MCFT - MasterCraft: A Tale Of Cyclical Headwinds And Secular Tailwinds

2023-09-11 08:10:46 ET

Summary

- MasterCraft offers a terrific risk/reward profile over the next few years, even with elevated interest rates or an economic contraction.

- It has a net cash balance sheet, a largely variable cost structure, excellent margins, and cash flow, and is well positioned for long-term growth.

- It has tremendous brand equity, an exceptional innovation track record, and is a commendable operator.

- The discount at which it trades to peers is untenable and likely to narrow or be eliminated.

Introduction

MasterCraft ( MCFT ) offers a tremendous opportunity for the long-term investor based on the following assumptions:

- There will be far more recreational boats sold this decade than last, even with higher average rates.

- Its market share will remain stable or improve.

- That the discount to peers narrows.

I believe these assumptions are highly probable, and I’ll cover each in detail. However, what makes this such a great risk/reward setup is that none need to be true for MasterCraft to be a more than satisfactory investment.

Overview

MasterCraft is a leading recreational powerboat manufacturer based in Vonore, Tennessee. North America accounts for approximately 95% of the company’s sales, and it operates in three segments.

Ski-Wake (70% of revenue)

MasterCraft has been manufacturing ski-wake or “towboats,” as they are often called, for half a century. The brand has been #1 by market share for the last six years . It is closely followed by Malibu ( MBUU ), which is by far its most formidable competitor. However, when including Malibu’s entry-level brand, Axis, it has the most share (~30% combined) .

Collectively, the two companies dominate the category with about 50% market share. The category is an oligopolistic one, with the top five brands accounting for about 72% of the market . MasterCraft’s retail prices range from $90,000 to $300,000 and $80,000 to $300,000 for Malibu.

