WU - Marqeta: I'm Not Going Anywhere

Summary

- Despite strong Q2 results, Marqeta's stock plunged 24% the following day.

- Founder Jason Gardner is planning to transition out of his CEO role, but it's not as bad as it seems.

- Marqeta stock also flash-crashed by 30%+ a few days before its earnings release.

- Valuation looks attractive, with Marqeta's Net Cash position representing ~40% of its Market Cap.

- Marqeta has strong execution. High-quality business. Long growth runway. I'm not going anywhere.

For a more in-depth analysis of Marqeta, Inc.'s ( MQ ) business, I'd like to direct readers to my Marqeta deep dive article . This is a review of Marqeta's recent Q2 results. Enjoy!

Investment Thesis

Marqeta is a modern issuer processor that is disrupting the issuing-facing side of the payment ecosystem. The company provides a scalable and configurable, cloud-based platform for Customers to launch and manage their own card programs.

The company recently reported Q2 results that beat expectations — but the stock sold off the next day, mostly because Founder-CEO Jason Gardner is planning to step down as CEO.

The selloff might be an overreaction.

In this article, I'll explain why.

But first, let's take a look at Q2 results.

Growth

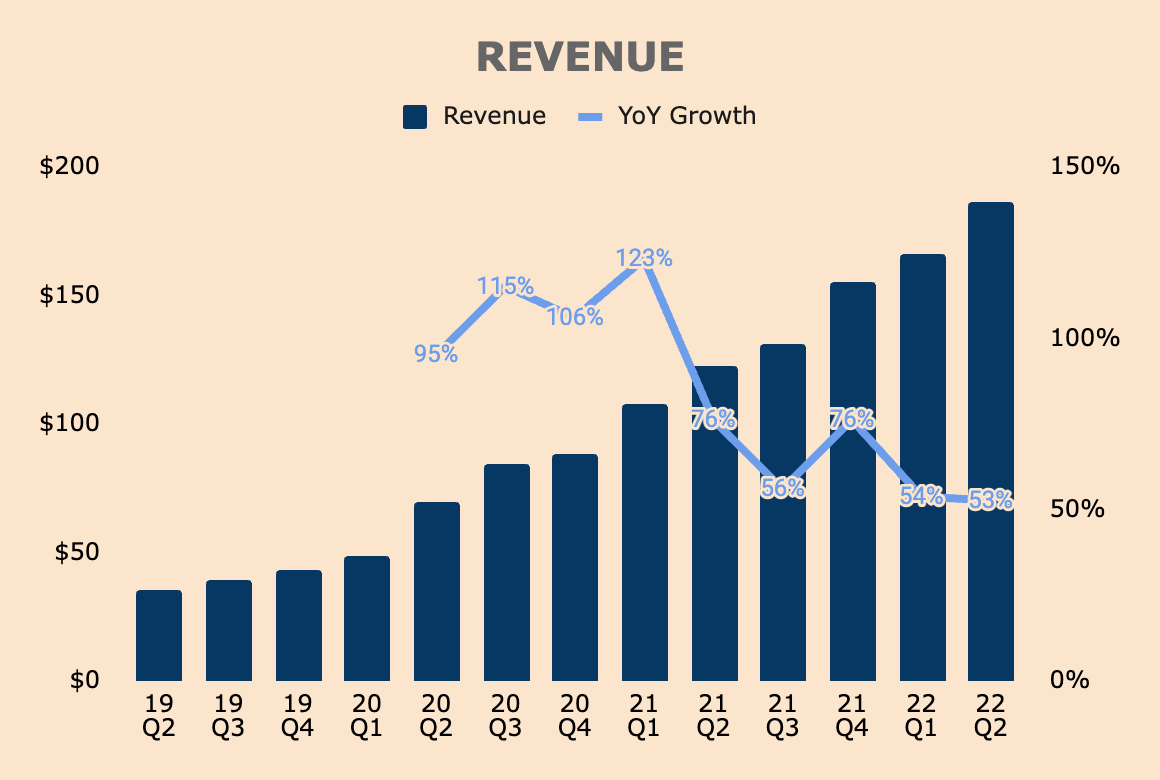

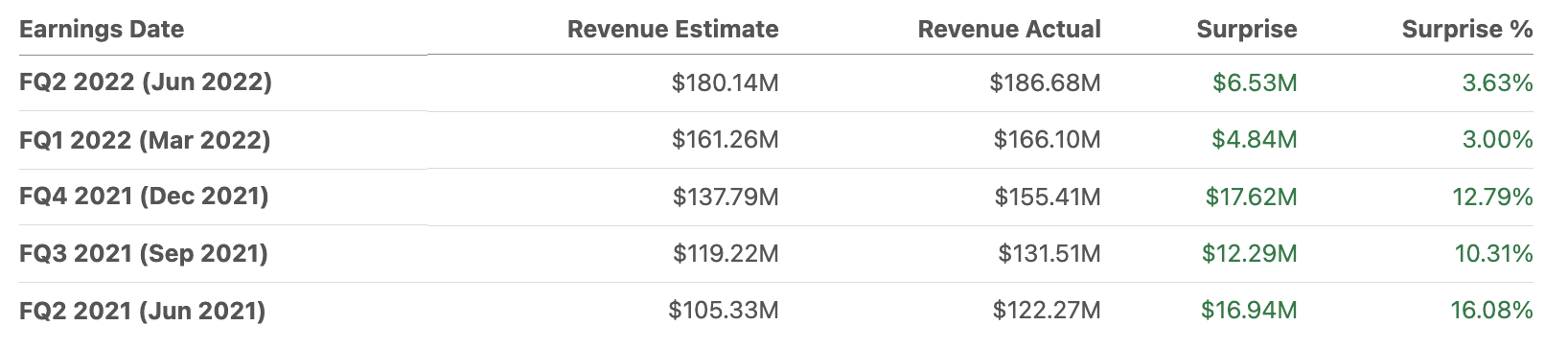

In Q2, Marqeta grew Revenue by 53% to $187 million — beating analyst estimates by 3.7% — primarily due to three reasons:

- Increase in Total Processing Volume ((TPV)).

