OCDDY - Marks and Spencer: High-Yield In The Retail Industry Given Balanced Risks In Recession Year

Summary

- Marks and Spencer has a strong market position in the consolidated non-cyclical industry.

- M&S generated around £1 bln in FCF in 2022 and is expected to be cash-positive in the near future.

- The company is on the way to gradual deleveraging. From 2019 FY total debt was reduced by £627 mln or 15%.

- M&S debt has a low refinancing risk and CDS spreads offer a contraction to BB and BBB peers.

Company Overview

Marks and Spencer Group plc (MAKSF) (MAKSY) ("M&S") is a leading British retailer bringing quality, great value food, clothing and homeware to millions of customers around the world.

- M&S was founded in 1884 by Michael Marks and Thomas Spencer in Leeds. For now, M&S is headquartered in London, England.

- It focuses on a wide spectrum of apparel, home, furniture, beauty, food, household items and much more.

- M&S has a primary listing on the London Stock Exchange and is a constituent of the FTSE 250 Index.

- M&S consists of JV with Ocado and 3 major business units which are presented below.

Exhibit 1: Business units.

Business units. (Earning report)

{kind=link}

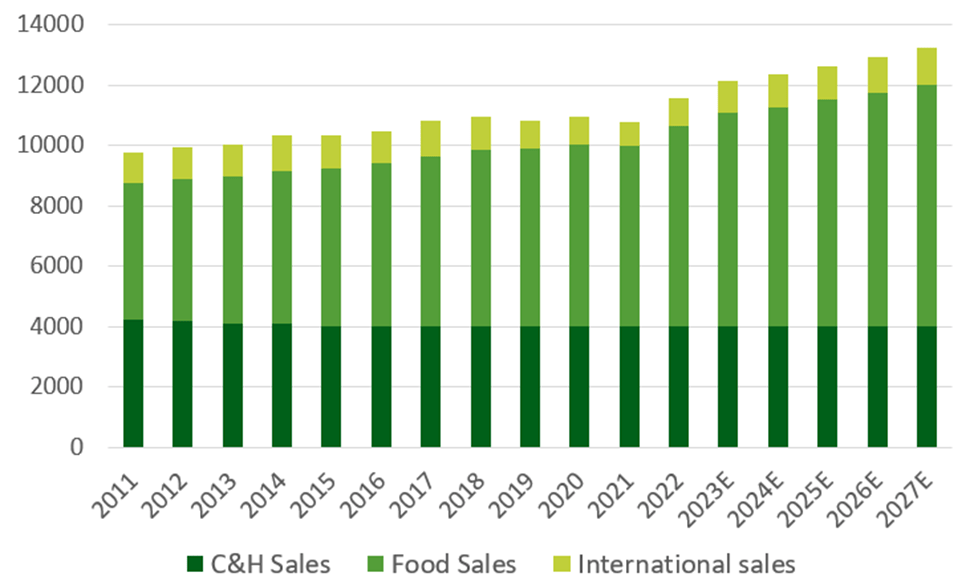

The revenue structure seems to us to be stable with the majority of future CF coming from Food. Clothing & Home (C&H), in turn, keeps generating stable sales. The international division provides additional diversification of risks.

Exhibit 2: Revenue structure.

Revenue structure (GS estimates)

