TW - MarketAxess Is Making Market Share Gains But Is Now Overvalued

Summary

- MarketAxess delivered solid Q4 2022 results, showing market share gains.

- The business is performing well, and things look positive for 2023. There is a lot to like about the company.

- That said, the valuation has become extremely stretched. We believe shares are now seriously overvalued.

One of the most attractive types of businesses are platform businesses with network effects. They tend to have winner-take-most characteristics where one or a few players earn most of the profits, have outstanding financials, and dominate the industry. In the case of electronic bond trading, it is MarketAxess ( MKTX ) and Tradeweb ( TW ) that have the strongest competitive moats. We wrote a previous article where we compare the two, and we also go into more detail as to why they have such strong competitive advantages. Unsurprisingly, investors are willing to pay high multiples for these types of businesses, and electronic bond trading has the added tailwind that there is still a lot of bond trading done by phone that can be brought to the electronic trading platforms, which should help keep high growth rates for still some time. That said, the valuation of both companies is starting to get quite stretched, and MarketAxess in particular now looks overvalued.

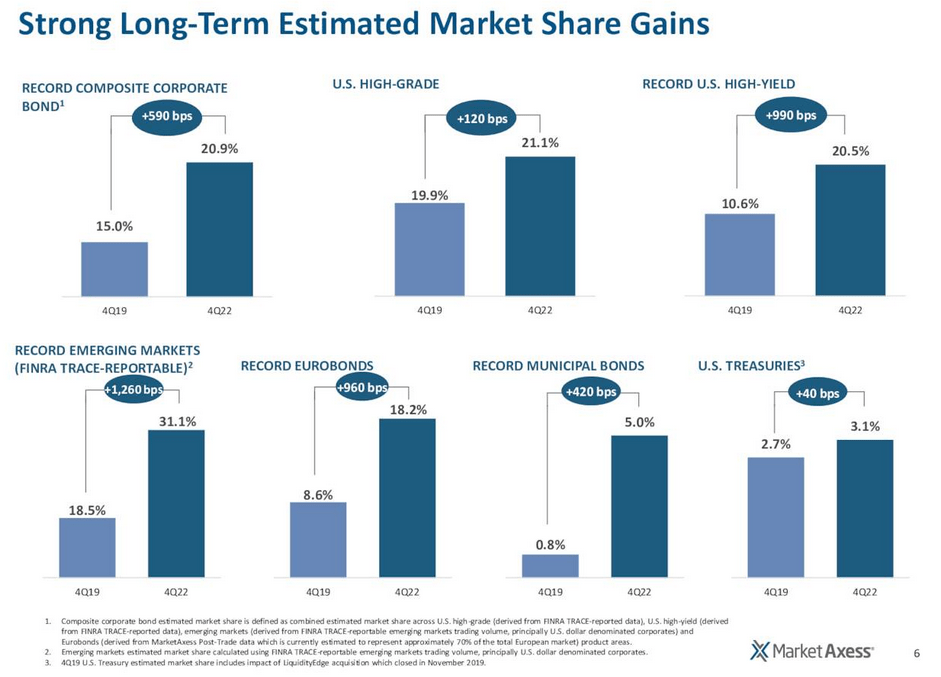

MarketAxess reported very decent numbers for its fourth quarter 2022 results, delivering the third consecutive quarter of market share gains across nearly all their product areas. Revenue grew 8% to $178 million, EBITDA was 10% higher, and EPS grew 15% . These results include the negative impact of a 9% decline in total credit fee capture, mainly the result of the lower duration of US high-grade bonds traded over the platform. Adding to the good news, the company delivered record estimated market share in high-yield in municipals, record share in Eurobonds, and accelerating share gains of almost 300 basis points in emerging markets.