- Higher Revenue Take Rate due to favorable merchant mix and card mix.

- Higher usage of additional services not tied to TPV, such as card fulfillment.

Although growth is slowing down, it's still robust given tough YoY comps driven by government stimulus last year.

{kind=link}

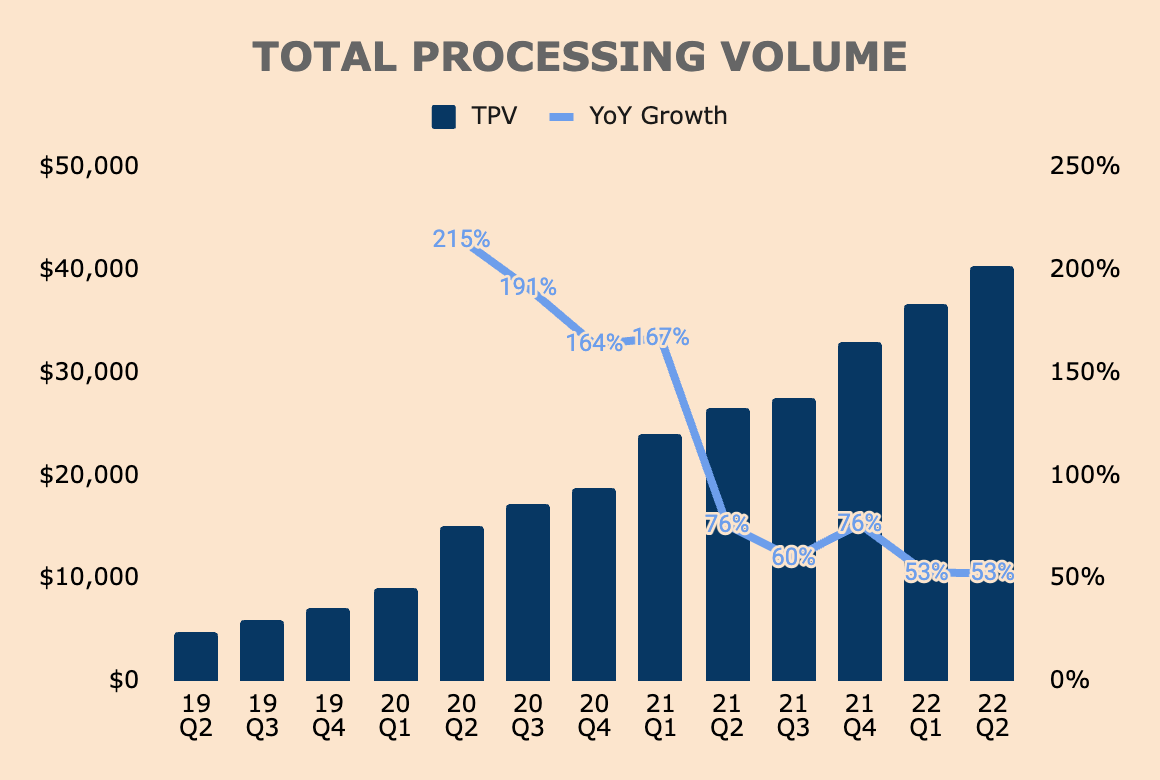

Here, we can see how TPV has trended over the last few quarters. Similar to Revenue, TPV grew by 53% as well, processing a total of $40.5 billion. This beat estimates by 4.5%.

{kind=link}

TPV growth was driven by continued growth among customers:

- Top 5 Customers grew by 48%.

- Non-top 5 Customers grew by 81%.

- On-demand delivery accelerated by 10 points.

- Expense management more than tripled YoY.

- Growth accelerated in low discretionary categories including groceries, fuel, and utilities (~1/3 of TPV).

TPV growth was offset by other parts of the business which showed signs of weakness.

- Financial services slowed by a few points due to tough YoY comps.

- BNPL growth dropped below 100% for the first time.

- Growth decelerated in high discretionary categories including retail, travel, and home improvement (~1/6 of TPV).

Higher discretionary categories could be under further pressure as consumers cut back on spending amidst a high-inflation environment.

Being that as it may, management keeps on executing its growth plans, landing new deals in Q2 that'll amplify network effects:

- Partnered with Western Union ( WU ) in Europe.

- Introduced 40+ new credit card APIs .

- Partnered with Mastercard Prepaid Managed Services ((MPMS)) to become the payment processor for Opal Plus , a new mobility-as-a-service app launched in Australia.

- Expanded partnership with Klarna to issue the Klarna Card .

- Joined Mastercard's Network Enablement Partner Program, which increases its exposure in the Asia Pacific region.

So, despite the incredible growth seen in 2021, Marqeta still manages to post 50%+ growth in a tough market environment — further confirmation of Marqeta's strong value proposition, increasing adoption of fintech applications, and the growth of Marqeta's ecosystem of disruptive customers and legacy financial institutions.

