MKFG - Markforged: Canary In The Additive Manufacturing Coalmine

2023-10-26 03:59:47 ET

Summary

- Markforged preannounced weak Q3 earnings, resulting in a significant decline in share price.

- Soft results have been blamed on macro uncertainty and the increase in the cost of capital.

- While new products have the potential to support growth, an extended period of stagnant revenue and large losses has undermined investor confidence.

- If demand weakness continues into 2024, Markforged may be forced to raise capital on unfavorable terms.

Markforged ( MKFG ) preannounced weak third quarter earnings on the 23 rd of October, resulting in a dramatic share price decline. On the back of this, William Blair downgraded Markforged’s shares to Market Perform, stating that a continued lack of growth and profitability have created dilution risk.

I had previously suggested that Markforged's prospects were questionable, and that M&A speculation may have led the stock to become overvalued. M&A activity in the additive manufacturing industry has died down for now, and Markforged's stock has declined over 60% since my last article. Markforged could still be an acquisition target at some point, with Nano Dimension ( NNDM ) in particular providing positive commentary on Markforged's business, but any offer may not be appealing to existing investors from a valuation standpoint.

While there are still questions about the breadth of appeal of Markforged's distributed manufacturing approach, recent weakness is probably the result of a soft demand environment rather than company-specific issues. After this week's price decline, Markforged's stock is now priced more in line with comparable companies, but poor investor sentiment towards the additive manufacturing industry may drag the stock lower.

