IAU - Mass Debt Maturity Wall Will Likely Pressure The FED To Capitulate

2023-11-20 12:58:29 ET

Summary

- The majority of debt was refinanced and fixed at low rates during 2020-2021.

- FED rate hikes haven't affected the interest paid on much of the debt yet.

- The mass debt maturity wall starting in 2024 has significant implications.

- Debt refinancing has major liquidity and income aspects.

Introduction

Global debt has grown to 350% of world GDP in 2023, and it is probably one of the matters of urgency for the U.S. and for the world as well after inflation is beaten. As we know how fast interest rates have risen since the beginning of 2022, one should investigate the changed interest rate environment in relation to the large debt levels.

On face value, in the post-GFC period, leverage was transferred to the U.S. government from the private sector. Financial sector liabilities to GDP collapsed; however, what has really happened is that the financial sector, instead of a major deleveraging, transferred the majority of its cross-border dollar liabilities off the balance sheet, in the form of FX Swaps, accounting for $80 trillion in 2023. Total dollar liabilities (on and off balance sheet) to GDP grew from GFC levels of 677% to 705% of U.S. GDP in 2023. Therefore, the dollar system is more leveraged today than it was during GFC.

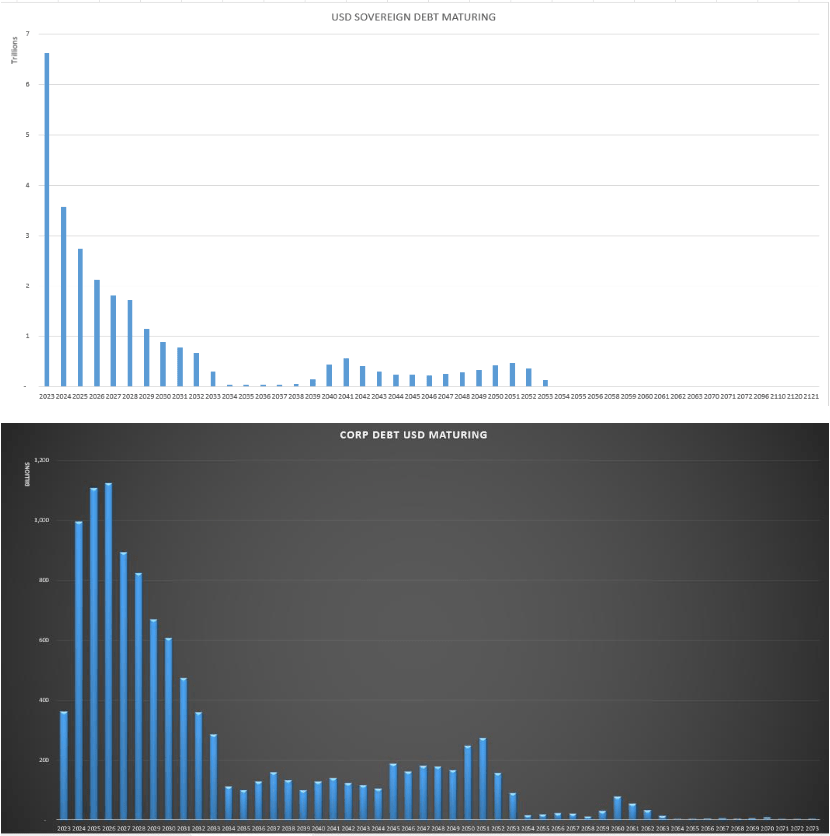

Debt Maturity Wall

Due to the pandemic response of zero fed fund rates and government stimulus, a significant part of global and U.S. debt was refinanced and fixed at low rates. Also, a lot of new debt was issued during the 2020-2021 period. This is the reason why the hyper-aggressive rate hiking cycle of the FED didn't cause a similar magnitude increase in interest due on the global dollar debt load. The number of new issuances in 2022 generally went down, floating rate debt is less significant in volume than fixed rate and only a low percentage of debt expired during that year. Currently, on average, corporations and companies are paying 4.5% interest on their debt, households are paying 3.5% on their residential mortgages, and the government is paying 2.2%. Meanwhile, from 2021 to 2023, the FED raised the rate from 0% to 5.5%. Floating rate debt is only including credit cards, C&I loans, leverage loans, structured products (ABS, CMBS, CLO) and margin loans.

Near 35% of the total corporate dollar debt and 63% of total government dollar debt matures from 2023 to 2027. Residential mortgages are typically 30-year fixed term in the U.S., and 40% of them were refinanced through 2020-2021. Residential mortgages have an average of 5.5 years of life cycle since GFC; however; it is highly uncertain how the lifecycle will change. If households will not refinance and keep their low-rate debt, that means the lenders' assets are low-yielding while funding costs can be reasonably expected to rise. U.S. Treasury-backed money market fund accounts are yielding nearly 5% in 2023, therefore bank deposit rates can be reasonably expected to rise to some degree in order to maintain sufficient funding for the banking sector. Furthermore, if the lender is experiencing funding pressures, it may be forced to sell it at market price or pledge as collateral at face value with the FED rather than pay fed funds rate which is almost certainly more than what the original mortgage asset is yielding, as 30-year mortgage rates were ranging between 2.5% and 4.5% during 2019-2021. There is an argument that a risk transferred is not a risk eliminated, which might be very well in the case of U.S. residential mortgages. The household sector interest rate risk was transferred to the financial sector since GFC, as the 30-year fixed rate term became the largest share. Auto loan debt is typically a 5-year fixed term; however, they have an average lifecycle of 2 years due to customer habit.

{kind=link}

According to the current communication from the Federal Reserve, they will hold their benchmark rate higher for a longer period, not fall into the mistake of prematurely loosening as Volcker did in the 1970s. Therefore it is critical to assess the maturity distribution of the global dollar debt load, to project how the interest rate environment would affect the interest due on the debt load. As a high-level overview, a mass maturity wall has two implications: the liquidity aspect and the interest rate aspect.

