MKFG - Markforged: Takeover Speculation Creates An Interesting Catalyst

Summary

- Markforged saw its shares spike in response to news that the company could be preparing to be taken over.

- The driver behind this is a filing made by management, and it could result in attractive upside if it comes to fruition.

- But fundamentals are problematic and make MKFG stock a rather risky prospect at the moment.

Although it's no longer thought of as the panacea that it once was around a decade ago, the additive manufacturing space, also referred to as the 3D printing market, still has a place in the broader economy. Unfortunately, because of how the industry has developed, many of the players in the space generate rather significant net losses and cash outflows. But this does not mean that they aren't growing. For a larger firm or a strategic investor looking to get into additive manufacturing, some of the smaller players in the market might make for attractive takeover targets. And based on recent developments , perhaps the most likely takeover candidate at this time is Markforged Holding Corporation ( MKFG ). Growth achieved by the company has been generally positive, but profits and cash flows are problematic. The recent development that came courtesy of management suggests that there might be some opportunity here. And frankly, if it weren't for that development, I would rate the company far more harshly than I have ultimately opted to. But based on all the data available, I believe that a 'hold' rating is appropriate at this time.

Markforged - A niche 3D printing firm

At its core, Markforged operates as an additive manufacturing enterprise that helps to provide engineers, designers, and manufacturing professionals with the products and services needed for their own 3D printing needs. The company does this through a platform that it developed called The Digital Forge. This platform combines 3D printers and metal and composite proprietary materials with the company's own cloud-based learning software aimed at optimizing the 3D printing process. To really understand the company, though, it would be helpful to break it up into the two core aspects that make it what it is.

First and foremost, Markforged has its own portfolio of 3D printers that include desktop printers that produce quality parts in settings where space is limited, industrial composite printers that provide more robust functionality such as the ability to use a wider variety of materials and print modes, and metal printers that can fabricate complex metal parts should customers need them. The company also provides its customers with industrial-grade materials for the printers that they produce. Examples of these materials include carbon fiber, copper, stainless steel, Onyx, and a variety of others. The next aspect of the company involves the firm's own software. This software was developed alongside the company's first printers so that the firm could ship the printers and the software as a complete and integrated solution. But over the company's life, it has expanded its software capabilities. Examples here include design functionalities, integrated cloud part repository services, fleet management accessibility utilizing premium software subscriptions, and more.

