PUMSY - Marks and Spencer Group: Too Speculative To Buy

Summary

- British retailer Marks and Spencer Group plc saw a big uptick in price recently following its Christmas trading update. While its growth is strong, its profits are wanting.

- High inflation has impacted Marks and Spencer's operating profit in the recent past, and going by the company's outlook can continue to do so, along with an expected weakness in consumer spending.

- Marks and Spencer Group's market multiples do indicate upside, but given its sensitivity to broad macro conditions and also its weak current liquidity, it's too speculative to buy.

2023 has started on a particularly good note for British retailer Marks and Spencer Group plc ( MAKSF ), whose price is up by 25% over the past month. There are both sectoral and company-specific reasons for this. In Sectorial terms, consumer stocks have reported a sharp uptick recently. Among the ones I’ve covered, British stocks like Deliveroo ( DROOF ) and Fevertree Drinks PLC ( FQVTF ) have made gains, as have German companies like Zalando ( ZLNDY ) and Puma ( PMMAF ). With the worst of inflation appearing to be behind us, there’s a possibility of better performance in the near future even in the face of an expected, shallow recession.

Strong trading update

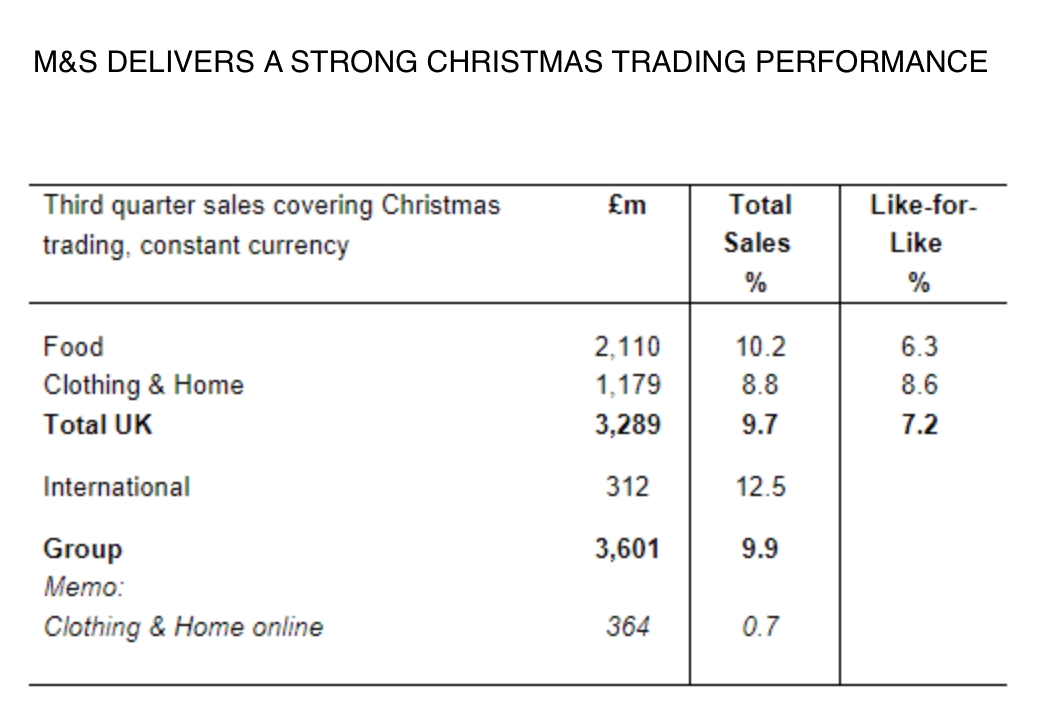

But the company has something else going for it, too, considering its recent performance . In the week from the time it released its recent Christmas trading update, its price was up almost 9%. Going by how upbeat the update was, it’s hardly surprising. Marks & Spencer ("M&S") saw a ~10% rise in sales for the 13 weeks to December 31, 2022, compared with the 13 weeks to January 1, 2022. It says that “M&S Food outperformed the market on volume and value in the critical four-week Christmas period for the second year running.”

