MARUF - Marubeni: Choose Buffett's Japan Pick As Good Times May Be Over In America

2023-05-11 06:01:06 ET

Summary

- Warren Buffett has painted a gloomy picture for Berkshire against the backdrop of a slowing U.S. economy.

- At about the same time, he has ramped up investments in Japan's Sôgô Shôsha including Marubeni.

- I look at the reasons for this, by using some of his own insights like "Never invest in a business you cannot understand".

- I target a 20% upside, after applying some moderation given the current uncertain market conditions.

- I also justify my bullish stance through a comparison of valuations and returns with Berkshire itself.

Last Saturday, May 6, Warren Buffett, the Chairman and CEO of Berkshire Hathaway ( BRK.B , BRK.A ) gave a gloomy forecast for his conglomerate, and given that its businesses are present in most sectors of the economy, this does not bode well for America's economic health in general. Tellingly, less than one month back on April 11, news broke out that he had incremented his positions in Japan's five largest trading houses which include Marubeni Corp ( MARUY , MARUF ), Itochu Corp. ( ITOCF , ITOCY ), Mitsubishi Corp. (MSBHF), Sumitomo Corp. ( SSUMF , SSUMY ) and Mitsui & Co. ( MITSY , MITSF ) to 7.4% after initial investments in August 2020.

Now, as the "Oracle of Omaha", he is someone who investors listen to attentively and try to emulate his stock picks. Therefore, it is worthwhile to analyze the reasons which motivated his choice which is precisely the aim of this thesis, while at the same time, I assess whether it is appropriate to buy the Japanese stock now that it is at an all-time high at $144 level as per the chart below.

First, I make a comparison between Buffett's conglomerate and the Sôgô Shôsha , or the name given to Japan's five largest trading houses which shows that the value investing Guru has been faithful to his own insights during stock picking.

Warren Buffett: Never Invest in a Business you cannot Understand

As I elaborated in a previous thesis on Itochu last week, these five trading houses are collectively referred to as the Sôgô Shôsha, having their origins in the particular way in which corporate Japan evolved after the Second World War. Thus, in the 1945 postwar period trading activities were heavily controlled by the U.S. and its allies, and free trade returned only in 1950. Subsequently, there was a significant number of acquisitions giving rise to the Sôgô Shôsha like Marubeni involved in a wide range of business activities, somewhat similar to Berkshire which does everything from insurance, and railroads to electric utilities and retail.

