MAS - Masco: Expectations May Be Getting Too High (Ratings Downgrade)

2024-01-20 00:33:15 ET

Summary

- Masco's shares have performed well due to solid operating results and resilience in the US housing sector.

- The company is primarily focused on home remodeling rather than new construction, making it less sensitive to interest rates.

- While Masco's earnings have been strong, its valuation is now full, and a meaningful beat in earnings is needed to maintain momentum.

Shares of Masco ( MAS ) have been a solid performer over the past year, thanks to solid operating results and resilience in the US housing sector. Since I rated shares a buy in October they have returned 30%, exceeding even my bullish expectations . While hopes of more dovish Federal Reserve policy have lifted construction stocks, I do not expect Masco to be as much of a beneficiary, and shares now look fully valued.

{kind=link}

While lower interest rates have buoyed construction-related stocks, it is critical to remember that Masco is primarily a play on home remodeling and not on new construction. Plumbing is about 60% of Masco’s business, and 83% of that unit’s revenue comes from repair/remodeling. Decorative architecture accounts for the remaining 40% of revenue; nearly all of that unit’s revenue (97%) is repair/remodel. Overall, only about 11% of Masco’s business is tied to new construction.

While homeowners may in part finance major remodeling activities, it is not nearly as rate-sensitive as purchasing a house where consumers will typically borrow 80%. Perhaps counterintuitively, I have argued Masco is a defensive stock within the sector from higher rates. Higher rates can “trap” consumers with low mortgages into their existing home given how prohibitively expensive a new mortgage could be, meaning they are more likely to remodel their home than move when they seek change. If we see increased housing turnover this year, that source of demand could be lower.

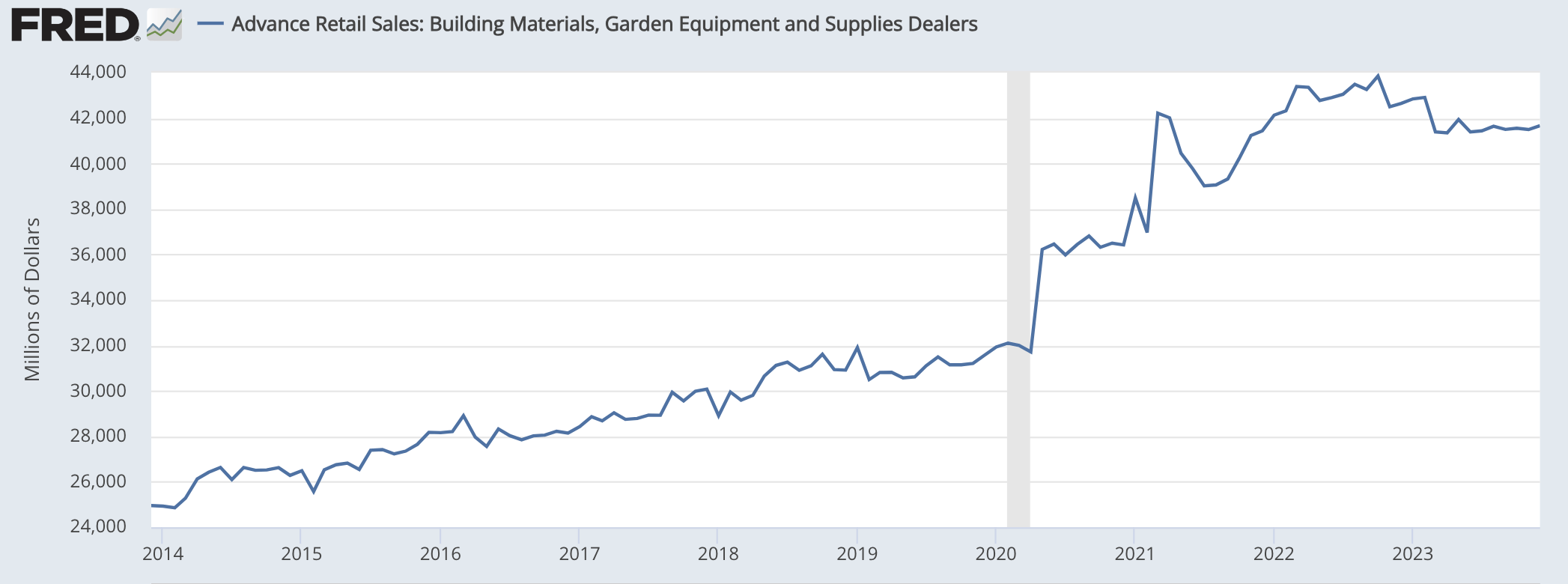

This week, the government released its monthly retail sales report, and I closely watch performance among building materials retailers—companies like Home Depot (HD). The level of building materials spending is quite elevated relative to history; that post-COVID spike has proven durable. However, we are not seeing any evidence of growth in spending recently. Spending has essentially stayed in within 1% of its March 2023 levels for the past nine months.

