MARUF - Marubeni Corporation: Commodity Exposures Reflected In Valuation Considering Outlook

2023-08-07 03:08:49 ET

Summary

- Marubeni's exposures are still very commodity exposed, reflected in how their results have tracked the general commodity deflation we've seen.

- China continues to be a drag on results and may continue to underperform expectations, especially in real estate for steel demand.

- The jury is still out on the US economy, and a shrunken US wallet could be the next shoe to drop.

- The multiple has expanded over the last half-year to what is now a fairer valuation. Not as compelling anymore.

Marubeni ( OTCPK:MARUY )( OTCPK:MARUF ) has traded up a lot since we last covered them. We thought they seemed pretty undervalued at the time, but the appreciation changes the function a little, especially as we continue to be concerned with what might happen in global markets which determine the demand for the major commodity exposures in Marubeni. On the basis of our economic view and the fact that funds can be rotated into cheaper Japanese equities, we aren't that crazy about Marubeni.

Quarterly Results

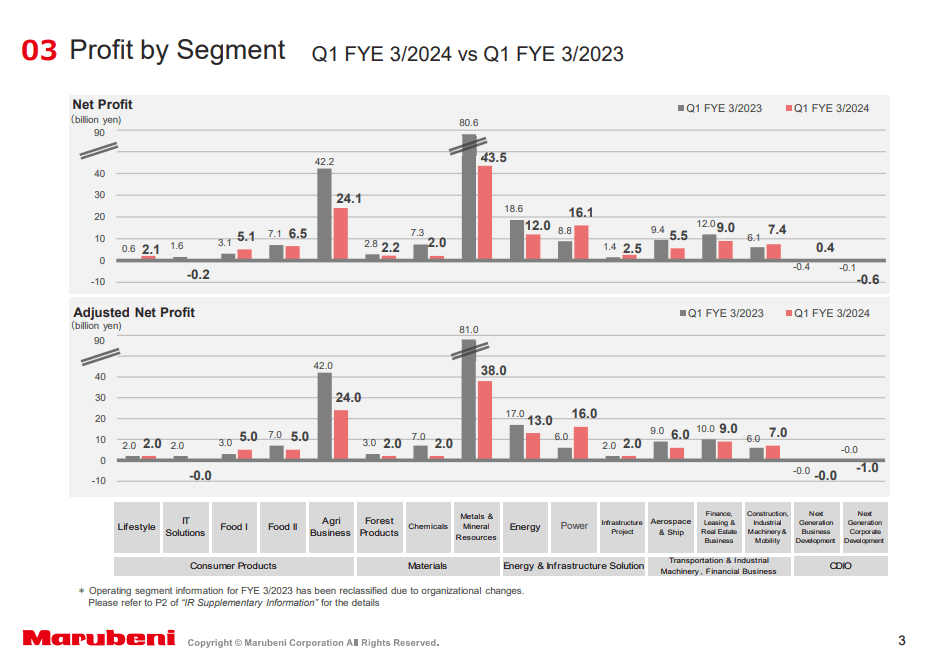

In our last article , we broke down some of the key Marubeni exposures. The ratios have changed a lot, mainly because Marubeni has a lot of commodified and volatile exposures . The energy business is pretty levered to gas and oil prices. We are pretty optimistic about both of these commodities due to structural factors on an ongoing basis, but results are down YoY in this segment.

{kind=link}

The bigger issue is their metals business which was around 40% of their exposures now around 30%. Steel prices and coking coal prices have come down meaningfully as a results of shrinking in the global steel wallet. In particular China is a problem for steel prices in global markets where construction is weak and development is a severely impaired industry. While US markets remain resilient, there are still risks that the last leg of inflation will be much more stubborn than what came before. In fact, it is likely that malignant inflation from supply chain issues has been digested and deflated comps have been for the most part lapped as of now. The remaining inflation is likely to be more related to greed and pricing propagating throughout the US and global economies. If that proves stubborn, the Fed is unlikely to hesitate in raising rates further, as the 2% maximum inflation target appears to be non-negotiable. The key US wallet could take a hit if rate hikes are to continue, and markets would broadly suffer.

There's quite a big agribusiness within Marubeni, that should do pretty well considering food security concerns that have been recently exacerbated by Russian strikes in Ukraine, but again these are basic products that ultimately are exposed to inflation in their production as well as generally high end-price volatility which has been to the downside lately, highly sensitive to reopened capacity and other difficult to predict elements. The power businesses is a generation focused business, but they depend on power prices which are pretty correlated to resources like gas. We happen to have a pretty optimistic view on gas given the risk of a cold winter incoming and therefore on electricity prices, and investment into growing capacity in this business as well as strong price realisation YoY in their wholesale business overseas has delivered some great results.

Bottom Line

Excluding power which is doing well, that's 60% or so of the exposures already accounted for. While oil and gas markets are a little more independent from the demand situation due to structural support from the supply side (not much incremental downside), and these influence about 20% of the business or so, the rest of it in steel, coal, and agri is quite levered to assets that still have some downside if the US wallet has to shrink for the Fed to be satisfied, and continued underperformance in the Chinese economy which is another legitimate concern, although things are likely to rebound to some extent from this trough which has already lasted about as long as most bear market cycles. The exposures are commodity, and the expansion of the multiple from around 5-6x to almost 8x reflects a revaluation of the company to a more fair value. There are some more solid businesses in the remaining 40% including power are businesses whose economics are a little more predictable, but they aren't super recession resistant either. There isn't really a strong value case anymore for Marubeni specifically, and would prefer to aim for the same exposures but as pureplays in more obscure recesses of the market.

For further details see:

Marubeni Corporation: Commodity Exposures Reflected In Valuation Considering Outlook