MCFT - MasterCraft: 30% Upside For Patient Investors

2023-10-02 16:33:30 ET

Summary

- MasterCraft shares have underperformed the small cap Russell 2000 Index, falling over 14% in 2023.

- The company has gained market share organically and benefits from favorable demographic trends.

- Despite disappointing guidance for the current fiscal year, MasterCraft has a pristine balance sheet and offers long-term upside potential.

Shares of MasterCraft ( MCFT ) have underperformed the broader small cap Russell 2000 Index ( IWM ) thus far in 2023, falling over 14%. While the near-term picture is murky following the post-pandemic bust in powerboat sales, MasterCraft shares offer long-term investors the opportunity to own a business which has:

- Gained share organically over long periods of time.

- Favorable demographic trends as the population ages and retirees are more inclined to spend on recreation including boats.

- Benefitted from accretive capital allocation by making opportunistic acquisitions.

- Has a pristine balance sheet with ~$60 million in net cash.

- Trades at a very low multiple of normalized earnings (shown below).

Current Results

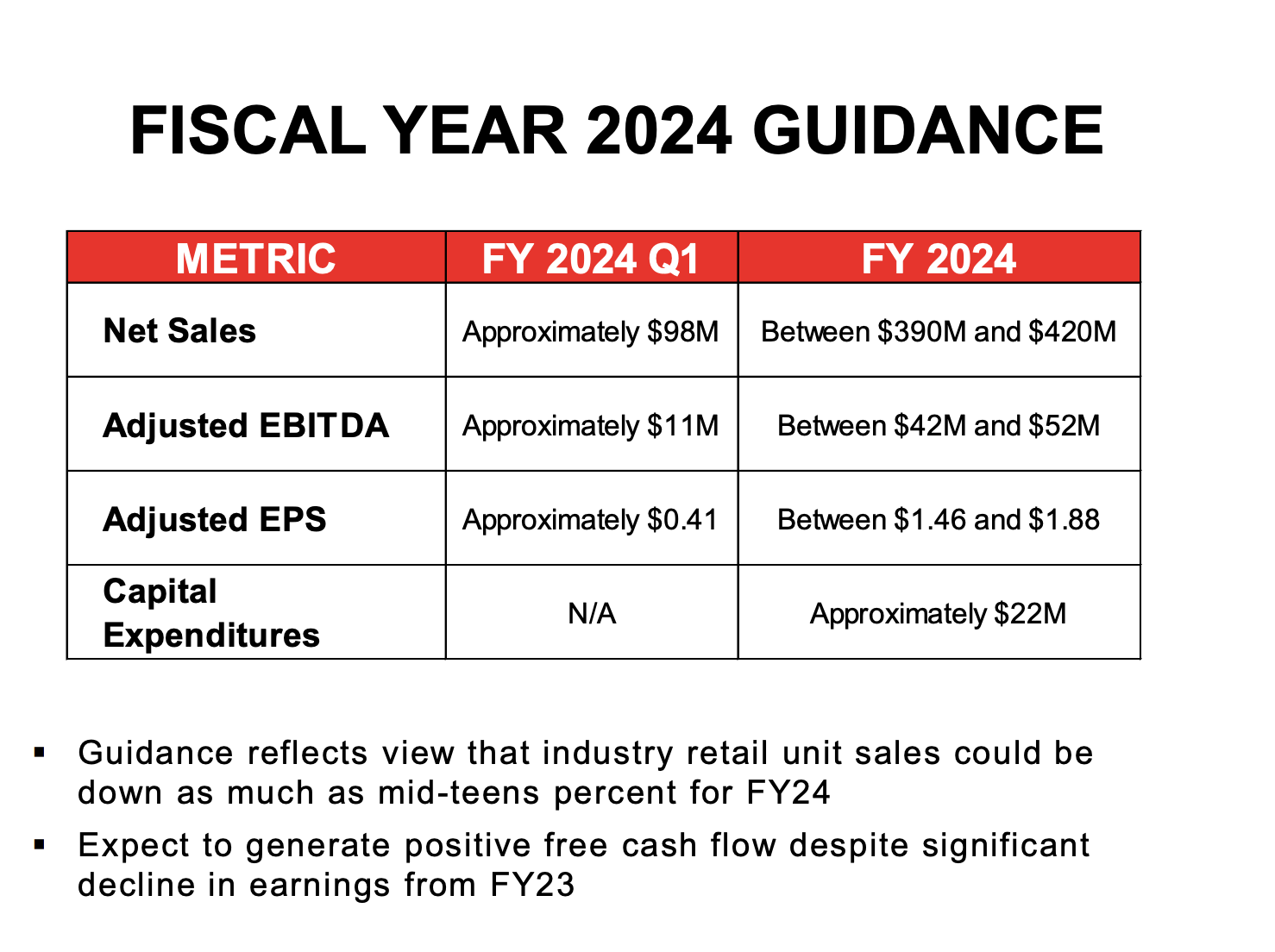

MasterCraft shares plummeted in late August after the company gave very disappointing guidance for the current fiscal year. Having enjoyed a multiyear boom as boat sales soared during and immediately following the pandemic, MasterCraft guided to a sharp fall in revenue and EBITDA in the year ahead (as shown below).

