MAS - Masco: Consumer Demand To Return In 2024 And Beyond

2024-01-17 16:51:03 ET

Summary

- Masco Corporation is a well-diversified company in the building products industry that benefits from strong housing demand.

- The company operates in the plumbing and decorative architecture segments, with the plumbing segment being the largest revenue generator.

- Masco has a solid investment thesis with immediate value from dividends and buybacks, and potential long-term growth opportunities through acquisitions and international expansion.

Investment Introduction

An industry hit hard with rising interest rates was surely the construction industry, and more specifically in the case of Masco Corporation ( MAS ) the building products industry. The company manufactures a variety of products for a home, from shower equipment to paints and doors. It's a well-diversified business that benefits from strong housing demand. Some anticipate a further cooling off for the housing market, but I think it will remain robust for both 2024 and 2025. Perhaps not with the same demand and price increases as seen in 2021, but a market with enough demand that a company like MAS is a good opportunity to invest in and benefit from this. We are roughly 3 weeks out until the next earnings report from the company on February 8, and even if the fourth quarter of the year might notoriously be quite slow, I do anticipate a decent YoY sales and EPS growth, which could send the share price up. If it doesn't happen, I still believe in MAS over the long term and think the current price level is a good one to start or add to a position.

Company Introduction

Masco is a company that operates in the building products industry . This is quite a broad market which I think can generally be described as quite seasonal and dependent on strong economic growth in a country to expand. In the US where MAS is operating the last few years have been tough for the industry as rising rates put pressure on margins and earnings, whilst also lowering consumer demand. Over the long-term this is just the seasonality of the industry I think and underlying tailwinds remain very much in place for the industry. Some of these tailwinds are increased spending by both government and business for better infrastructure. With better infrastructure comes more prosperity in areas and housing demand naturally follows, ultimately trickling down to benefit a company like MAS.