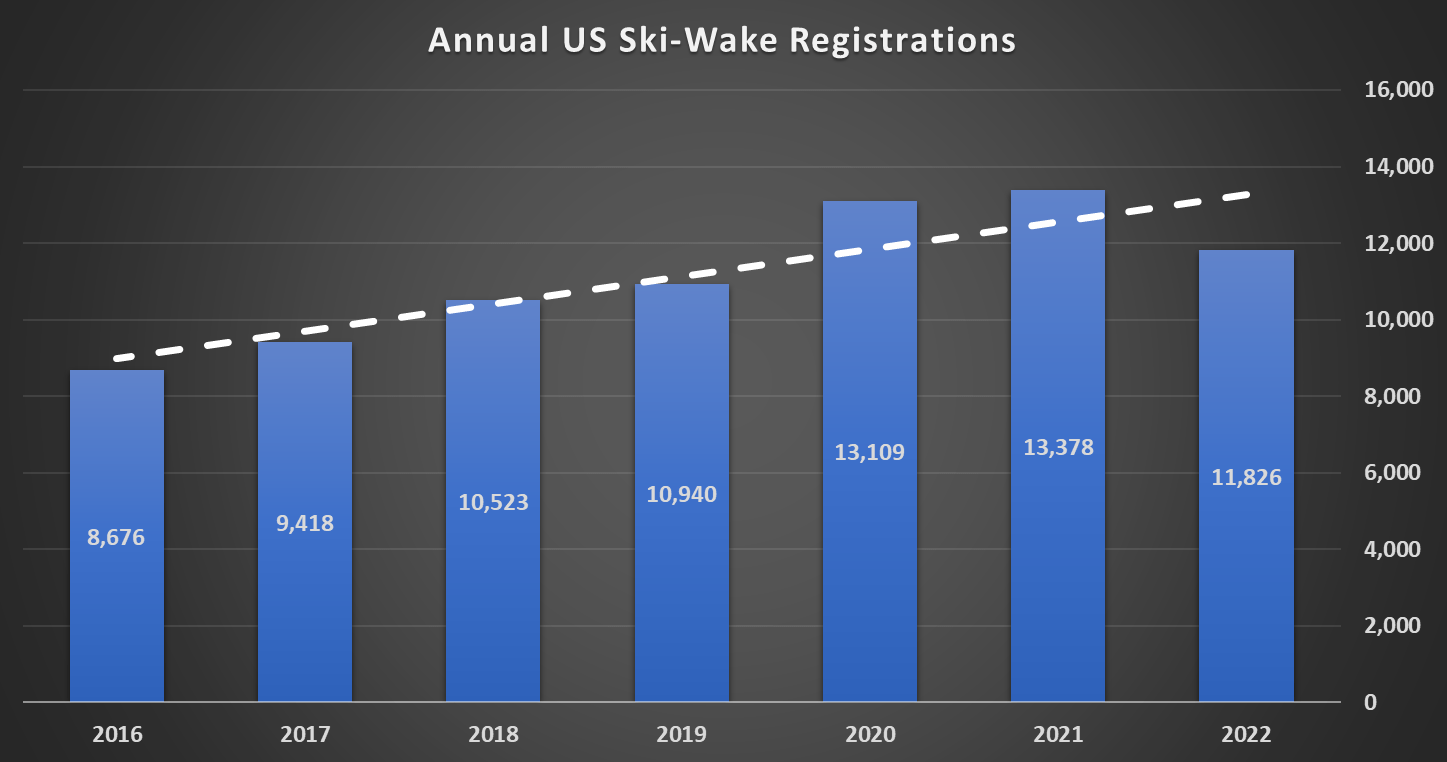

As you can see below, the ski-wake category was in a secular uptrend before the pandemic hit.

Author's calculation, Trade Only, SSI data

{kind=link}

Note: The increases above trend in 20’ and 21’ were almost exactly offset by the decrease in 2022. We will examine this point in greater detail later.

The chart above uses SSI reports, which are compiled using state DMV registration data and other sources. As I can only access the preliminary reports , which do not include data from every state, the above chart understates the number of new registrations. However, it is still a reasonable estimate for y/y relative change. In calendar 2022, for instance, MasterCraft delivered 3,487 wholesale units and had a market share of 20.8% . However, retail sales exceeded wholesale, which means new registrations were above 16,764 for the category.

The pandemic resulted in a surge in new boat sales, with about 30% coming from first-time boat buyers, which appears to be slightly above the typical ratio. In other words, the demand for new boats is primarily a function of the replacement cycle. Although this is anecdotal and therefore cannot be quantified, many customers, as I was informed by the dealers I spoke with, trade up within five years on account of being within the manufacturer’s warranty window. This makes resale much easier. “A lot of people sell at 2-3 years, depending on how many hours they put on the boat,” one dealer observed.

This category has a unique characteristic that must be understood when thinking about its long-term prospects. MasterCraft, Malibu, and their peers don’t sell a product; they sell an experience. To own one is to transform your social experience completely. This can be difficult for people to understand if you have never been on one. This is undoubtedly the case with other recreational boat categories, but not to the same extent.

I've spent a couple of summers in Canadian cottage country and have been on a few. I've observed that social dynamics with friends and family change measurably on and off the boat. It creates an environment in which you cannot only connect with people in a new way but are bound to. And rather than the boat becoming a part of their social lives, it becomes the center of their social lives.

Later, we’ll examine MasterCraft’s competitive position within this category and whether it's likely to strengthen or weaken, primarily through qualitative comparisons to Malibu.

Pontoon (21% of Revenue)

The company entered the pontoon category by acquiring Crest in 2018. In 2022, Crest had approximately 4% market share , which was flat y/y. The competitive landscape is concentrated, but less so than ski-wake, with the top five brands accounting for about 52% of the market. As of 2021, Crest was ranked #9 by market share.

