TSM - Marvell Technology And The AI Hype Cycle

2023-07-10 04:08:21 ET

Summary

- AI hype cycles regularly occur since the 1950s, often overestimating AI's potential. Yet they still push this multi-generational project forward.

- The latest hype cycle, fueled by generative AI, has led to increased investment and demand for Nvidia's GPUs, leaving scraps for other hardware manufacturers.

- Marvell has good data center hardware, but it is not the best. AI server builders generally choose the best. They are poorly armed, fighting over scraps.

- MRVL has some giant non-cash charges they would prefer you ignore.

- Spring metrics for generative AIs show that interest may be waning now that the novelty has worn off. There may also be seasonal effects here.

The AI Hype Cycle

AI hype cycles are pretty regular things that date all the way back to the 1950s. In 1967, one of the pioneers of AI, Marvin Minsky , said this :

We are now immersed in a new technological revolution concerned with the mechanization of intellectual processes. Today we have the beginnings: machines that play games, machines that learn to play games; machines that handle abstract-non-numerical-mathematical problems and deal with ordinary-language expressions; and we see many other activities formerly confined within the province of human intelligence. Within a generation, I am convinced, few compartments of intellect will remain outside the machine's realm - the problems of creating "artificial intelligence" will be substantially solved .

- Marvin Minsky, Computation: Finite and Infinite Machines , 1967

In the first place, I don't need to tell you that Minsky was very wrong about that last part, and he lived long enough to realize that. But also, doesn't it read exactly like a lot of what we are reading today?

Each one of these hype cycles fails on one level, but also pushes forward this multi-generational project. For example, the last one began in 2012 and gave us a wealth of hidden consumer-facing AI features, like all the things iPhone and Pixel can do with photos, or the AI behind TikTok that picks the next video for you. We also saw incredible advances in computer vision, and factory automation.

So now we are on to a new cycle, kick-started by generative AIs that create images and text. This has led to an explosion of investment, and orders for NVIDIA ( NVDA ) GPUs, the workhorses of AI math. But ardor for these tools may already be cooling now that the novelty has worn off.

{kind=link}

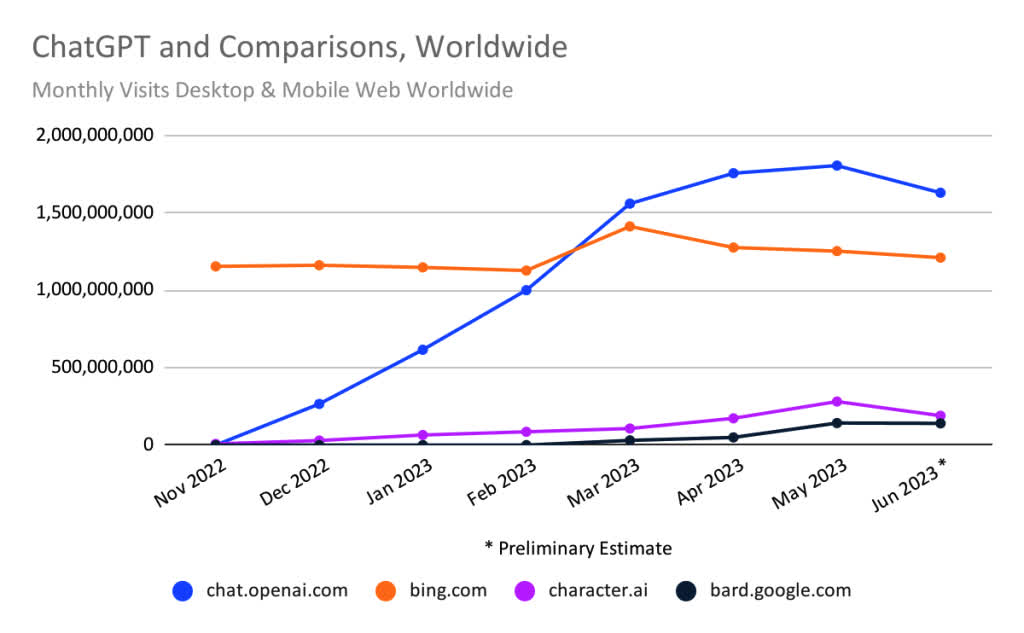

Google ( GOOG ) Bard is the only one that still saw growth in June, according to Similarweb , a web data research firm. There is probably some seasonality in there, with kids out of school, but the rocket growth rate for ChatGPT (blue line) began coming off in April. Worldwide, traffic dropped 9.7% and unique visitors 5.9% in June. Time spent at ChatGPT per visit has been in decline since April. SensorTower, which tracks mobile apps, reports that both Bing and ChatGPT app downloads were down 38% MoM in June. Seasonality can only explain so much of this.

