MRTN - Marten Transport: A Turbulent Near-Term Due To Weak Freight Markets

2023-04-24 17:32:43 ET

Summary

- MRTN’s revenue growth should improve in the back half of 2023.

- On the profitability side, the company should benefit from the installation of auxiliary power units to improve fuel efficiency, bring in new tractors and trailers, and moderate fuel prices.

- I have a buy rating on the stock.

About the company

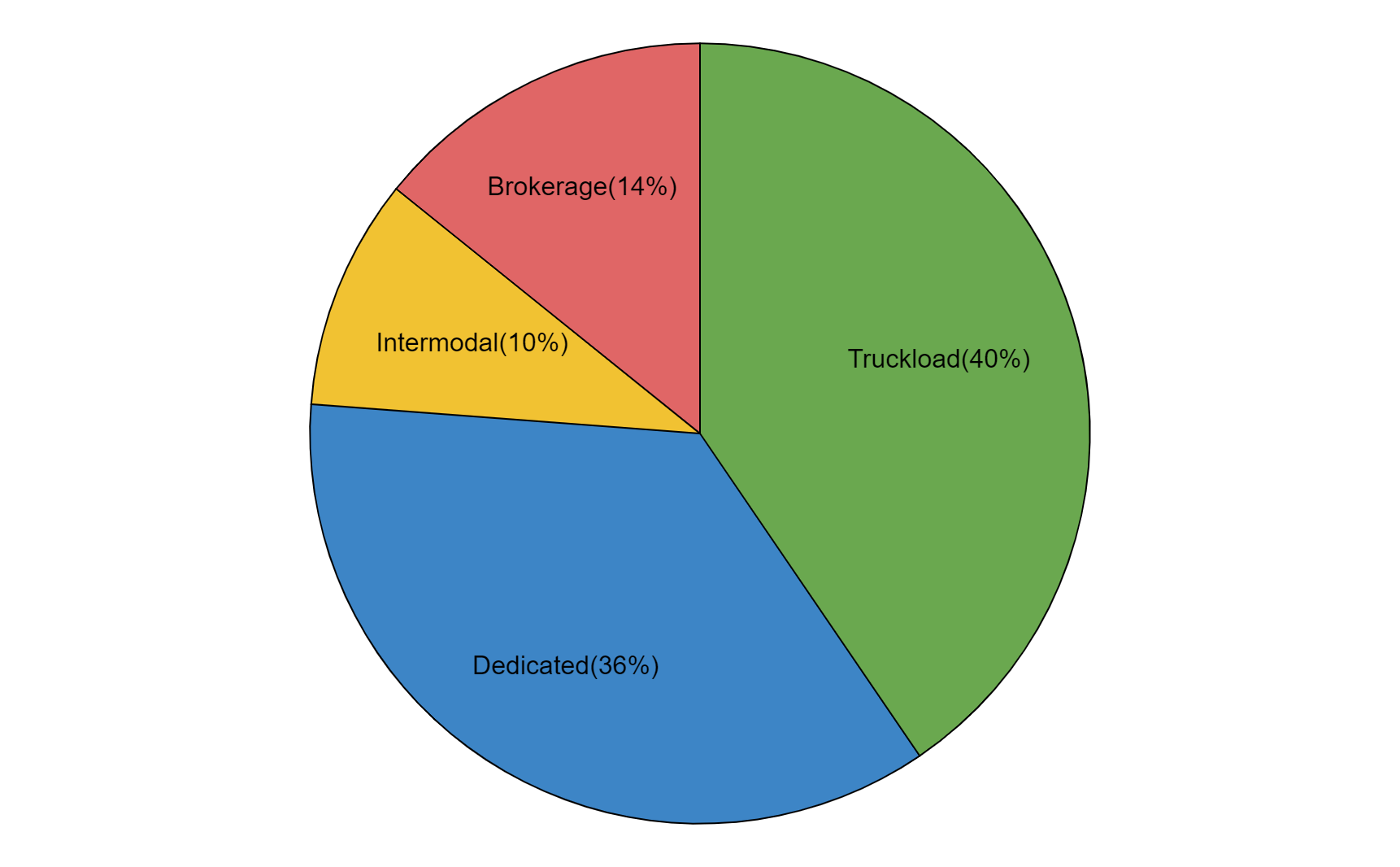

Marten Transport ( MRTN ) is a leading temperature-sensitive truckload carrier, specializing in the transportation and distribution of food and other consumer packaged goods that require a temperature-controlled or insulated environment. The company offers refrigerated and dry truck-based transportation capabilities across its five distinct business platforms - Truckload, dedicated, intermodal, brokerage, and MRTN de Mexico. Approximately 58% of the truckload and dedicated segment’s revenue in 2022 resulted from hauling temperature-sensitive products and 42% from hauling dry freight.

MRTN's segment distribution (Created by DzD Analysis by taking data from MRTN)

{kind=link}

Q1 FY23 Financial Overview

Marten Transport recently reported its first quarter FY23 financial results, which missed the consensus estimates. After announcing the results, this led to a more than 6% drop in the stock price. The company’s revenue increased by 3.7% Y/Y to $298.02 mn but was below the consensus estimates of $309.89 mn. The truckload segment’s revenue, net of fuel surcharge revenue, increased by 7.5% Y/Y to $102.3 mn, due to the increase in miles driven during the quarter, partially offset by lower average revenue per tractor resulting from the increased number of tractors. The dedicated segment’s revenue, net of fuel surcharge revenue, increased by 10.7% Y/Y to $86.8 mn, due to an increase in average revenue per tractor. The intermodal segment’s revenue, net of fuel surcharge revenue, declined by 8.6% Y/Y to $23.4 mn due to the lower loads carried in the quarter. The brokerage segment’s revenue declined by 8.1% Y/Y to $42.3 mn due to a decrease in average revenue per load.