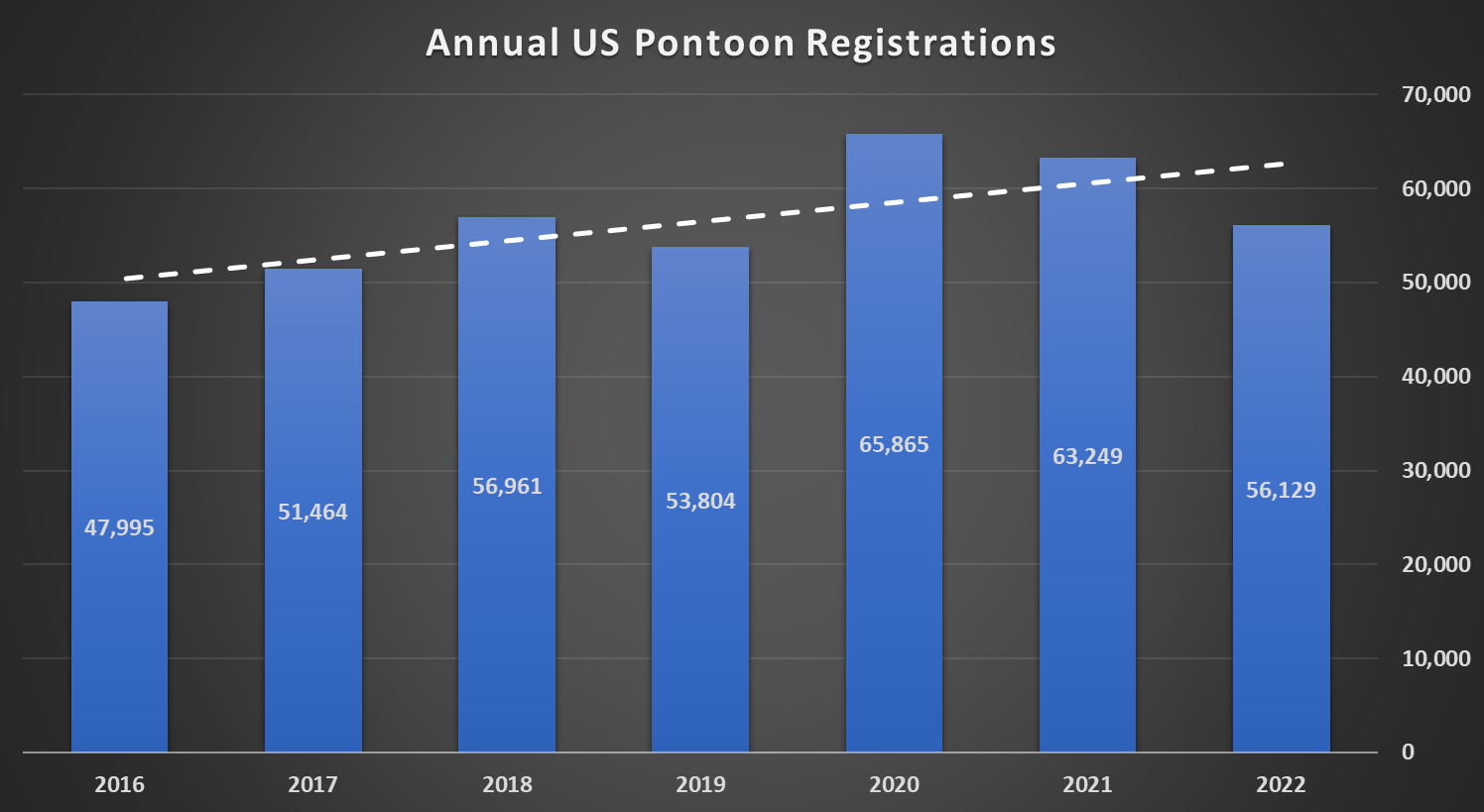

With all the bells and whistles, an “ultimate luxury” Crest pontoon retails for more than $200,000. However, its 2023 ASP was $50,000, which would approximate an average retail price of $70,000 based on typical dealer margins. Pontoons were also growing in popularity before the pandemic. As of 2019, over 1.1 million pontoons were registered in the US, and over half were purchased new or pre-owned in the preceding five years.

Likewise with the ski-wake data, the chart below understates total new registrations, which was above 80,000 units in 2022 based on Crest’s market share and units sold.

Author's calculations, Trade Only, SSI data

{kind=link}

In my view, the long-term outlook for this category is very favorable. This is evidenced by, among other things, companies from different categories entering the space in recent years, with still more to come. For instance, Malibu has expressed keen interest in entering the market : “We are going to be in pontoon. So, if there's not an acquisition to be made, then we will greenfield pontoons.”

Since acquiring Crest, the company has revamped all three product lines, and management believes it has a strong value proposition : “We think the price is right and the product is right.” Although I agree that they have a solid value proposition, I believe this is the category in which they are least differentiated. For this reason, I don’t expect a material change in its market share in the near term. However, due to the sheer volume in this category, a 1% increase in market share would result in a $40m increase in revenue vs. $23m for ski-wake based on current ASPs and 2022 registrations.

Crest also expanded its distribution network from 161 to 185 locations in 2023. You can check out Crest’s 2024 lineup here .

Luxury Day Boats (9% of revenue)

The company’s newest brand, Aviara, entered the luxury day boat market in F2020. It has four luxury bowriders, ranging from 28 to 40 feet, available in outboard and sterndrive propulsion. Retail prices range from approximately $200,000 to over $1,300,000. Aviara competes with Malibu’s Cobalt , which makes cruisers and bowriders ranging from 22 to 36 feet, with a retail price range of $75,000 to $625,000.

Aviara’s sell-through rate has far exceeded management’s expectations. In fact, it ended 2022 with almost no dealer inventory available for sale . In 2023, Aviara grew revenue by 50% to $52m but is still operating at a loss due to startup costs and the associated operational inefficiencies. However, the loss shrank to $4.5m from $9m in 2022.