{kind=link}

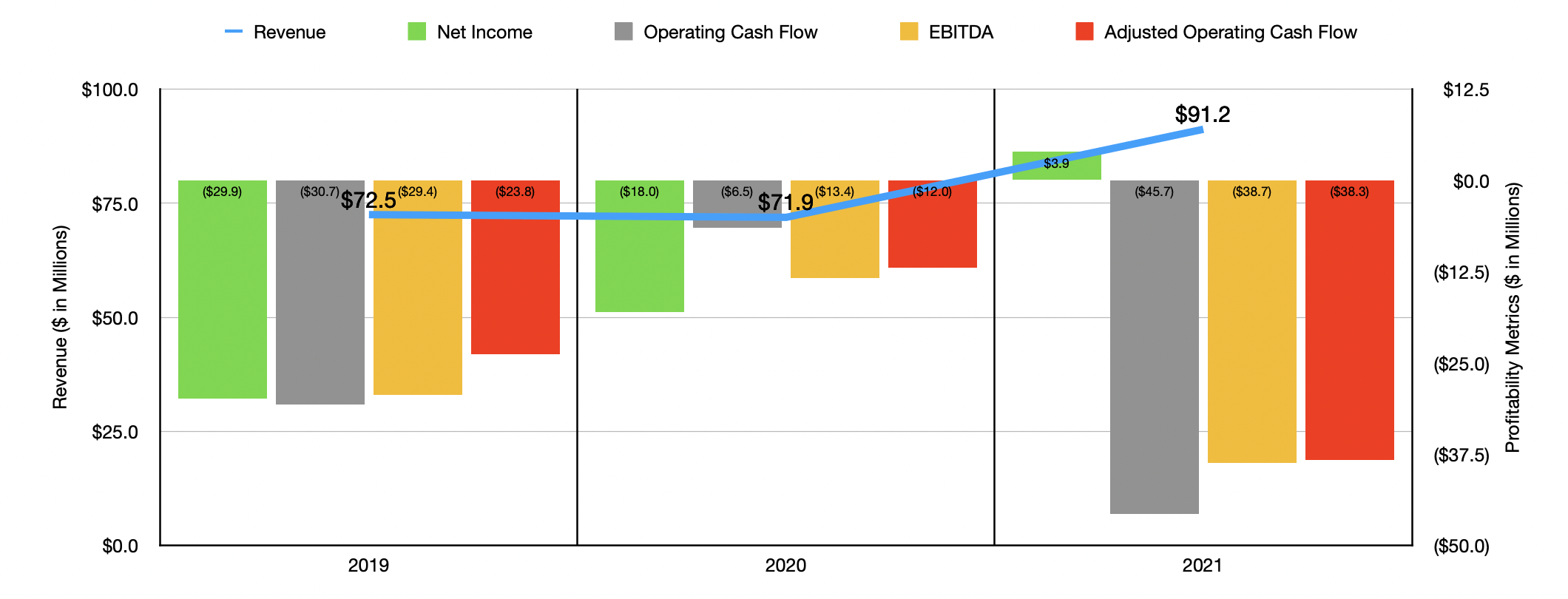

From a fundamental perspective, the past couple of years has seen some improvement for the company. But in other ways, the firm has suffered. Revenue, for instance, rose from $72.5 million in 2019 to $91.2 million in 2021. Essentially all of this increase came from 2020 to 2021, with revenue shooting up 26.8% in response to broad-based growth. Hardware sales, for instance, shot up 25%, primarily driven by more hardware units of the company's industrial composite and metal printers. Consumables revenue jumped 26% thanks to an increase in material utilization by active printers in the field, the incremental volume as a result of new printer sales, and the return of certain printers to active duty that were temporarily inactive because of the COVID-19 pandemic. And services revenue for the company jumped 58%, largely thanks to an increase in the number of hardware units sold since they have a warranty and maintenance contract attached to them. The introduction of software subscription solutions also aided in this growth.

It's great to see revenue increase. But some of the company's bottom line results have been mixed. Admittedly, net income has improved year over year, turning from a net loss of $29.9 million in 2019 to a net profit of $3.9 million in 2021. At the same time, however, operating cash flow worsened from negative $30.7 million to negative $45.7 million. If we adjust for changes in working capital, it still would have worsened, going from negative $23.8 million to negative $38.3 million. Even EBITDA has shown some signs of pain, turning from negative $29.4 million to negative $38.7 million over the three-year window covered.