We may already see a bit of the bloom off the rose.

But let's get back to that explosion of investment, orders for Nvidia GPUs, and other data center hardware, because that's why we're here. Investors see this, and want to know who is next:

That meteoric rise, which may not be done, also puts Nvidia at about 50 years of year-forward earnings under very generous assumptions. Who else benefits from this massive wave of hardware and R&D investment?

I am here to tell you two things:

- Nvidia is taking all the money, leaving scraps for the other hardware players.

- There is a narrow list of companies that make hardware up to these tasks that can pick up those scraps. Marvell's ( MRVL ) offerings are good, but not the best.

Yet, this:

Marvell is likely to see a small benefit to their top line and gross margin, but that reaction to their earnings call, where "AI" was mentioned 98 times, is excessive given the reality.

Nvidia Is Taking All The Money

I wrote an entire article on that subject , but briefly:

- Nvidia began preparing for this moment about two decades ago when they began developing software that could allow GPUs perform other very compute-heavy tasks besides graphics. This is their moat.

- Because they come with a complete hardware-software suite, their solution has been the default for AI research since 2012.

- They get something like a 75% gross margin on their data center GPUs, which at the moment face substantially no competition because of that moat.

- Nvidia hardware takes up about 90% or more of the hardware costs of a typical AI server. That leaves scraps for everyone else.

Let's zoom in on that last bullet.

{kind=link}

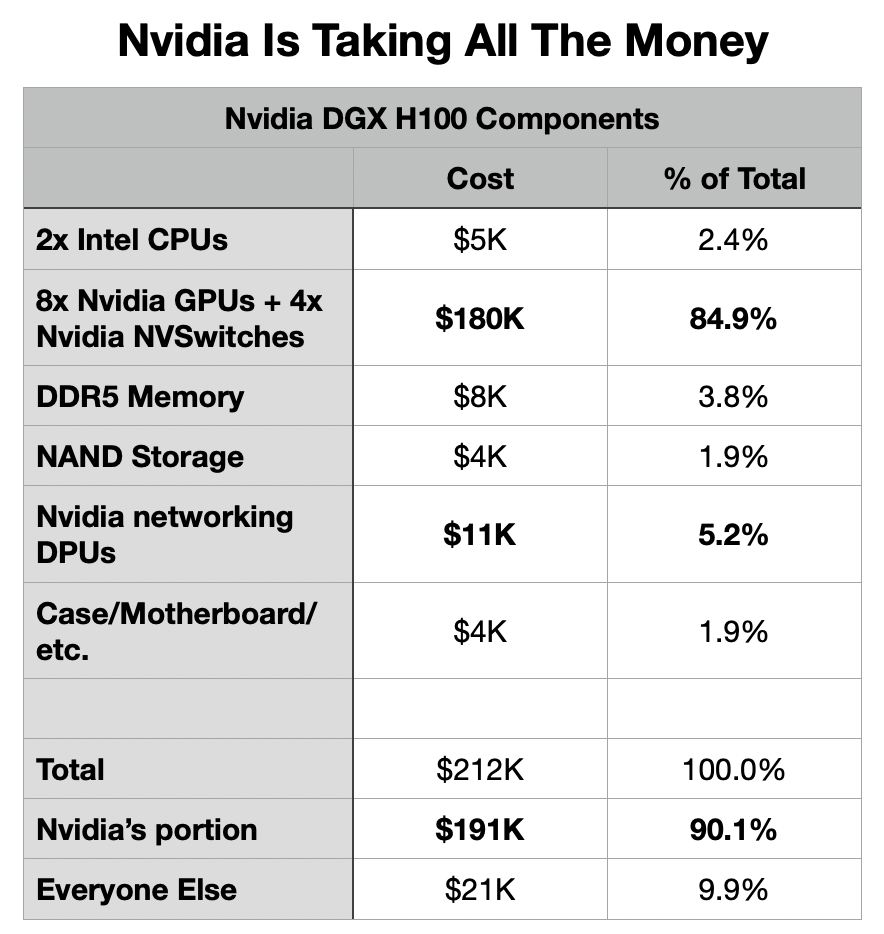

These are some approximate sales costs that go into Nvidia's DGX H100, their AI supercomputer building block. Nvidia sells individual GPUs, that server, or supercomputer "pods" with 16 or more of the servers plus network hardware. The DGX H100 is sort of the gold standard for AI servers now, and about 90% the materials by sales value are Nvidia. And that doesn't even include their markup on the server.