With respect to its Clothing and Home division, the company added that its “market leadership position with its highest market share in seven years.” Research by NielsenIQ also affirms Marks and Spencer Group plc as Britain’s fastest-growing grocer .

{kind=link}

Encouraging as this is, there’s much more to unpack on the M&S story, which isn’t all positive. To start with, let’s stay with the trading update for another moment. A small reason for its positive sales during the Christmas period is a base effect since stores were closed on January 1, 2022. Its acquisition of logistics provider Gist Limited last year has also bumped up its numbers. At the same time, the company has managed to grow its like-for-like sales by 7.2% anyway. So it’s not the company’s biggest concern but I believe still essential to mention.

Operating profits decline

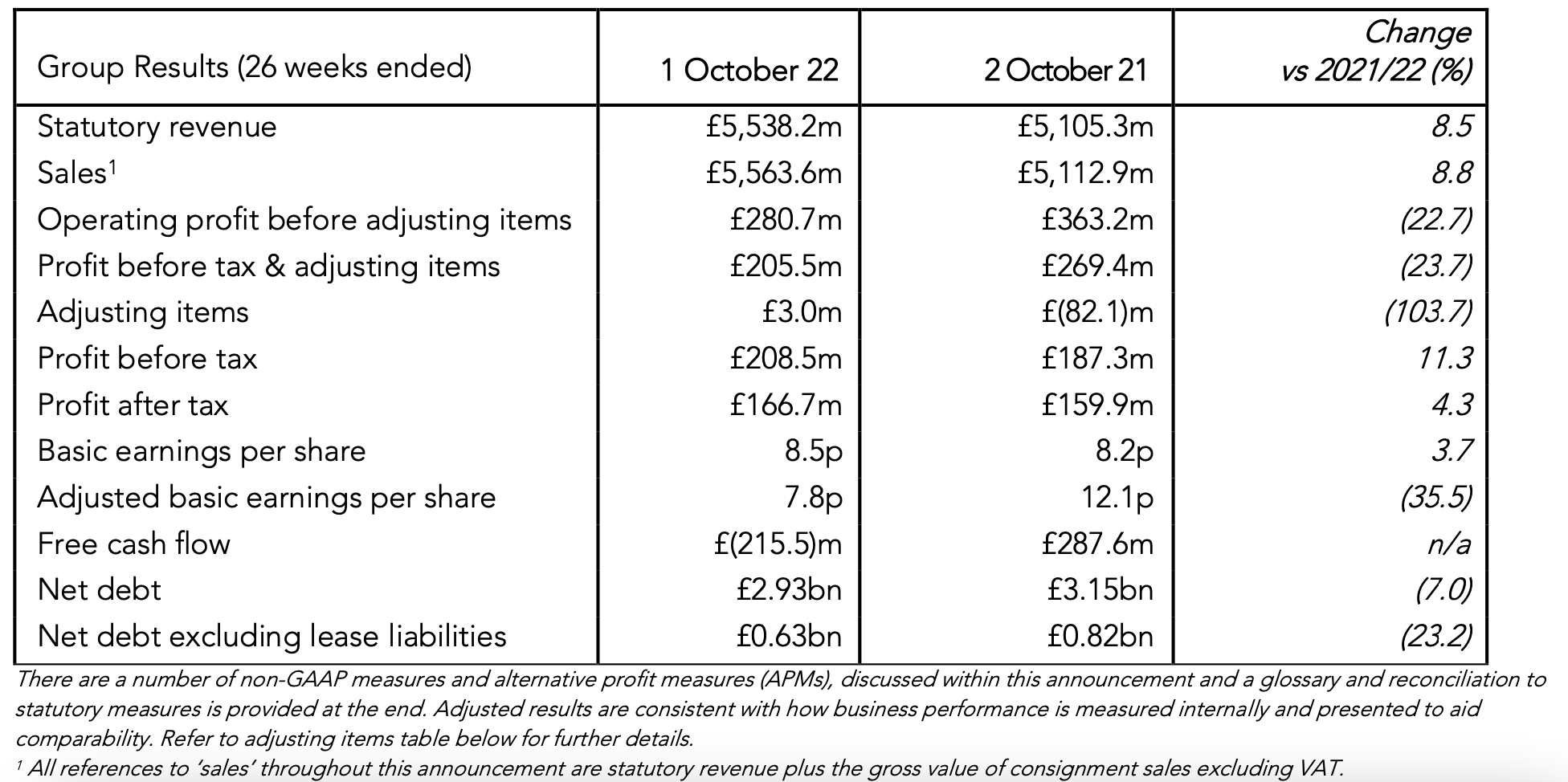

In fact, even its last quarterly results for the 26 weeks to October 1, 2022, showed a revenue rise of 8.5% year-on-year (YoY). This continues its growth run that started in its financial year ending April 2022, when it saw a 19% increase after three straight years of shrinking numbers, to reach the highest revenue figure of GBP 10.9 billion in 10 years. Both its profit before tax [PBT] and net profits are also up by 11.3% and 4.3% respectively. This is essentially due to adjusting items, like charges related to store closures and impairments, acquisition-related charges and credit on account of revaluation of the amount payable for Ocado, the grocery delivery services provider, among others.

Its operating profit is actually down by 22.7% however, primarily on cost increases. The UK, its big market is still seeing high inflation, with the latest figure at 10.5% for December 2022. While inflation has started coming off, down from the 40-year high of 11.1% in October 2022, it’s still a long way off from being manageable. Going by the significance of the market to M&S (see chart below) the operating profit number needs to be watched carefully for now.

{kind=link}

Liquidity is wanting

I’m also uncomfortable with its liquidity situation. It reported a negative free cash flow of £215.5 million compared to a positive figure of £287.6 million during the same period last year. This is largely down to a decline in operating earnings as well as working capital outflow, which partly results from increased inventory in anticipation of the festive season as well as cost price inflation. Further, its current ratio at 0.9x isn’t ideal either. Taking a longer-term view reveals that its current ratio hasn’t looked good in the past decade. But then it has been cash flow positive through this time, which isn’t the case now. So the next aspect to consider carefully for me to be its cash.