L iquidity Impact

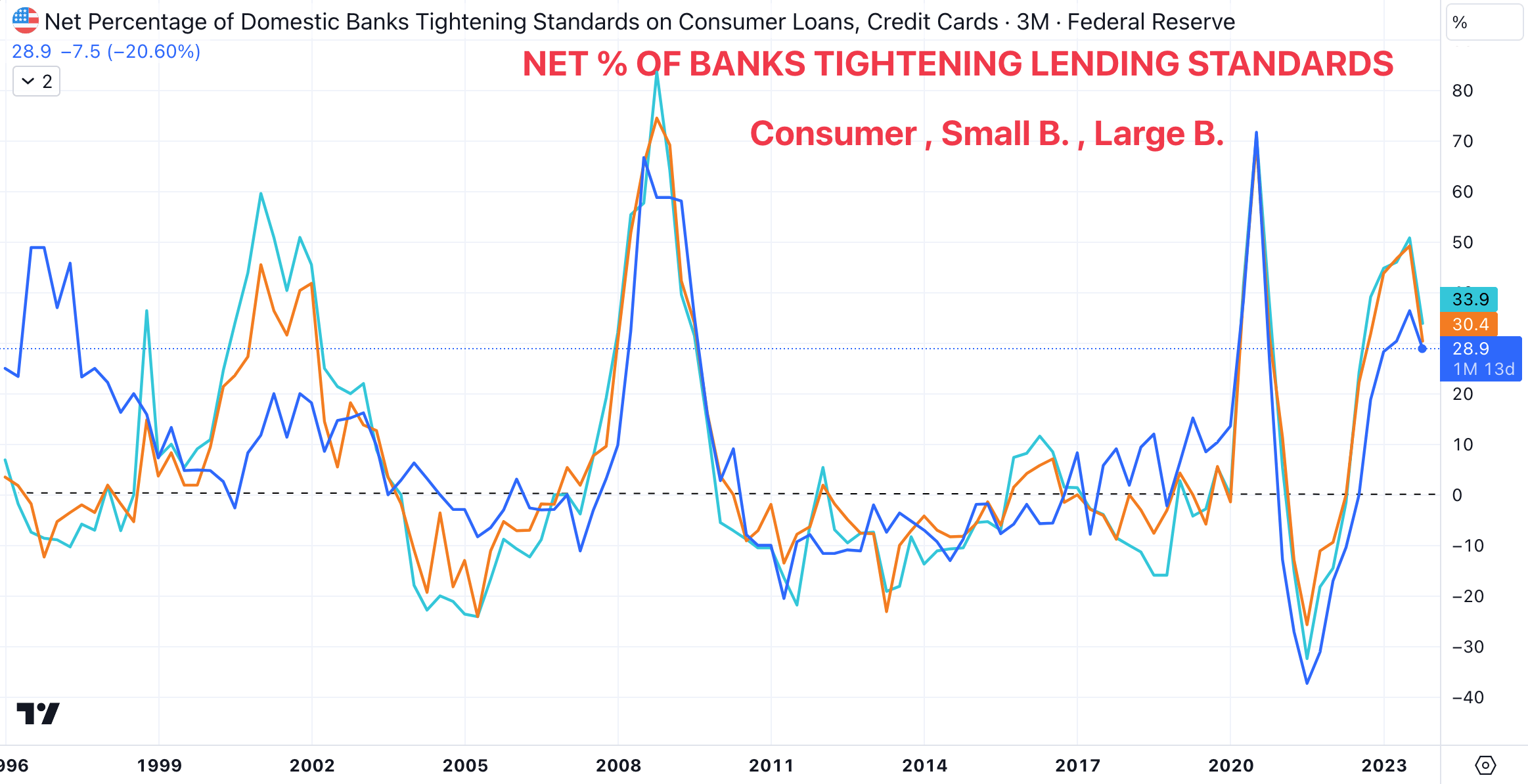

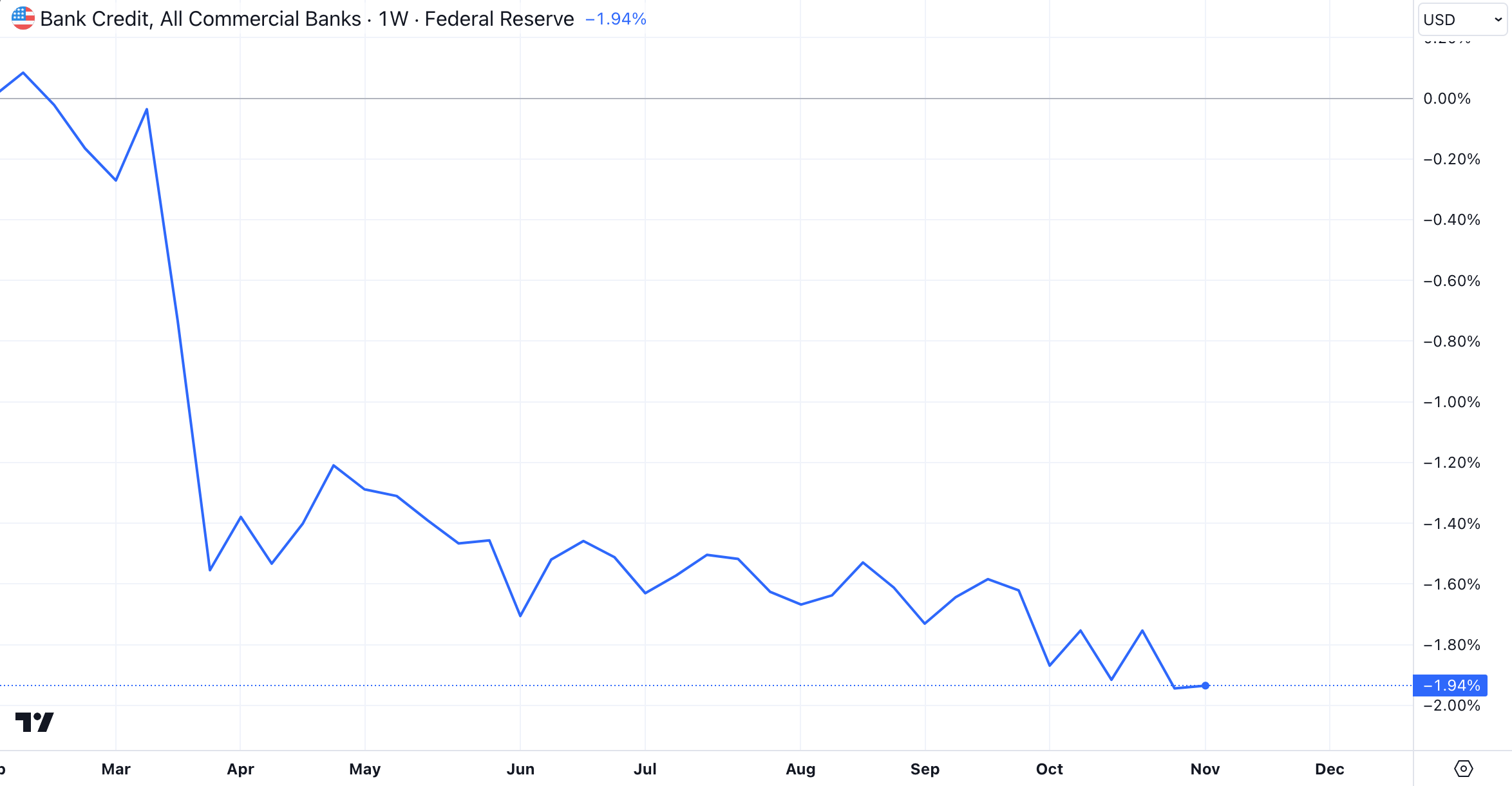

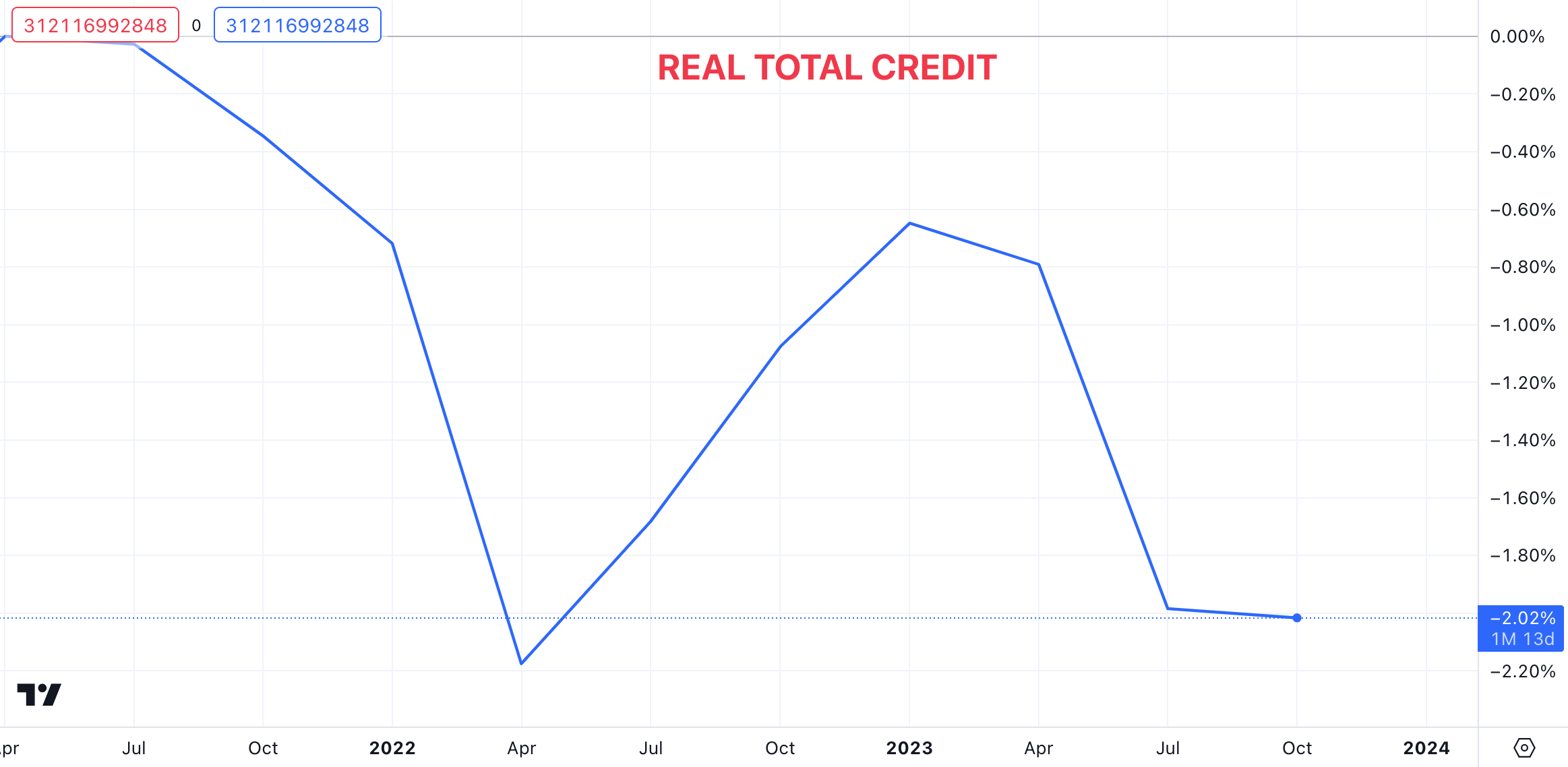

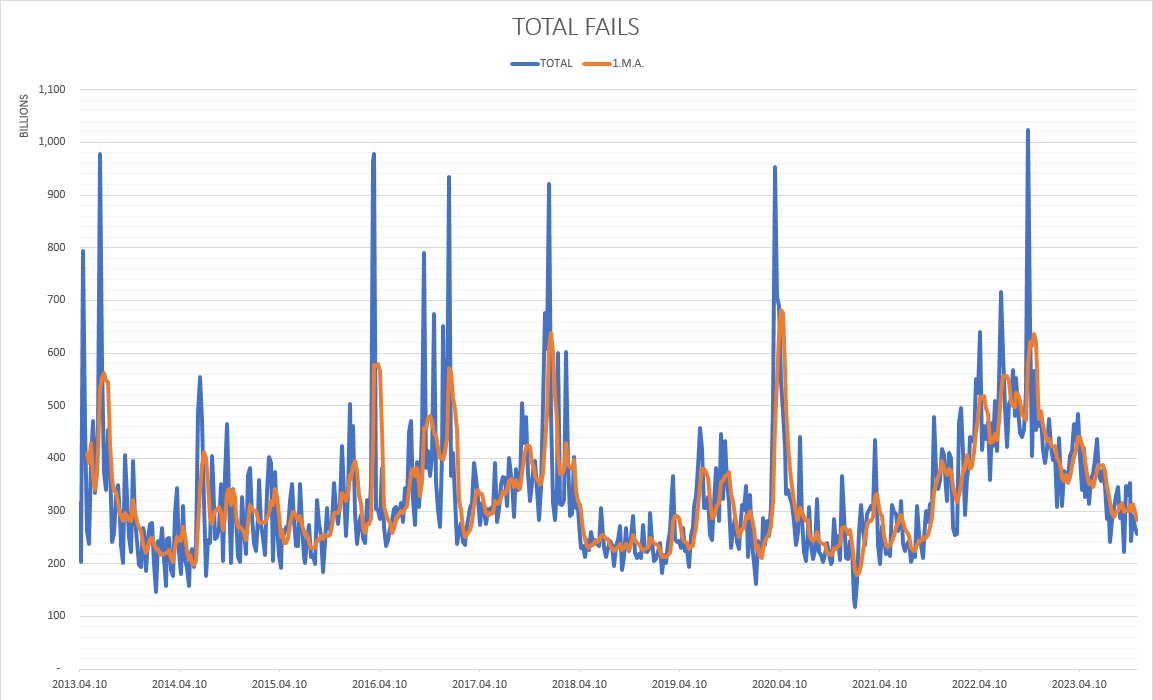

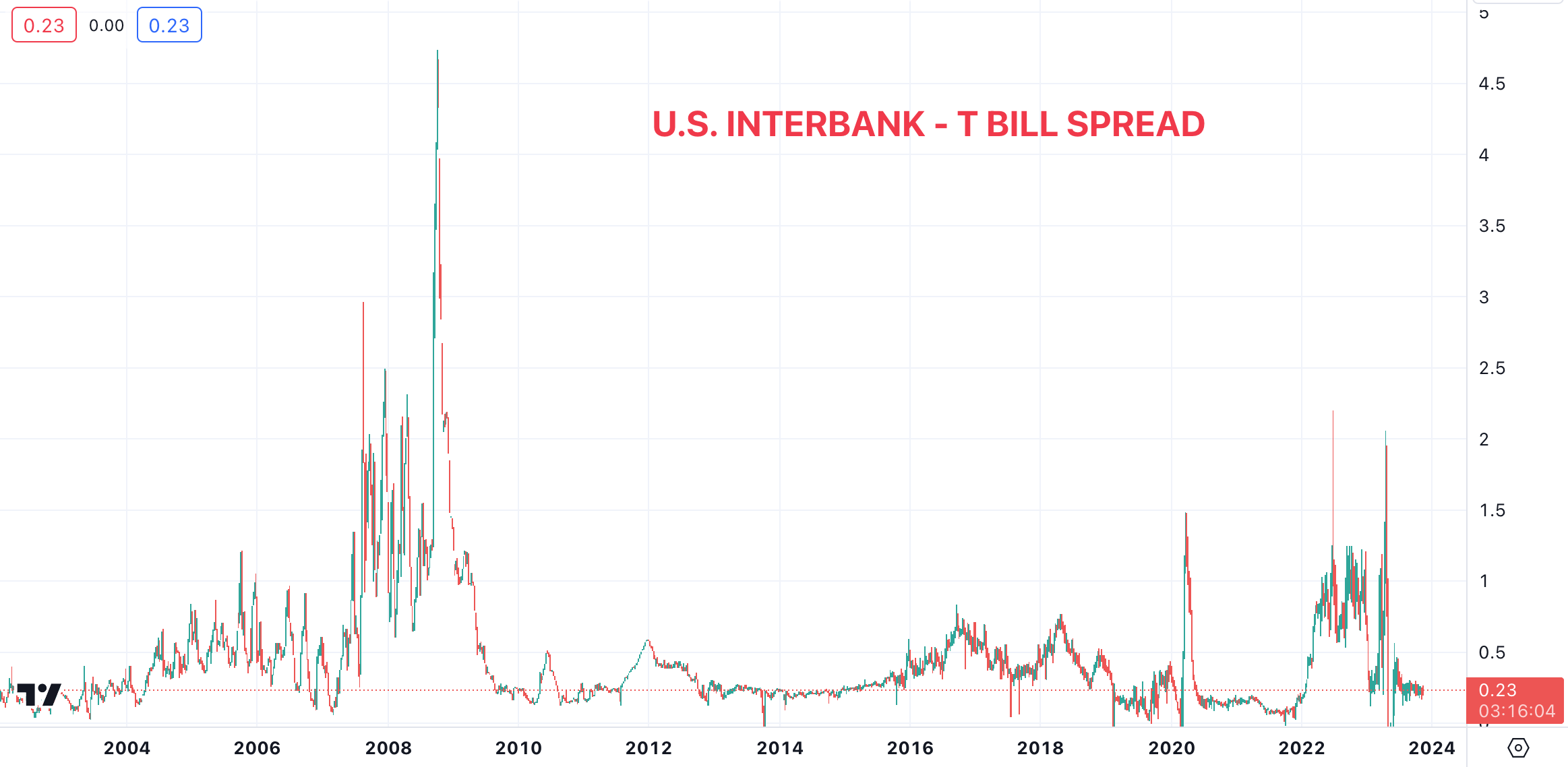

It is hard to capture the exact liquidity impact of the debt maturity wall. However, as global debt constantly grows, our system is always refinancing the maturing debt. Refinancing depends on both the lender's and the borrower's abilities. Lending standards are tightening at a scale of recession levels while nominal bank credit is contracting in the U.S., and total global dollar credit is contracting in real terms since 2022. Triparty repo fails, bond market volatility, bid-ask spreads of high-yield bonds, and money market rate spreads have been signaling elevated stress and probably liquidity problems since 2022. In September 2022, UK pension funds got margin calls on their receiver swaps, and in March 2023, there were several bank closures including Credit Suisse.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