{kind=link}

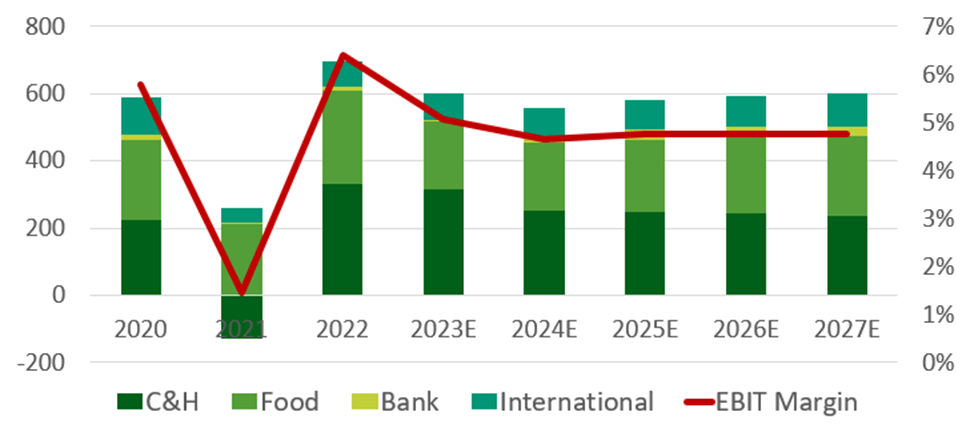

Now, as for EBIT, the situation is completely different. C&H accounts for 52.5% of M&S's EBIT. This share is expected to further decrease with the projected increase in Food and International contributions.

Exhibit 3: EBIT structure

{kind=link}

Financials

Marks and Spencer has strong stable financials with consistent revenue generation and positive FCF generation. Performance in FY 2022 was strong due to both post-pandemic recovery and progress on its longstanding restructuring initiatives focused on cost optimization, store estate management and digital capability enhancement.

Furthermore, M&S is on the way to gradual deleveraging. From 2019 FY total debt was reduced by £627 mln or 15%.

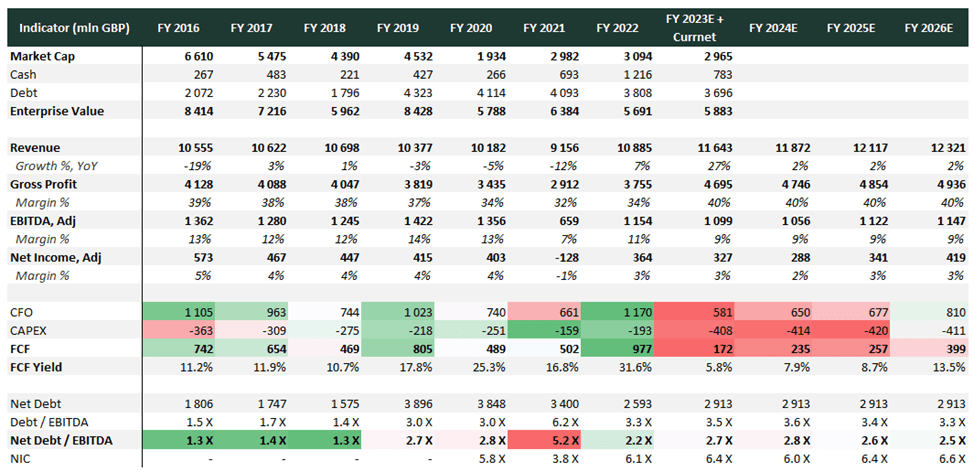

Exhibit 5: Company historical financials and the consensus estimate

Company historical financials and the consensus estimate (Bloomberg, Analyst research)

{kind=link}

Currently, M&S has a reasonable leverage, reducing Net Debt / EBITDA to 2.7 X from 5.2 X in the pandemic year. Yes, for the retail business, it can be called significant, but it is levelled by properties and quality. Also, the level of interest coverage ratio does not raise any questions.

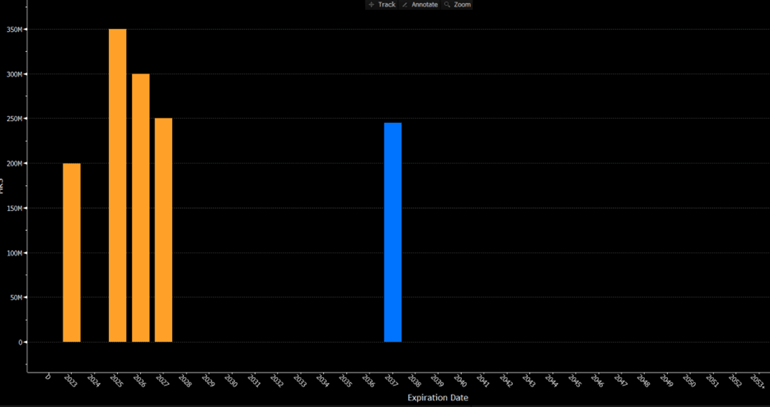

M&S repurchased £150 mln of its medium-term notes in 1H22, reducing refinancing risk further. The next major maturities are in 2025 - 2026 with total amount of £650 mln, which are fully covered by C&CE (£773 mln) and undrawn £850m Revolver credit facility until June 2025.

