TSCDF - Marks and Spencer: Weak Operating Margin Encourages Caution

2023-06-30 03:50:32 ET

Summary

- Marks and Spencer stock has seen a significant rise of 68.2% in the last six months due to improved financial health and restored dividends.

- M&S plans to reduce costs by £400 million over the next five years, which could improve its operating margin, but it is still concerned by its operating margin at 5.25% in 2022/23, down from 6.5% the previous year.

- However, high food inflation and a weak economy pose risks to cost control.

- Despite these concerns, M&S expects modest growth in revenues in 2023/24 and has seen net profits rise by 18% in the past year.

- However, I recommend holding on investing in M&S due to the potential risks.

Despite the impressive price increase it had seen when I last wrote about the British grocer and retailer Marks and Spencer ( OTCQX:MAKSF ), I was hesitant about the stock, prompting a Hold rating on it. But I was obviously in the minority since investors have continued to remain bullish on it. MAKSF is up by another 30% since, resulting in a huge 68.2% rise in the last six months.

{kind=link}

There are good reasons for this. The company's results for its full year ending April 1, 2023 (2022/23) reflect some bettering in financial health and it has also restored its dividends. At the same time, its market valuations also look attractive right now. But the devil, as they say, is in the details. The devil, in this case, is in three words, the operating margin. Let me explain.

Improving operating profits

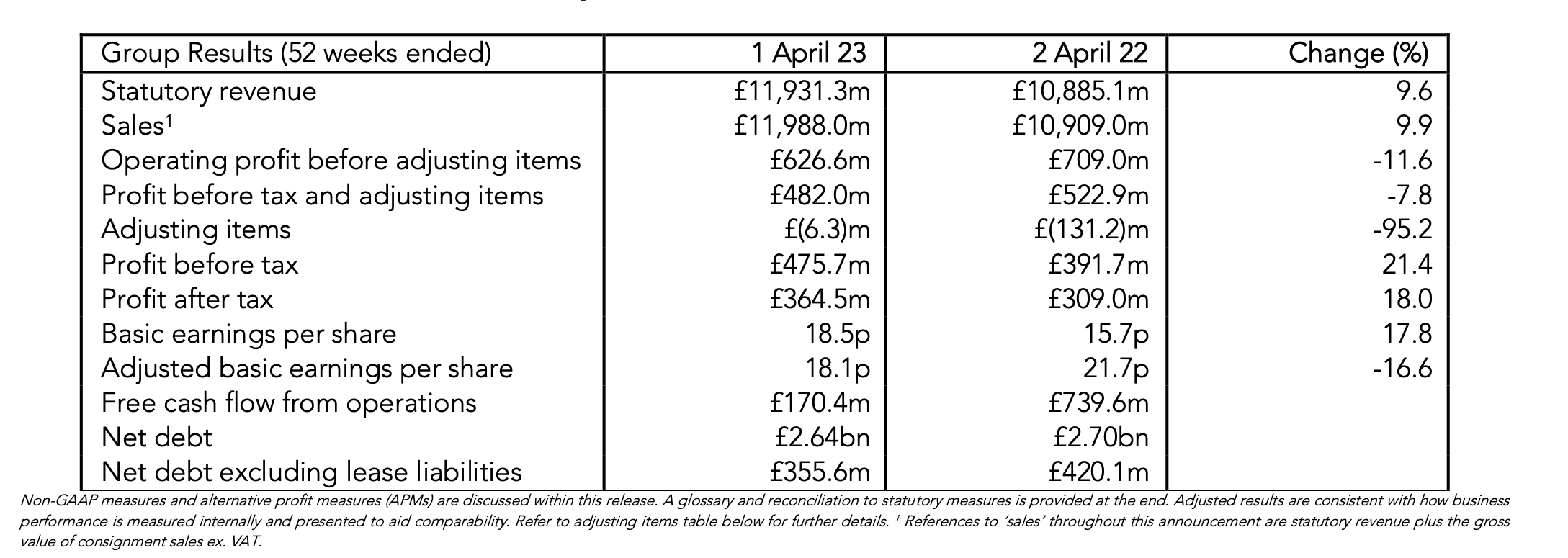

M&S's 2022/23 results do assuage concerns about its GAAP operating profit to some extent. They had dropped by a big 22.7% in H1 2022/23 . By comparison, the H2 2022/23 figures have remained the same as in the same time period last year. As a result for the full year, operating profit is down by 11.6%, which isn't ideal but it is still a reflection of improving health.

