TW - MarketAxess: 4 Reasons Why I Would Buy The Dip

2023-12-13 07:49:40 ET

Summary

- MarketAxess Holdings shares have fallen sharply but have still delivered a total return of 1,700% since going public in 2004.

- MKTX is a high quality recession-resilient business that deserves to trade at a premium valuation.

- The company is poised to benefit from a continued shift of credit trading onto electronic platforms.

- MKTX is currently trading at an attractive valuation vs. peers and on a standalone basis.

- I am initiating coverage of MKTX stock with a buy rating.

Shares of MarketAxess Holdings ( MKTX ) have fallen sharply and have delivered a total return of -50.3% since hitting an all-time high on December 22, 2020.

Despite this recent drop, MKTX has still delivered a total return of 1,700% since becoming a public company in 2004. Comparably, the S&P 500 has delivered a total return of 467%.

There are four reasons why I believe investors should consider buying the recent dip:

1. MKTX operates a high quality recession resilient business with a wide moat

2. The secular growth story of electronic corporate bond trading has a long way to run

3. The valuation picture has improved considerably and MKTX is now reasonably priced

4. The company is an attractive acquisition target for a number of larger players

1. High quality recession resilient business with a wide moat

MKTX is a leading operator of electronic trading platforms. The company offers trading solutions for U.S. Treasuries, EU Gov't Bonds, Municipal Bonds, Leveraged Loans, ETFs, Eurobonds, Emerging Markets Bonds, U.S. High-Yield Bonds, and U.S. Investment Grade Bonds.

Trading commissions account for 87.4% of total revenue while information services and post-trade services account for 6.8% and 5.7% of revenue respectively.