{kind=link}

At the midpoint, management is anticipating revenue and EBITDA to be down 32% and 64%, respectively from all-time record results in 2022 and 2023. 2022-23 benefitted from:

- Work From Home - work from home benefitted boat sales as some workers believed they would be able to permanently work from anywhere. As such, many moved out of cities to areas with lakes and purchased powerboats. Similarly, having Monday and Friday as work-from-anywhere options leads more people to invest in boats which could be enjoyed in 3-4 day weekends.

- Loose monetary conditions - home price appreciation and ultra-low interest rates in 2020-21 allowed people to take out low rate second mortgages to purchase powerboats.

- Excess savings - the soaring savings rate (result of stimulus and people sheltering in place rather than traveling) provided funds for the purchase of powerboats.

- Supply chain disruption led to low channel inventories which gave more pricing power to MasterCraft which led to limited discounting and improved gross and operating margins.

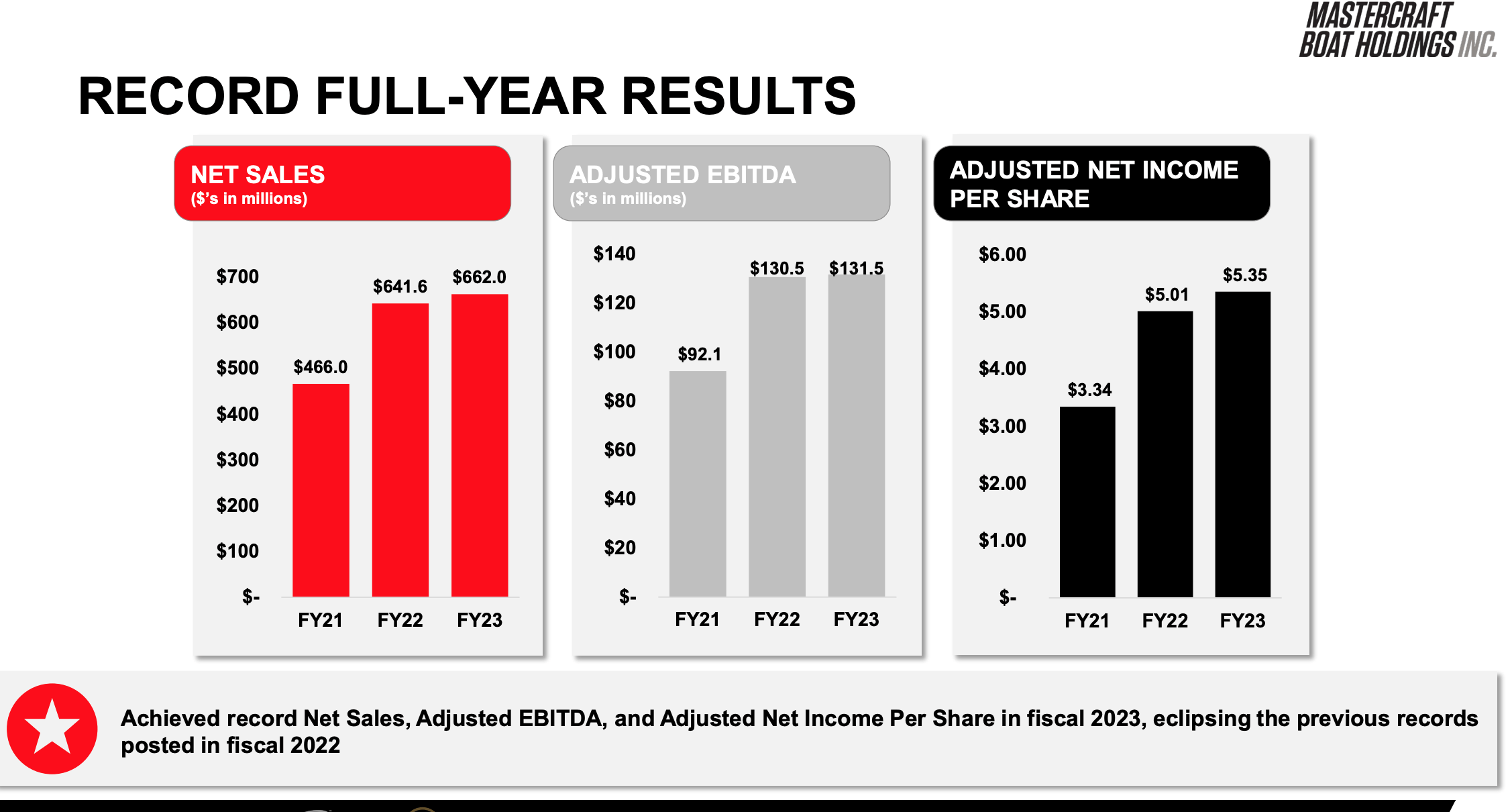

This led to a fantastic set of results in 2022-23 as shown below.