Exhibit 6: Debt distribution

{kind=link}

Another thing that we have to mention is that leases are the main part of the total debt, contributing around 62%. Group net debt increased by £229.9 mln since 1H 2023 driven by net increase in lease liabilities, relating to five new UK leases, and the consolidation of Gist lease liabilities.

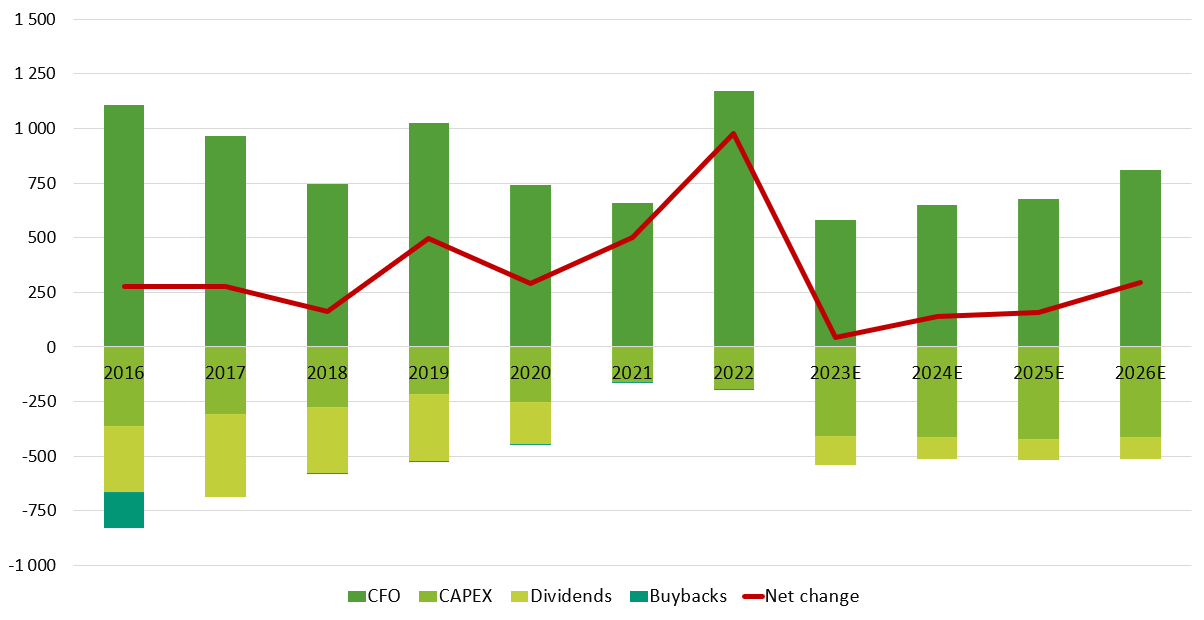

Speaking about capital allocation strategy, M&S has demonstrated good financial discipline by suspending dividends during the pandemic and despite strong 2022 FY performance. Management values strong liquidity in these uncertain macroeconomic times. But we expect that potential renewed dividend payments and a big CAPEX program are going to eat a tangible part of CFO.

Exhibit 7: CF distribution

CF distribution (GS estimates)

{kind=link}

Nevertheless, CEO said on the last call that the priority for M&S now is business improvement and growth. But at some point, M&S needs to start capital returns to shareholders.