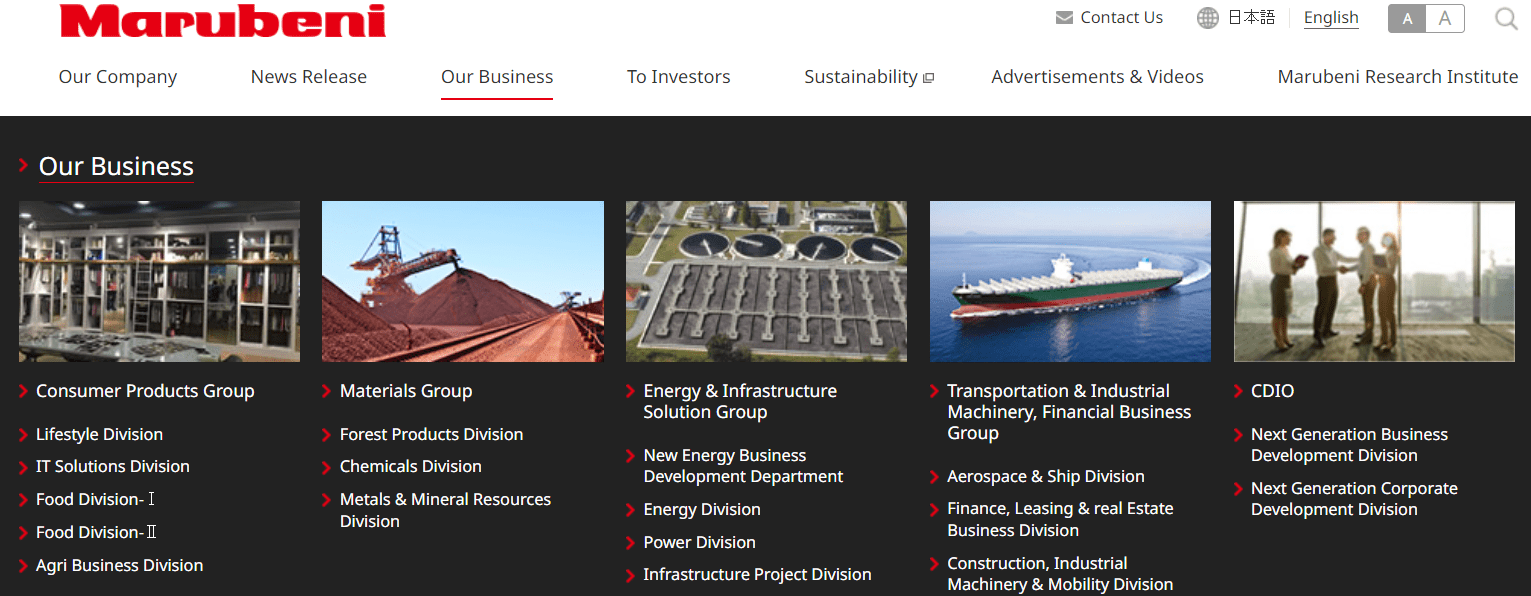

As for Marubeni, with a market cap of $24 billion, it is structured into five groups as pictured below, that trade everything from cereal to paper pulp and provide IT solutions as well as mine minerals. The conglomerate also engages in the production and sales of energy, and delivering infrastructure works.

Business Groups (www.marubeni.com)

{kind=link}

Thus, there are similarities with Berkshire, not necessarily in terms of the business functions, but more as to the highly diverse nature of individual businesses and the fact that they are all managed under one roof.

Coming back to why Buffett chose Marubeni, here, one of his seven insights comes to mind which reads as "Never invest in a business you cannot understand". Thus, this may be a stock located in faraway Japan but, with experience gained managing Berkshire, the billionaire certainly has a grasp of how things are done in such businesses, which it must be said can be beyond the grasp of most investors simply due to the complexity involved.

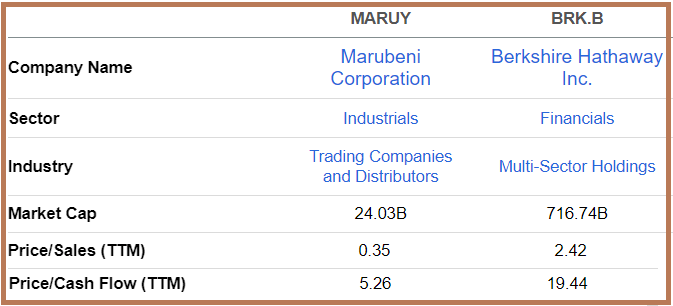

For this matter, the stock is classified under the "Trading Companies and Distributors" industry as illustrated below but it is more structured like a "Multi-Sector Holdings" group just like Berkshire.

Comparing Key Metrics (seekingalpha.com)

{kind=link}

Now, looking from the risk perspective, a group owning businesses that are completely different from each other also provides for diversification, an important criterion during uncertain times. Along the same lines, while being a U.S. ally, Japan entails fewer geopolitical risks than Taiwan.

Geopolitics, Undervalued Stocks and Finances

In this context, the billionaire drastically reduced his stake in Taiwan Semiconductor Manufacturing ( TSM ) in February, due to the rise in geopolitical tensions between China and the United States while betting more money in Japan tends to show that he has a preference for safer regions. Now, as an island located in the Pacific Ocean, Japan is indeed safer, but progress has also been made in Tokyo's role as a financial center. Thus, as of 2013, reforms have been carried out in corporate governance, namely for independent oversight at the board level. While more progress remains to be done, these changes have been welcomed by the international investment community, thereby improving the country's investment outlook.

There is also the added advantage of Japanese equities are relatively attractive for an internationally diversified investor.

An example is Marubeni with a trailing price-to-sales ratio of 0.35x, or nearly seven (2.42/0.35) times lower than Berkshire's 2.42x. Furthermore, the Japanese conglomerate's trailing price-to-cash flow multiple is also lower, by 3.7 (19.44/5.26) times. Thus, using the cash flow metric, Marubeni could potentially climb to $535.5 (144.73 x 3.7) based purely on a comparison with Berkshire and on the current share price of $144.73. However, being modest and assuming an increment of 1.2 times instead of 3.7 times from its present value, I have a target of around $173.7 (144.73 x 1.2).

This represents a 20% upside which is more reasonable given current market conditions and considering Marubeni's financial results for FY-2023 which ended in March this year.