Financial Highlights (Source: M&S)

{kind=link}

This is really down to better revenue growth, which picked up from 8.5% year-on-year (YoY) first half of 2022/23 (H1 2022/2023) to 9.6% for the full year 2022/23. This was to be expected since the company had reported a robust trading update for the Christmas season, which saw it becoming the fastest growing grocer as per a Nielsen study. As a result, it saw a healthier increase in H2 growth to 10.6% compared to H1.

Weak operating margin

An improvement in operating profits, however, did not translate into better margins. The margin remained weak in H2 2022/23 at 5.4% (estimated from total revenues, and not the sales figures that M&S provides separately), compared to 5.9% in H2 2021/22. It has improved a bit from H1 2022/23 though, when it was a 5.1%, resulting in the full-year number at 5.25%. But here's the real rub. The full-year margin declined by a whole 1.25 percentage points from 6.5%.

When inflation is under control, margins while still being important, are less significant. But inflation is not under control and has not been for some time as we all know. In fact, even with the decline in inflation figures to 7.8% in May 2023, from their double-digit highs in October last year, they are still significantly higher than what the Bank of England would like, at 2%.

This means that retailers like M&S have to play the balancing game between revenue growth and margin contraction. If they pass on their cost increases to customers fully, which incidentally it has not done, then demand can drop. But if demand is sustained, then margins have to drop. Additionally, we are in a time of an economic slowdown, if not impending recession here in the UK, which means there is the likelihood of demand weakness in any case.

Impact of structural cost reduction

But the company has a plan to deal with this situation in the form of a programme to reduce costs structurally. It targets a cost reduction of over £400 million over five years under this programme, which is expected to be achieved with higher store rotation, profitable online growth and productivity improvements to offset inflation.

To get a sense of what this means for M&S's margins, I did some number crunching. This is based on the assumption that the cost reduction is at exactly £400 million and is reduced equally across the five years, which comes to £80 million per year. If this figure is deducted from the company's costs during 2022/23, the operating profit rises to just shy of the levels seen in 2021/22. However, the margin is improved by just 0.5 percentage points because of this. This is really because £80 million is really a small proportion of the £11.3 billion costs for the year.

The company aims at an ~8% margin based on this reduction, with a 10% margin for the Clothes and Home and a 4% Food segment margin for the segment. It is not clear, how it hopes to achieve this based on the restructuring alone, though a natural decline in inflation can help, which I will talk about next.

Reduced inflation can help, or can it?

If M&S sustains revenue growth, a cooling off in inflation can certainly help its operating profits. At the same time, it is important to look out for specific items in inflation. In this case, I would look out for food price inflation, which remains particularly high at 18.4%. This is important for the company, since its food business accounts for over 60% of its revenues. So it is really a significant cost to consider for M&S. With its operating margin already squeezed to the lowest levels in a decade, save the COVID-19 period, I am still somewhat cautious about the margin picture.

Source: Office Of National Statistics

{kind=link}

The positives

It's not all gloomy for M&S, though. It expects a "modest growth in revenues" in 2023/24. It is also confident that its strategy "is beginning to deliver improved performance and there remains much within the Group's control." This is encouraging considering that it acknowledges that "market conditions are expected to become more challenging".

The company's net profits have also risen by a strong 18% in the past year and it plans to restore a "modest annual dividend". It also has an attractive TTM price-to-earnings (P/E) ratio of 10.9x compared to 22.5x for the consumer staples sector. It is especially favourable compared to Tesco ( TSCDF ), the UK's biggest grocer by market share, which is trading at 26.9x.

What next?

If I were less concerned about the macroeconomic situation, I would have upgraded M&S to Buy. After all, it has managed to grow revenues at a challenging time, its net profits are strong and its P/E is attractive.

At the same time, it is clear that important operating profit margins are struggling at this point, even with improvements in H2 2022/23 in the profit figures themselves. But a weak economy and high food inflation don't bode well for its operating margins, indicating either they will be squeezed further which should ultimately reflect on net profits too or its revenues slump or both.

Going by the company's recent performance, maybe it can pull it off yet again. But that's just not enough argument to invest in it, high performing as its stock is right now. I'm retaining a Hold on Marks and Spencer.

For further details see:

Marks and Spencer: Weak Operating Margin Encourages Caution