Like with other categories, the total addressable market increases as you go down in size. Aviara recently introduced the AV28 for F2024, its first 28-foot offering, which management expects to be a “big part” of Aviara’s growth for the year.

In my view, Aviara is amply differentiated, so I expect this to be the category in which the company captures the most share over the long term.

Current Headwinds

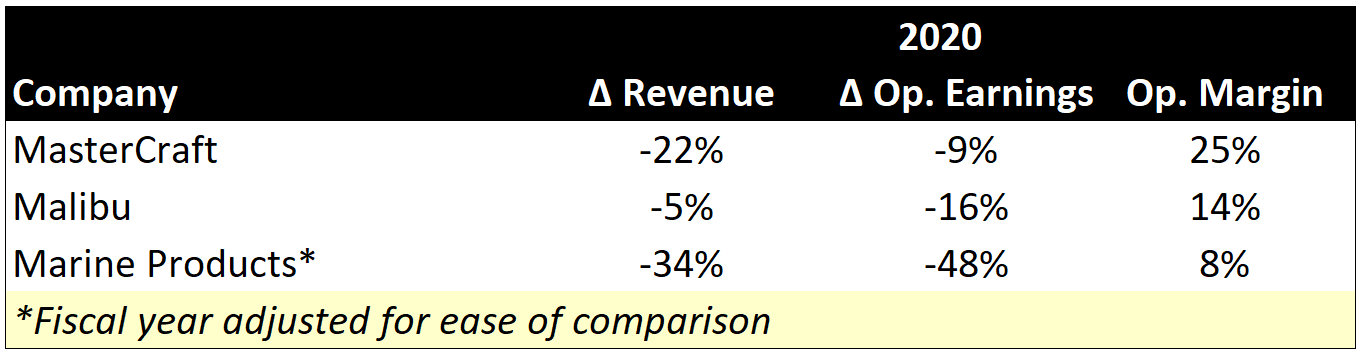

Now that supply has caught up with demand, inventory levels at many dealers are now at or above pre-pandemic levels, according to various sources. The cost of boat ownership has also risen dramatically, thanks to higher input costs and interest rates. These factors have conspired to reduce consumer demand and increase floor plan carrying costs for dealers, hurting their earnings and cash flows.

“We are increasingly cautious as demand signals are pointing towards a retail slowdown.” Said the CEO of OneWater Marine ( ONEW ), a dealer with 100 locations, during an earnings call in August.

In response, dealers and OEMs have become more aggressive with promotional activity, putting pressure on margins. This is perhaps best captured by an anecdote shared in the same call. " We were scratching for every deal. And it got to the point where a customer would come in, you would talk to them, build a relationship, give them a price, they'd leave. They'd come back three days later with a competitor with a much better price, you would try to work them on pieces and benefits and sell them and give them a new price. They leave for 4 or 5 days, they come back with a cheaper price. I mean, it was really, we worked every deal till there was no grub left.”

However, he noted that “premium inventory is still selling very well.” The softening in demand is disproportionately coming from the entry-level consumer, who is more likely to finance purchases and, therefore, is most sensitive to the price of credit. This is likely to have a greater impact in the pontoon segment than the ski-wake segment, as pontoon consumers are more price-conscious , and there is a higher percentage of retail financing.

It is also worth mentioning a relatively new concern facing the ski-wake category. Sterndrives, a market in which Malibu’s Cobalt brand dominates, now produces better waves than ever. Regarding this development, Malibu’s CEO explained , “Are they [waves] a 7, 8, 9, 10? No. But for that entry-level customer, they don't necessarily need that 7, 8, 9, 10. And so they're looking at maybe other boats that do other things.”

It is difficult to quantify how significant a problem this is or could become. However, I suspect this is not an intractable problem for either company. In a nutshell, the marine industry is a cyclical one, and 2024 is looking comparatively gloomy to 2023. However, it appears that MasterCraft and its peers will navigate the downturn unscathed, based on current forecasts.

“ I want to be very clear that this is not 2009 when the customer disappeared,” declared Malibu’s CEO in its last earnings call .

Looking Ahead

“It’s tough to make predictions, especially about the future.” Yogi Berra once quipped.

