MRTPY - Marston's: A Call Option On The U.K. 'Pub Culture'

2024-01-21 10:40:00 ET

Summary

- Marston's is focusing on reducing its net debt and improving its balance sheet by selling off some of its real estate assets.

- The company's underlying financial performance has improved, with a strong operating profit and positive free cash flow.

- Marston's is a call option on the UK pub culture and the stabilization and potential decrease of interest rates, which will support the value of its real estate assets.

Introduction

An update on Marston’s ( OTCPK:MARZF ) ( OTCPK:MRTPY ) has been long overdue and I am glad to see the company is pulling itself out of its misery. About six years ago, I argued this UK owner and operator of pubs was focusing on short-term milestones rather than its long-term health as the dividend payments were prioritized. Eventually, reality caught up with the company which was facing a very tough time during the COVID pandemic and the fallout. The debt levels still appear to be very high but the net debt should mainly be seen as mortgage debt secured against the real estate assets (the pubs).

{kind=link}

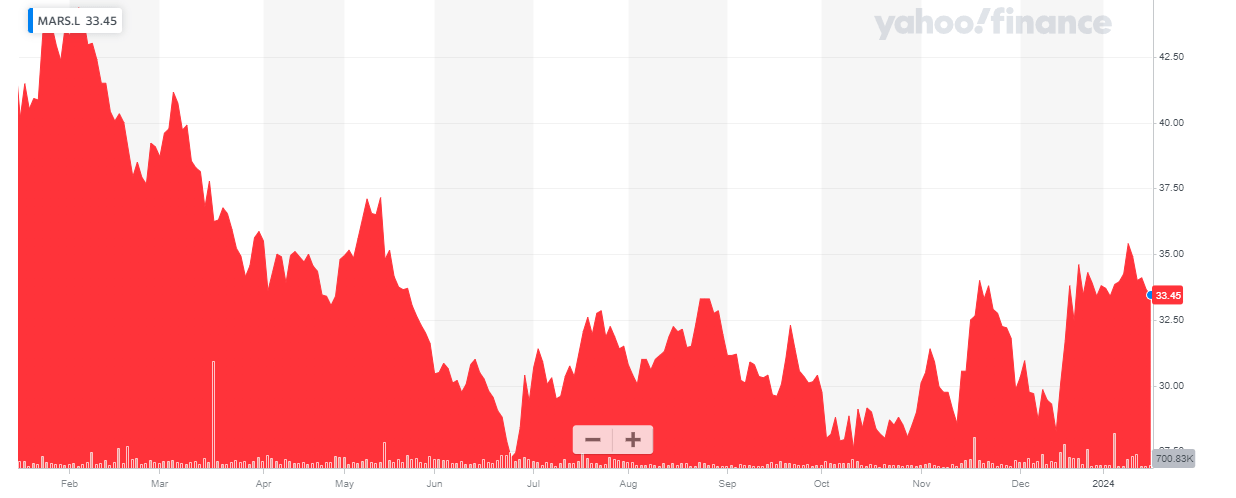

While the company is currently trading at just 33.5 pence, it has approximately 630 million shares outstanding resulting in a market capitalization of approximately 215M GBP (approximately $270M at the current exchange rate). The average daily volume in the UK, where the stock is trading on the London Stock Exchange with MARS as its ticker symbol, is approximately 1.8 million shares per day. This represents approximately 0.6M GBP which is the equivalent of approximately $750,000. I would strongly recommend to trade in the company’s shares using the London listing. And of course, it goes without saying limit orders are strongly recommended for this type of stocks.

This article is meant as a follow-up article on an older article from a few years ago as well as a more recent article published during the COVID pandemic where I discussed the company’s decision to sell a portion of its brewery to Danish brewing giant Carlsberg ( OTCPK:CABGY ).

