MTZ - MasTec: Solid Upside Potential From Backlogs Acquisitions

2023-03-22 05:56:15 ET

Summary

- MasTec’s revenue in the near term should benefit from healthy backlog levels and acquisitions.

- In the long term, the company should benefit from government funding for clean energy, a shift towards renewable sources, and 5G deployment.

- Based on my DCF calculations, MTZ stock is currently trading at a discount.

Investment Thesis

MasTec Inc. ( MTZ ) should benefit from strong order backlog levels and acquisitions in 2023. The company had a $13 billion order backlog at the end of 2022 and acquired five companies in 2022. In the long term, the company should benefit from healthy secular trends such as 5G deployment, increased demand for fiber connectivity, a shift towards renewable sources, and a reduced carbon footprint. Additionally, the funding from the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) should benefit the company’s order backlog in the medium- to long-term. Based on my DCF calculations, I believe the stock is currently undervalued, making it a good buy.

Growing through Acquisitions

MasTec’s acquisition strategy has helped the company diversify its business while capitalizing on growth opportunities in various end markets. The acquisitions have significantly contributed to the company’s revenue growth, which has been impressive in the last few years. The company acquired more than 15 companies over the past two years. MasTec’s revenue grew by ~55% to $9.78 bn in 2022, compared to $6.32 bn in 2020. MasTec completed five acquisitions in 2022 and fourteen acquisitions in 2021. The company significantly increased its presence in the electric distribution and transmission market from 8% of the total revenue in 2020 to 28% in 2022. It reduced its presence in the Oil & Gas market from 28% of the total revenue in 2020 to 12% in 2022. In Q4 FY22, the company acquired Infrastructure and Energy Alternatives Inc. (IEA), which is one of the largest utility-scale renewable energy infrastructure solutions providers in North America. Post this acquisition, the company’s Clean Energy and Infrastructure segment’s revenue is expected to grow from $2.62 bn in 2022 to $5 bn in 2023.

MasTec’s Liquidity and Capital Structure (Investor Presentation)

MasTec's acquisition of IEA was funded through the issuance of senior notes, which increased the company's debt by around $1.1 billion. This caused the net leverage ratio to reach 3.7x at the end of 2022, with net debt of $2.89 billion and adjusted EBITDA of $781 million. However, the company has the plan to bring down its leverage ratio in 2023 by focusing on debt repayments and improving its cash flow from operations while moderating its capital expenditures. The company is planning to reduce its leverage ratio to the low 2s by the end of 2023. MasTec's strong liquidity position of $1.2 billion at the end of 2022 provides it with the flexibility to pursue further acquisitions and diversify its business. By strategically managing its debt and cash flow, MasTec can maintain its financial strength and capitalize on growth opportunities.

What’s the near-term outlook for the company?