{kind=link}

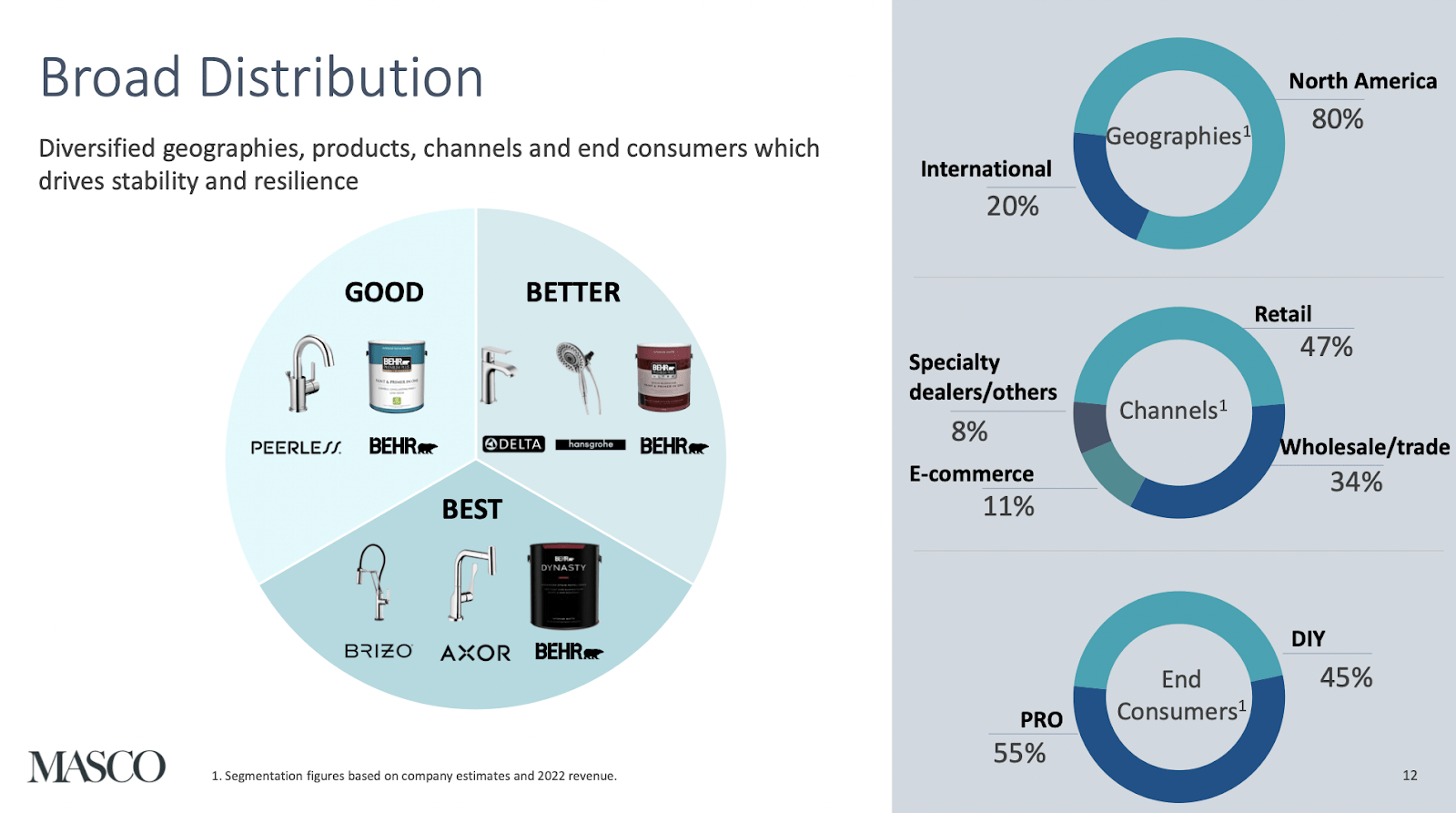

Now that we have covered the recent history of the industry and some of the tailwinds, let's take a closer look at what MAS does. The business is divided into two primary segments, those two being Plumbing and Decorative Architecture. Revenue wise the largest segment is the plumbing one, pulling in around 60% of the total revenues. In terms of sales for the plumbing segment, nearly half is actually coming from wholesale and the remaining 50% or so go by either retailers or e-commerce sites.

The second segment differs here a little as a much larger portion is through retailers instead. I think a cause for this is that the way the plumbing segment is set up, it's more efficient sometimes to go the wholesale route, both for delivering the products and also for consumers. It means they can buy bigger amounts at a time and not be held back by delivering times as much. Market-wise, MAS still very much remains an American company that has 80% of its revenues from North America, with the remaining 20% being international.

Valuation

I don't think it's reasonable right now to assume that MAS will be a 2x stock in the next 12 months, for that you need to look at an entirely different sector or industry in my opinion. What MAS is, however, is a solid bet on continued demand in the US housing market.