Marston’s balance sheet got better after the Carlsberg deal, but the company has a long way to go

During the COVID pandemic, Marston’s sold its brewery division to Carlsberg, retaining a minority stake, a move that likely saved the company in 2020. As Carlsberg is currently the operator and manager of the brewing company, Marston’s can just sit back, relax, and rake in the dividends while perhaps waiting for Carlsberg to try to acquire the remainder of the brewery division it doesn’t own yet. I’m not attaching too much weight to the latter scenario as I think it is doubtful Marston’s will see anything close to the book value of 250M GBP , which values the brewery division at almost 25 times net profit (which was 9.9M GBP in FY 2023 ). So for now, I will just assume Marston’s can continue to count on its attributable profit from the brewing division.

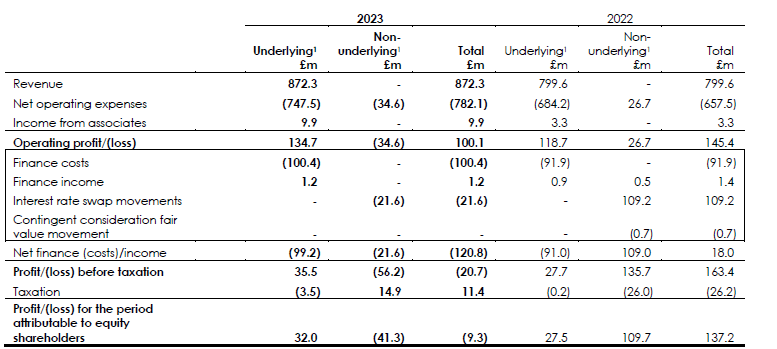

The company’s financial result ends in September and its financial performance shows a remarkable improvement compared to the preceding year. That being said, the exceptional items are pushing the bottom line result into the red territory but the underlying result remains very strong while the positive free cash flow helps the company to rebuild its balance sheet, a million at a time.

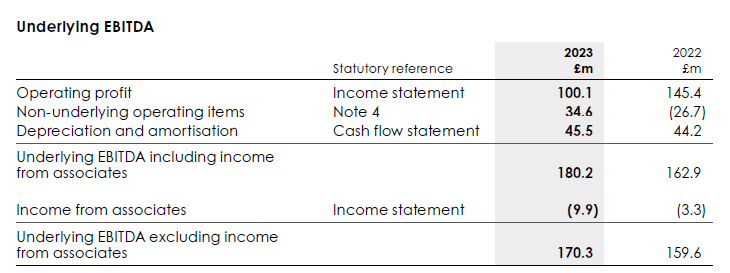

The total revenue increased by just under 10% in FY 2023 while the like for like revenue increased by more than 10% (some pubs were sold and that’s why the like for like result is higher than the reported result). You see there was an operating profit of 100M GBP on a reported basis but the underlying operating profit was roughly 135M GBP before the company recorded an impairment charge.

{kind=link}

On a reported basis, the total net finance cost increased to 121M GBP, mainly due to an increase in interest rate swap revaluations. As the income statement above shows, the total finance costs on an underlying basis increased by approximately 8.5M GBP. A nuisance, for sure, but more than fully covered by the increase in the operating profit.

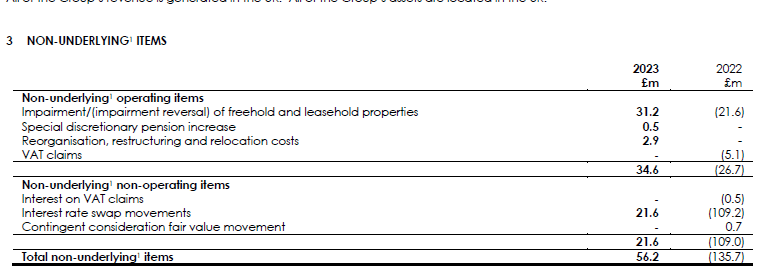

The company also published the details of its non-recurring items (see below). As mentioned before, the impairment charge was definitely weighing on the results and perhaps the most important reason why Marston’s posted a net loss. The impairment charge was related to the value of the real estates, which is subject to a revaluation on an annual basis.