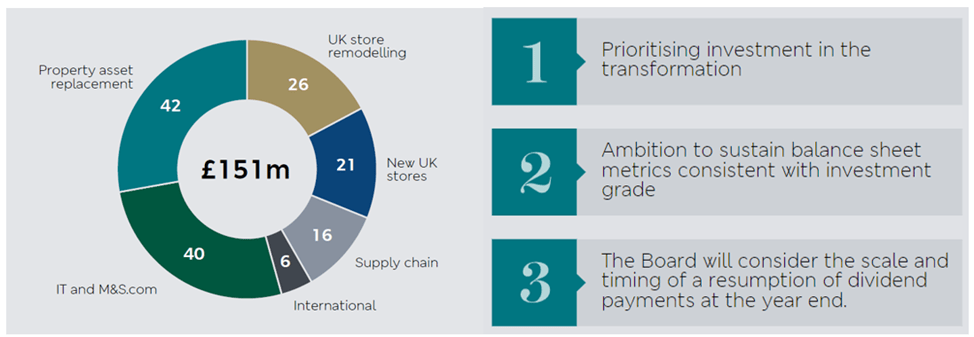

Exhibit 8: CAPEX structure

{kind=link}

On the other hand, Marks and Spencer expects to spend £400 mln in CAPEX in 2023, significantly higher than the approximately £200 mln in past years. High future CAPEX expectations are reflected in the investments in new store formats/store rotation program and improvement of omnichannel capabilities.

Property made up accounts for over half of the CAPEX, essential maintenance and asset replacement spending continued. Besides, M&S continue to develop new channels to communicate with customers, increasing spending on application and IT development. In other words, M&S reshapes for growth, prioritizing investment in the transformation.

Besides, M&S has a higher NI margin comparing with retail peers like Tesco and Sainsbury's due to C&H business. This allows M&S to develop its fast delivery business in JV with Ocado.

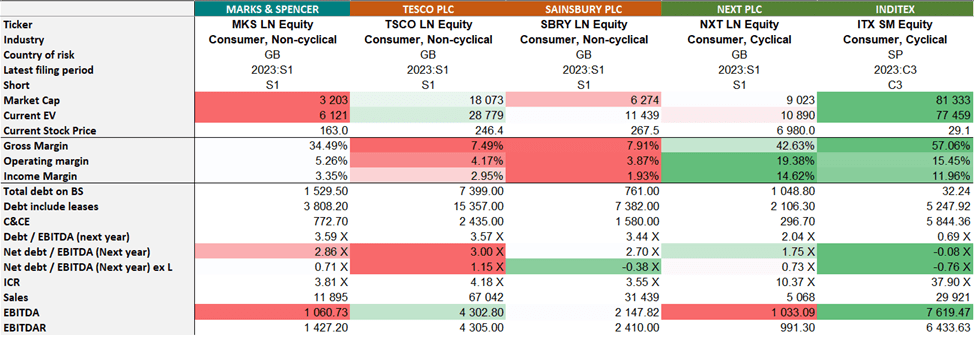

The level and structure of debt can be called comparable with competitors.

Exhibit 9: Peer's analysis

{kind=link}

Furthermore, CFO on the last earnings call confirmed that they are convinced to reduce leverage which indicates the company's determination to further reduce the debt burden.

Strong market position

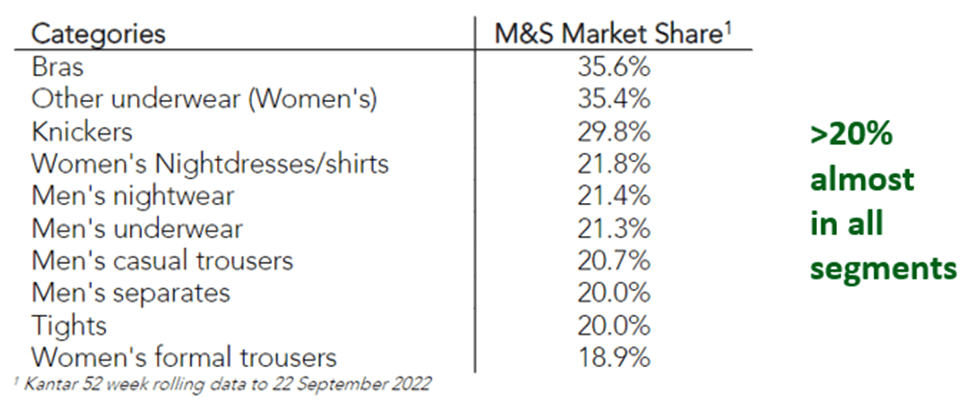

M&S benefits from being the second-largest UK clothing retailer, with a simplified product range and a larger full-price sales mix.