AWS ( AMZN ), for example, is balking at these servers, because they have a lot of experience in building their own servers and data centers. Nvidia is maxing out everything in their configuration, and AWS can save money on CPU, memory, storage and the motherboard. And of course, AWS will skip Nvidia's markup, not included in the table. But they are still stuck with that $180k line item for Nvidia GPUs and the NVSwitches that link them together.

Marvell's portion of this are network controllers, network switches and storage controllers. Even if they are not maxing out everything like Nvidia, AI customers need high speed and low latency. Bottlenecks can emerge anywhere in the pipeline, and you are only as fast as your slowest part. How does Marvell stack up against the competition? They are good, but not the best. What people building AI infrastructure tend to go for is the best.

There is also a scenario, cannibalization , where hardware vendors like Marvell will see decreased sales from the AI investment frenzy.

Hardware

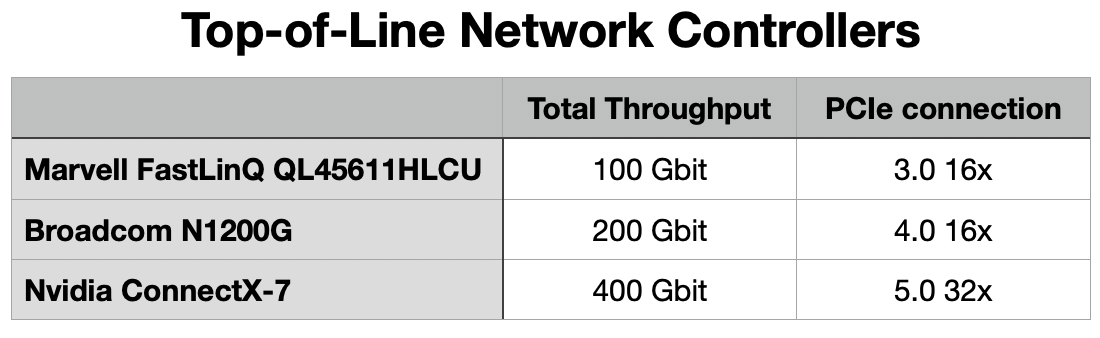

Nvidia uses their own ConnectX-7 as a network controller in their server configuration, 10 of them in all. These came over with Mellanox with the rest of their network hardware, and were the main reason for the acquisition.

AWS and Google Cloud, for example, have their own hardware for networking, but let's look at the third party options, starting with controllers:

{kind=link}

Here, no one is buying Marvell for their AI servers, there are too many possibilities for bottlenecks at the network controller.

Things look better in network switches with Marvell's Teralynx 10 matching Nvidia and Broadcom ( AVGO ) with total throughput of 51.2 terabits. But the math is a little unfriendly to network switches compared to the controllers. I expect Nvidia to sell the GPU-equivalent of about 400k of the DGX H100 servers in the next 4 quarters, whether it's their build or others'. These will come with 2-4 million network controllers, but that only requires about 16k-32k network switches. But still, the Teralynx 10 is their most competitive offering in the data center.

On storage controllers, Marvell has a pretty decent offering here with their Bravera SC5, but it eclipsed by the higher PCIe and NVMe standards and throughput in competing products from Microchip ( MCHP ) and Silicon Motion ( SIMO ). Most AI servers will sport one of these each.

So in the first place, these companies are fighting over the scraps, the 10%-15% of an AI server's cost that doesn't go to Nvidia. In the second place, Marvell's technology is good, but not the best. AI server builders are usually in the market for the best.