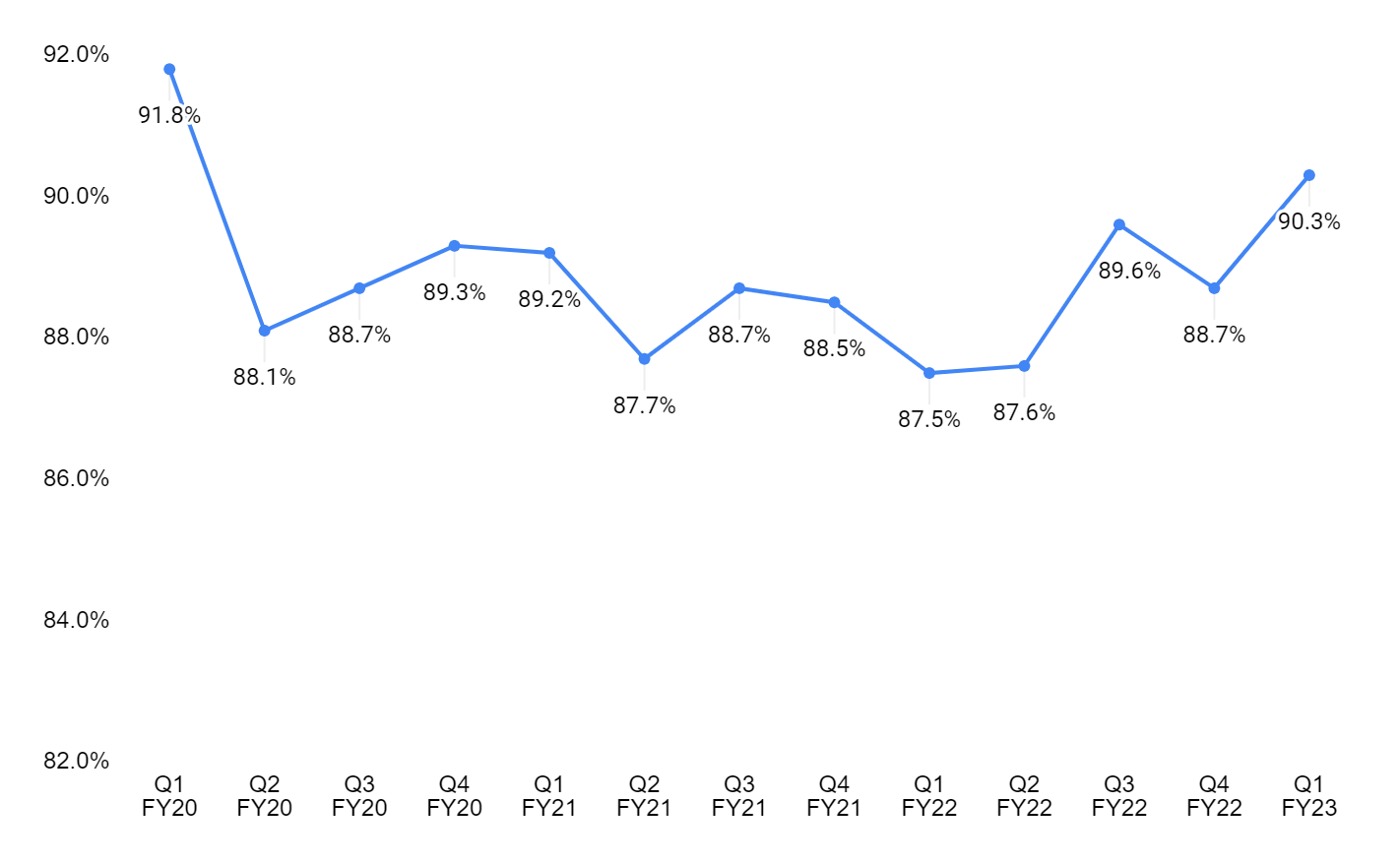

The EPS in the quarter declined by 15% Y/Y to $0.28, which is slightly above the consensus estimate of $0.27. The decline was due to an increase in the operating ratio, net of fuel surcharge, by 320 bps to 88.6%. The increase in operating ratio was due to higher salaries and wages, depreciation of equipment, and insurance and claims. The EPS decline was partially offset by the company’s share repurchase program.

Outlook

MRTN’s revenue has increased over the last few quarters given the increase in demand and rise in fuel surcharges. However, in the next two quarters of 2023, I anticipate a slowdown in revenue growth due to the softness in the freight market caused by weak demand. Nevertheless, MRTN's business of hauling freight for the food industry may not be impacted to the same extent as other transportation companies, as food is a necessary and perishable item that requires regular transportation. This is expected to offset the weakness in other markets, providing a buffer for MRTN. I believe that once the freight market stabilizes, which I expect to happen in the second half of 2023, MRTN's revenue growth will improve. In order to further expand its business, MRTN is also strategically expanding its operations in Mexico. This includes expanding its current operations space in Laredo to accommodate new equipment, as well as acquiring land in the Rio Grande Valley to build a new facility with increased capacity. These expansion efforts demonstrate MRTN's proactive approach to capitalize on growth opportunities and strengthen its position in the market.

On the profitability side, the operating expense as a percentage of revenue (operating ratio) has been increasing over the last three quarters. The increase is due to the rise in fuel costs, wages, depreciation and maintenance of equipment, and casualty claims. The company is employing technology in its operations, which should help the company run its operations more efficiently and improve profitability. Additionally, the company is bringing in new equipment, which will increase the average age of its fleet, leading to lower maintenance costs. To manage the increased fuel prices, the company has installed and is tightly managing the use of auxiliary power units in its tractors to provide climate control and electrical power for its drivers without idling the tractor engine, and it has also improved the fuel usage in the temperature-control units on trailers. For the remainder of 2023, I believe the company’s initiatives and moderation in fuel costs should help improve the operating ratio.

MRTN's operating ratio (Created by DzD Analysis using data from MRTN)