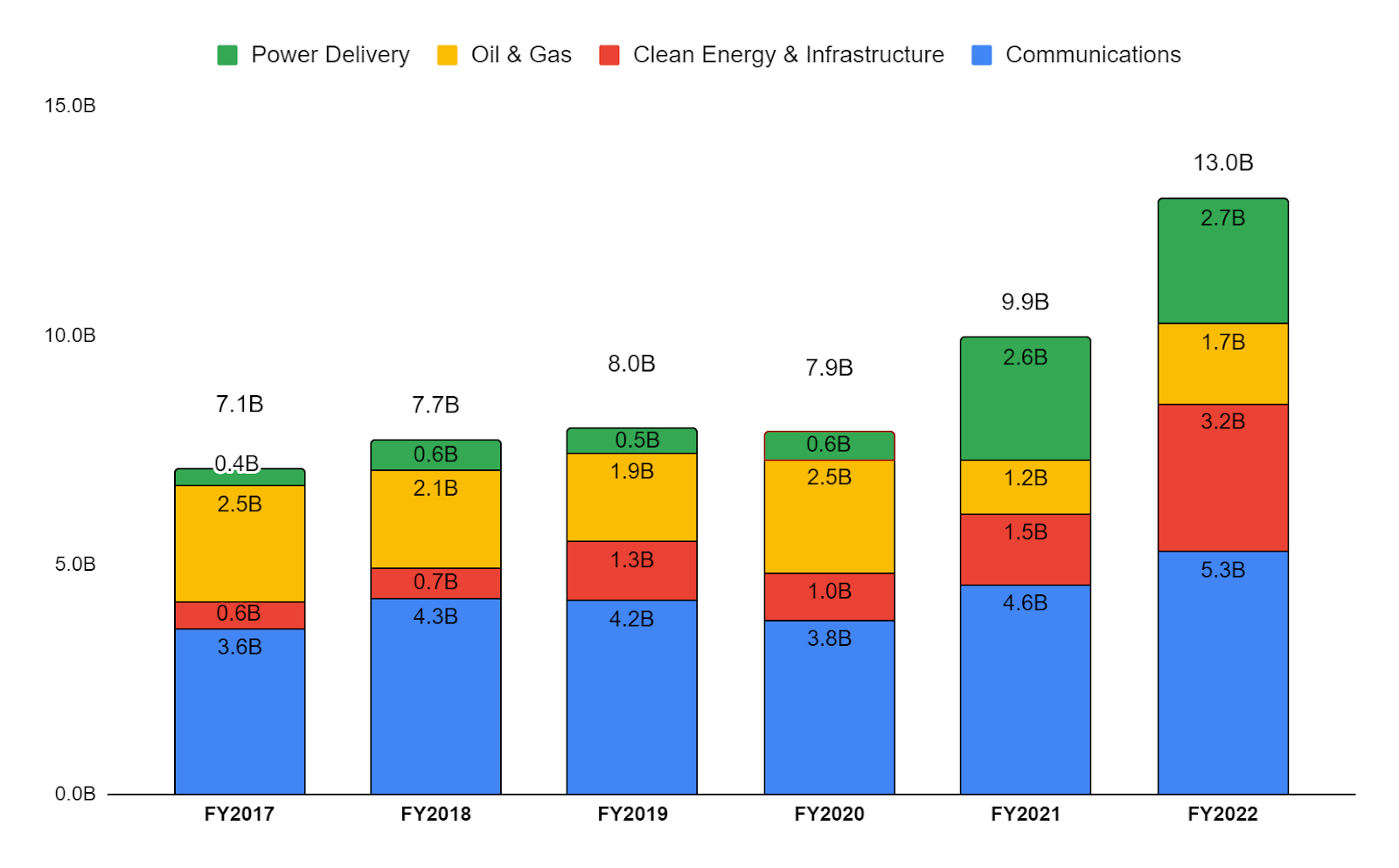

MasTec's backlog order (Created by DzD Analysis by taking data from MTZ)

{kind=link}

I believe that MasTec’s revenue in 2023 should benefit from the healthy backlog order level. The company's backlog level increased by 30% Y/Y to $13bn in 2022, excluding the $1.5bn of acquired IEA backlog, driven by robust demand across various end markets, such as power generation and distribution, telecom, and renewables. In the Communications segment, the company is likely to benefit from the growing investments in 5G and fiber deployment by companies such as AT&T ( T ), Verizon ( VZ ), and T-Mobile ( TMUS ), with AT&T recently announcing a Joint Venture with BlackRock to build a commercial fiber-optic platform in the United States. In the Clean Energy and Infrastructure segment, the company faced regulatory-related supply chain headwinds for solar renewable projects in 2022. However, this headwind should be fully gone by mid-2023, thus improving the segment’s revenue in the second half of FY23 and beyond. In the Oil & Gas segment, the company should benefit from the increased activity for projects related to natural gas and hydrogen. In the Power Delivery segment, the company faced headwinds in 2022 due to supply chain constraints. However, in 2023, as the supply chain challenges ease, the segment’s revenue should improve.

Overall, I believe that MasTec's revenue should grow in double digits in 2023, driven by healthy demand across its end markets and strong backlog levels.

Long-term growth opportunities

MasTec has healthy long-term trends across all its segments, including Communications, Power Delivery, Oil & Gas, and Clean Energy & Infrastructure. The Communications segment should benefit from the federal funding of $20 billion related to the Rural Digital Opportunity Fund (RDOF) and $9 billion in funding for 5G in rural America. Additionally, the segment should also benefit from 5G tower deployments, smart city initiatives, developing smart home trends, and the increasing need for fiber connectivity. The U.S. Infrastructure Investment and Jobs Act (IIJA) is providing approximately $65 billion to improve broadband connectivity in the country.

The Clean Energy & Infrastructure (CE&I) segment should benefit from the funding under the U.S. IIJA and the Inflation Reduction Act (IRA). Approximately $370 billion will be disbursed under the Inflation Reduction Act to improve energy security and accelerate the clean energy transition. Additionally, the trends in electric vehicles, battery storage, and a shift towards renewable energy by large corporations should benefit the company. MasTec facilitates infrastructure building and MRO activities for its CE&I customers.

The Power Delivery segment should benefit from the $65 billion investment under IIJA in clean energy transmission and the electric grid. The government plans to build thousands of miles of new and resilient transmission lines to facilitate the expansion of renewable energy. Additionally, the aging infrastructure and smart utility projects should benefit the segment. The Oil & Gas segment should benefit from the Oil & Gas Climate Initiative (OGCI) , taken by major oil companies. This initiative focuses on addressing climate change and significantly reducing carbon footprints by 2050. MasTec provides carbon sequestration technologies and pipeline infrastructure, which should help it take advantage of the ongoing carbon neutrality programs across the world.

Overall, I believe MasTec has good long-term growth prospects and is well-positioned to take advantage of these opportunities. This should benefit the company’s backlog levels and revenue growth in 2023 and beyond.