The Cannibalization Scenario

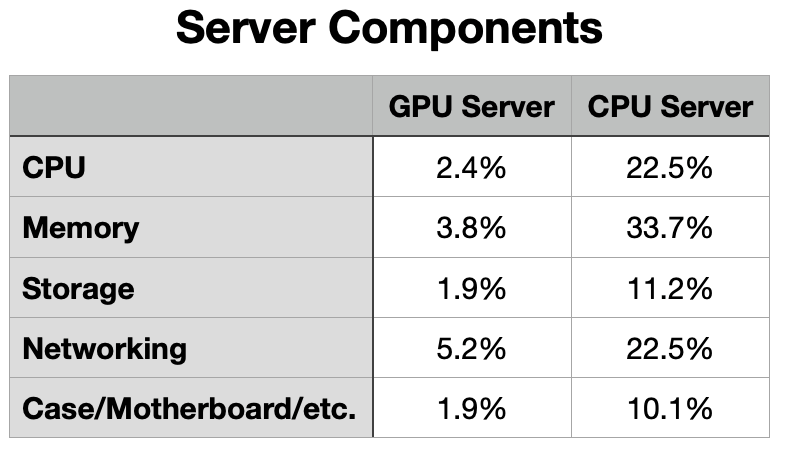

The ugly scenario for all the data center hardware manufacturers besides Nvidia is that GPU compute infrastructure not only grows fast, but comes to displace CPU servers. For the price of one of those GPU servers, you can get 10 or more really good CPU servers. At some point, hyperscalers may have to make choices, and if they stop building CPU servers at a rapid pace, replacing them with one-tenth the number of GPU servers, this is bad news.

Networking is only about 5% of a GPU server's component costs, but about 20% of a CPU server.

{kind=link}

A world without GPU servers is better for non-Nvidia data center hardware manufacturers, not worse. The memory companies have the most to lose here.

Competing Q2 Guidance

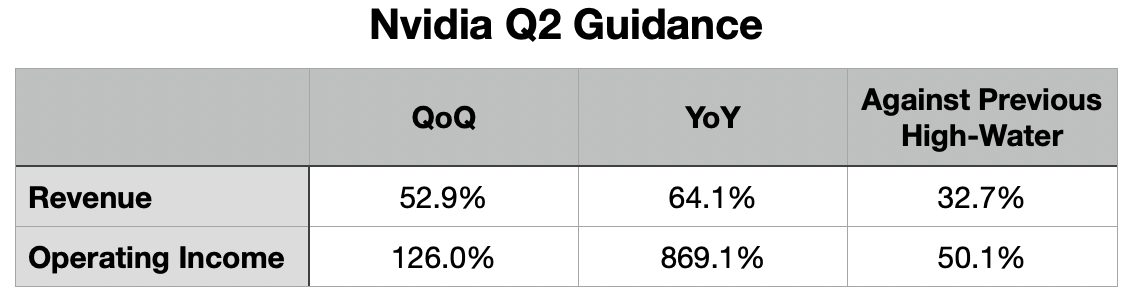

Nvidia's guidance for fiscal Q2 was what kicked the AI hype cycle into full gear:

Keep in mind that QoQ and YoY are against soft comps, especially the year-ago quarter (Nvidia guidance midpoint)

{kind=link}

My estimate is that Nvidia could sell as much as $40 billion in their data center segment in the next year. If they do that, they are trading at about a half century of 1-year forward earnings. But there is a very real story here of AI infrastructure growth. My read is that the guidance tells us that Apple ( AAPL ) has mostly vacated TSM's ( TSM ) 4 nanometer node, opening it up for Nvidia, AMD ( AMD ), Qualcomm ( QCOM ), Mediatek and others. Nvidia appears to be only constrained by TSM 4 nanometer capacity, and whatever their allocation is there.

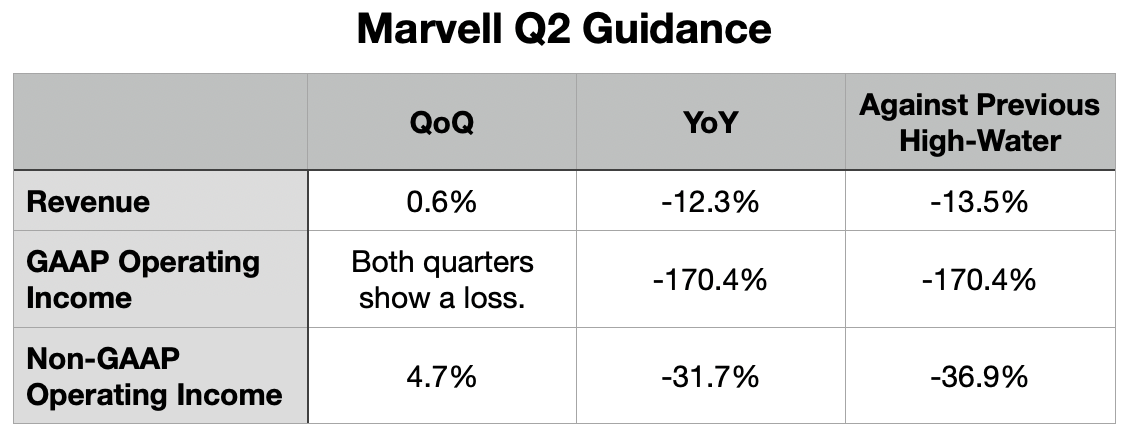

Let's check in on Marvell's guidance:

