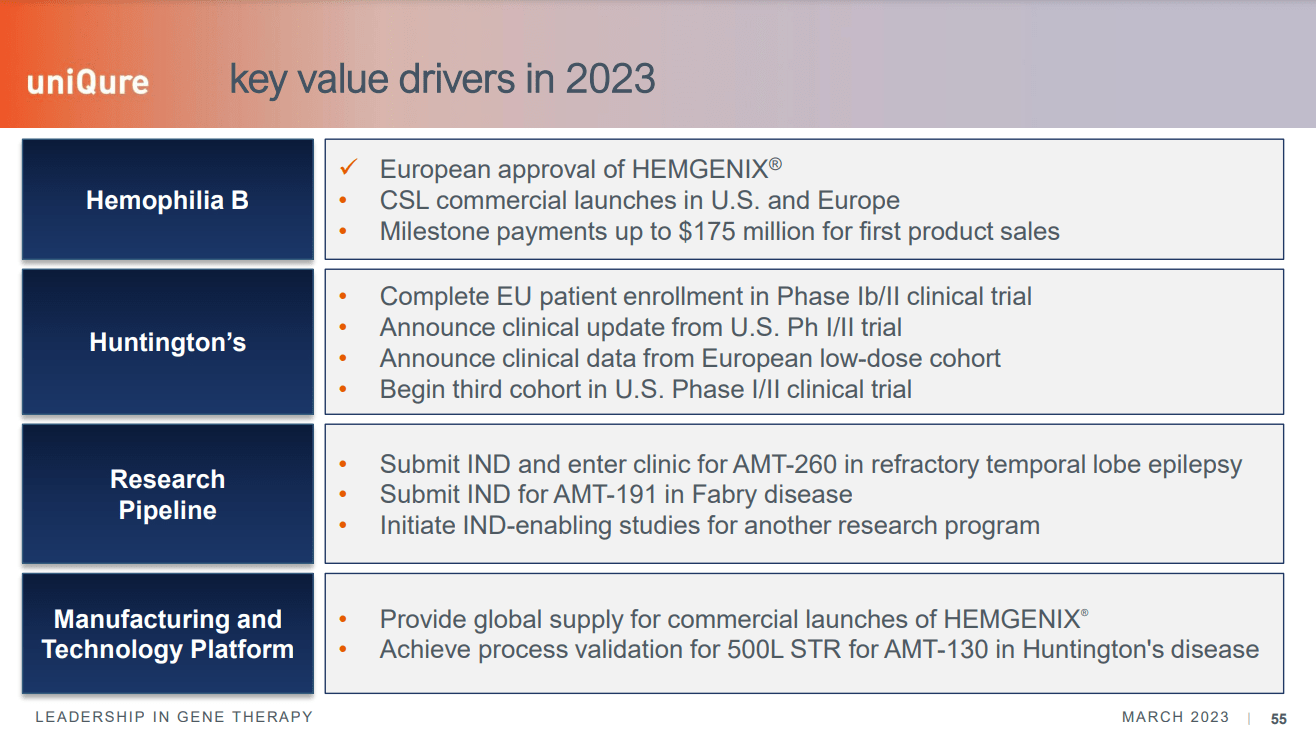

Naturally, this begs the question of what are the next potential catalysts which can unlock the value in this stock. uniQure has listed a few key value drivers in 2023, which are shown below.

uniQure Corporate Presentation, March 2023

{kind=link}

In my view, the critical ones that can serve as a catalyst to unlock this value are:

- Commercial launch of HEMGENIX in US and Europe.

- uniQure receiving major milestone payments tied the CSL Behring contract.

- Promising initial results from the clinical trials in the Huntington's disease treatment (AMT-130 program).

- Potential acquisition bid - I think uniQure is a good target with its pipeline of products and especially with the cash flows secured from the AMT-061 approval.

Risks

As with investing in any young pre-revenue company, there are major risks in investing in uniQure. For one, the above-mentioned catalysts may not get realized or could fail to move the price materially. Secondly, commercialization efforts on CSL Behring's part to bring HEMGENIX to market may not succeed or suffer from delays and/or lower than anticipated sales. Any of these circumstances would put the cash flows for uniQure at risk. To counter this risk, uniQure recently announced the sale of lower tiered royalty interest for $375MM in cash. This provides the company enough capital to survive until 2026+ while still retaining rights to the $1.3B in future milestone payments plus some royalties tied to HEMGENIX sales. Finally, any delay or negative results from the AMT-130 trials or any of the subsequent trials could have a material impact on its value.

Conclusion

uniQure has crossed the critical milestones of securing FDA and EMA approvals for its AMT-061 treatment. CSL Behring is now on the path to commercialize this treatment in the US and EU. However, it seems that the market is yet to recognize the valuation implication of these approvals with the stock being range bound. When the market recognizes and corrects its mistake, the patient investor could be rewarded with a potential doubling of the stock price in my view.

For further details see:

Market Is Still Not Pricing In The FDA And EU EMA Approvals For uniQure