{kind=link}

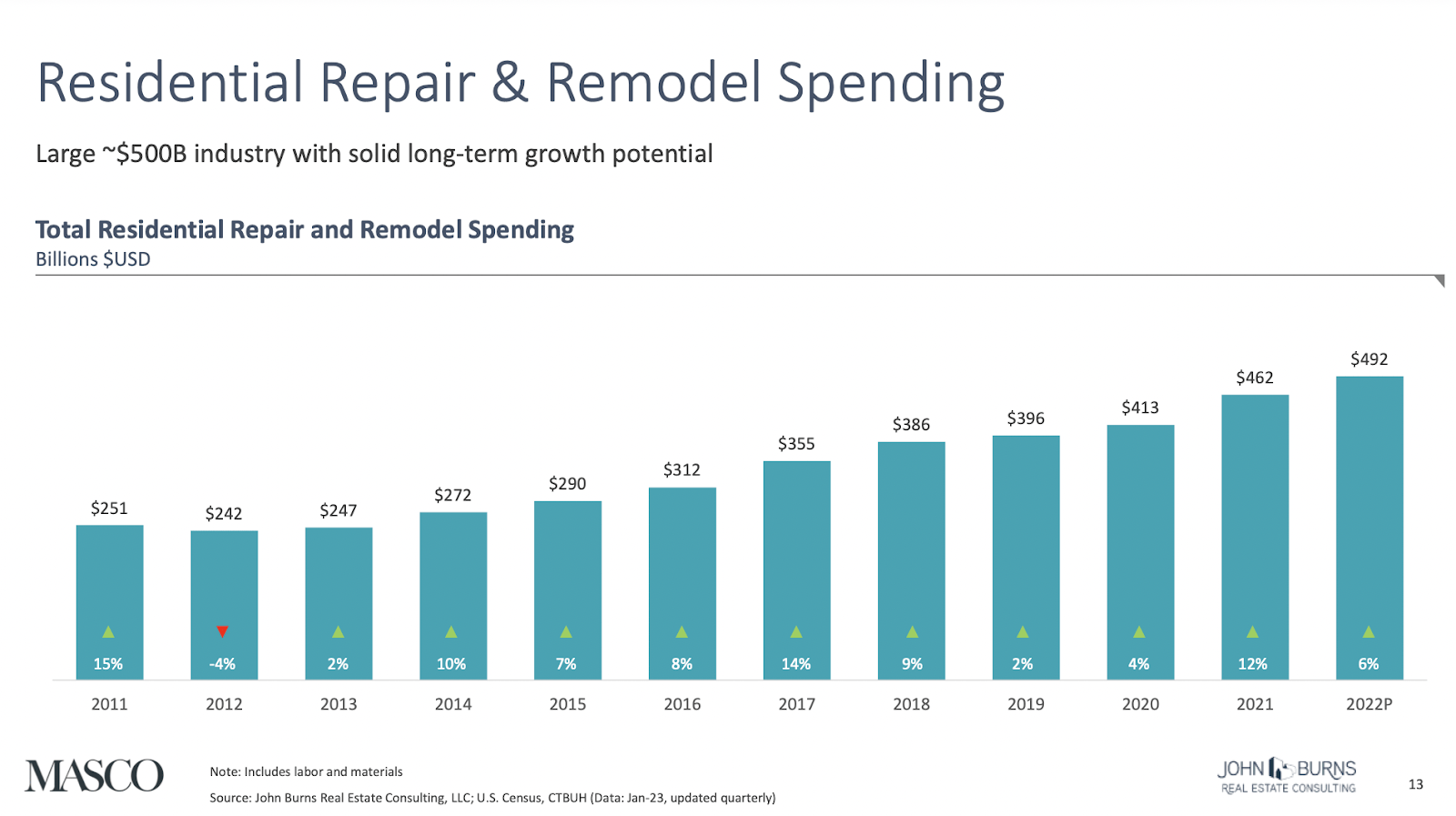

Some of the leading tailwinds are increased spending by consumers for residential repair and remodels in their homes. Seeing as the products that MAS makes aren't solely a one-time purchase, meaning they can be replaced and upgraded, consumers will likely do so during the span of their stay in a home. The chart above here quite conveniently finishes in 2022 before rising inflation and high-interest rates were a factor. But despite that, I think the trend will continue and 2023 will just be a slight pause for growth. I think MAS is in a good position in 2025 to perhaps beat out its previous record sales and get close to $9 billion in annual revenues.

