SUM - Martin Marietta Materials: Not A Buy Despite Good Growth Prospects

2023-07-11 14:59:19 ET

Summary

- Martin Marietta Materials is expected to see growth due to favorable pricing, robust demand, and increased federal spending through the IIJA and CHIPS Act.

- Despite inflationary headwinds, expected price increases are anticipated to lead to margin expansion for the company.

- The stock's expensive valuation, trading at a premium compared to historical levels, has led to a neutral rating despite promising long-term prospects.

Investment Thesis

Martin Marietta Materials (MLM) should post good growth driven by favorable pricing and robust demand for its products. The company is expected to benefit from increased federal spending through the IIJA and CHIPS Act, as well as its continued focus on reinvestment and strategic acquisitions. These factors are likely to contribute to the company's revenue growth in the long term. On the margin front, while there are still inflationary headwinds, the expected price increases in the latter half of the year are anticipated to more than offset them, leading to margin expansion.

The only problem I see with the stock is its expensive valuation. Since my last bullish article on the company in April, the stock has appreciated over 22%. Currently, the company's stock price is trading at a premium compared to its historical levels. While the long-term prospects for the company appear promising, the premium valuation of the stock makes me uncomfortable in giving a buy rating at this time. So I'm moving to a neutral rating.

Revenue Analysis and Outlook

In my previous article, I talked about the company's good growth prospects driven by pricing and demand momentum. The company has reported its first quarter results since then and the company's revenue in the first quarter of 2023 experienced a 10% year-over-year growth, reaching $1.35 billion. This growth was primarily attributed to strong pricing and sustained robust demand, which outweighed the negative impact of shipment declines caused by historically wet weather in California.

Analyzing the results by product category, all of the product lines except for the Ready Mixed Concrete category reported positive year-over-year growth during the quarter. The Ready Mixed Concrete category, on the other hand, experienced a decline of 24.4% compared to the previous year, primarily due to the divestiture of Colorado and Central Texas operations.

MLM Revenue (Company data, GS Analytics Research)

Looking ahead, the company should continue to benefit from strong demand for its products, which will support revenue growth. The company's revenue should be further bolstered by a healthy customer backlog and the positive impact of carry-over pricing, as well as further price increases in the latter half of the year. These factors should outweigh any negative impact from weakness in the residential and light non-residential end markets.

The demand for products related to the infrastructure end market is expected to remain largely insulated from the broader macroeconomic challenges. This is primarily due to the record government contract awards, which serve as a leading indicator of future demand. According to management , in the 12-month period ending on March 31, 2023, the value of State and Local government highway bridge and tunnel contract awards grew by 16% year-over-year, reaching a record $104 billion. This growth is primarily driven by enhanced federal investment from the Infrastructure Investment and Jobs Act (IIJA), which should further drive revenue growth for the company in the future.

Furthermore, the Cornyn-Padilla Amendment signed by President Biden in 2023 allows states and local municipalities to allocate unused COVID-19 funds for infrastructure projects. This is expected to provide an additional $40 billion of infrastructure funding to MLM's top 10 states, further supporting the company's revenue in the infrastructure end-use market in the long term.

The heavy non-residential industrial projects, led by energy investments, onshore manufacturing, and data centers, are also expected to continue driving demand for the majority of the company's total non-residential shipments. The large project pipeline remains robust, and the estimated aggregate requirement for key Gulf Coast petrochemical projects has increased by 33% from the end of last year till the time MLM reported Q1 results in May. Additionally, the growth in electric vehicles, related battery plants, semiconductors, and other critical products and domestic manufacturing projects, supported by enhanced federal investment from the Inflation Reduction Act and CHIPS Act, should further benefit the company's non-residential business in the long term.

While the residential end market is somewhat of a soft spot, the decline in housing starts has been less than feared, and in May housing starts returned to y/y growth. The sentiment among major public homebuilding remains positive and, once the interest rate peaks over the next few months, this market should bottom and we should return to growth in FY24. This along with the long-term secular tailwind from a structural housing deficit resulting from a decade of underbuilding, should drive demand for single-family homes across MLM's key geographies, leading to revenue growth in the coming years.

In addition to these factors, the company plans to maintain its focus on the disciplined execution of its strategic plan for growth through reinvestment in the business and strategic acquisitions. The company's sound financial position, with a net leverage ratio of 2.4x at the end of the first quarter within the target range of 2x to 2.5x, should further support its revenue growth in the long term through investments in the business as well as inorganic growth.