Profitability

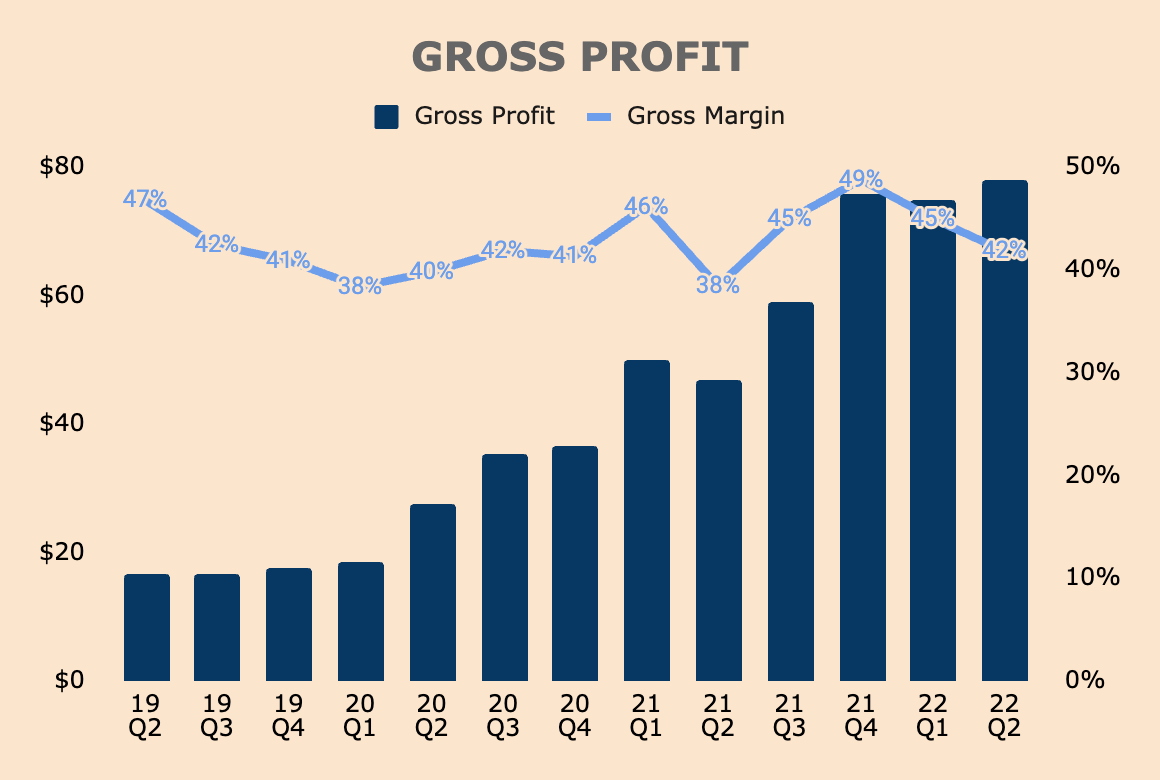

Gross Profit grew faster than Revenue, up 66% YoY to $78 million. This improved Gross Margin YoY, from 38% to 42%, and this is due to:

- Unusually high network fees in Q2 last year as a result of contract amendments in Q3 2021, which did not recur in Q2 this year.

- Favorable volume mix.

- Customers increasing usage of additional services, like card fulfillment, dispute handling, and cross-border premiums.

Moreover, it's still an improvement from 2020 Q2 Gross Margin of 40%, showing some signs of economies of scale. It's also worth noting that Q2 usually returns the lowest Gross Margin due to the timing of network incentive contracts. As such, you can see how Gross Margin fluctuates with each passing quarter.

{kind=link}

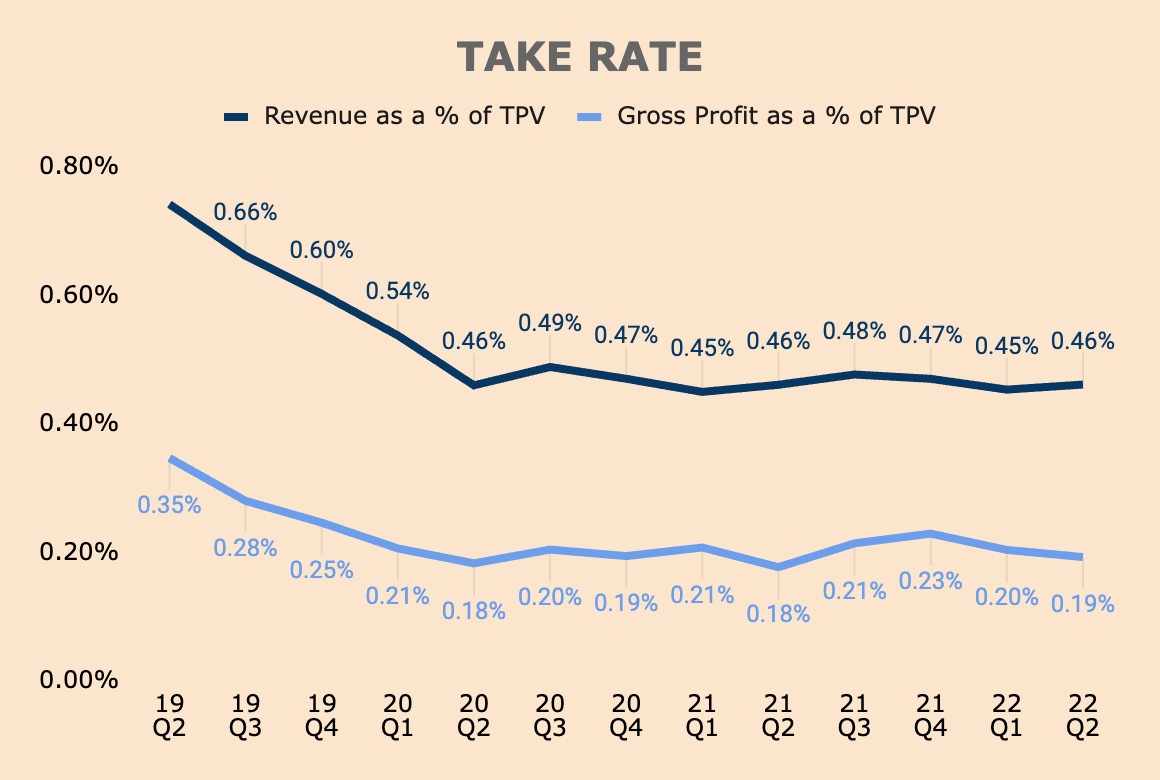

Keep in mind that as TPV increases, Marqeta, as a % of TPV:

- Receives higher network incentives from the card networks — like Mastercard ( MA ), and Visa ( V ) — which is margin accretive.