For this purpose, revenues were up by 8% mainly due to higher energy prices and agribusiness, especially food. As for gross trading profits, there was an increase of 17.4% Y-o-Y thanks to higher sales of both wholesale and retail power, as well as better oil and LNG pricing. These were slightly offset by the divestiture of U.S-based Gavilon's grain business on which I elaborate later. As for the bottom line, operating profits increased by 19.8% due to better performance of the leasing and power businesses, but this was slightly offset by lower deliveries in forest-based products.

However, looking forward, the group expects FY-2024's results to be pressured by lower commodity prices as a result of an uneven recovery in China which is seeing consumption led by the services sector than uptake in manufacturing. Also, the group expects less consumer spending from the U.S. as a result of higher inflation and monetary tightening.

Profitability and Debt

Thus profits are expected to be 22.7% lower in FY-2024 than in 2023, somewhat like the majority of Berkshire's businesses which are expected to report lower earnings this year.

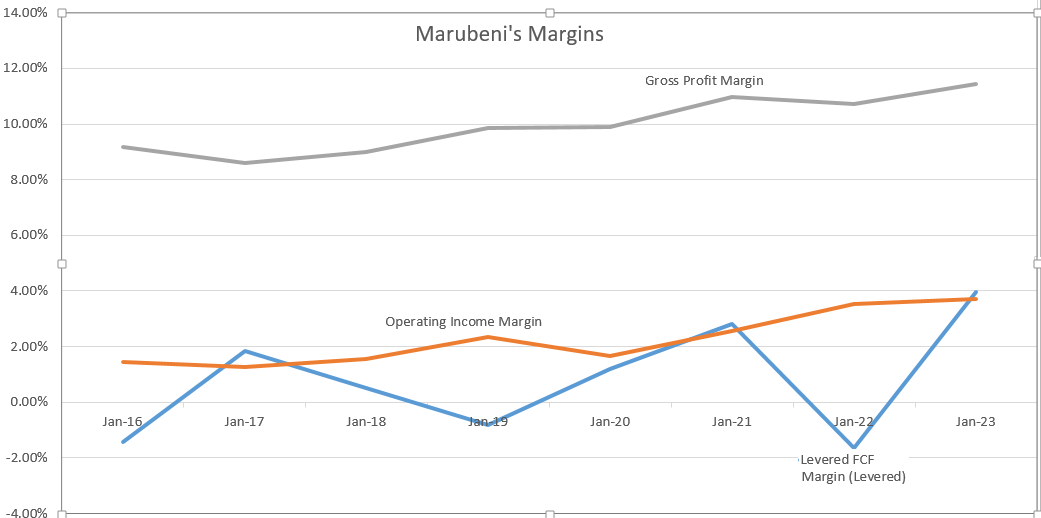

Still, looking at the trend, both Marubeni's gross and operating margins have been on a sustained upward path since 2016 as shown in the grey and orange charts respectively.

Charts Built using data from (www.seekingalpha.com)

{kind=link}

The levered FCF margin chart is also shown in blue, and despite fluctuating widely for the last six years shows a net progression. Again performing a comparison of the FCF margin with Berkshire's -3.56% (table below), Marubeni's 3.95% is much better.

To this end, the higher free cash flowing into the group's accounts has been mostly helped by the 156.8 billion yen generated from financing activities due to the Gavilon divestiture, but with 603.6 billion yen of operating cash flow resulting in an FCF of 763.1 billion yen, Marubeni remains a cash-generating business, enabling it to reduce its debt.

Thus its debt-to-equity ratio has decreased from 0.83 in fiscal 2022, to 0.52 this year after it repaid some borrowings including bonds. This is a big reduction and is positive when navigating uncertain market conditions. Furthermore, with its profitability likely to take a dent in fiscal 2024, the group has offloaded some assets in the form of the grain and ingredients segment of Gavilon as I touched upon earlier, done as part of a restructuring and resulting in at least $1.125 billion flowing into Marubeni's balance sheet.

Justifying the Target Price Considering Risks

Thus, the Japanese Sôgô Shôsha has strengthened its balance sheet which makes it a buy for risk-averse investors. Still, some could wait for retrenchment to the $138-140 support range, and, to justify my bullish stance, Marubeni also does share buybacks and has a progressive dividend policy . Thus, from April 1, 2022, to March 31, 2025, the initial yearly amount set for distribution to shareholders is 78 yen ($0.58) per share. This is not much but the policy states that the dividend is either maintained or increased subject to profits, not reduced.