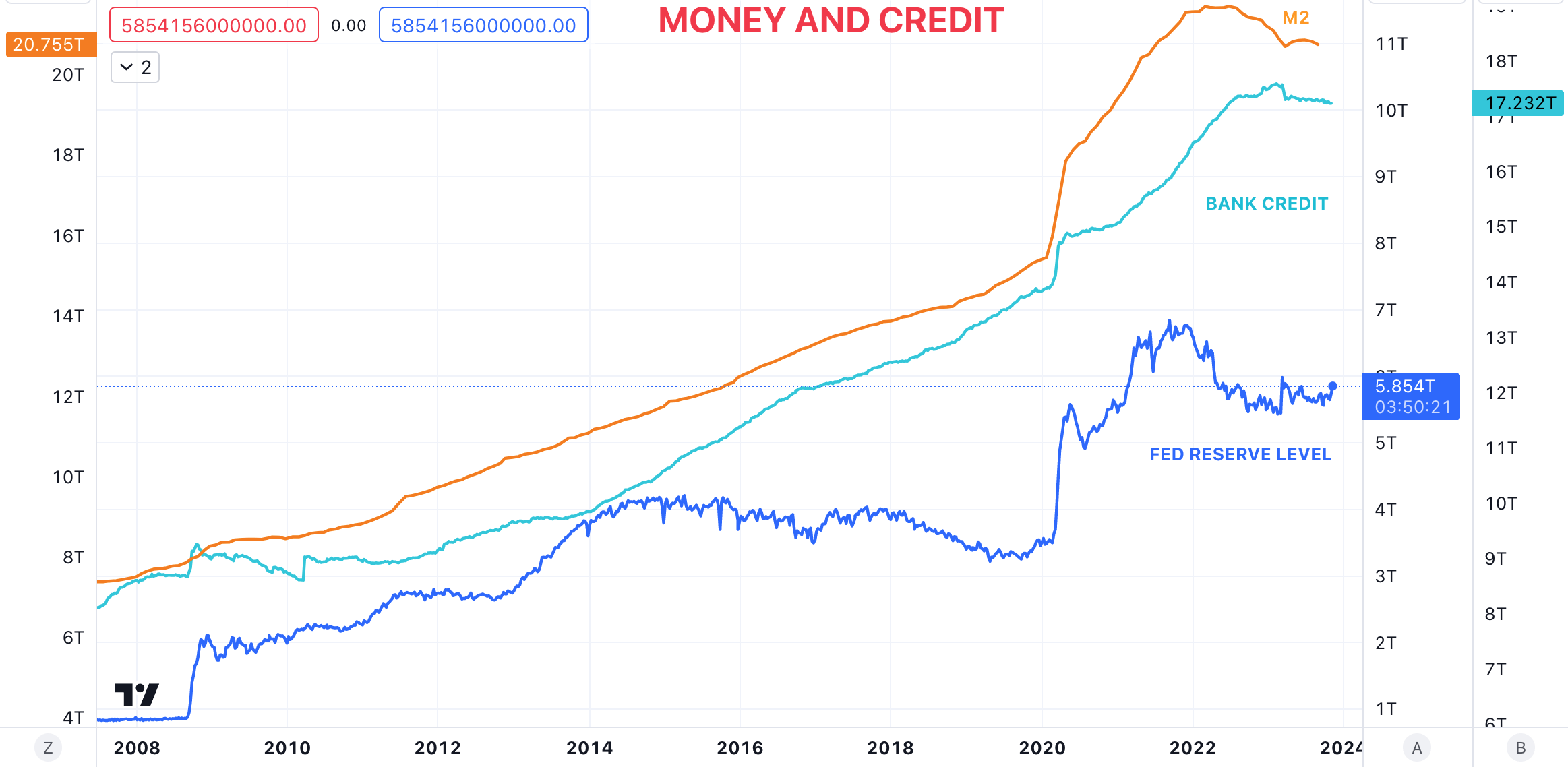

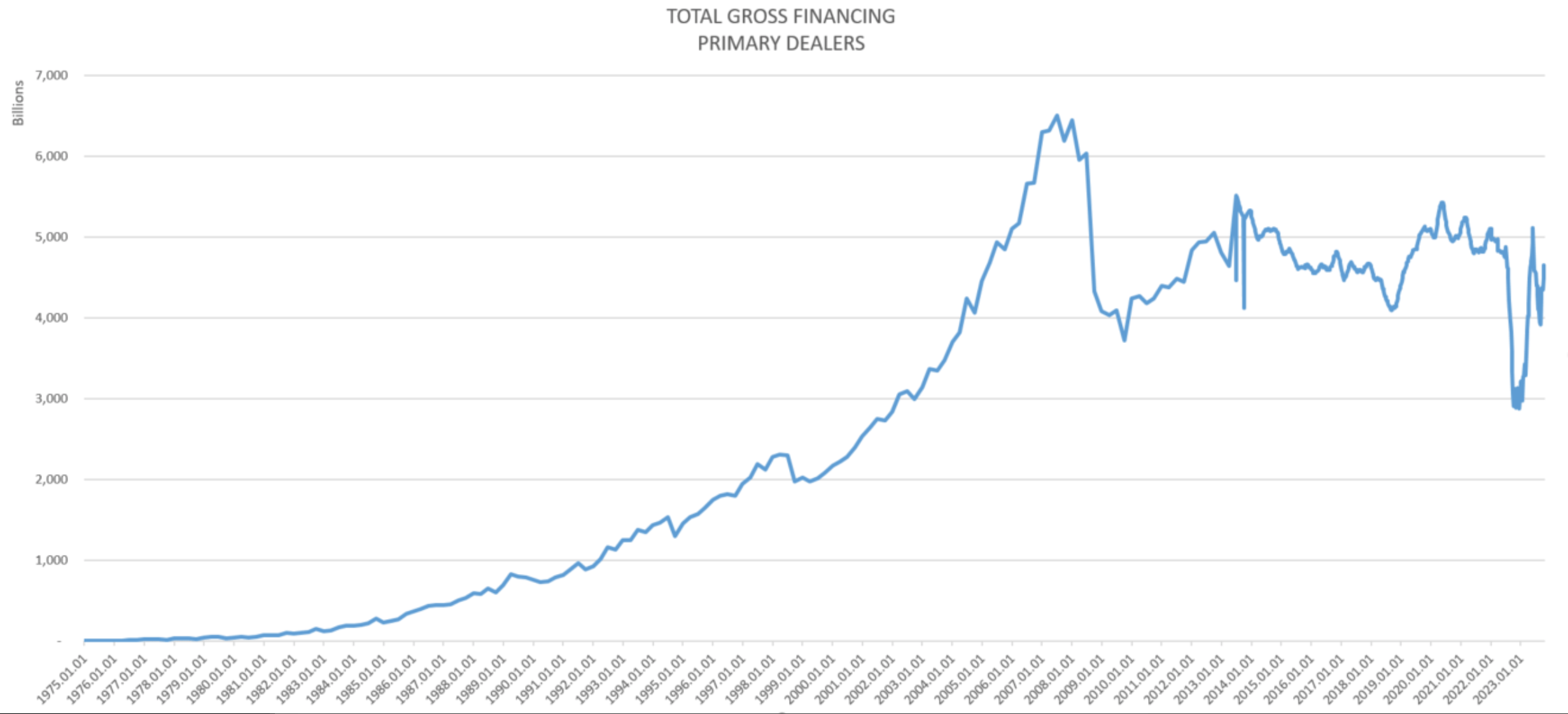

One should note that the monetary aggregate M2 is contracting, while the FED net liquidity level has been reduced as well as bank credit recently. The primary dealer's (globally systematically important financial institutions) leverage collapsed in 2022 by $2 trillion, then rebounded on Chinese reopening hopes, just to crash again by $1 trillion in 2023. Overall, the primary dealer network's leverage level has been deteriorating since 2021 which signals possible risk aversion.