- Pays less issuing bank fees to partner banks — like Sutton Bank — which is margin accretive.

- Incurs higher Revenue Share payments to Customers — like Block ( SQ ) — which is margin dilutive.

With that in mind, we can see how Take Rates have trended.

Take Rates saw a steep drop in the better part of 2019. I believe this is due to Block making a larger proportion of total Revenue — Marqeta has to give up more Revenue as Block reaches specific volume tiers. However, we're seeing take rates stabilize over the past few years, likely because Block's concentration continues to drop as other Customers on the platform outpace Block's growth.

{kind=link}

As you can see, in Q2, Revenue Take Rate was 0.46% and Gross Profit Take Rate was 0.19%.

Management expanded more on Q2 Revenue Take Rate:

Our net revenue take rate was in line with last year but improved 1 bp versus last quarter. On a sequential basis, the improvement was driven by favorable business mix and strong growth in additional revenue streams not directly tied to every dollar of TPV, such as card fulfillment, KYC/KYB services, dispute handling and cross-border premiums. These benefits were partially offset by the impact of Powered by Marqeta TPV growing faster than the rest of the business.

As a reminder, in our Powered by Marqeta business, we primarily have a processing relationship with our customer. Therefore, the take rate is typically lower than in our Managed by Marqeta business.

(CFO Mike Milotich, MQ FY2022 Q2 Earnings Call )

Over the long run, I'd love to see Take Rates improve as 1) Block's concentration drops and 2) Marqeta upsells additional services.

Higher Take Rates mean economies of scale.

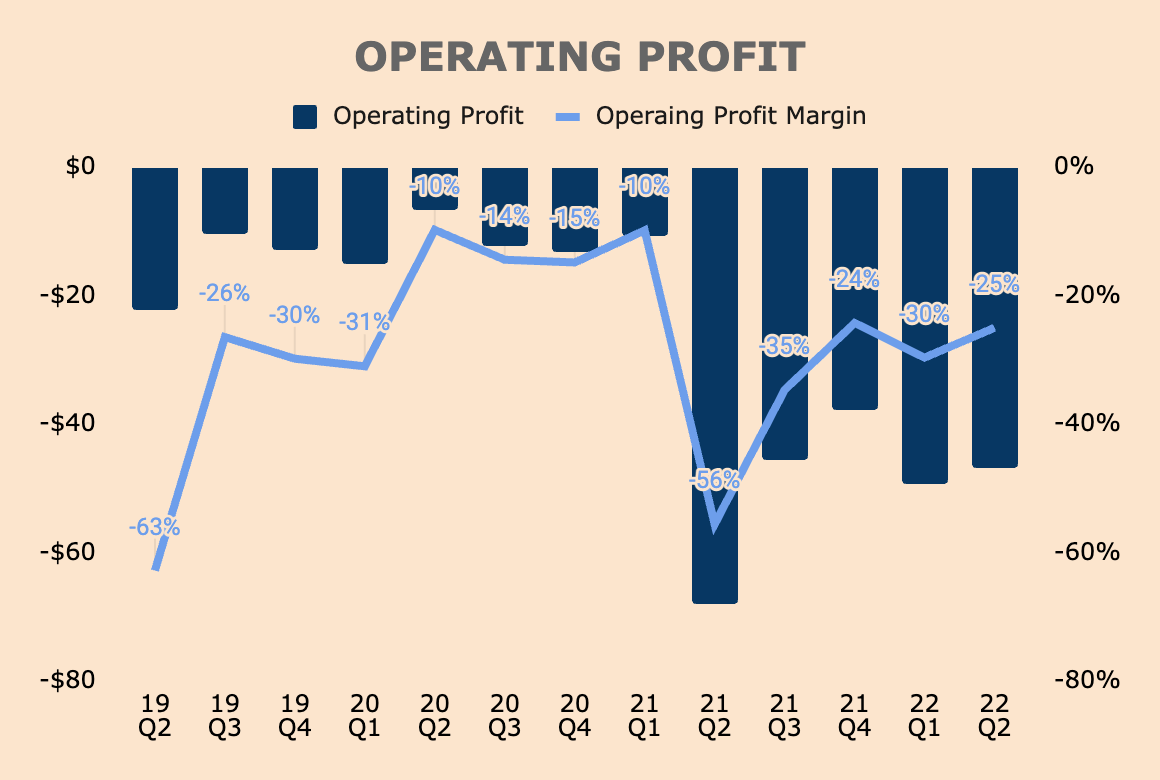

Moving on, Marqeta recorded an Operating Margin of (25)%. Although improving, it's still in the red, primarily due to high Stock-based Compensation, which makes up 19% of Revenue in Q2.