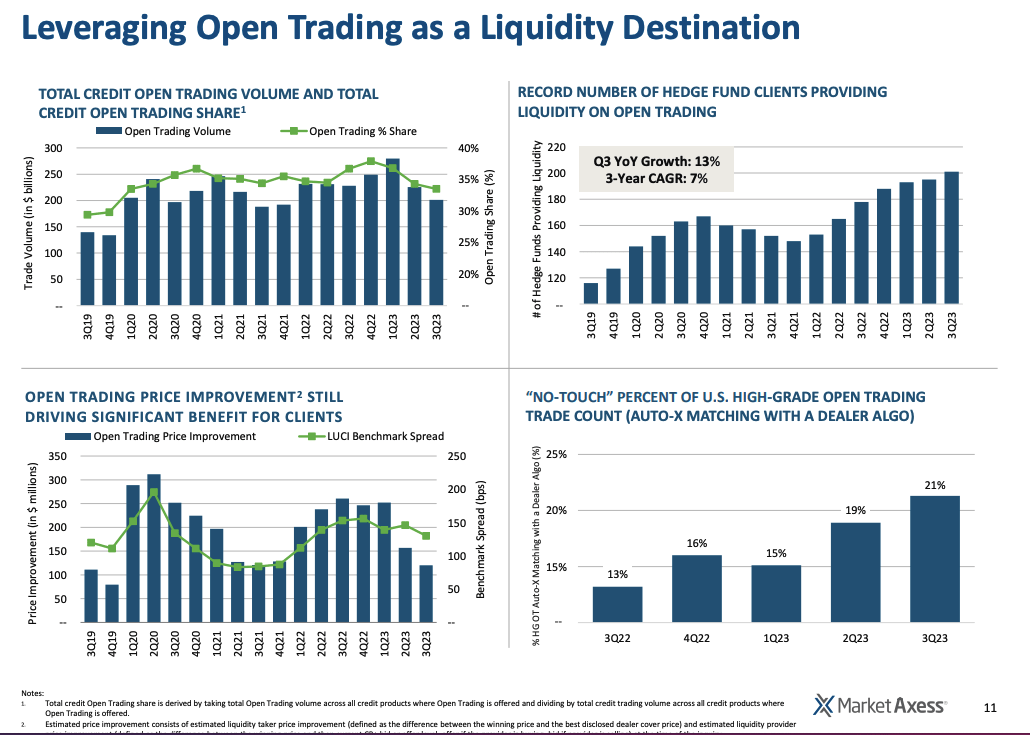

MKTX is strongest in credit trading. Trading related to credit products accounts for ~96.5% of commission revenue. Within credit trading, MKTX stands out as a strong player in the all-to-all trading ("Open Trading") electronic market. Open Trading allows institutional investors such as hedge funds and asset management firms to trade directly with each other which eliminates the need to trade with broker dealers as a middle man. ~91% of credit volume executed on MKTX platforms is executed by institutional clients with the remaining ~9% executed between dealers.

While the electronic trading business can experience some volatility over the short-term due fluctuations in trading volume, the business is fairly stable as can be seen in MKTX's consistent ability to generate EPS growth. Furthermore, the lack of cyclicality can been seen in MKTX's relatively low average 3yr trailing historical beta of 0.55 over the past 10 years.

Despite competition from other players such as Tradeweb ( TW ), Bloomberg, Intercontinental Exchange ( ICE ) and others, MKTX has been able to generate high and stable profit margins. The reason for this is that MKTX has a competitive advantage over all other players in the electronic credit trading market due to its scale. Thus, MKTX enjoys a relatively wide moat.

As the leading electronic credit trading platform MKTX is able to offer deeper markets than competitors and thus drive more trading to its platform which results in pricing power. Evidence of this competitive edge can be seen in the very high and stable level of MKTX profit margins.

{kind=link}

2. The secular growth story of electronic corporate bond trading has a long way to go

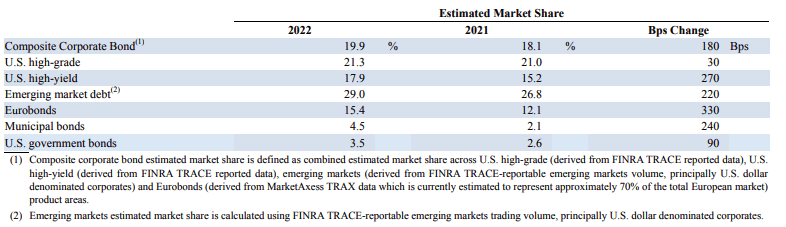

Despite recent growth in electronic trading in credit markets, the majority of trading is still done over the phone. MKTX estimates that just 40% of U.S. high-grade bonds, 30% of U.S. high-yield bonds, 15% of municipal bonds, and 10% of emerging market debt is traded electronically. Comparably, 65% of U.S. government bonds are electronically traded.

In addition to growth of electronic trading more broadly, MKTX is also poised to an even higher growth potential electronic trading in the Open Trading space.

As the leader in electronic credit trading MKTX is well positioned to benefit from the secular shift towards electronic trading. Over the past 10 years, MKTX has grown EPS at a 12.9% CAGR and I believe this level of growth can continue over the next 10 years.

Current consensus earnings estimates call for EPS growth of 13.8%, 14.2%, 13% and 10.9% for FY's 2024-2027. I believe that MKTX will be able to meet these lofty expectations.

{kind=link}

3. The valuation picture has improved considerably

MKTX is a highly valued stock with a forward P/E ratio of 34.7x. However, this multiple represents a substantially more attractive valuation than has been the case recently.

In early 2021, MKTX had traded at more than 75x forward earnings. While the business experienced a boom due to covid-19, MKTX's closest peer TW never traded at anywhere close to that valuation and was trading in the mid 30s at the time.

Additionally, it is worth pointing out that MKTX has $420.5 million of cash on its balance sheet and no debt. Thus, after back out cash MKTX is trading at a forward P/E ratio of ~33.3x.

Currently, MKTX is actually trading at a modest discount to TW. While both companies are expected to grow earnings by low double digits over the next few years, I believe MKTX is better positioned to benefit from the secular shift to electronic trading in credit as credit trading is MKTX's largest business while it is a much smaller part of TW's total business which is more driven by U.S. Treasury trading.