MarketAxess Investor Presentation

{kind=link}

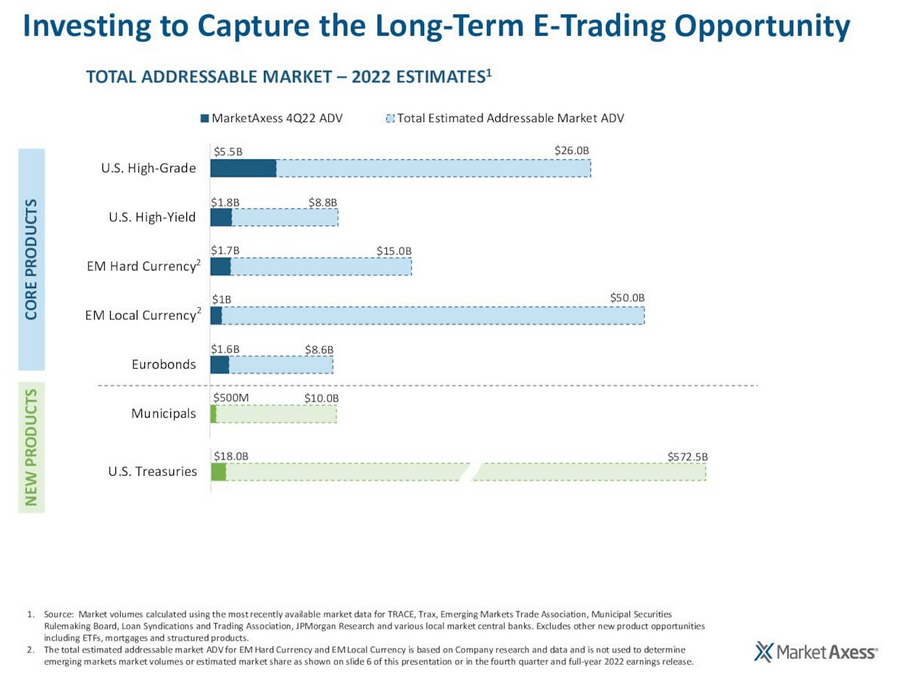

The company has ample room to continue growing, as it has only captured a small percentage of the TAM in its different product categories. The company is therefore ramping up investments to try to capture this opportunity, which will impact profitability in the short/medium term, but is expected to pay off in the long-term.

MarketAxess Investor Presentation

{kind=link}

MarketAxess ended the quarter with cash and investments of $515 million and no outstanding debt. During the earnings call there was some hinting that the company could leverage its strong balance sheet for some acquisitions, saying that there are a number of FinTech providers in the market that will start facing capital challenges.

With fixed-income markets recovering, and the company making market share gains, it looks well positioned for growth in 2023. That said, while there are reasons to be optimistic about the company, we believe shares are now seriously overvalued.

Automation Tools

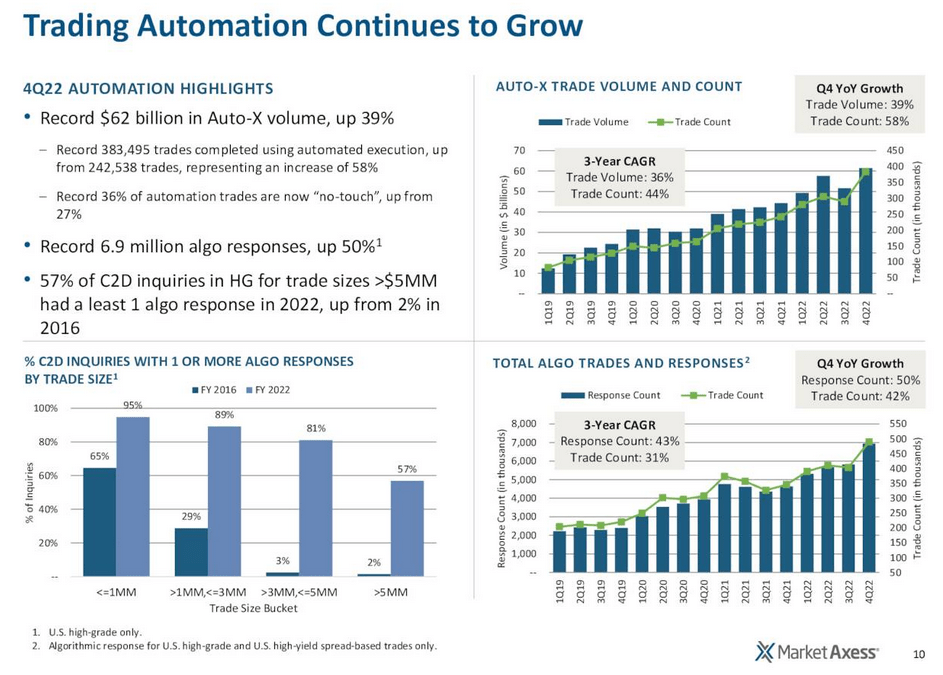

One area where the company is delivering incredible growth is in automated trading. We believe these technology developments further strengthen the company's competitive moat, and they also improve the efficiency of the platform and enable it to offer more attractive pricing to its customers. The slide below highlights the enormous growth the company is seeing in automated trading.

MarketAxess Investor Presentation

{kind=link}

During the earnings call CFO Chris Gerosa touched on the subject, saying that automation now accounts for ~20% of the total trades on their platform. He also described some more advanced technology they are currently working on:

Automation continues to be a driver of activity on the platform. It had nothing but records across the Board in Q4, record volume of $62 billion in our Auto-X solution and then overall trades on the platform was automation accounted for 20% of total trades on our platform. So we -- not only did we see heightened growth in Q4, but overall the year of 2022 sort of record volumes of total of $220 billion in automated volumes.

As we look forward in 2023, we continue to hear from our largest clients around their cost controls that they are facing, particularly given the AUM performance of 2022. So they are facing bigger and bigger tech challenges and looking to us to help outsource some of those challenges in workflow solutions like our automation tools. As I mentioned in our open remarks, we are launching in the first half of this year what we're calling Adaptive Auto-X, which is a true client algorithm which adapts to market conditions as it trades. So it's a unique solution that's being rolled out for the first time in credit trading in the U.S.