{kind=link}

{kind=link}

The lending environment and lenders' potential risk appetite has clearly changed compared to the 2020-2021 refinancing boom period. We are already experiencing delinquency rises in the leveraged loan & CLO, credit card, auto loan & ABS, CMBS space. If the secondary market is less liquid for the underlying debt, lenders would be less willing to originate, which transforms liquidity problems in financial markets into real economy borrowers' inability to fully access credit. If mass maturities and refinancing meet with lender risk averseness and contracting credit availability, the liquidity situation can deteriorate meaningfully.

Interest rate projections

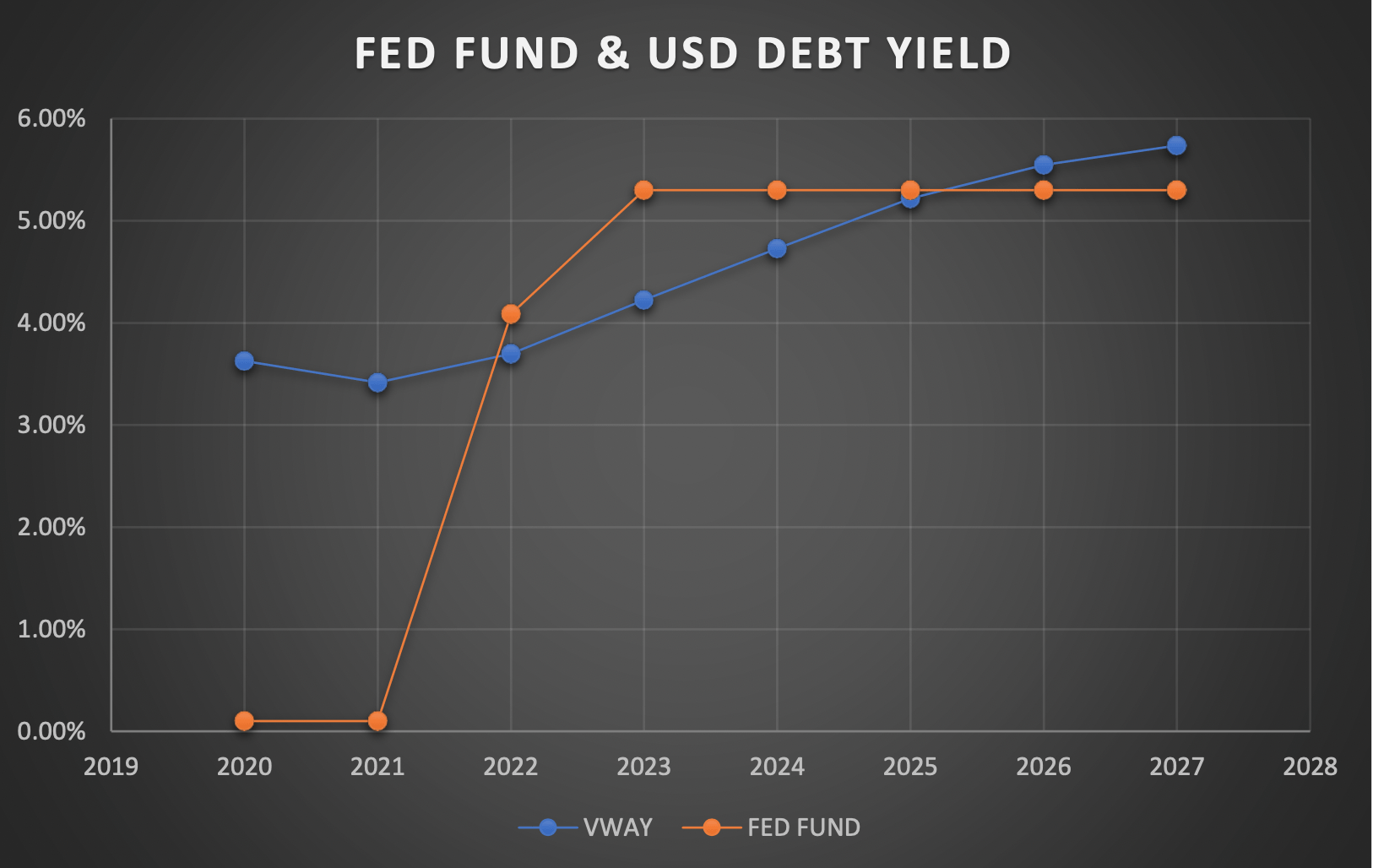

The central bank interest rate rises have only affected the floating rate debt and new issuances, as during the zero rate environment of 2020 and 2021 a large portion of current debt was refinanced and fixed at low rates. Different debt types have different lifecycles; however, based on origination data and bond maturities, we can project how the debt load interest will change over time if the interest rate environment stays where we are currently in 2023 (the FED is near the top of the cycle and signals will hold rates higher for longer). The interest rate projections were set up for each major debt type (corporate, government, residential mortgage, auto loans) and then a volume-weighted average yield (VWAY) was calculated.