Risks

In my thesis, I have assumed the supply chain will improve over the course of 2023, which should benefit the company’s revenue growth. However, if the supply chain constraints continue to persist throughout 2023, MasTec’s growth should be below my assumptions. Additionally, the company faced certain headwinds related to regulations in its solar panel business. If these headwinds continue beyond the first half of 2023, the company’s revenue growth should be negatively impacted in the fiscal year.

Valuation

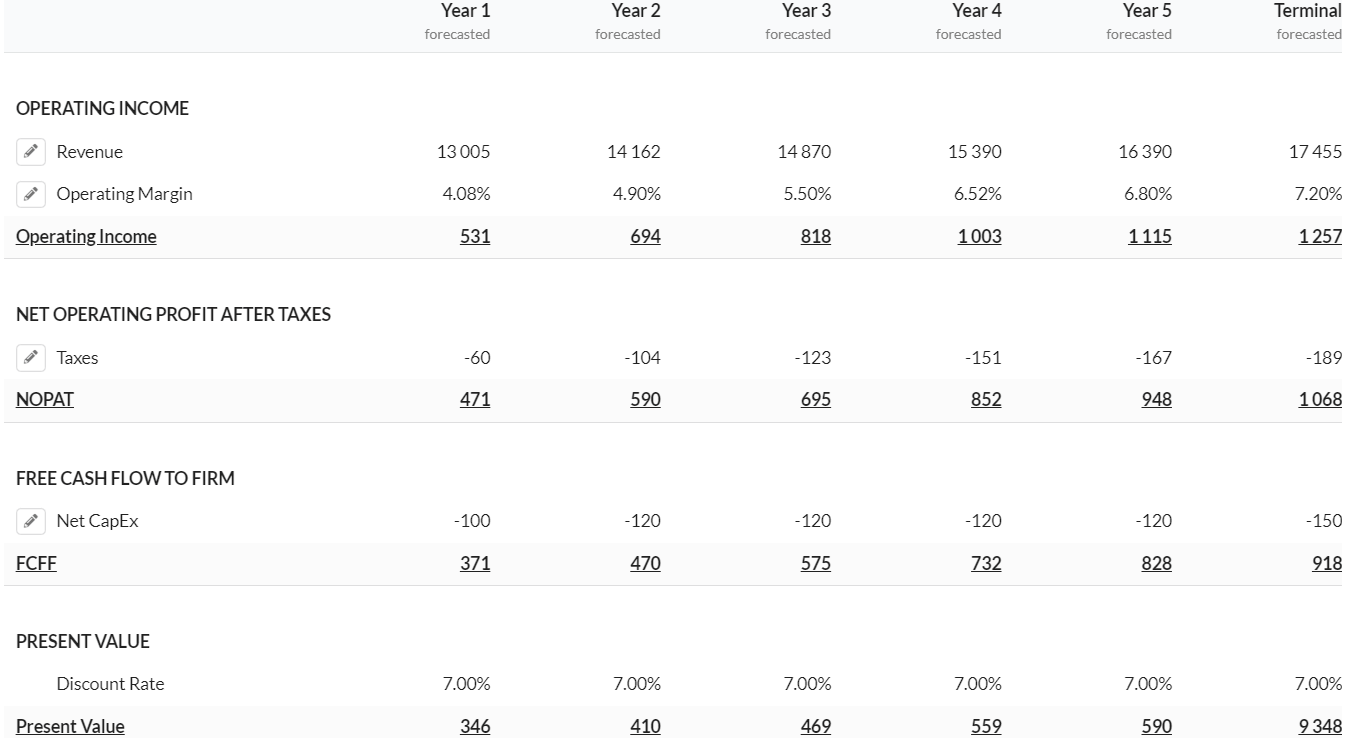

WACC calculation (Created by DzD Analysis using DiscoverCI calculator) DCF Valuation (Created by DzD Analysis using Alpha Spread)

{kind=link}

I arrived at the conclusion that MasTec is currently undervalued by conducting a DCF analysis. In my DCF analysis, I assumed revenue would grow in double digits in 2023 given the healthy demand and strong order backlog levels. Beyond 2023, the revenue growth should be between mid-single-digit and high double-digit due to the healthy trends across end markets. Additionally, I factored in the company's capital expenditure of approximately $100 million in 2023, based on the management’s guidance. This would likely impact the company's operating margins in the near term, which I expect to improve gradually as these investments come to fruition. I used a discount rate of 7.14% by using the cost of equity of 10.91% and the cost of debt of 3.57%, which is below the industry level , and arrived at a fair value of $110.83 for MTZ.

Conclusion

MasTec has strong growth prospects fueled by its robust backlog and recent acquisitions. The company's position in expanding end markets such as communications, renewables, power generation, and distribution puts it in a favorable position to benefit from secular trends. With its current low valuation, MasTec appears to be an attractive investment opportunity. Therefore, I believe MasTec is a good buy.

For further details see:

MasTec: Solid Upside Potential From Backlogs, Acquisitions