Margin Analysis and Outlook

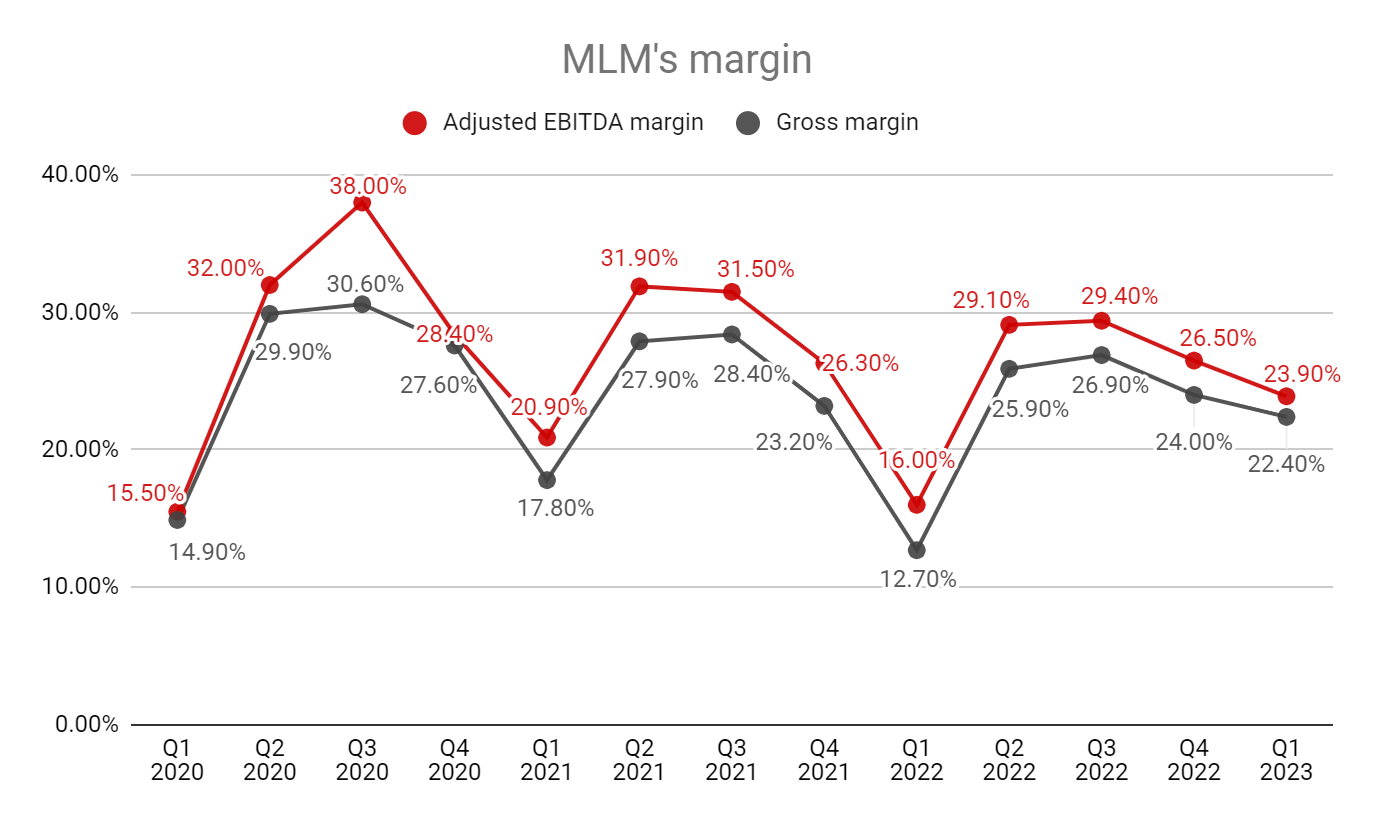

The company's adjusted EBITDA margin experienced a significant expansion of 790 basis points year-over-year, reaching 23.9%. This growth was primarily driven by the positive effects of strong price realization and the implementation of a value-over-volume commercial strategy. These factors successfully offset the negative impacts stemming from ongoing inflationary pressure during the first quarter of 2023.

{kind=link}

Looking ahead, while some impact of inflationary headwinds still remains, diesel prices in the U.S. are coming down, which should help reduce freight costs. Further, the company is also planning mid-year price increases. This, coupled with a significant contribution from the higher-margin Southeast market driven by robust aggregate demand, should help the company in more than offsetting the negative impact of inflationary pressures for the rest of 2023. As a result, I expect margin expansion in 2023 and beyond.

Valuation and Conclusion

The company's stock is currently trading at a forward price-to-earnings (P/E) ratio of 27.71x based on FY23 consensus earnings per share ((EPS)) estimates of $16.02. This valuation represents a premium compared to its 5-year forward P/E of 25.81x.

The company is also trading at a premium to its peer Summit Materials ( SUM ), which is exposed to similar end-markets, based on consensus FY23 and FY24 estimates .

The company's revenue is expected to continue benefiting from robust demand for its products and strong pricing. Moreover, with the increased level of investment from the IIJA, the Inflation Reduction Act, and the CHIPS Act, the company's longer-term revenue outlook appears favorable. Additionally, the margin is anticipated to benefit from strong pricing and the company's ongoing focus on commercial and operational excellence in the coming years.

However, despite the positive prospects for the company's long-term growth, the current premium valuation limits the upside. Hence, I am moving to the sidelines and have a neutral rating on the stock.

For further details see:

Martin Marietta Materials: Not A Buy Despite Good Growth Prospects