{kind=link}

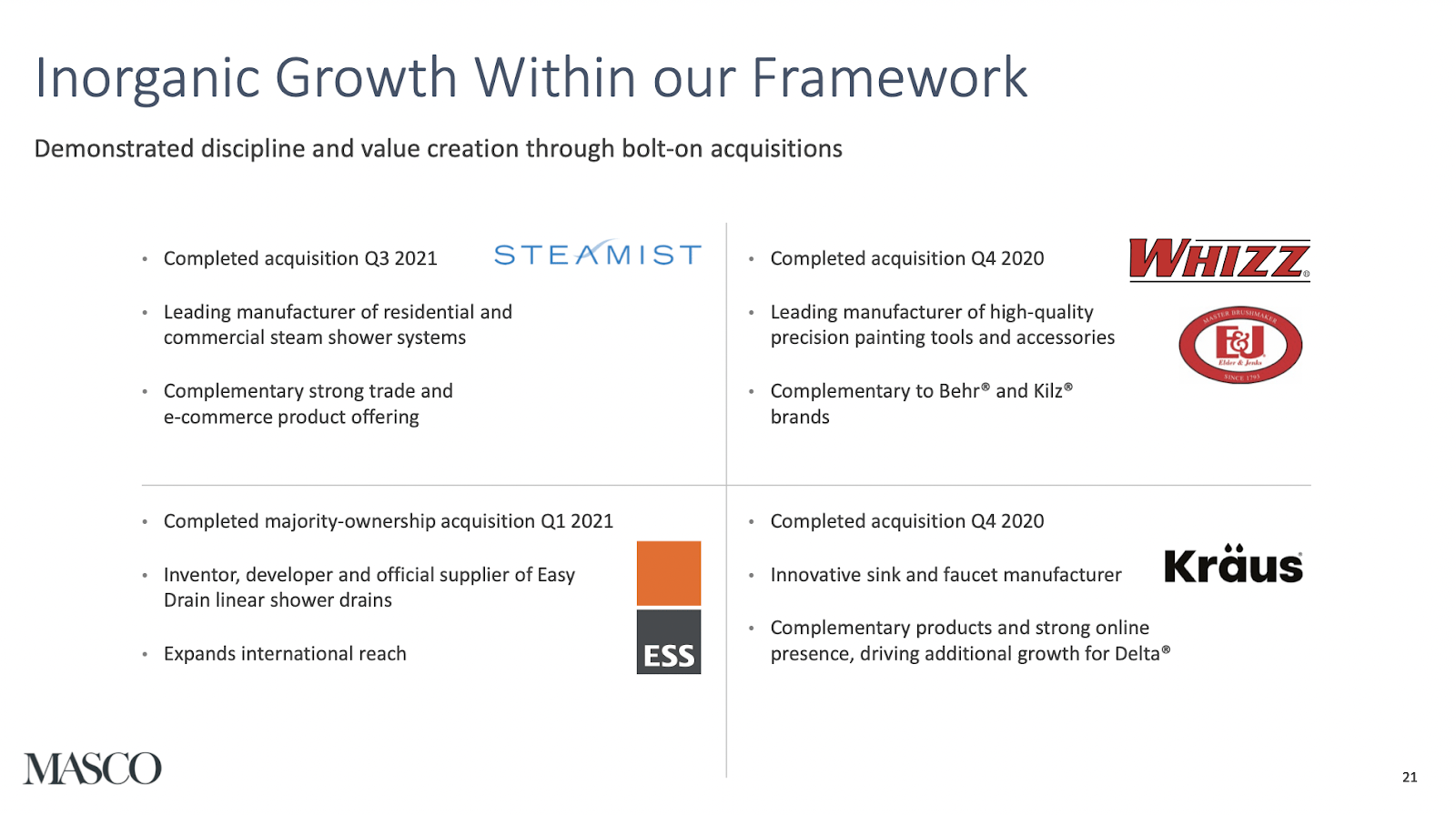

I have talked a little bit about the growth of the company and how that often is derived from the housing market, but MAS does present a level of appealing inorganic growth if I can put it that way. MAS has since its start been quite active in acquiring business, most notably since 2020. 5 of the main acquisitions in recent times are Steamist, Whizz, Elder & Johns, Kräus, and ESS . Most of these acquisitions have been complementary to already exciting brands or segments in the company but one that stands out is the ESS acquisitions which brings more international exposure to MAS. I think that is an exciting route for them to go down the next decade as even though the US housing market is one of the largest in the world, being operational and active in other markets will lead to more long-term growth opportunities in my opinion.