M&S's share of the UK clothing market reached its highest level in almost 8 years and its food division increased its market share due to a strong Christmas trading period. C&H has market share positions of more than 15% in categories which are less acutely exposed to discretionary spending, such as underwear and school uniforms.

Exhibit 10: Market share by categories

Market share by categories (Presentation for investors)

{kind=link}

Real Estate property & Stores

Another thing that makes you believe is a convincing portfolio of diverse real estate. U.S. private equity firm Apollo Global Management is considering a takeover bid for retailer Marks and Spencer because of significant real estate assets. The latter could be worth around £2 bln , which potentially covers a tangible part of total debt.

On the other hand, Marks and Spencer has been making property improvement to revive its fortunes. M&S is set to open 104 food shops and shut sixty-seven full-line clothing stores in the next 3 years. Overall, it plans to reduce the number of full stores offering food, clothing and home sales from 247 to 180 by 2026 and increase its Simply Food outlets by 104 to 420.

This is where most of the CFO will be distributed. And thus, it also raised questions regarding whether the implementation of this strategy will be successful or not.

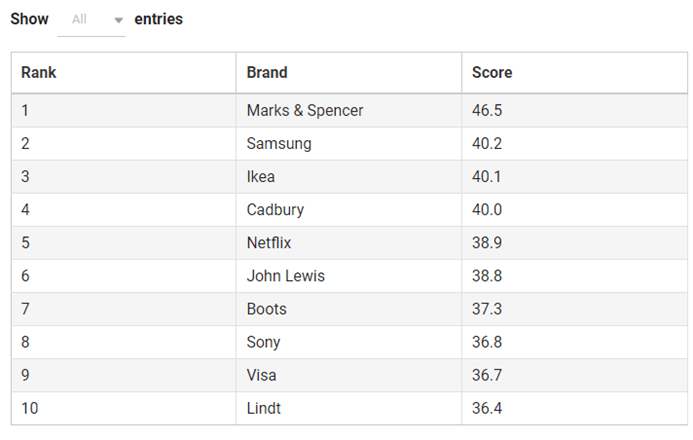

M&S's strong value brand perception

Marks and Spencer top for customer loyalty and satisfaction. The company benefits from strong brand recognition in food and a well-established market position in clothing.

Marks and Spencer has won a poll to figure out to which clothing brand or retailer UK shoppers are most loyal .

Apart from this, M&S has been ranked as the UK's best brand based on overall brand health, impression, quality, value, satisfaction, and reputation.

Exhibit 11: The UK's top brands

The UK's top brands (Retail gazette)