{kind=link}

As we sit today, consumer confidence has declined while interest rates have soared. Meanwhile, the migration of workers out of urban areas has slowed significantly. Lastly, the dealer channel is now somewhat oversupplied leading to discounting which will compress gross and operating margins.

While I don't anticipate MasterCraft getting back to 2022-23 levels anytime soon, as I show in the next section, I believe that normalized results will be well in excess of those expected in the current year.

'Normalized' Earnings & Valuation

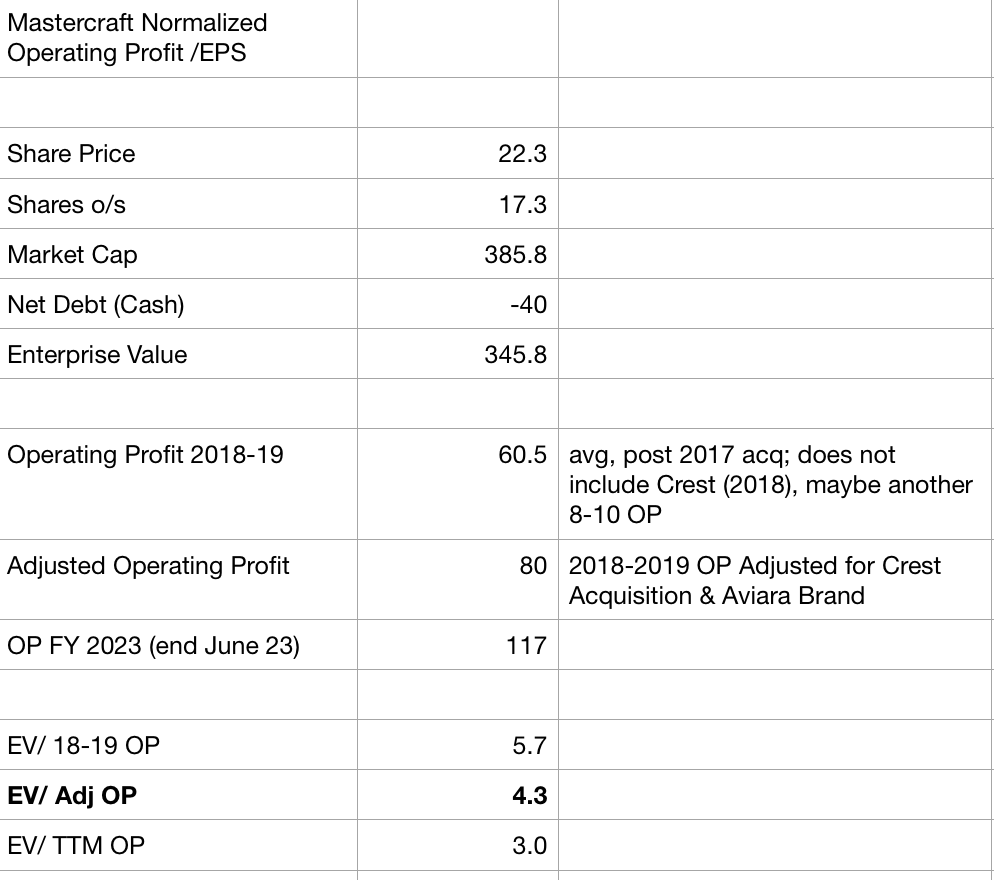

Below I attempt to estimate normalized EPS for MasterCraft:

Normalized Operating Profit & Valuation (Company Filings, Author Estimates)

{kind=link}

To estimate normalized earnings power, I look back to the pre-pandemic period of 2018-19. The early part of the 2010s was marred by an excess inventory and weak consumer spending following the GFC which led to significant deterioration in boat sales. Earnings inflected upward in the middle part of the decade. 2018-2019 are illustrative of what I believe MasterCraft can earn in a good but not overheated external environment.

From here, I adjust for the 2018 acquisition of Crest as well as the organic development of the higher-end Aviara brand which was created in late 2018/19 and only began contributing from 2020. This gets me to a normalized operating profit of ~$80 million, implying an EV/OP of just over 4x. After taxing operating profit and adjusting for net cash per share, MasterCraft trades at just 7x normalized EPS.

I think a more appropriate valuation is around 10x normalized EPS. Taking into account ~$3/share in cash on the balance sheet, this suggests a fair value of ~$29 per share, or 28% upside. My 10x multiple is a significant discount to the broader market and takes into account the cyclicality of the powerboat industry.

Conclusion

Despite the bleak near-term outlook, looking out 2-3 years, I think MasterCraft is poised for a significant rebound in profitability as excess inventory is cleared from the dealer channel and profits rebound. With a large net cash position on the balance sheet, MasterCraft is well-positioned to withstand a prolonged downturn and ultimately emerge in a stronger position. Shares trade at a low multiple of normalized earnings and offer reasonable upside to long-term, contrarian investors.

For further details see:

MasterCraft: 30% Upside For Patient Investors