{kind=link}

I think this spending pattern speaks to do things. First, this speaks to how consumer spending on remodeling work is much less rate-sensitive and cyclical. While existing home sales are down by over 35%, building material sales are down just about 5%, validating why I have seen Masco more defensively. By the same token though, we are not yet seeing any meaningful improvement. Sales are elevated, which is why Masco has performed well. That said, there is not clearly an impetus for material sales growth.

Indeed, while I think Masco has managed through the past three years quite well, which is why I rated the stock a buy, this has me more cautious. When the company reports earnings on February 8 th , I am concerned that it may not live up to its increasingly lofty valuation.

Now, that was not the case last quarter. In the company’s third quarter , it blew past estimates, earning $1.00 vs the $0.92 consensus. This was up 1% from last year, even as revenue fell by 10% to $$1.98 billion. As such, it raised its full year guidance to $3.65-3.75 from $3.50-$3.65 previously.

Results were stronger despite the sagging top-line because of much better margins. Gross margins jumped by 430bps to 35.8%. Prices were up modestly, but input cost inflation has come down considerably, which has helped the company recapture margin. On the other hand, SG&A spending rose by 260bp of revenue to 18.2%, partially offsetting this gross margin gains, as it continues to invest in its brands and lost some operating leverage from lower revenue.

Overall, volume was down by 12% with a 1% benefit from currency and from pricing. Plumbing volumes were down 14% with 4% of positive pricing. Masco is seeing softness in Europe and China (about 20% of company revenue comes from oversees), and management expects ongoing pressure from low volumes

In its decorative architecture/paint segment, it has seen a divergence by customer type with do-it-yourself (DIY) paint volumes below 2019 levels. Pro paint sales were down low-single digits whereas DIY was down low double-digits. With the COVID boom fully normalized, I do not expect to see further material revenue declines, though I also do not foresee a surge in spending either, and management sees “uncertain” demand.

Indeed, while a guidance increase is always welcome, Masco’s adjusted EPS has been $3.07 YTD, implying Q4 EPS of about $0.63 at the midpoint. For perspective, it earned $0.65 last year. Now, I suspect it may beat the midpoint slightly, but earnings will essentially be flat year over year. That is a strong performance with revenue running down 10%, and it speaks to the margin recapture we have seen as input prices have fallen. Management targets 18+% segment margins whereas they will be ~17.5% this year. We have seen Masco nearly fully return margins to normal levels, with just a little bit of further progress.

Getting back above 18% could be about a 3-4% tailwind to earnings, but analysts are currently forecasting about $3.97 in earnings in 2024, up nearly 7% from 2023, which also implies a solid recovery in sales in 2024, which we have yet to see. With new construction only about 11% of its business, even a surge in activity from lower rates is not going to materially move its earnings.

Even at $4 in EPS, shares are now trading 17x forward earnings, a fulsome multiple for a mid-single digit revenue growth company. It does have a strong balance sheet with $560 million in cash and less than 2x leverage. I also remain positive on the long-term outlook because the US housing stock is aging, which should support ongoing repair and remodeling work.

Census Bureau

Three months ago, I felt Masco was a good business at a good price. I continue to believe it is a good business. Its margin performance has been strong. It is defensive, and it has a favorable long-term trend. However, it has rallied like an aggressive, interest-rate sensitive stock, which its business really isn’t. That has made it a good business at a not-so-good price. Given its rally, I think it will need to deliver a meaningful beat and optimistic guidance in two weeks to keep its momentum, and I am not seeing evidence that is likely to occur.

I view earnings more likely to be the $3.80-$3.95 zone, and I would struggle to pay more than 16x or $62, leaving shares about 10% above fair value. Given the quality of the business and secure dividend, Masco is not a short—it is not that over-priced. However, for investors who have enjoyed such a large gain, it now is prudent to take some profits, and when there is a pullback, Masco could once again be an attractive buy.

For further details see:

Masco: Expectations May Be Getting Too High (Ratings Downgrade)