MARUY - Marubeni: Agri Business And Coking Coal Pressures

2023-12-19 07:46:28 ET

Summary

- There continues to be pressure on some of the commodity businesses, which weighs on results.

- The agricultural products business is by far the weakest of the major businesses, and it is driven by enduring S/D pressures as compared to before COVID-19.

- Nonetheless, the valuation is attractive, and the company has quite dramatic capital allocation plans.

- Still, we prefer the Japanese mid-cap and small-cap universe.

Marubeni (MARUF)(MARUY) continues to demonstrate some cyclical qualities as pressures are maintained as of the close of the last quarter on the metals and agri business. The situation is at a more normalised level now, and there isn't too much incremental pressure. Moreover, Marubeni is looking to allocate the proceeds from Gavilon which it sold in October 2022, and in general they seem to be getting a little more aggressive in their plans to keep rotating their portfolio. While Marubeni is interesting, we still think that there is more upside in the relatively safe Japanese mid and small cap space where there are more opportunities that have still not re-rated on corporate governance changes like Marubeni has, so it's a pass.

Earnings

The following are this quarter's figures.

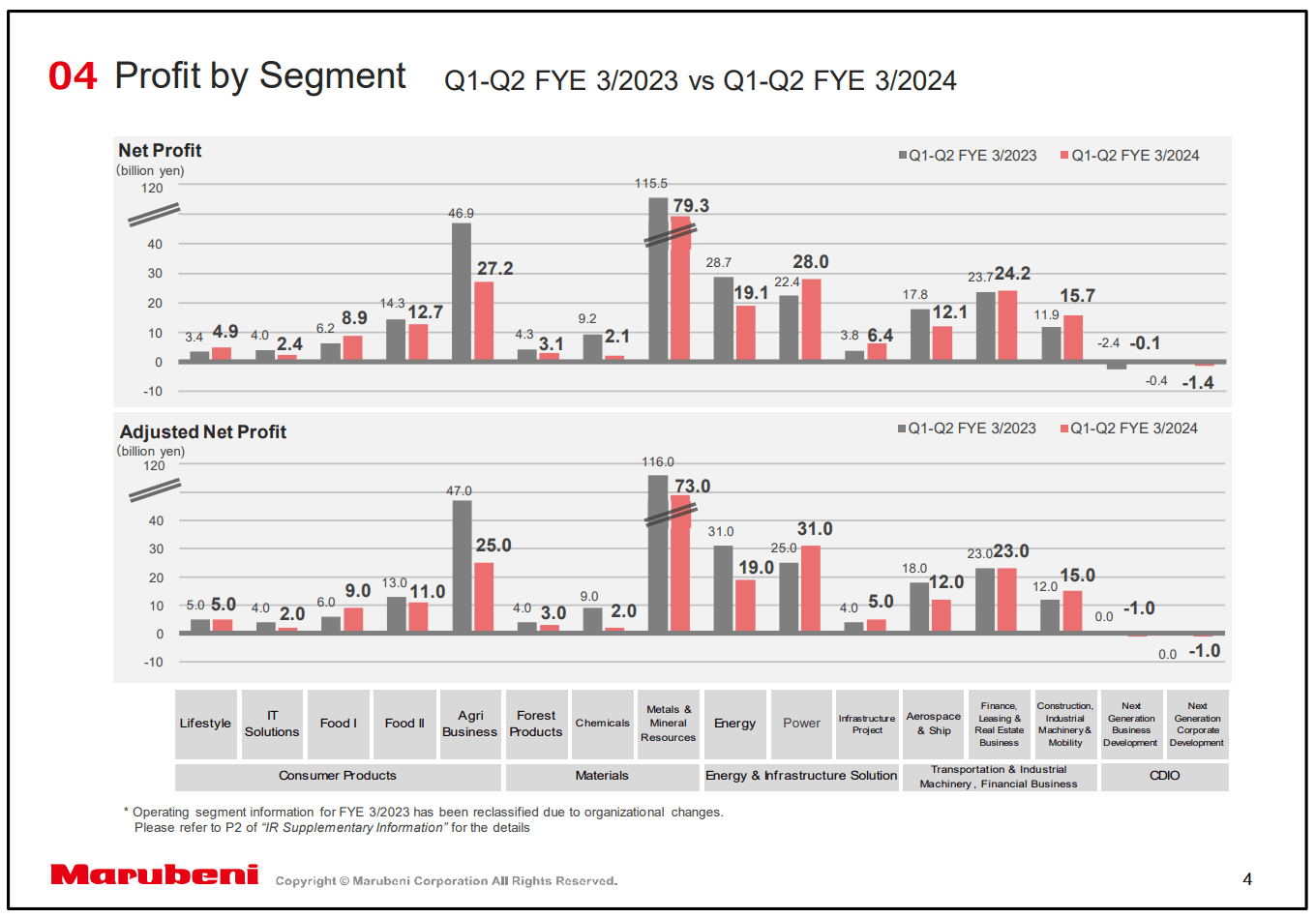

Latest Segment Results (Q2 Pres)