Market

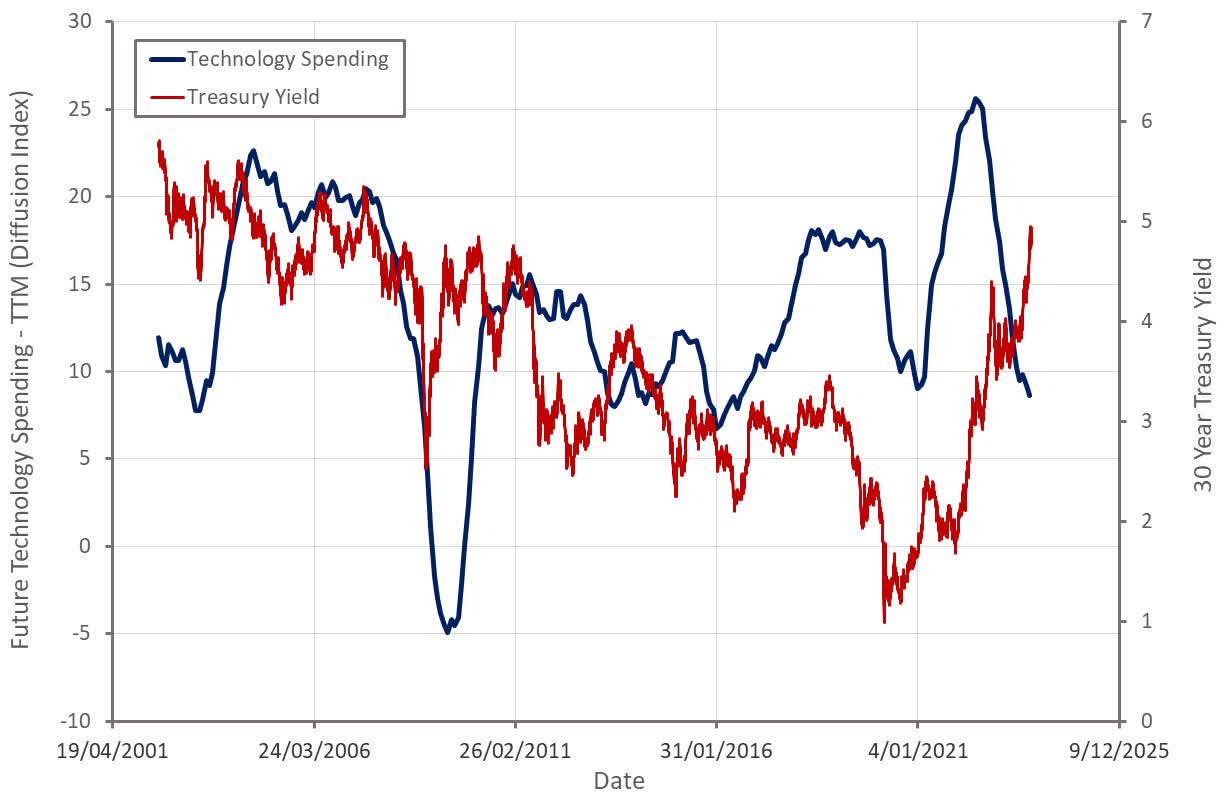

The rise in the cost of capital over the past 12 months is restricting capital investments by potential customers. Based on manufacturing survey data and company results, this weakness appears to be widespread, although additive manufacturing may have been disproportionately impacted due to the more experimental nature of the technology and the fact that it is currently used more in design and prototyping than production.

Figure 1: Treasury Yields and Manufacturing Survey Data (source: Created by author using data from The Federal Reserve)

{kind=link}

Markforged noted on its second quarter earnings call that it was having difficulty closing deals but was confident in its longer-term growth projections. This confidence was supported by the fact that the company’s pipeline increased materially YoY in the second quarter.

Based on this commentary, Markforged appears to have been dramatically caught out by macro weakness in the third quarter. The company recently preannounced earnings, with revenue coming in roughly 20% below guidance. Macroeconomic headwinds reportedly accelerated towards the end of the third quarter, leading to delays in closing deals. Weakness is also now expected to continue through the remainder of the year.

Markforged

In a terrible demand environment, the only real glimmer of hope for Markforged investors is the company's slate of new platforms and capabilities. An example of this is the FX20 composite printer, which was announced in 2021 and has been shipping since 2022. The FX20 enables larger builds at higher speeds and is reportedly generating interest amongst customers within markets like aerospace and automotive. The PX100 metal binder jet printer is also adding to Markforged’s order pipeline. Shipping of the PX100 is only expected to commence in the second half of 2023 and it is not expected to materially contribute to revenue until 2024. New products will also be introduced in coming quarters and are expected to support growth in 2024, although there is currently little information available about this.

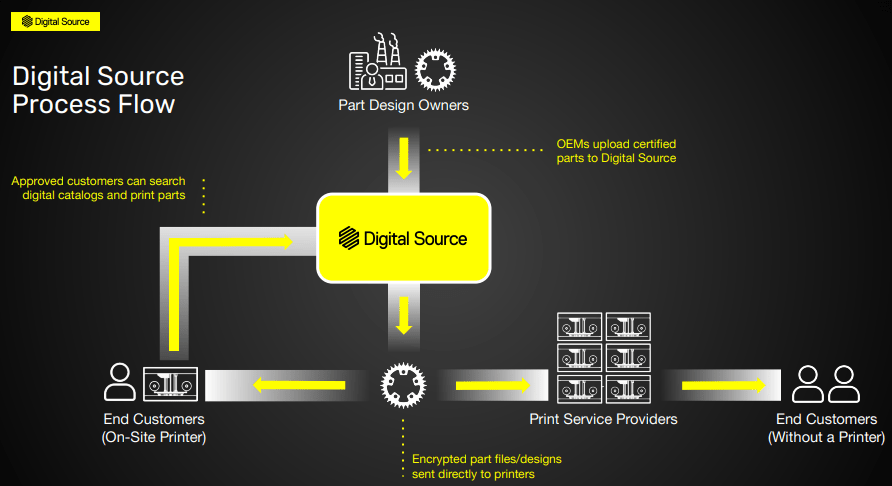

Markforged is also adding to its software offerings, recently introducing the Digital Source platform. Given Markforged’s focus on distributed manufacturing, the Digital Source platform is an important development for the business. Additive manufacturing can reduce inventory levels and improve supply chain resilience through on-demand printing at the point of use. This concept hasn't really taken off though, in part because of quality concerns and because this approach jeopardizes the IP of OEMs.