{kind=link}

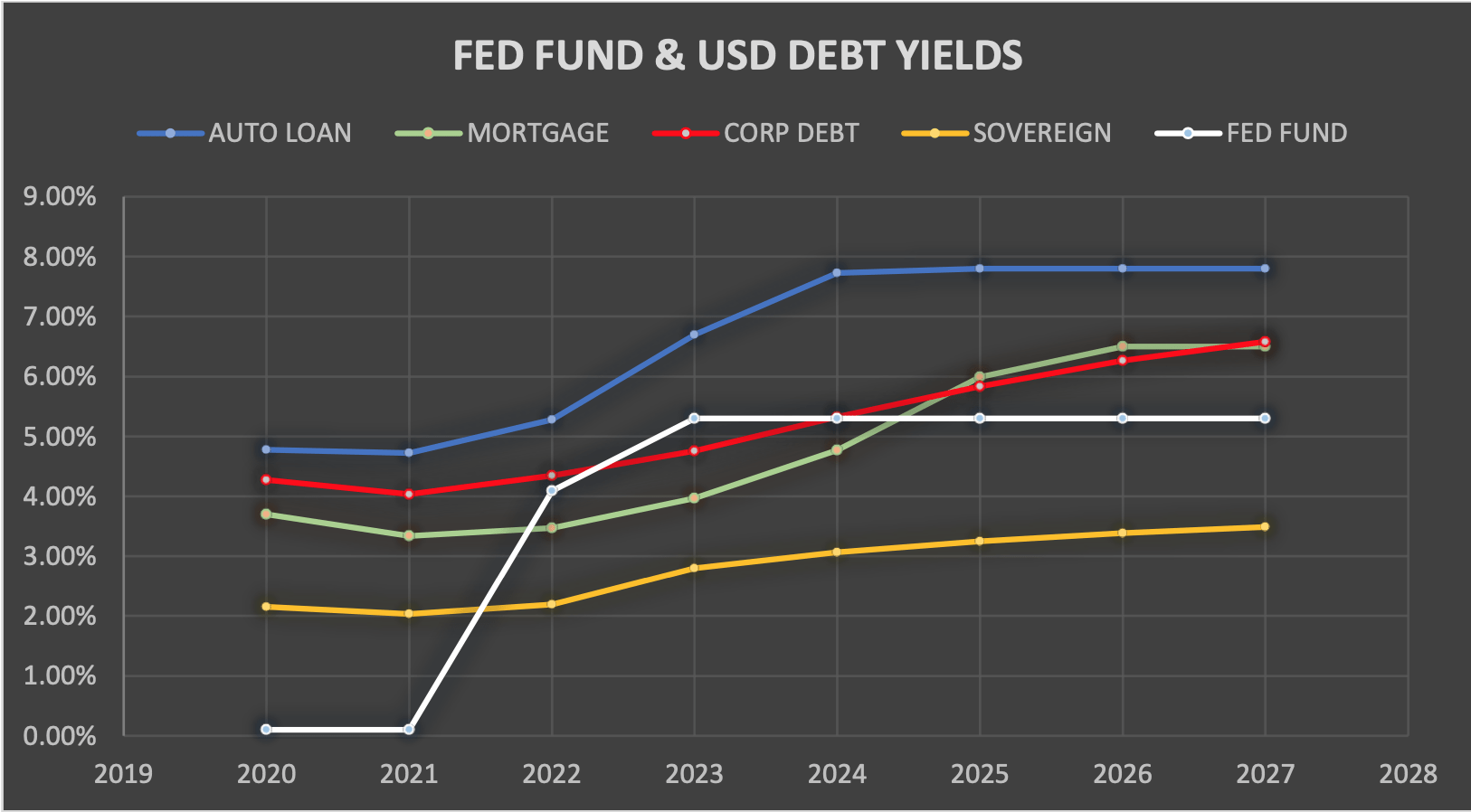

FED FUND RATE & WEIGHTED AVERAGE DEBT YIELD PROJECTION (AUTHOR,BLOOMBERG)

{kind=link}

As it is visible on the charts, currently each type of debt is yielding below FED Fund rates except auto loans and of course floating rate debt such as credit cards and some structured bonds (CMBS, CLOs, Auto ABS, etc.) Auto debt yield is changing the quickest due to the fast float turnover, so auto loan debt obligations will reach terminal yield at 8% by the end of 2024. If the residential mortgage market habits of the past 15 years continue, mortgage debt will reach terminal yield at 6.5% by the end of 2026. Corporate and government debt yields would not reach the terminal yield until the end of 2027. Note that the fed fund rate is expected to peak by the end of 2023.

The projections help us understand how the interest obligations would change in relation to the central bank rate cycle. If we look at the VWAY, it would only match fed funds by the end of 2025, and still wouldn't peak by the end of 2027. This clearly shows that the higher-for-longer policy would have lag effects of over 4 years. In comparison, from 2021 to the end of 2023, the fed fund rate is expected to change by 5.3%. In the same period, the dollar debt yield has only changed by 0.6%, and that extra interest is payable first in 2024 only). This explains well the resiliency of the US economy and financial system towards the higher rate environment. However, from 2023 to 2024, the debt yield is projected to grow by another 1.5%, and interest payments are going higher year by year.