{kind=link}

Perhaps a brief explanation on the £21.6M loss on the interest rate swap movements: the company has posted a lengthy explanation (see below) but to summarize it: the slightly lower interest rates (The UK treasuries saw a YoY rate decrease between September 2022 and 2023. A small decrease but enough to impact the value of the interest rate hedges it had in place) reduce the value of the hedges. And in the shorter duration segment: an increase of market interest rates slightly increases the liabilities. In the end, these hedges will be pretty neutral but they do cause some severe swings every once in a while. In the preceding financial year, there was an unrealized gain of in excess of 100M GBP on these interest rate hedges.

And that’s why the underlying result of Marston’s is tremendously better than the reported result. The underlying net income was 32M GBP which works out to 5.1 pence. Which indeed means the stock is currently trading at an earnings multiple of just 6.7 times the underlying earnings.

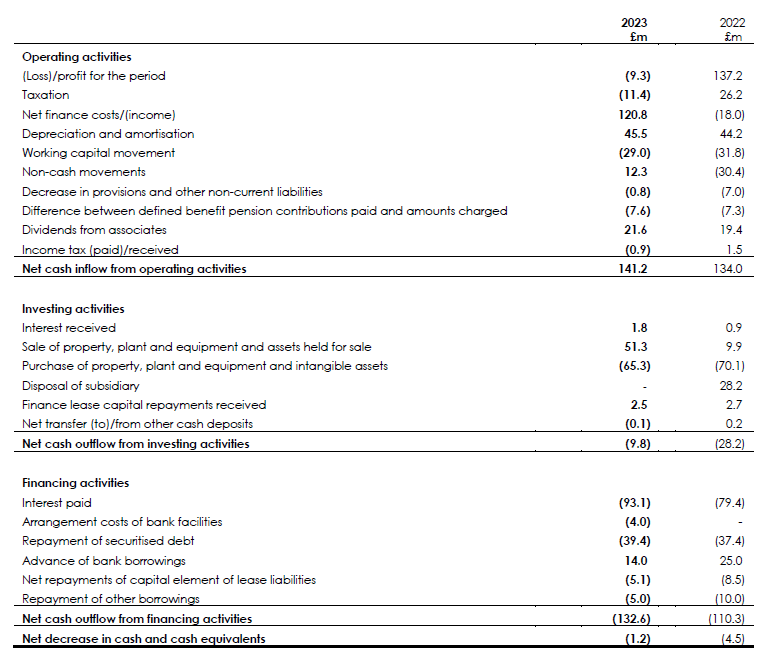

And that result shows up in the company’s cash flow results. The cash flow statement below shows a total operating cash flow of £141.2M but this includes a 29M GBP investment in the working capital position and excludes the 93.1M GBP in interest payments and 5.1M GBP in lease payments. So on an adjusted basis, the operating cash flow was 73.8M GBP after adding back the 1.8M GBP in interest received. Note: the company also paid almost 12M GBP in taxes although it owed less than 5M GBP.

{kind=link}

The total capex was £65.3M which was fully covered by the underlying cash flow, but more importantly, Marston’s continues to sell off some weaker performing pubs and assets, and that brought in 51.3M GBP in 2023. This cash inflow from asset disposals almost fully covered the capex program so I do consider it a pretty good asset rotation program. Kick out the weaker ones, and reinforce the stronger assets. And meanwhile, pay down some debt in the process: during 2023, Marston’s repaid a net amount of 30M GBP of its bank debt and other borrowings which further confirms the company’s focus on reducing its net debt.