{kind=link}

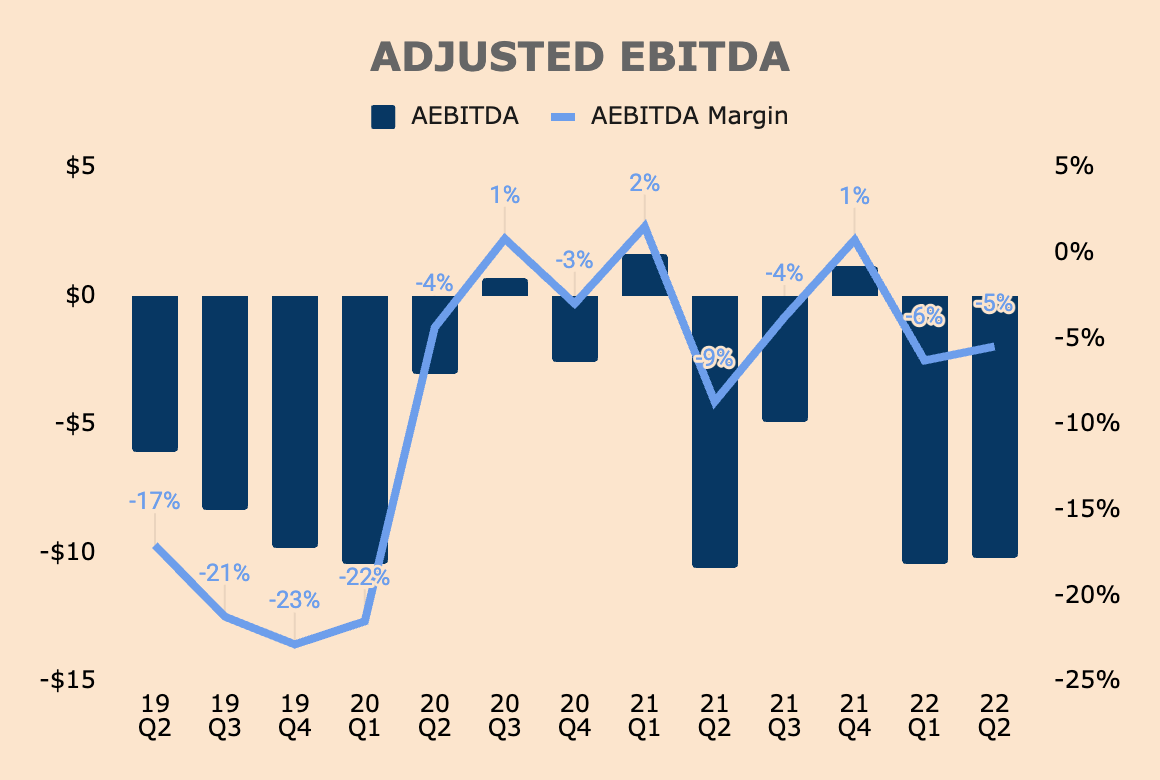

Adjusting for SBC and other non-cash expenses, Marqeta had an Adjusted EBITDA of $(10) million in Q2, an annual run rate of $(40) million. This cash burn is minuscule considering Marqeta's strong balance sheet.

{kind=link}

Putting the pieces together, Marqeta's profitability metrics seems to be trending in the right direction, showing good earnings potential, economies of scale, and operating leverage. Still, the company is unprofitable on a GAAP basis. But that's because management is reinvesting into growth — and given management's track record, I'm confident that their growth plans today will reward shareholders in the future.

Financial Health

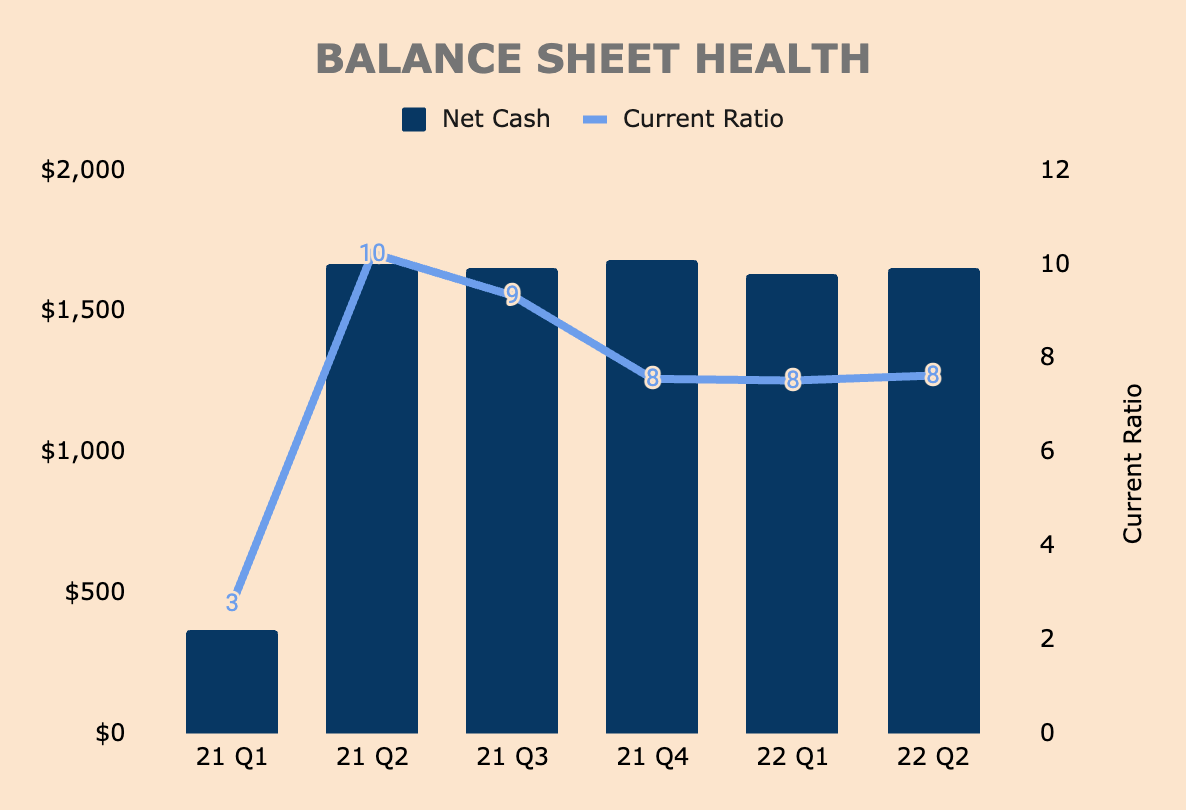

Turning to the balance sheet , Marqeta holds $1.7 billion of Cash and Short-term Investments. The company has virtually zero debt so that makes its Net Cash position at $1.7 billion as well. It has a Current Ratio of about 8x, which is very healthy.