The Value You Get

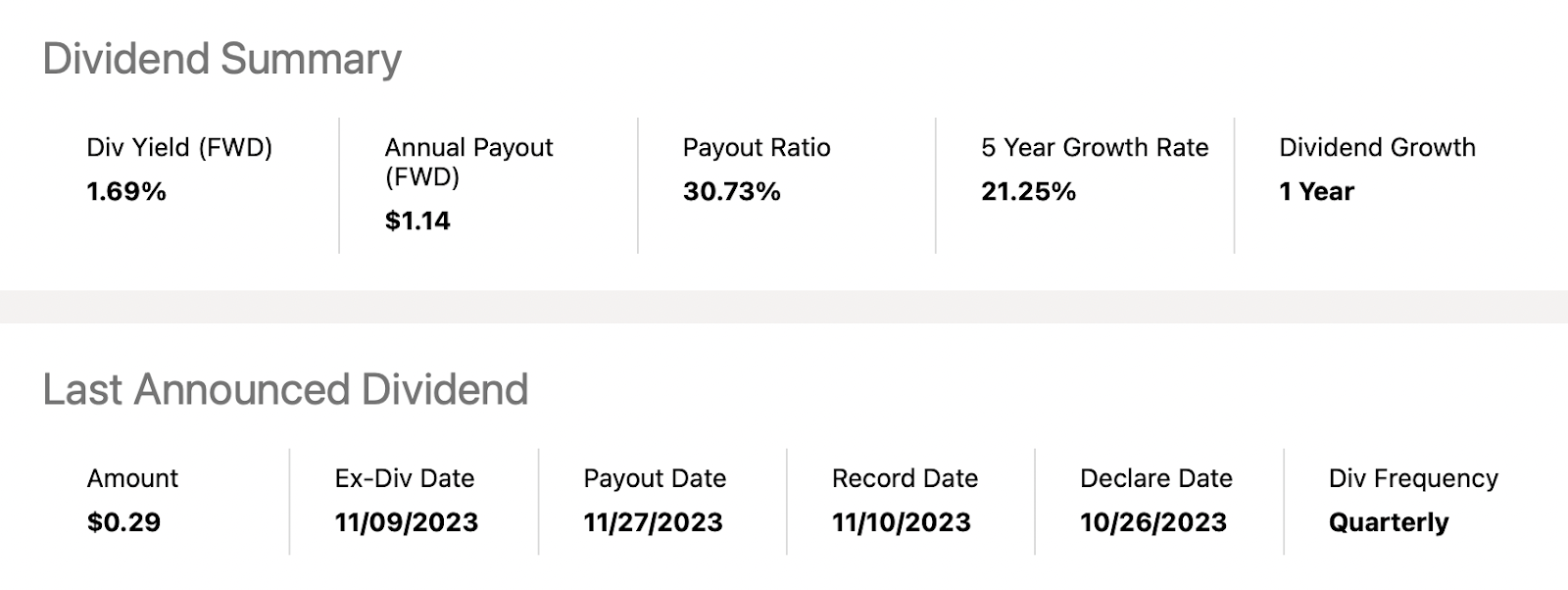

There is quite a lot of immediate value you get with MAS right now. With immediate value I mean both dividends and buybacks. The dividend yield is 1.69% right now and YoY the shares have declined by 2.6%. Combined that is 4.29%. Over time I do think MAS can manage to generate a CAGR of EPS by 5 - 6% the next decade. That together with the immediate value you get is a 9.29% - 10.29% annual return on your investment. I tend to look for anything above 8% and since we have that here the buy thesis holds.

{kind=link}

A dividend is something I value quite a lot in investing. It's often something I value more than extreme growth opportunities. It brings a lot of stability to a portfolio but a combination of both growth and dividend is the best possible scenario, and with MAS you get that. The dividend has not been in place for a very long time, but I am convinced it's both here to stay and to be increased as well. The last dividend was declared on October 26 which means MAS will have an annual payout in 2023 of $1.14 per share. I do think a 7% is reasonable to assume as a CAGR for the dividend, meaning that in 2024 it will be $1.21 per share. This is something I will be looking for in the next earnings report and if the increase is higher than 7% I would expect the share price to jump a fair bit as well.

Price Target

{kind=link}

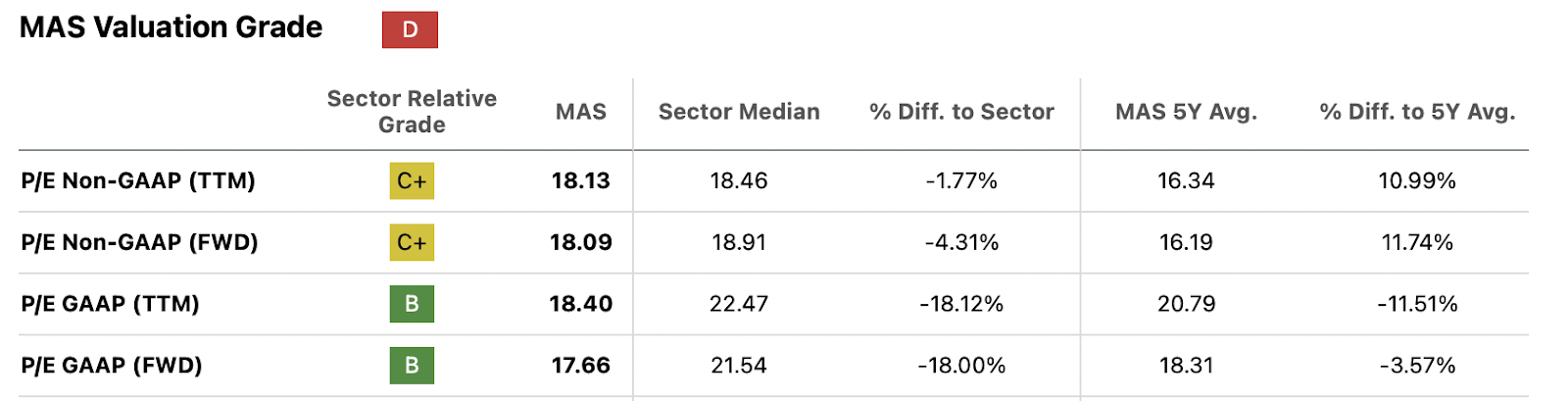

MAS is a company that I think is best viewed in terms of a p/e metric. A p/b metric for example doesn't make too much sense here as MAS produces a product that they sell, rather than operate assets they derive value from. On a p/b metric MAS is 11.7% above its historical average. With a premium like that, you might wonder where I see the value. Well, for me the growth story revolves a lot around the return of consumer demand and for material expense to stabilize. This would help MAS in growing the bottom line faster.