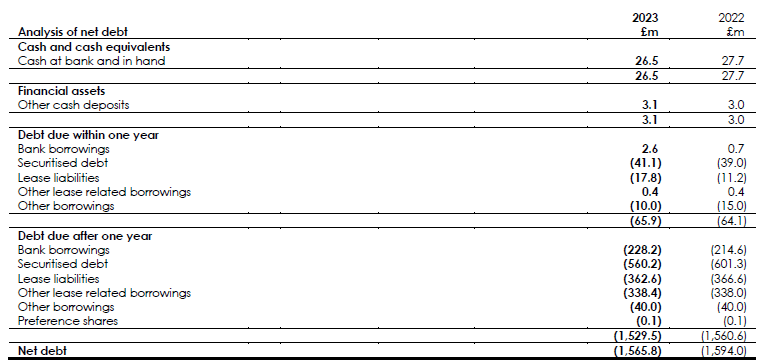

The net debt remains high. As you can see below, the company has to deal with a total net debt of 1.57B GBP which is massive for a company that’s generating just a few tens of millions in free cash flow per year. And as a lot of investors rely on a quick glance at computer-generated metrics and multiples before making an investment decision, it is understandable why Marston’s wouldn’t pass a first glance.

{kind=link}

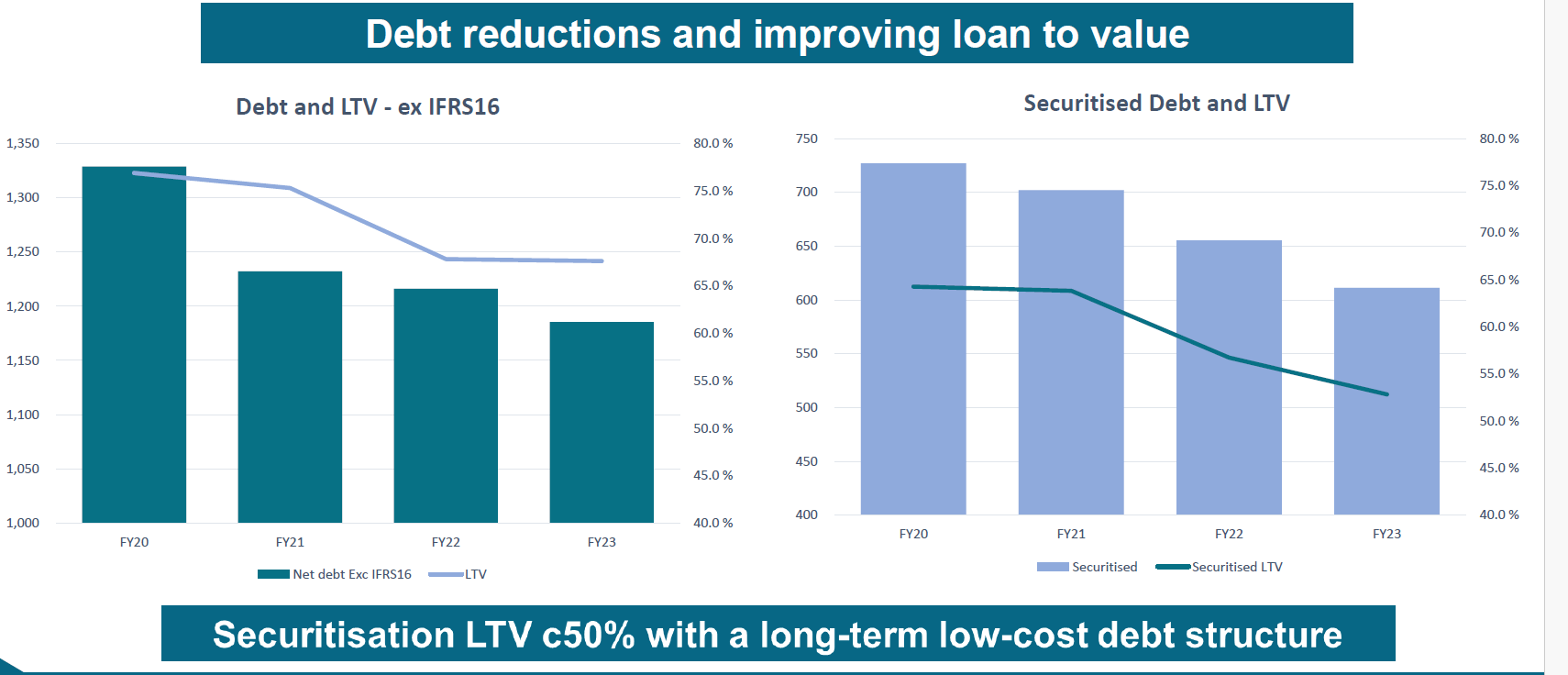

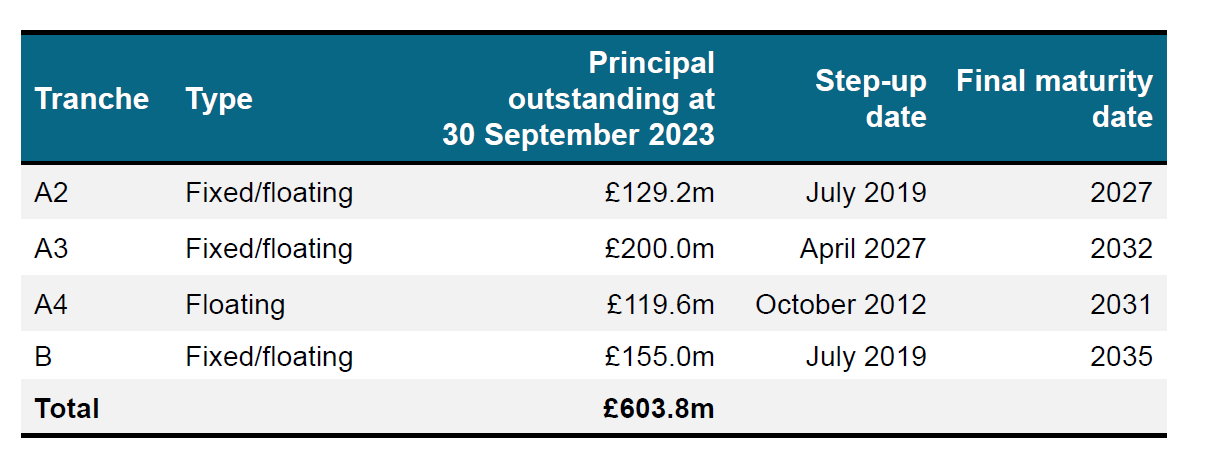

There are however two important elements you need to take into consideration here. First of all, the vast majority of the debt is related to the real estate assets. You’ll see the total amount of securitized debt is decreasing, but that’s because the debt agreements oftentimes stipulate a small annual amortization: the lender is happy a portion of the principal gets repaid every year, and Marston’s is happy as it helped the company to secure a decent interest rate. Securitized debt (secured against real estate properties) for sure is the cheapest debt for the company and as there are still hundreds of properties that are not the subject of securitization, I expect Marston’s to continue to focus on real estate backed loans. The weighted average cost of debt for the securitized loans was 5.1% and that cost of debt has been hedged all the way until the last securitized loan matures in 2035.

{kind=link}

{kind=link}

The real litmus test to see if the real estate valuation is somewhat reasonable are the recent pub sales.

The company reported a net profit of 7.9M GBP on the disposal of the assets in 2023 which seems to confirm the current fair value of the pub assets is reasonable and realistic. The net book value of the real estate assets was 2.065B GBP which means that if you would apply the entire net debt to the real estate value, you’d end up with an LTV of 76%. That indeed IS very high but keep in mind I just painted a theoretical picture. The operating company reported an underlying EBITDA of 170M GBP excluding the income from associates.

{kind=link}

If we would assume the operating company (i.e. the pub operations excluding real estate ownership) is working with a leverage ratio of 2x EBITDA (this is arbitrary, just to explain how we should look at the consolidated debt level), about 340M GBP of the 1,565M GBP net debt would be attributable to the operating company which means the LTV ratio of the real estate related debt is a more realistic 60%. The company does not disclose the breakdown of those debt levels so you should read the explanation above as a ‘theoretical’ division between OpCo debt and real estate debt. And then I have not added the value of the brewery division to either of both.