{kind=link}

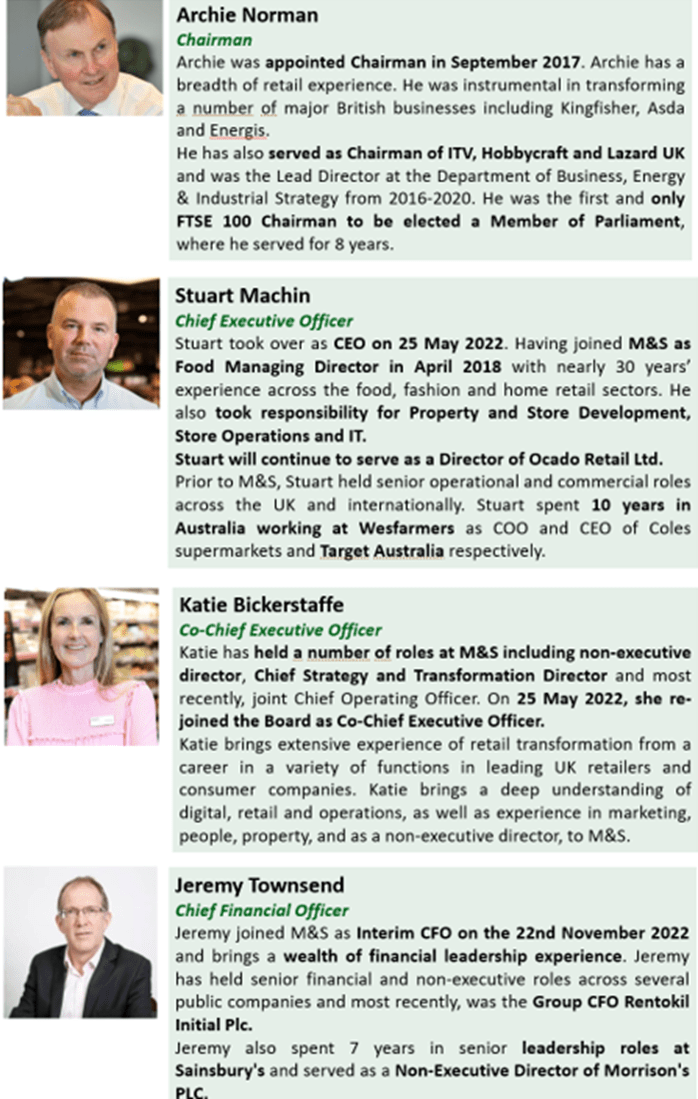

Strong industry expertise with big challenges ahead

In addition, it should be noted that M&S's new CEO created an all new team in the 1Q of 2022, which brings a little uncertainty. Nevertheless, management consists of professionals who have been in business for more than a decade with wide experience in other industry giants such as Target.

Exhibit 12: Management team

Management team (Annual report)

{kind=link}

Bonds selection

M&S' BB-rated USD bonds offer a considerable upside to BBB retailers like Next and Tesco, whose spreads reflect higher ratings. Despite 10Y UST rally in recent months, the option to lock in yields now still exists.

Exhibit 13: Bond issues

{kind=link}

As we write before, it's overly complicated to find the bottom of the bond market in this rapidly changing economic environment. Thus, it is vitally important to start forming bonds portfolio with extended durations. This M&S's bond issue certainly belongs to the latter.

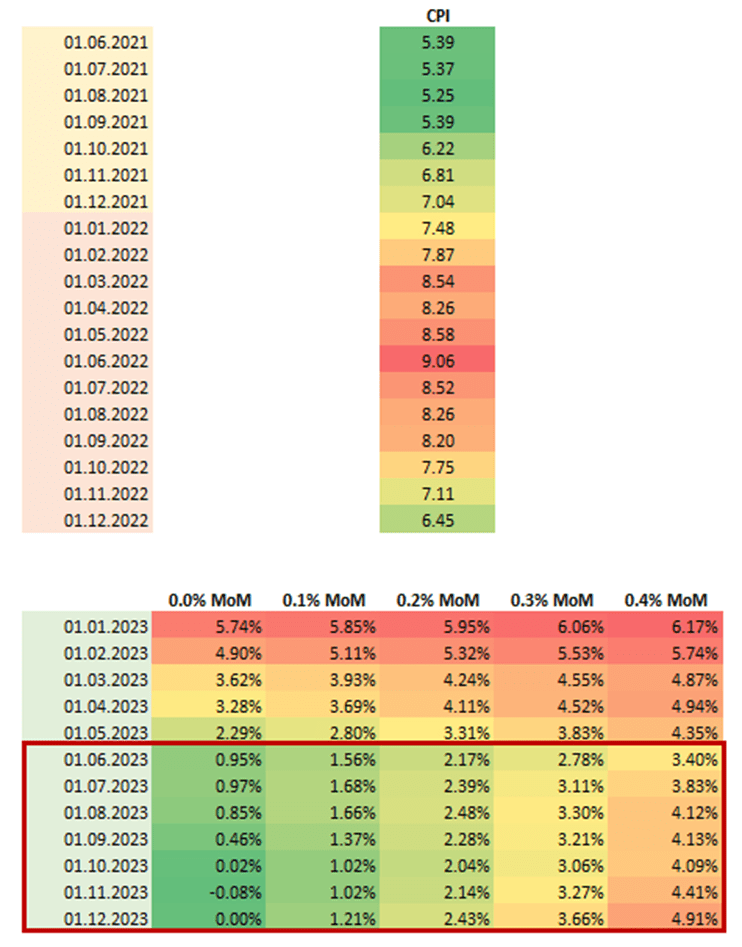

Moreover, it seems that we have already passed the peak of inflation in US. CPI has already decreased by 3% from the maximum.