I’m particularly concerned about the fact that it has mentioned inflation with regard to both the operating profit decline as well as working capital decline, a challenge that can persist for some time. On the other hand, the increase in PBT and net profit is down to what appear to be one-off factors. If they aren’t around when it next releases its results in May 2023, it could impact the price negatively.

{kind=link}

Not an upbeat outlook

There was reason to be hopeful if the company’s outlook was positive. That’s not the case. It maintains the guidance that was first published when it first released its FY22 results. It expected to outperform in terms of sales even at the start of the current financial year while maintaining a dim view of its profits. It says “we start 2022/23 from a lower adjusted profit base….given the increasing cost pressures and consumer uncertainty, we do not currently expect to progress from this lower profit base in 2022/23.” In other words, we shouldn’t be surprised by weak profits in the second half of the year.

Market multiples suggest an upside

This also reflects in its price-to-earnings (P/E) ratio at 10.8x compared to 21x for the consumer staples sector. The context to this is that its operating margin is 21.5% less than that for the sector and its net margin is 33% lower, which goes beyond just its own financials.

On the positive side, its gross margin is 14% higher than the sector. Further, its P/E is lower than its median of 17.2x for the past 13 years. Its absolute price is also quite low, still down by almost 40% from a year ago. Its revenue growth is also just 1.9% lower than the sector average but its price-to-sales (P/S) is minuscule at 0.3x compared to the sector average of 1.1x.

What next?

Both Marks and Spencer Group plc's growth figures and market multiples suggest that there’s potentially more upside. But its profit position is unconvincing for now. It’s not loss-making, to be sure, but the profits have declined. Its liquidity position is another concern. And inflation, the key reason for this as well as a weak economy could impact them further in 2023. We could be one poor inflation report away from its price tanking again. Marks and Spencer Group plc is too risky to buy right now, I’d Hold off from buying it. There are safer and healthier stocks and ADRs around.

For further details see:

Marks and Spencer Group: Too Speculative To Buy