Interest rate impact

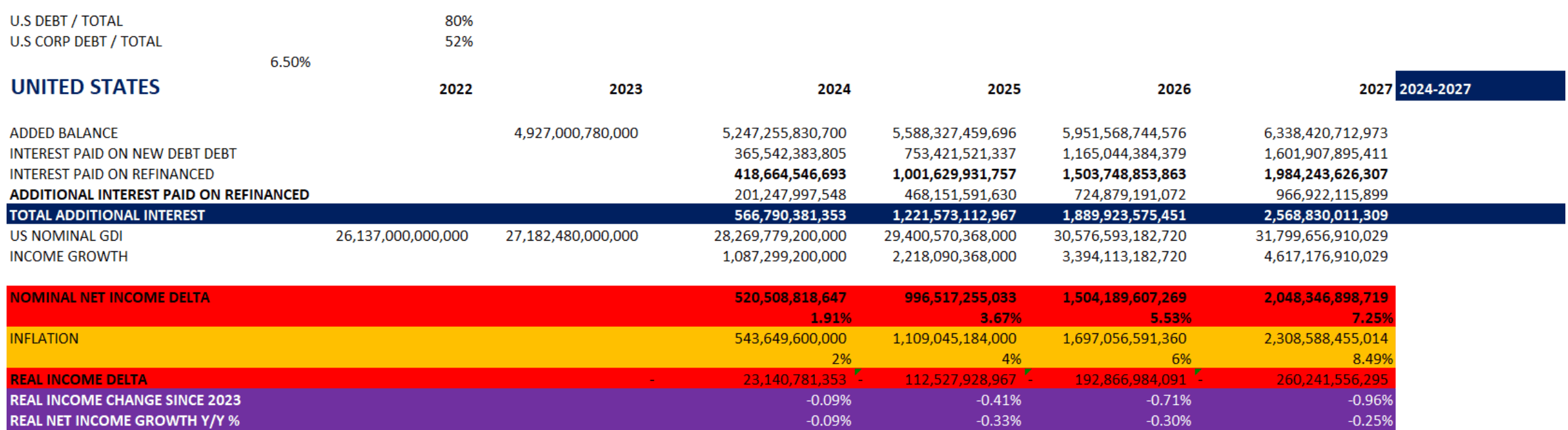

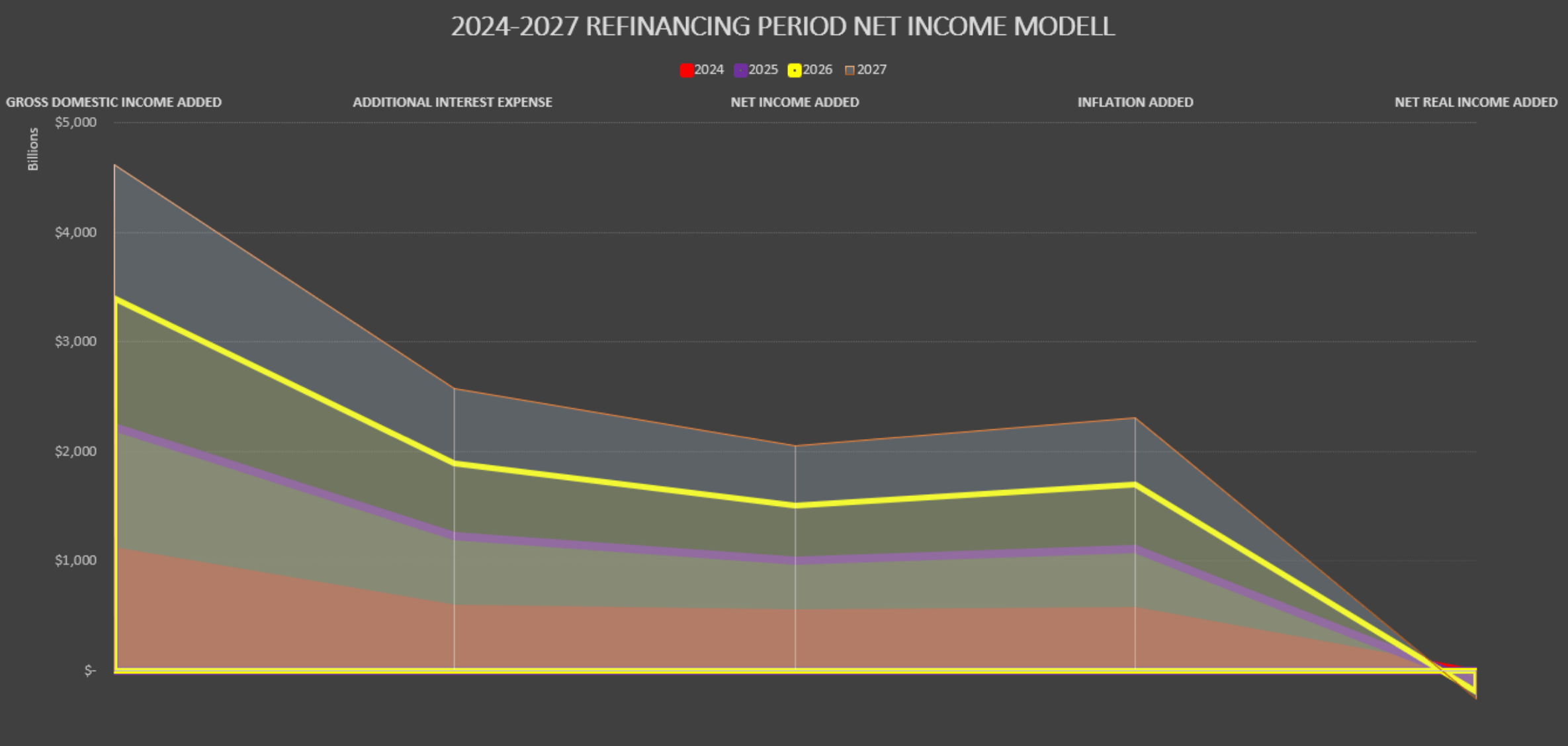

Gross Domestic Product measures government investment, business investment, consumer spending, and net exports, while Gross Domestic Income measures interest income, tax revenues, wages, profits, and exports. It is supposed to measure two sides of the same coin; however, interest expenses are not included in either of those. To assess the true net domestic income, we have to deduct the additional interest expense caused by refinancing at higher rates and adding new debt at higher rates. If nominal GDP-GDI would grow 4%, and inflation averages 2% during 2023-2027 (2% real growth - no recession scenario), then our net real income (GDI growth minus additional interest expense) would decrease at an annual rate of -0.24% from 2024 to 2027. From 2023 to 2027, the U.S. domestic net income (GDI-INTEREST) is projected to add 7.25% nominally, while inflation is projected to grow by 8.5%. That accounts for a loss of -0.96% real net income from 2024 to 2027 for the U.S. There is no recession taken into consideration, and if nominal GDI and GDP start falling, the growth can be much worse. To average -0.24% real net income growth for four consecutive years appears to be depressionary to a certain degree. This probably suggests that the economy's natural rate of interest is much lower compared to where current risk-free rates are.

The additional interest is the difference between the original rate on debt and the new refinanced rate on debt. The new additional debt is what was added to the debt balance plus the rate of principal which was paid back that year in case of loans (bonds are interest only, principle due at maturity, loans are structured to pay back principal and interest at the same time). The refinanced debt which was originated but not a new additional loan, and the new refinanced interest rate differential between the old one shows the additional interest paid on refinanced debt. All calculations are cumulative starting from 2023. Its purpose to assess the 2023-2027 maturity wall total impacts.

U.S. INCOME AND INTEREST BURDEN PROJECTION (AUTHOR,BLOOMBERG)

{kind=link}

{kind=link}

Summary and portfolio allocation

The looming mass debt maturity wall has great significance in financial and credit markets and, therefore, in the world economy as well. As both global and U.S. debt to GDP is near 350%, today's modern economies are heavily leveraged. The FED's sharp interest rate rises hasn't effected much of the existing dollar debt burden yet, as majority of the debt was refinanced during 2020-2021, and mass debt maturities will only start in 2024. As our modern economies are conditioned on ever-growing credit, the maturing debt will have to be refinanced. Through the refinancing mechanism, the higher rate environment will start effecting the U.S. and the world's interest obligations on the debt burden. The maturity wall will have two major effects: liquidity and interest payment impacts. There are already signs emerging from financial markets, which suggests refinancing liquidity can cause problems, such as contracting money and credit, money market spreads, tightening lending standards, bid ask spreads etc. On the other hand, the higher-for-longer rate policy would cause the interest burden to rise beyond 2027, which would cause the U.S. real domestic income to contract -0.24% annually from 2024 to 2027, if the GDP is capable of growing 2% in real terms. In other words, losing a total of -0.96% real net income from 2024-2027 can be considered a depression. This shows the U.S. economy's natural rate of interest is much lower where it is currently.

All of this suggests that unless supply-driven inflation reaccelerates significantly, there will be tremendous pressure on the FED (other central banks as well) to cut rates heavily, as current rate levels are much higher than current debt levels and 2% real growth would indicate. Also investors can reasonably expect that we have just entered the next default cycle in 2023. Considering demand for safety and lowering rate trajectory, long-duration treasuries TLT , IEF , TBT appears to be a top portfolio position. Meanwhile, betting against (shorting) high yield bonds SJB , HYG or CLOs and leverage loans CBBB, FTSL provides investors the exposure to widening credit spreads and deteriorating delinquency conditions. Gold GLD , IAU , UGL , and AAAU may be also a safe heaven asset to consider when allocating capital, especially in a declining rate environment for US10Y .

For further details see:

Mass Debt Maturity Wall Will Likely Pressure The FED To Capitulate