Digital Source enables the licensing and 3D printing of manufacturer-certified parts in a manner that protects intellectual property. Vendors are able to upload digital part designs and printer process requirements, which allow the production of manufacturer-certified parts. Customers can license the right to print parts onsite but only receive encrypted print instructions, which protects designs. Markforged stands to benefit from increased demand for its products and a high-margin pay-per-print revenue stream, but adoption of this technology may be limited in the current environment.

Figure 2: Digital Source Process Flow (source: Markforged)

{kind=link}

Financial Analysis

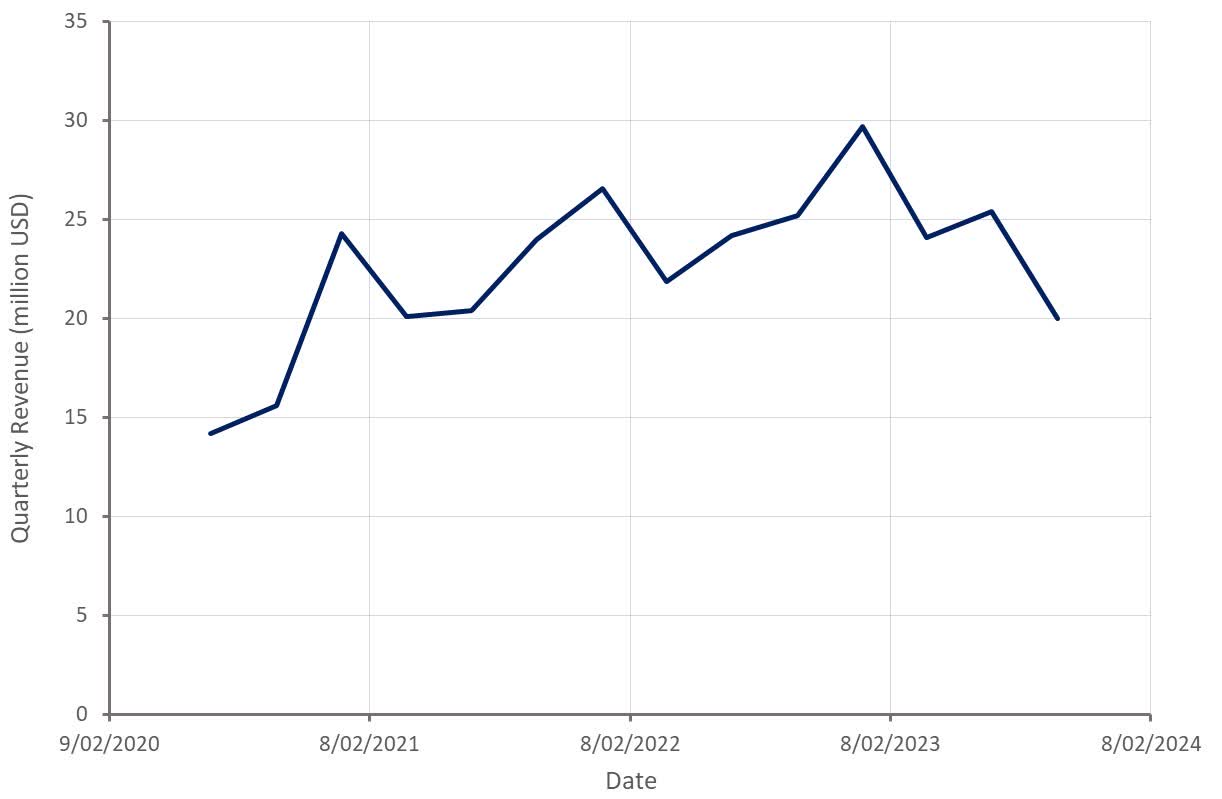

Markforged’s revenue in the third quarter was only 20 million USD , declining roughly 21% YoY and falling well short of management’s expectation that Q3 revenue would be broadly in line with Q2 . Based on a deterioration in the macro environment, Markforged has reduced full-year guidance from 101-110 million USD to 90-95 million USD. At the midpoint, this implies that fourth quarter revenue will be down approximately 23% YoY.

While Markforged is operating in a tough demand environment, the lack of growth over the past 3 years is likely a growing concern for investors. Growth is needed for the company to reach breakeven and would help indicate that new products are gaining traction amongst customers.