{kind=link}

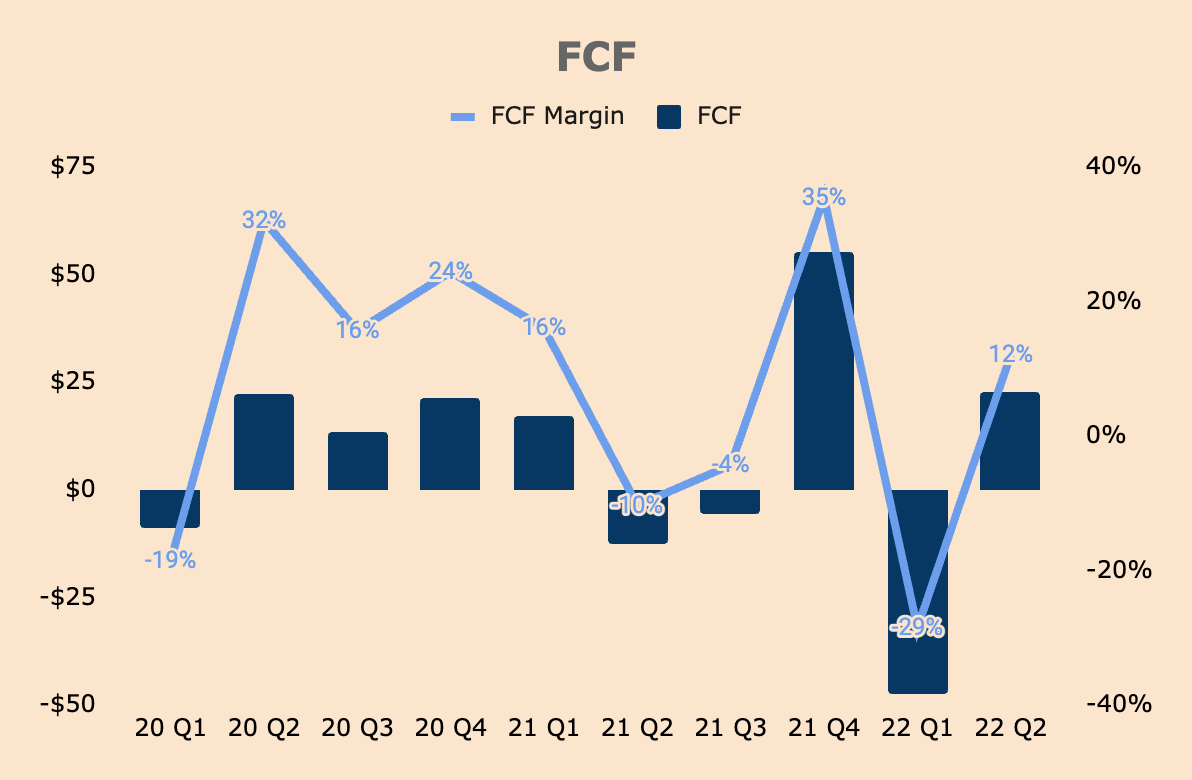

While AEBITDA is still negative, Marqeta is actually Free Cash Flow ("FCF") positive — in the last twelve months, FCF was $25 million. Along with Marqeta's high Net Cash balance, Marqeta has the financial prowess to withstand an economic downturn.

On top of that, in a time when other fintech firms are burning cash and trying to make ends meet, Marqeta has the opportunity to deploy its cash for growth or share buybacks.

{kind=link}

Outlook

For the back half of the year, management expects the fintech space to be "less aggressive about their investments in expansion" as they navigate through an increasingly uncertain macroeconomic environment.

Many of the tailwinds that drove our first half upside should continue. However, we also believe that many of the customers signed in the last 12-plus months as well as crypto customers will ramp their businesses more slowly than we expected a few months ago .

Because these are newer customers ramping up, the impact of less investment by our customers and their programs is more significant in Q3 and Q4 than it was in the first half.

(CFO Mike Milotich, MQ FY2022 Q2 Earnings Call)

Accordingly, management feels "it is prudent to be cautious" about guidance. For Q3, management expects:

- Revenue to grow 36-38% YoY , factoring in lower contribution from new customers as well as tough YoY comps in BNPL and expense management.

- Gross Margin to be 43-44% .

- AEBITDA Margin to be (8)-(9)% citing that Q3 should be its "most negative margin quarter" as the company continues to invest for growth.

Management also provided some color for full-year performance:

- Revenue to grow 39-40% YoY with growth stepping down further in Q4.

- Gross Margin to be 43-44% .

- AEBITDA Margin to be (7)-(8)% , and eventually, reach its long-term goal of 20%+ AEBITDA Margin.

With its $1.7 billion war chest, M&A is also probable.

There are a lot of great companies out there that are relatively small that could be very strategic to Marqeta. So we have been active as a corp dev department really looking and scoping out like what is out there and how can we not only increase our road map but add new features and functions to our platform that allows us to grow, expand and build even deeper moats and taller walls around our technology.