Talking profits with respect to the longer term, one key metric is the Return on Equity (RoE) which measures how well a company is generating returns (profit) for its shareholders, and here, Marubeni scores the highest. Normally, a figure between 15-20% is considered good, and, with a score of 20.78%, it means that the management is good at generating benefits for investors.

Comparison of Metrics (www.seekingalpha.com)

{kind=link}

On a more cautionary note, with the interconnection of investor communities through technology, rules-based trading, and funds flowing rapidly from one place to another, stock market fluctuations in one part of the world, whether on the upside or downside can be rapidly contagious to another part of the world. In these circumstances, do not expect Japan's stocks to be sparred in case the S&P 500 were to fall below 4000 which means that investors should be prepared to suffer from capital depreciation.

Conclusion: Buffett's Pick is a Buy

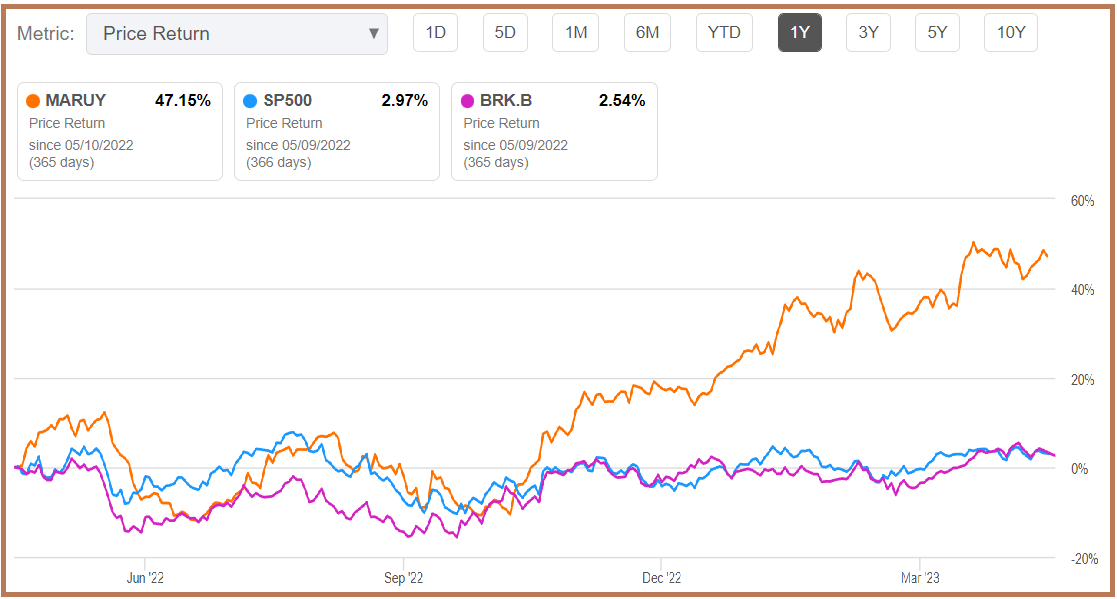

Still, as shown in the chart below , Marubeni has been outperforming both Berkshire and the S&P 500 since November of last year when it became obvious that the three successive 75 basis points hikes brought by the Federal Reserve since March 2022 would not be enough to tame inflation. More recently, U.S. CPI is slightly down Y-o-Y, but tight monetary policy has already caused cracks to appear on the liquidity front as seen with the banking turmoil while risks of an economic slowdown have gone up.

Comparison of Performances (seekingalpha.com)

{kind=link}

On the other hand, inflation remains relatively lower in Japan, or 3.2% in March compared to both the U.S. and Europe. Therefore, its central bank is under no immediate pressure to tighten its ultra-low interest rates which means that there is no danger to the real GDP growth of 1.3% for 2023 coming from monetary policy.

In conclusion, through comparison with Berkshire and to some extent with Itochu, this thesis has shown that Buffett's pick is a buy even at current levels. To further substantiate my position, the stock has a valuation grade of B- and is at least 60% undervalued relative to the sector based on price-to-earnings multiples implying the target of $173.7 remains moderate, but is justified given the risks lurking on the horizon.

For further details see:

Marubeni: Choose Buffett's Japan Pick As Good Times May Be Over In America