Growth

Revenue growth has yet to return to the historical ~15% growth the company had been delivering. Given the recovery in fixed-income markets and the market share gains, we believe growth in 2023 should be better than in 2022, but it remains to be seen if the company can consistently deliver double digit revenue growth again.

Guidance

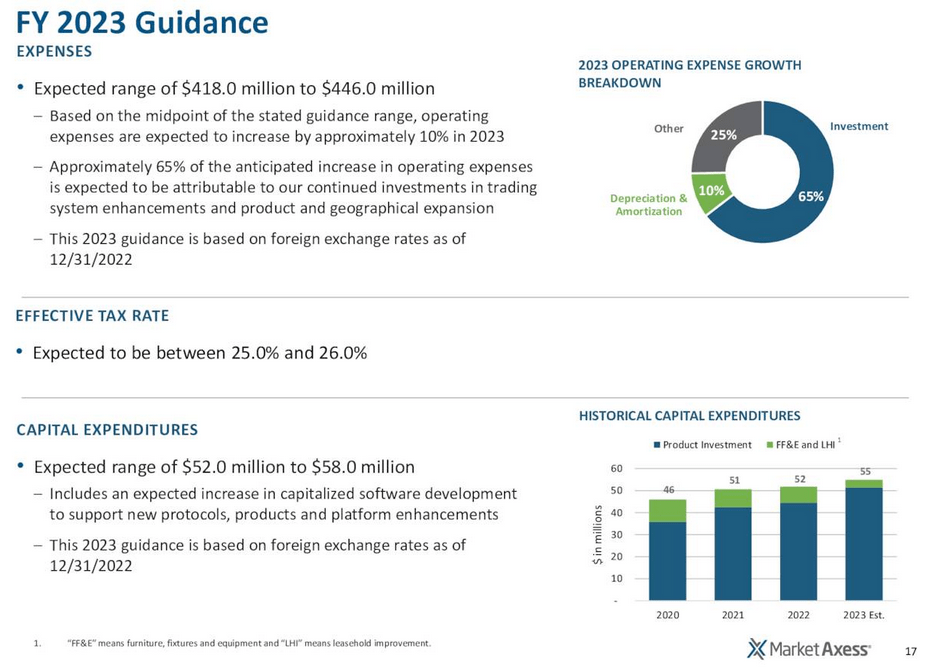

The company is expected to increase operating expenses by ~10% in 2023. Investors should therefore have relatively low expectations about earnings growth for fiscal year 2023, as the company is not likely to experience much operating leverage, if any. Still, we believe the company is doing the right thing trying to capture as much of the opportunity as it possible can as the world continues to transition to electronic trading platforms.

MarketAxess Investor Presentation

{kind=link}

Valuation

Despite growth currently running below historical averages, shares are trading above their ten year averages on most valuation multiples. For example, the EV/Revenues multiple is ~18.8x, higher than the ~17.4x ten year average, and very demanding on absolute terms.

EV/EBITDA is also quite high at ~33.5x, and above the ten year average of ~31x. Shares were starting to look reasonable at close to a 20x multiple, but they quickly rebounded.

Similarly the price/earnings ratio is extremely high at ~56x, and above the ten year average of ~49x. While this is a quality business with a very strong competitive moat, we don't believe the level of growth merits a multiple this high.

The price/free cash flow is very close to the price/earnings multiple, also above 50x, and very close to the ten year average.

Based on optimistic EPS estimates, the fair value we calculate is only ~$222 per share. According to our net present value calculation shares are therefore overvalued by ~63% when using a 10% discount rate.

| EPS |

| Discounted @ 10% |

| FY 23E |

| 7.74 |

| 7.04 |

| FY 24E |

| 8.85 |

| 6.40 |

| FY 25E |

| 10.32 |

| 5.82 |

| FY 26E |

| 12.00 |

| 6.04 |

| FY 27E |

| 13.80 |

| 6.41 |

| FY 28E |

| 15.87 |

| 6.77 |

| FY 29E |

| 18.25 |

| 7.08 |

| FY 30E |

| 20.99 |

| 7.40 |

| FY 31E |

| 24.14 |

| 7.74 |

| FY 32E |

| 27.76 |

| 8.09 |

| FY 33E |

| 31.92 |

| 8.46 |

| Terminal Value @ 3% terminal growth |

| 455.71 |

| 145.20 |

| NPV |

| $222.45 |

Risks

Given that the company is delivering some market share gains, has strong competitive advantages, and a very solid balance sheet, we believe the biggest risk for investors is the extremely stretched valuation.

Conclusion

MarketAxess delivered positive fourth quarter results with market share gains, and revenue and EPS growth. Together with the recovery in fixed-income markets, this sets up MarketAxess to deliver solid growth in 2023. While this sounds great, the problem we see is an extremely stretched valuation that is difficult to justify.

For further details see:

MarketAxess Is Making Market Share Gains, But Is Now Overvalued