Figure 3: Markforged Revenue (source: Created by author using data from Markforged)

{kind=link}

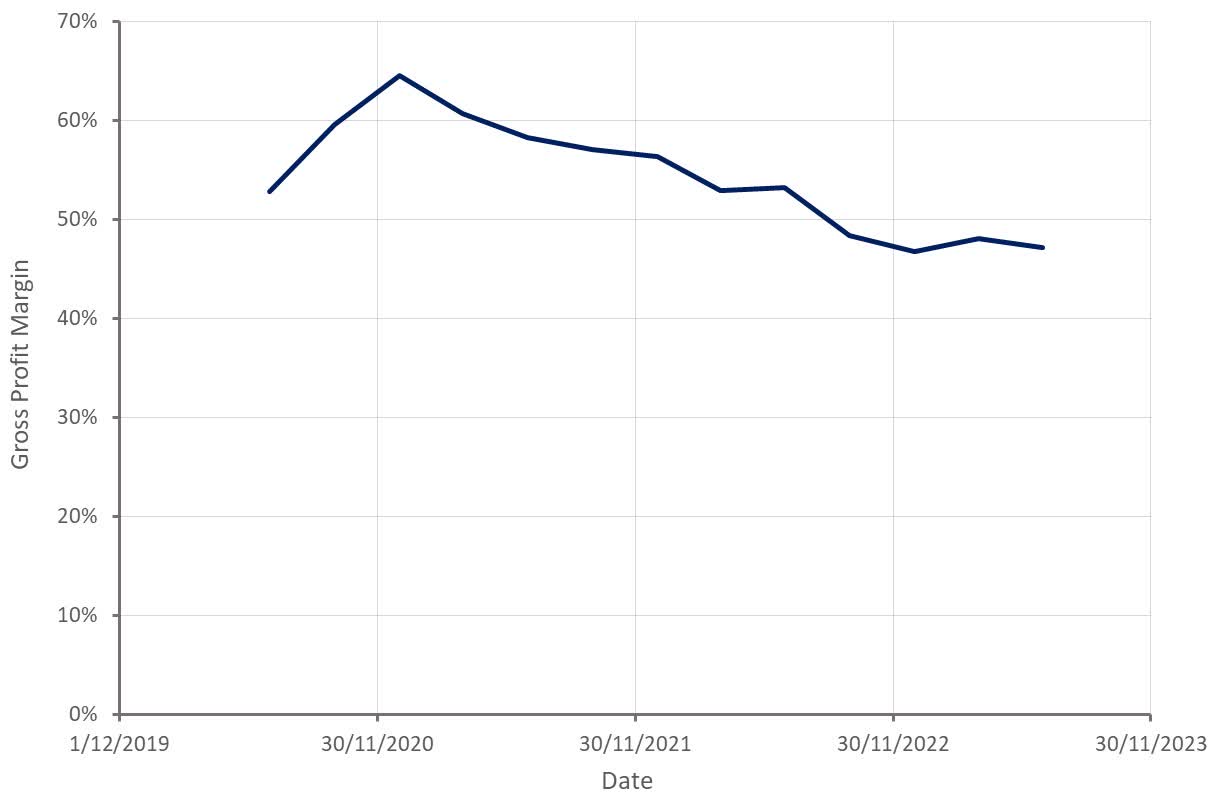

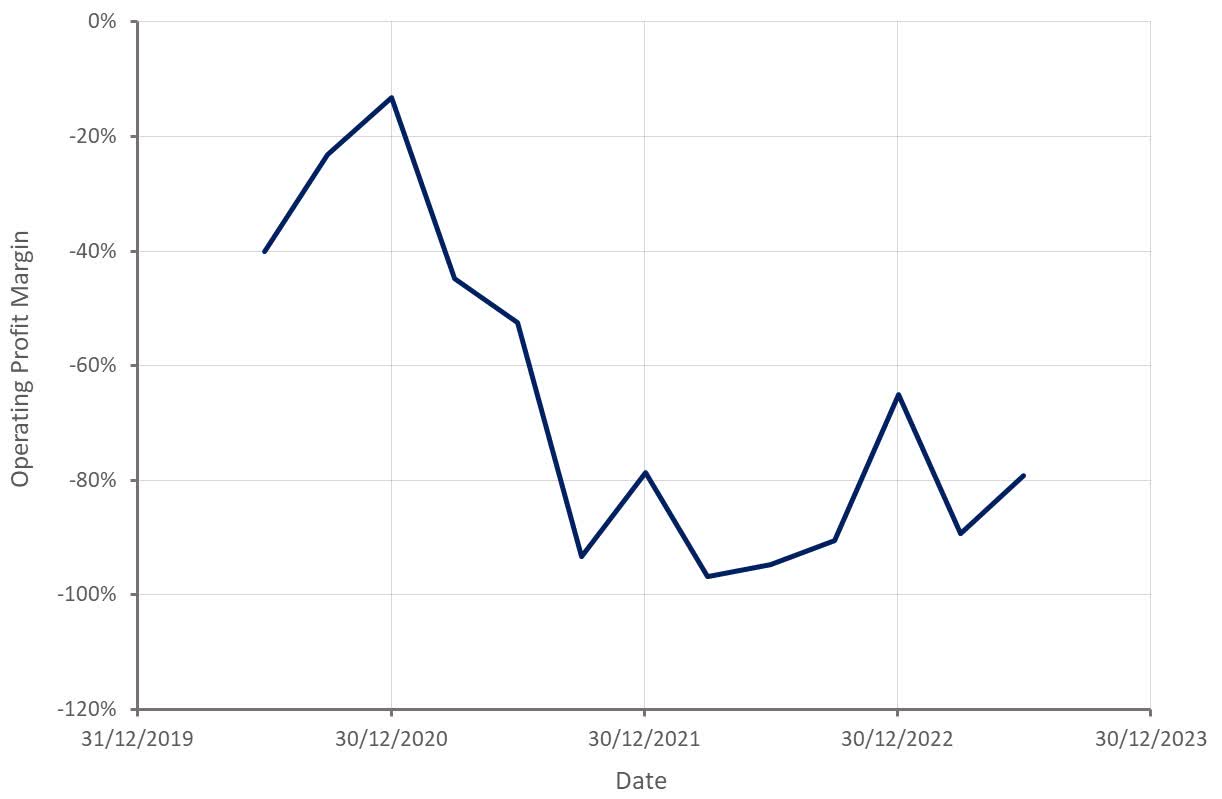

Markforged’s gross profit margin has been under pressure in recent quarters due to the production ramp of the FX20 . Gross profit margins appear to have bottomed though and Markforged expects that margins will gradually expand to historical levels (50+ percent) in 2024. Given unexpected weakness in the third quarter, gross profit margins could still remain under pressure in the near term.

Figure 4: Markforged Gross Profit Margin (source: Created by author using data from Markforged)

{kind=link}

Markforged’s non-GAAP operating expenses were down 11% YoY in the second quarter due to an increased focus on costs. Net cash used in operating activities in the first half of 2023 also decreased by 10.9 million USD YoY. Cash utilization was expected to continue declining in coming quarters but weak third quarter results probably mean that cash burn will remain elevated. In response to recent headwinds, Markforged is accelerating its cost reduction efforts to try and bring its cost base into line with anticipated revenues.

On the second quarter earnings call, Markforged reaffirmed an expectation of reaching operating profit breakeven by the end of 2024 and achieving positive cash flows in 2025. The feasibility of this will be heavily dependent on the company's future growth path but it now seems reasonable to expect this timeline to be pushed out substantially.

Markforged ended the third quarter with 126 million USD of cash, cash equivalents and short-term investment. Liquidity therefore won't be a problem for another 12-18 months, but there is now a serious risk that the company will have to try and raise capital under extremely unfavorable conditions.

Figure 5: Markforged Operating Profit Margin (source: Created by author using data from Markforged)

{kind=link}

Conclusion

In recent months there has been a growing consensus that the global economy would reaccelerate in the second half of 2023. While there are pockets of strength, conditions have continued to deteriorate for many companies, leading to a discrepancy between expectations and reality. Markforged is just one example of this.