MKTX is also trading at a much more attractive valuation relative to other more mature exchanges such as CME.

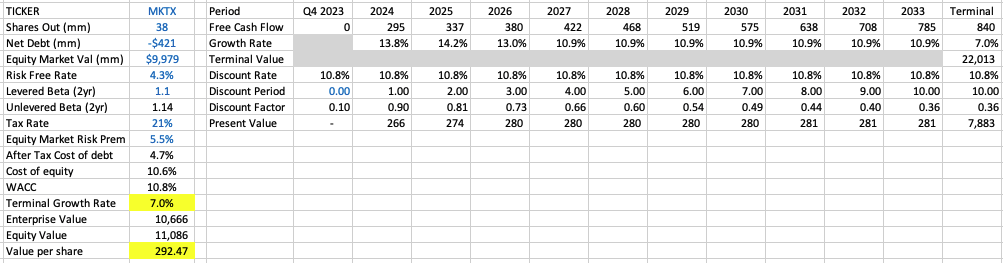

Based on a DCF valuation, I find the intrinsic value per MKTX is $292 per share. Key assumptions include a levered beta of 1.1, free cash flow growth rates in line with consensus EPS growth rates through 2027, a 10.9% free cash flow growth rate for 2027-2033, and a terminal cash flow growth rate of 7%.

While 7% is generally a relatively high terminal growth rate, I believe this is something that MKTX will be able to achieve given its leading position in the electronic credit trading business and long-term tailwinds from new issuance and increasing trading volume. Additionally, the levered beta of 1.1 is based on the most recent trailing 2 year period. Historically, MKTX has exhibited a much lower beta. When using a levered beta of 0.93 (the realized beta over the past 5 years) the fair value of the company increases to $398 per share. Thus, I view this DCF valuation as somewhat conservative as the beta estimate is toward the higher end of what I perceive the real risk of the business is.

{kind=link}

4. The company is an attractive acquisition target for a number of larger players

MKTX has an enterprise value of ~$9.5 billion based on the current trading level of the stock. This makes MKTX one of the smaller players in the trading business.

Given the company's leading position in the electronic credit trading space and potential growth in that market I believe MKTX would make a highly attractive takeover target for a number of players including Bloomberg, Tradeweb, CME, ICE, or LSE Group. All of these players are larger players in the trading business and could easily integrate MKTX's offering alongside their own to become a more desirable partner for asset management firms, bank trading desks, hedge funds, and other trading firms.

I believe any acquisition would be done at a substantial premium to the current share price.

Risks To Consider

One risk to consider is that competition from Tradeweb in the credit trading space leads to an erosion of MKTX's market leading position. Currently Tradeweb has 16.8% market share and 6.7% market share in fully electronic U.S. high-grade and U.S. high-yield trading.

However, the market appears large enough for both players to play as both companies have maintained high profit margins. Thus, the electronic credit trading business may evolve into an oligopoly structure. That said, investors should continue to monitor market share and profit margins closely to ensure that this market is large enough for both MKTX and Tradeweb to play in.

Conclusion

MKTX is a high growth company with a strong history of delivering long-term shareholder results. However, MKTX has experienced recent weakness which was driven by multiple contraction following a period of extreme overvaluation which coincided with a boom in business related to the covid-19 pandemic.

The long-term secular growth story which has allowed MKTX to deliver strong growth historically remains in place and the company is poised to experience double digits EPS growth for the foreseeable future.

I find MKTX to be attractively valued compared to peers such as Tradeweb. Additionally, I believe MKTX is trading below its intrinsic valuation.

MKTX has an attractive market position and could be an acquisition target for a larger player.

For these reasons, I rate MKTX a buy but would consider downgrading my rating if the valuation were to become substantially less attractive.

For further details see:

MarketAxess: 4 Reasons Why I Would Buy The Dip