(CEO Jason Gardner, MQ FY2022 Q2 Earnings Call)

Management has a history of sandbagging guidance, so we may see better-than-expected results. Furthermore, Marqeta has consistently beaten estimates during its time as a public company. Although past performance is not indicative of future results, it's still a confidence booster for investors — a well-needed dose during this volatile market environment.

{kind=link}

Valuation

Despite beating estimates, Marqeta sold off more than 24% the following day. Its strong Q2 results were totally eclipsed by the news that Founder Jason Gardner is planning to transition out of his CEO role, becoming Executive Chairman of the company once his replacement is found.

Although this came in unexpectedly, I think the markets might have overreacted here. First, this is a "transition" to another role, rather than an abrupt "departure" entirely. Second, Gardner is the largest shareholder of the company so it is in his best interest to drive shareholder returns. And third, Gardner made it very clear that he'll still be heavily involved in the company.

I'm sharing this with you because I've always valued thoughtful transparency and because this transparency will allow me and the Board to attract, select and hire the best CEO to drive even higher levels of success for our customers, employees and shareholders. Once we hire the next CEO, I will become Executive Chairman. As Executive Chairman, I plan to spend my time in the three areas I can contribute the most: our people, our products and our customers. I'm entirely committed to Marqeta and our overall success forever.

(CEO Jason Gardner, MQ FY2022 Q2 Earnings Call)

But whatever the reasons or rationale, I understand why the markets reacted so negatively to the news — seeing a Founder-CEO stepping down certainly raises a few eyebrows.

That said, let's look at Marqeta's valuation.

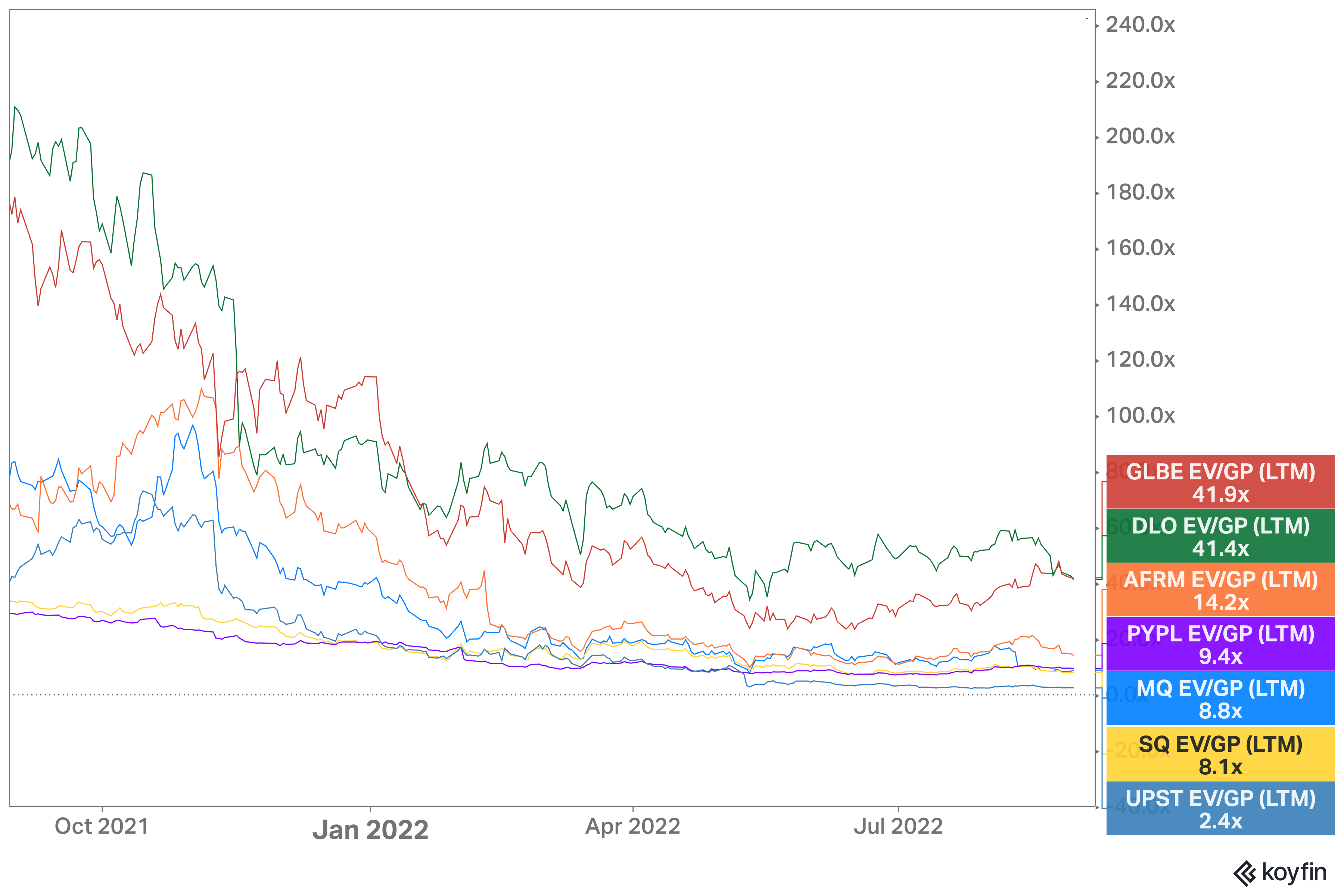

Marqeta currently trades at an EV/Sales and EV/Gross Profit multiples of 3.1x and 8.8x, respectively. In my view, that is pretty cheap for a high-quality growth stock with strong competitive advantages and a long growth runway ahead.

Compared to other fintech companies, Marqeta seems to be attractively valued.