{kind=link}

Valuation

{kind=link}

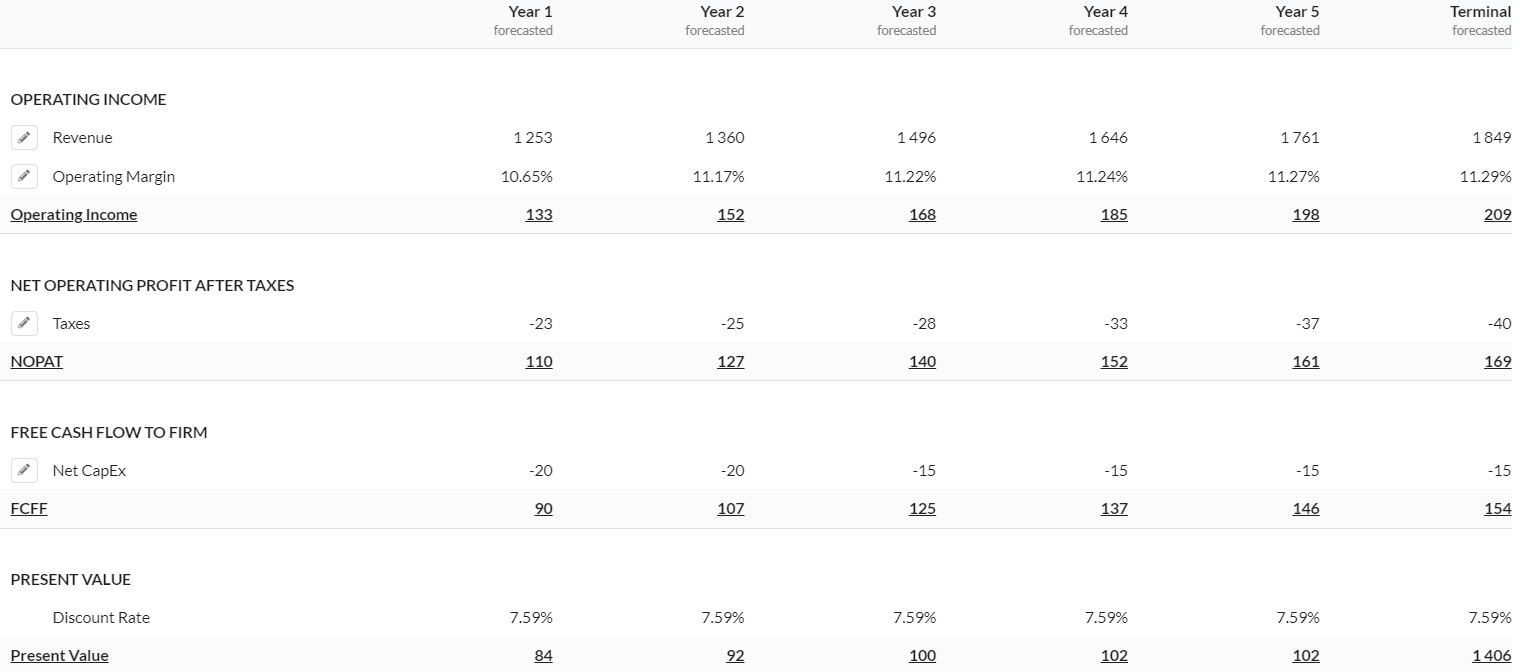

In my DCF calculations, I am assuming revenue growth to be negative low single digits in 2023 given the weak demand in the freight market. Beyond 2023, I have assumed growth to be in the high-single digits, with a terminal growth rate in the mid-single digits, as the company will benefit from the moderation in demand for its services. Management plans to double its capital expenditure in 2023 to bring in new tractors and trailers. I used a discount rate of 7.59% and arrived at a fair value of $24.43 for MRTN.

Using the relative valuation, the stock is currently trading at 16.96x FY23 consensus EPS estimate of $1.23 and 14.33x FY24 consensus EPS estimate of $1.45. This is well below the five-year average forward P/E of 18.14x.

Risks

-

MRTN faces the risk of weak demand in the freight markets due to the higher inventory levels. This will impact the company’s revenue growth in the near term.

-

I am anticipating profitability to improve in 2023 and beyond. However, if fuel prices and labor wages increase, it should significantly impact the bottom line.

Conclusion

In summary, I have a buy rating on MRTN stock despite the weak demand in the freight market. The reason is, I believe once the channel destocking is completed, demand should improve, leading to moderate revenue growth. Additionally, the company is expanding its business, which should further boost revenue growth. On the profitability side, the installation of auxiliary power units to improve fuel efficiency, bringing in new tractors and trailers, and moderation in fuel prices should benefit the company. Hence, I am optimistic about the company.

For further details see:

Marten Transport: A Turbulent Near-Term Due To Weak Freight Markets