The manufacturing sector remains under pressure, with macro uncertainty and the rapid rise in interest rates reducing the willingness of manufacturing companies to invest in their businesses. This situation is likely to persist for some time, and it is optimistic to think it will be resolved simply through a reduction in rates alongside strong economic conditions.

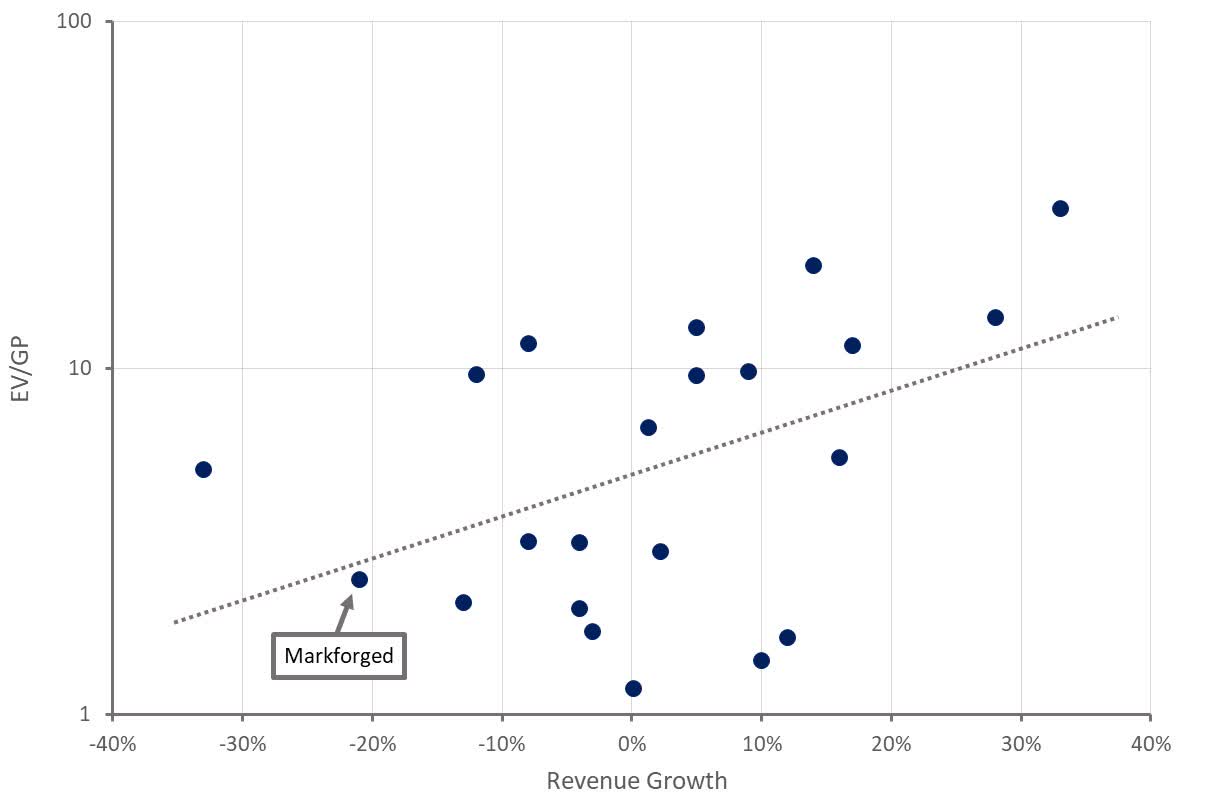

The recent fall of Markforged's share price brings the company's valuation more into line with comparable companies but consideration should also be given to the elevated risk of dilution. Particularly if demand remains weak for an extended period of time. In addition, if the third quarter results of peer additive manufacturing companies mirror Markforged's, valuations are likely to fall across the sector.

Figure 6: Markforged Relative Valuation (source: Created by author using data from Markforged)

{kind=link}

For further details see:

Markforged: Canary In The Additive Manufacturing Coalmine