{kind=link}

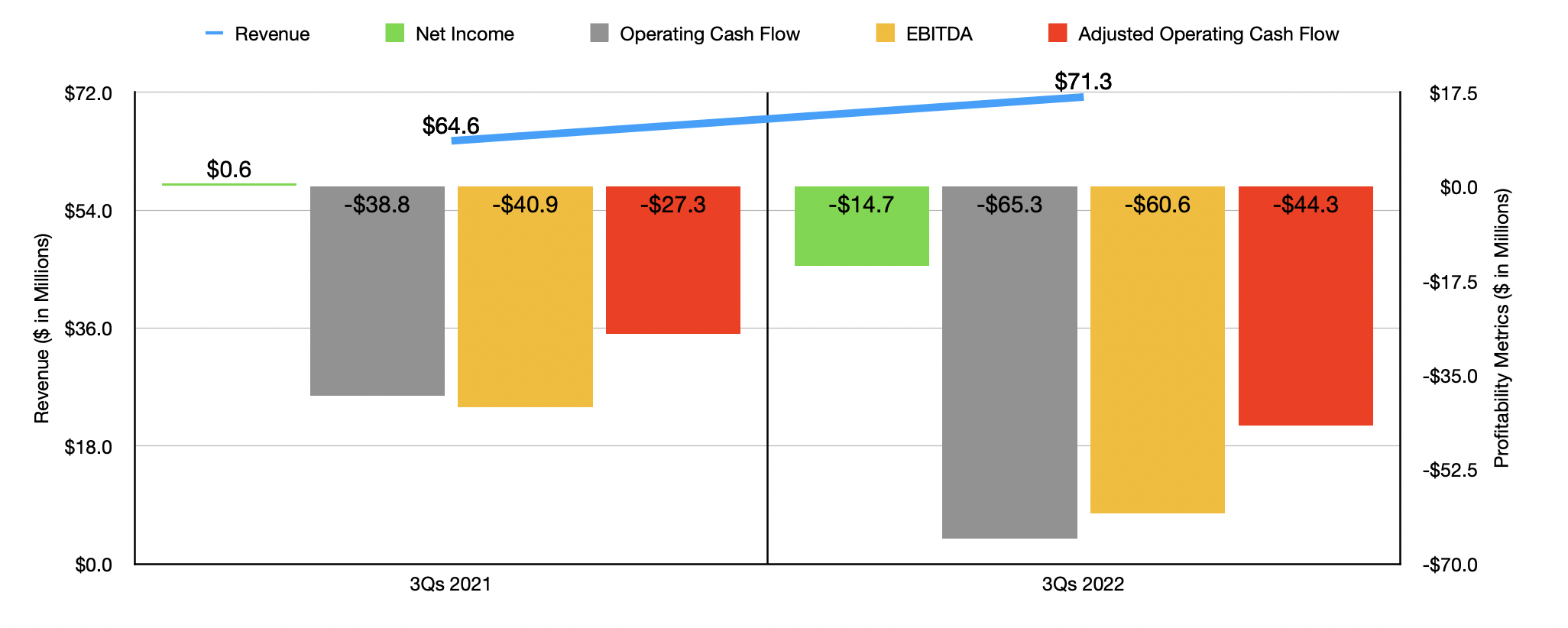

When it comes to the 2022 fiscal year, results for the first nine months were also mixed. Revenue, for instance, did quite well, totaling $71.3 million. This is 10.4% higher than the $64.6 million the company generated the same time one year earlier. Services revenue was, once again, the fastest-growing part of the company. During the nine-month window covered, sales growth there was an impressive 48%. Even though this is nice to see, services still only account for roughly 8.8% of the company's sales. Consumables revenue grew a more modest but still very impressive 18%. The laggard, then, was the hardware side of the equation, with sales growth of only 4%. Seeing as how hardware sales account for 67.5% of revenue, it had a dragging effect on overall topline performance. Profitability figures suffered greatly. The company went from a net profit of $0.6 million to a net loss of $14.7 million. Operating cash flow went from negative $38.8 million to negative $65.3 million, while the adjusted figure for this went from negative $27.3 million to $44.3 million. Even EBITDA took a hit, falling from negative $40.9 million to negative $60.6 million. Despite the rise in sales, the company suffered from a decline in its gross profit margin from 59 percent to 52%. This was largely due to increased costs to procure supplies of mechanical and electronic components, as well as increases in the cost of labor for the production of the company's newest printer. Higher freight and logistics expenses, as well as a shift in product mix, also negatively impacted bottom line results.

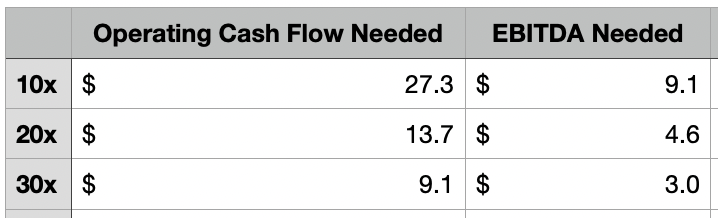

Based purely on the fundamental data, the company does not look all that exciting. Yes, sales continue to increase. But profits and cash flows are worsening. To make matters worse, you can't really value the company since all of the bottom line results are negative. To best address this then, I decided to look at three different scenarios. In each of these scenarios, I assume that the company should trade at a specific price to operating cash flow multiple and at a specific EV to EBITDA multiple in order to be at least fairly valued. For these scenarios, I picked multiples of 10, 20, and 30. As you can see in the table below, these numbers are not ridiculously out of the realm of possibility in due time. In fact, from an EBITDA perspective, it wouldn't take more than a 10% profit margin for the company to be fairly valued assuming the lowest multiplier is used. At the highest, this number shrinks considerably.

{kind=link}

Despite the rise in sales, the growing cash outflows of the company during 2022 would normally be enough for me to have a rather bearish stance on the firm. But the picture has changed to some degree in response to speculation that the company might be a buyout target. This stems not from random rumblings in the investment community, but instead is due to the fact that, last week, management filed a form with the SEC stating that it was adopting a change in policies aimed at rewarding upper management in the event of a change in control for the enterprise. Amongst other things, it includes continued benefits for the top brass, as well as the full acceleration of vesting for employees of the company. Of course, there is no guarantee that this will come to pass. But these types of filings are often made when serious discussions are happening. Such an announcement could prove to be a tremendous catalyst for shareholders.

Takeaway

From a purely fundamental perspective, I am impressed by the continued sales growth that Markforged has achieved. Having said that, bottom line results have been worrisome, particularly as of late. Even though the company has a tremendous amount of cash on hand and no debt, the material worsening of its cash flow picture would normally be enough for me to rate it a 'sell'. But given the recent filing made by management and the implications that could have on shareholders, I am myself taking a more ambitious approach to the company by rating it a 'hold', with the idea that it could offer investors an attractive upside if they are willing to accept heightened risk.

For further details see:

Markforged: Takeover Speculation Creates An Interesting Catalyst