Marston’s has confirmed no dividends will be payable over FY 2023 as the board wants to reduce the net debt level even further. An understandable decision and I fully agree with this approach.

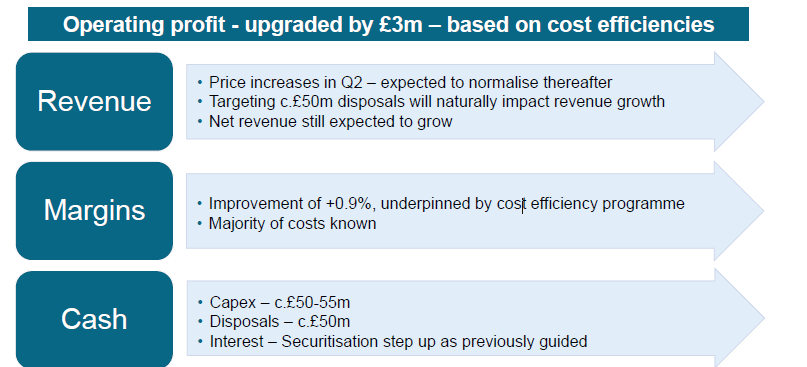

In the current financial year (FY 2024, which ends in September) the company will be hiking prices in the current quarter so the first half of this year might be relatively weak as it will include one quarter without price hikes while H2 2024 should be better. Margins should improve so this will add approximately 10-15M GBP to the underlying operating income. That being said, Marston’s plans to sell an additional 50M GBP of assets. This will reduce the asset base but the lower gross debt and lower interest expenses will compensate for that: while the operating profit will be hit by the asset sales, the net impact should be close to zero once the lower interest expenses kick in.

{kind=link}

Another important element: the cash flow from the asset disposals will once again be sufficient to cover the capex for this year. Which indeed indicates the net debt will decrease again this year, likely by 30-60M GBP (subject to working capital changes).

The company has not disclosed what it really wants to achieve on the net debt level front before it would consider paying a dividend again (it did mention it wants to achieve sales above a billion and borrowings below a billion by 2026, but it will need to step up its asset disposal program if it wants to reduce its debt to 1B GBP by the end of 2026). On an underlying basis and excluding the cash flow impact from asset sales, I’m ending up with a net free cash flow of 25M GBP, despite the aggressive investments in growth and improvements: the depreciation expenses are 40M GBP per year, but Marston’s continues to spend 50-55M on capex. If we would assume the sustaining capex equals the depreciation rate, the underlying free cash flow result would even jump towards 40M GBP or 6.3 pence per share. As Marston’s pension scheme currently has a surplus, the company will likely be allowed to stop contributing from 2025 on. This will save 7M GBP in annual cash outflow, which represents yet another 1.1 pence per share per year.

The risks to the thesis

An investment in Marston’s is also an investment in the pub scene in the UK betting and there are two main risks that could jeopardize the thesis here.

First of all, the pub culture needs to continue to exist. This is an intangible and the pub scene needs to be able to continue to rely on its clientele having sufficient discretionary funds available for a few beers and a night out.

Secondly, the capitalization rates for the pubs should not increase to a high single-digit capitalization ratio. Right now, the assumed cap rate is approximately 6% and while the balance sheet could handle an increase to 7-7.5%, that would be less than ideal. As interest rates are trending downward again, I think cap rate increases will remain relatively limited and this risk can be monitored by keeping an eye on the asset sales program for this year.

Investment thesis

Marston’s appears to have its priorities straight and further reducing the net debt likely is the best decision the company can make. While some other pub operators use an asset-light model, I do like the fact Marston’s has its own real estate empire as it allows the company to run the pubs as it desires while it can always sell some assets (like it is doing now) to support the balance sheet.

Marston’s is a call option on the UK pub culture and on the interest rates stabilizing and perhaps slowly decreasing, which will underpin the value of its real estate.

For further details see:

Marston's: A Call Option On The U.K. 'Pub Culture'