{kind=link}

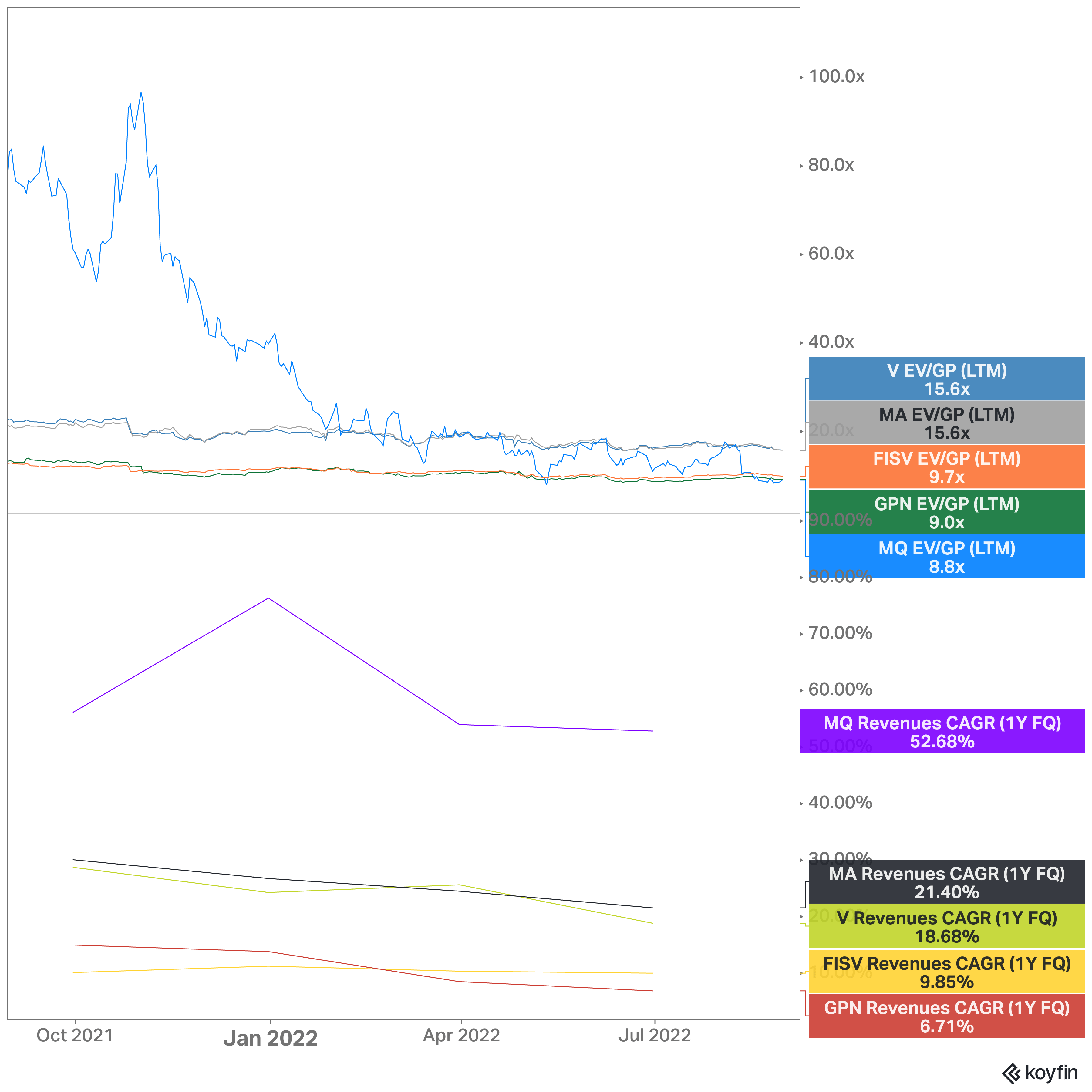

How about legacy payment processors and card networks? Marqeta is valued at the low end of the spectrum while growing many times faster than incumbents.

{kind=link}

Not only that, but Marqeta's Net Cash position represents ~40% of its Market Cap.

Smart money is also accumulating shares on the way down.

Fintel

At its current share price of ~$7.50, I believe the risk to reward is highly favorable for long-term fintech investors.

Risks

- Management Changes : Again, Jason Gardner's eventual exit may be a symptom of a bigger issue. To make matters worse, COO Vidya Peters is leaving the company — some investors might speculate that Peters left because she wasn't given the CEO role. On the bright side, Marqeta recently made a few significant hires, namely Visa veteran Mike Milotich as CFO and ex-Twilio SVP Simon Khalaf as CPO.

- Concentration Risks : Despite a decline in concentration from 72% last year, Block still makes up 69% of Marqeta's Revenue. It also ticked up slightly from 66% in Q1 as a result of its completed acquisition of Afterpay. We got a glimpse of how sensitive Marqeta's stock is to changes in Block's business — the stock flash-crashed by 30%+ when Fidelity National Information Services ( FIS ) announced that it will be powering the Cash App Card. But rest assured, management mentioned that "there's no implication for Marqeta." Still, its contract with Block is set to expire in 2024. If the contract is not extended, then that'll be a major blow for Marqeta.

- Competition : Fintech is a rapidly developing space, and incumbents and startups alike want a piece of the pie. In other words, Marqeta faces stiff competition such as Fiserv ( FISV ), FIS, Adyen ( ADYEY ), Stripe, and so on.

Conclusion

Marqeta continues to execute despite a shaky global economy. While management changes and Block's concentration are concerns, Marqeta is well-positioned to become a dominant player in the rapidly-evolving issuing-side of the payment ecosystem.

The fundamentals of the business continue to get stronger while the stock tanks, presenting a great buying opportunity.

There might be a change in the CEO. But Jason Gardner is entirely committed to the company.

He's not going anywhere.

I'm not going anywhere.

For further details see:

Marqeta: I'm Not Going Anywhere