My Estimates (Author)

My estimate for the coming is an EPS CAGR of 7%. This is far lower than what MAS has produced in the last decade, but I think a substantial discount is often warranted to both realize a better return for myself and my investments, but also to limit my own downside risk. I would argue that the aggressive M&A of MAS means higher earnings multiple like 19x is authorized here. It makes sense since the company makes acquisitions in the range of $100 - $300 million it seems and with annual net incomes of over $860 million then they have a big war chest to use for this.

In my upside I also include the dividend since that is a big part of my investment approach, and with the 2024 price target landing at $75 that leaves us a 13.4% upside right now. I mentioned earlier that the immediate value for MAS is 9.29% - 10.29% which means there isn't a large discrepancy between my predicted upside and the actual upside. This is a positive as it gives me a more accurate estimate of ROI. I substantiate my EPS estimates further by the strong beat the company had last quarter and how that might very well be the case in the next quarter too. The 2023 EPS estimate increased to $3.65 - $3.75 per share and about my FY2024 estimate it's just a 5.3% YoY growth rate, a very realistic number in my opinion as interest rates begin to decline later this year.

The Bear Thesis

{kind=link}

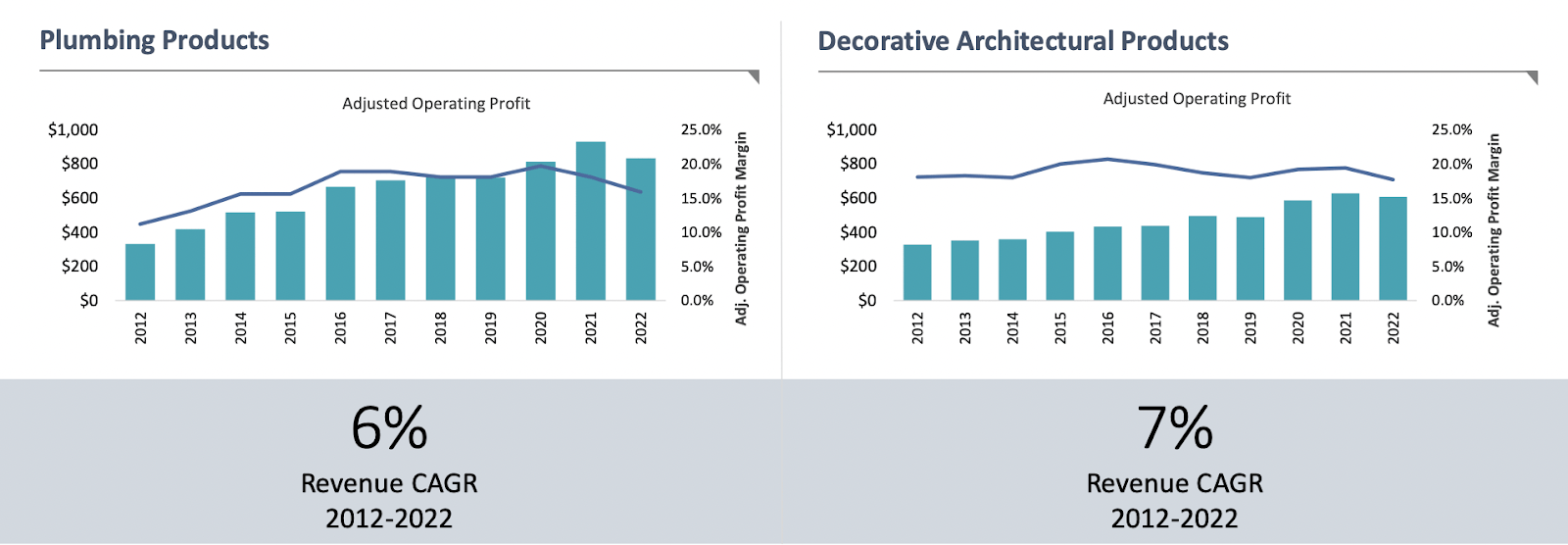

One of my concerns with MAS is the higher material costs. The average jump for material costs has been roughly 19%, digging into margins for companies like MAS. I don't see any short-term catalyst that would justify a drop in these prices, demand for housing seems too high to let that happen. The charts above here may indicate a strong track record of revenue growth, but margins haven't had quite the same growth, unfortunately. MAS seems like it needs to push hard with M&A strategies to expand both its product line and revenue opportunities to continue to post EPS YoY growth. That is a risky position to be in as organic margin growth is something I look very often for in businesses. But I think MAS makes up for it thanks to their quite aggressive growth strategy over the last few years, which has ultimately led to a NI CAGR of 18.4% the past decade, something a lot of companies would just dream of achieving.