{kind=link}

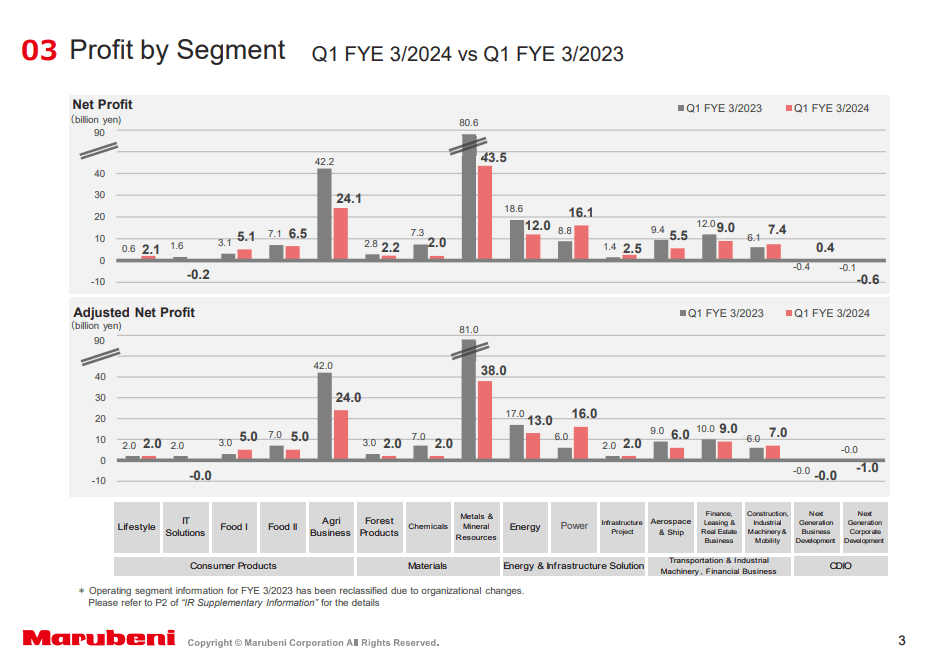

And the following are last quarter's figures, which we commented on in our last article.

{kind=link}

Beginning with the Agri business, which includes US businesses focused on crop protection chemicals, things look sequentially a little rough. The reasons for this are that the impacts of the end of COVID-zero in China and the associated supply side growth are weighing on the segment's price realisation and profitability. This is a bit of an enduring situation, where China has mounted substantial amounts of its own production in the last few years causing a permanent shift. Our rule of thumb is that factories take around 2-4 years to build, and the production, with some COVID delays is now up and running and creating a glut in the market.

The other segment that also saw some notable declines is metals and minerals. It was worse last quarter, but there are still difficult comps in the segment as demand continues to be quite weak for coking coal and prices are low YoY. We are more worried about this segment due to major demand sinks like China, compared to the Energy segment where the comps are simply very difficult in their E&P businesses. With the reserve-filling now over by the US, the Saudis might come out of their break and continue to cut supply to raise global energy prices and use that leverage on the market.

Nonetheless, at least some signs of letting up in major demand sinks like the US thanks to the beginning of the pivot, although it's not clear how bullish this signal will really be, means that Marubeni should be getting into better territory on an incremental basis.

Bottom Line

Looking forward, investors should be focused on the cash that came from the Gavilon divestment, which accounted for about 10% of market cap . CAPEX forecasts as well as shareholder distribution forecasts have each grown considerably more than 10%, and in the Q&A , the management has struck a tone of being more willing to take risks in the current environment, which they believe provides ample opportunities for portfolio rotation.

Improvements in the funding environment and also a relatively strong debt capacity both lend themselves to myriad possibilities to continue to drive returns. However, you can't expect better that basic industrial returns from Marubeni since they are on the private markets where multiples are still rich and there is massive competition to allocate dry powder.

The PE is around 7.5x which offers ample earnings yield. However, there are lower multiple businesses in Japan with objectively better economics. Moreover, in terms of trading dynamics, there are many small and mid cap stocks in Japan that have yet to rerate, with better economics and lower valuations. Marubeni is good but others are better.

For further details see:

Marubeni: Agri Business And Coking Coal Pressures