{kind=link}

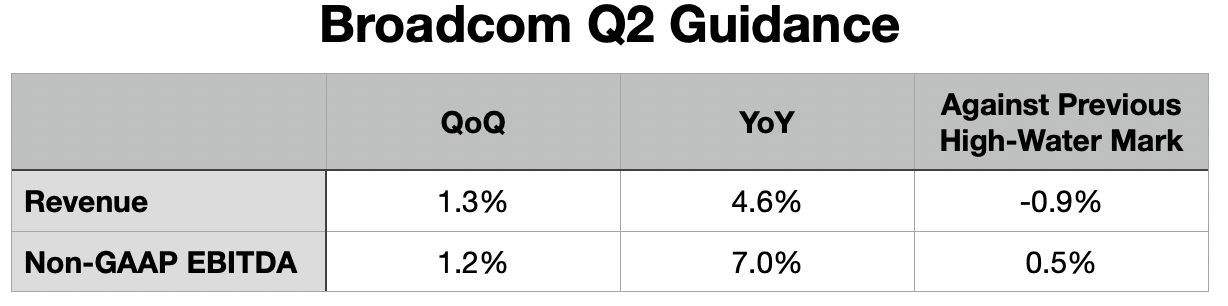

Marvell's C-suite had a difficult task: to convince investors that this guidance portended an AI boom for Marvell like Nvidia's. Amazingly, it worked. Their closest direct competitor is Broadcom. Here's their Q2 guidance:

Broadcom only guides to adjusted EBITDA (Broadcom guidance midpoint)

{kind=link}

Hardly a world-beater, yet:

Their guidance tells you everything you need to know about what Marvell and Broadcom stand to gain here, which is enough to offset some of the weakness in their consumer and enterprise end markets, but not more than that. The wild surge in Marvell and Broadcom stock stems from a misconception out there right now. People don't yet comprehend how much Nvidia is taking all the money.

The Non-Cash Issues

In the Marvell guidance table, you will note the large gulf between Marvell's GAAP and non-GAAP reporting. This is due to the giant non-cash charges they pull out of their non-GAAP reporting.

Like AMD, they are working off a 2021 acquisition for which they paid a lot, Inphi for $10 billion. It added almost $6 billion to goodwill, over doubling that line, which they work off at a rate of ~$150 million a quarter in non-cash charges to the operating statement. Their total amortization of goodwill was $270 million in the reported quarter, 20% of revenue.

With AMD, the giant non-cash charges from the Xilinx acquisition make sense - the Xilinx assets are growing so fast that they will soon compensate for the charges. In the last couple of quarters, the Xilinx assets really overperformed the rest of the company, and made the quarters look much better than they would have otherwise. There is no such indication with Marvell and Inphi.

Marvell would very much like for us to ignore those non-cash charges, as well as $60 million in restructuring charges, and $143 million for stock-based compensation. The latter is employee compensation directly at shareholder expense.

That chart starts after the Inphi deal closed in 2021 (Inphi shareholders got 17% of the combined company, in addition to $3.6 billion in cash), with share-based compensation diluting shareholders by 5% since then.

In total, the adjustments to Marvell's GAAP numbers was 39% of revenue in the reported quarter, $516 million. But let's be generous and give them their non-GAAP adjusted earnings. Let's be even more generous and match the growth rates in Nvidia's new bull case, something I think highly unlikely. In the next year, they would show non-GAAP EPS of $1.67. At Friday's close, they are worth around 35 years of non-GAAP 1-year forward earnings. That seems unreasonably high for a company in very competitive cyclical markets.

The GAAP number I get is -$0.01 EPS for the year forward.

So What's Happening?

Investors look at Nvidia and want to catch that lightning in a bottle with something else. Nvidia looks richly priced, so what else is there? If you are one of those investors, I am only here with bad news for you. Until Nvidia's software moat is drained, AI will not be that sort of tailwind to other hardware companies. In fact, it could wind up being very bad in the cannibalization scenario.

Also, everyone is taking the rise of generative AI as a given. I still think that the probability that we are seeing another investment bubble from which Nvidia benefits like crypto is low. But recent metrics suggest that the novelty of these tools may be wearing off, and growth may not be as astronomical as we thought even a month ago.

I am someone who thinks that AI will eventually change everything. It has already changed many things, like how we watch videos or interact with our photos or how factories are run. It is changing creative fields rapidly right now, a big reason for the Hollywood writers strike. But AI progress comes in waves. Like all the earlier ones, this hype cycle will burn out, but also leave lots of progress in its wake.

For further details see:

Marvell Technology And The AI Hype Cycle