State Of The Company

{kind=link}

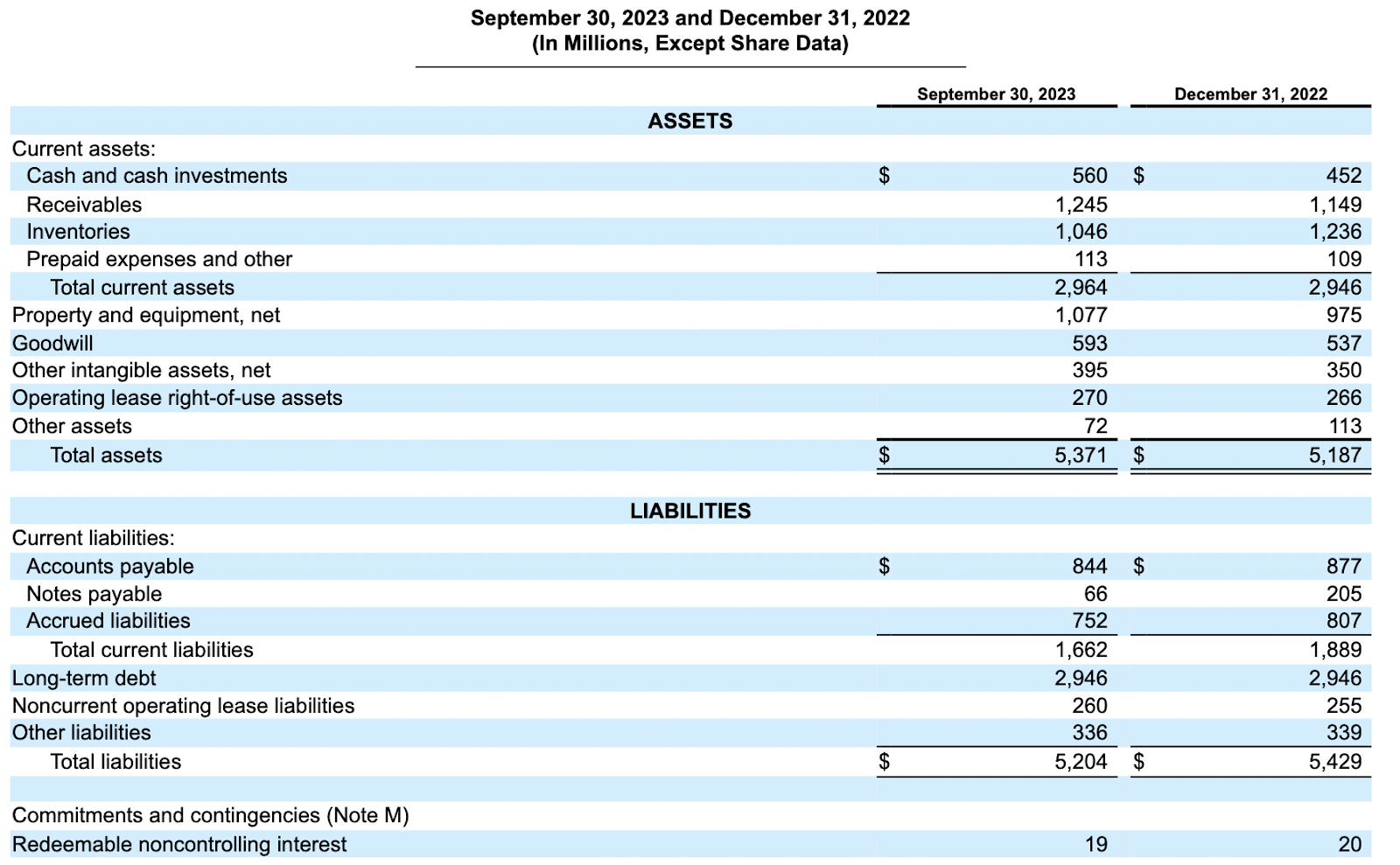

Right now the company is in a strong position to continue its M&A activity as I have reiterated in the article somewhat already. I think my claim for this is supported by the fact MAS holds $560 million in cash. The 10Q from Q3 FY2023 further reveals that MAS doesn't have a significant amount of debt due in the short-term which puts them in a less pressured spot. The largest amount of debt is due in 2027 and sits at $1 billion. I think that with the way MAS has been conserving cash and building it up as well, they won't face any issues paying this debt down when it's due.

{kind=link}

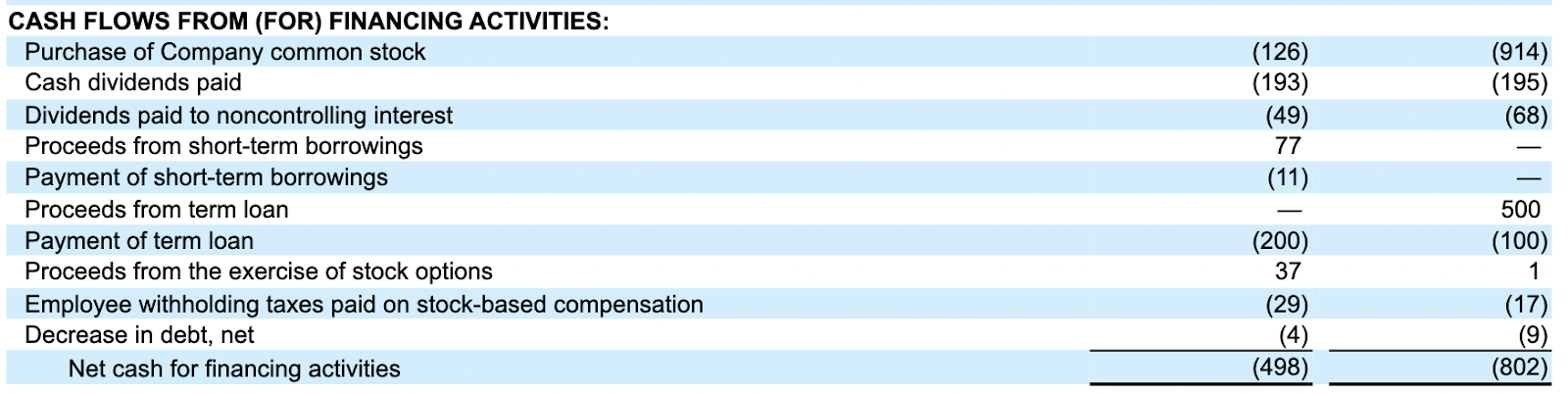

The cash flows from MAS have been largely devoted to buying back a lot of shares and delivering a strong dividend. Cash from operations where $954 million in the last 9 months and nearly $200 million was used for the dividend alone. Something that caught my attention though was the decrease in capital spent on share buybacks. In 2022 MAS spent nearly $1 billion for buybacks, but now it's not even $126 million. A cause for this might be the payable notes that MAS had earlier in April of 2023, which required a significant amount of capital. But since that is paid off I would expect the buybacks to pick up in 2024 again, and depending on the amount, I might have to increase my price target as well. In conclusion, I find the state of MAS as a company to be solid right now. MAS hasn't put itself in an overleveraged position and will in 2024 and beyond see a rise in demand as consumers are left with more capital when rates go down. MAS can afford to continue distributing the dividend and buy back more shares, which are factors I think should be rewarded with a higher valuation as well.

Investment Conclusion

The construction and building sector can be quite volatile at some times, but right now I think it's ripe for a comeback. MAS had a pretty good 2023 with all things considered, like higher rates and higher material costs. The current price does leave a solid upside for the stock in the next 12 months. Guidance was raised last quarter and margins seem to be on the rise too, which ultimately led to the run-up in price MAS saw following the release. We are now around 3 weeks off until the Q4 FY2023 report and I am rating the business a buy ahead. 2024 is a comeback year for a lot of companies, and MAS is one that I think can outperform the markets this year as consumer demand resumes.

For further details see:

Masco: Consumer Demand To Return In 2024 And Beyond