Below are a potential 5 paths for US CPI based on fixed MoM changes.

Exhibit 14: Possible CPI dynamics

Possible CPI dynamics (Analyst research)

{kind=link}

It could be mentioned that US CPI YoY will be below the projected Fed inflation target as early as June 2023 and real yield will become positive in March. The main decline in CPI will be in the next two months because in February and March last year, inflation was more than 2%.

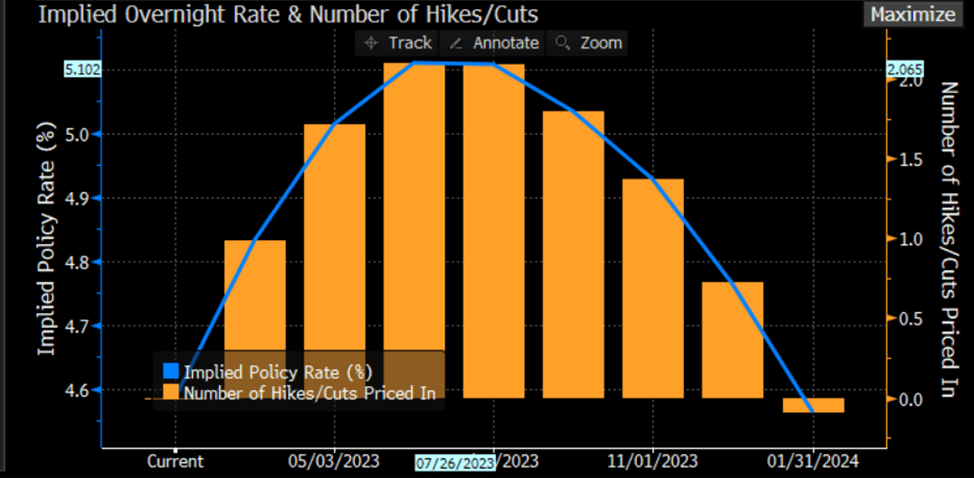

Exhibit 15: Implied overnight Rate & number of Hikes

Implied overnight Rate & number of Hikes (Bloomberg)

{kind=link}

In addition, the swap market prices the start of rate cuts as early as July this year. Therefore, it is worth paying attention to bonds with a long duration.

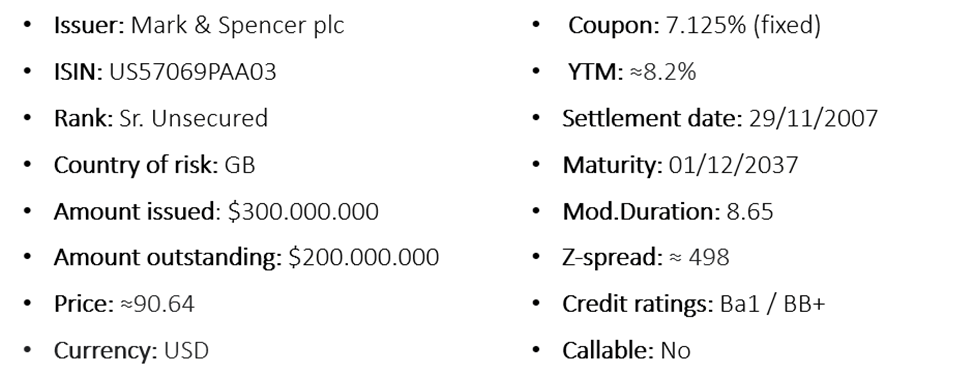

Exhibit 15: Bond description

{kind=link}

Investor takeaways

In our view, M&S remains the best option to buy in the bond universe in the retail segment to lock high rates on scrunching inflation expectations. We're overweighting M&S's bond issue with 9-years duration due to high exposure to interest change.

Key risks

- Consumer weakness and inflationary pressures are being faced across the industry.

- Restart of dividend payments

- Execution risks related to implementing a high degree of change in the business and new management team

- Multi-year pre-pandemic trend of weak underlying sales and declining profitability, but the company is looking for new growth points

- Weak consumer confidence

For further details see:

Marks and Spencer: High-Yield In The Retail Industry Given Balanced Risks In Recession Year