Before getting to the long-term view, I think it’s important to review management’s guidance for the year ahead, particularly since there may be some confusion about the disparity between it and Malibu’s guidance. Malibu has forecasted a mid-to-high teens revenue contraction in F2024, compared to MasterCraft’s 39% decrease at the mid-point. On the surface, this suggests that MasterCraft is much more economically sensitive. But looking deeper, we see that the disparity is less wide. The difference between the two can be explained thus:

- With inventory levels exceeding optimal levels, MasterCraft’s projected wholesale revenue contraction is larger than the expected retail contraction. Management estimates the difference is about 900 units across MasterCraft and Crest (approx. equal split). Using 2023 ASPs, this is equivalent to an $85m difference in revenue. After this adjustment, MasterCraft’s anticipated revenue contraction is 26%.

- Malibu’s saltwater segment’s wholesale revenue is expected to exceed retail sales due to below-optimal dealer inventories, assuming what is considered optimal isn’t reassessed downward.

- Finally, the expectation that retail sales for Malibu’s other segments are more resilient than ski-wake is probably embedded in the forecast.

However, a virtue of MasterCraft’s management is that they recognize Yogi Berra’s wisdom, as evidenced by their track record of under-promising and over-delivering. Embedded in their guidance is an extrapolation of recent retail trends with no change in interest rates. For reference, the market is pricing in a rate decrease of ~30bps by June 2024 , less than the anticipated ~68bps as of early July 2023.

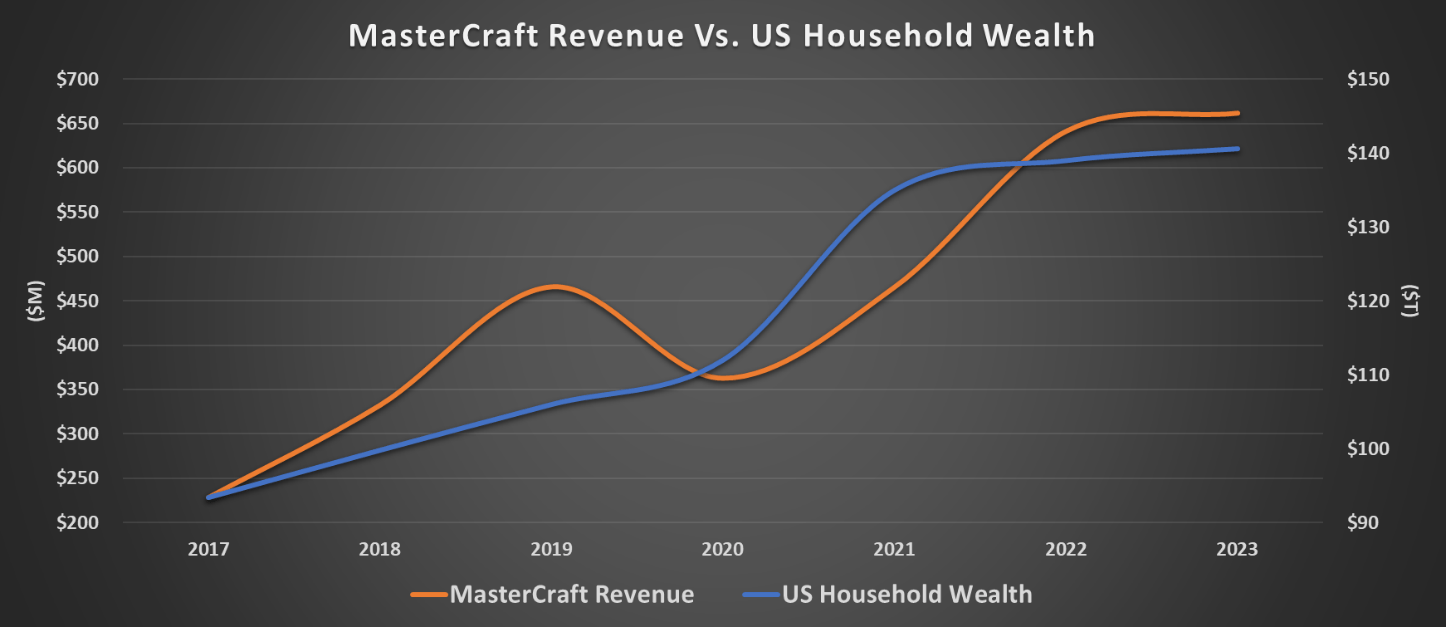

Turning our attention to the long-term, if you expect US household wealth to grow, it is hard to avoid the conclusion that MasterCraft’s business will grow along with it. That is, of course, unless you see some adverse industry or competitive shift to which it cannot respond.

Company disclosures, Federal Reserve data

{kind=link}

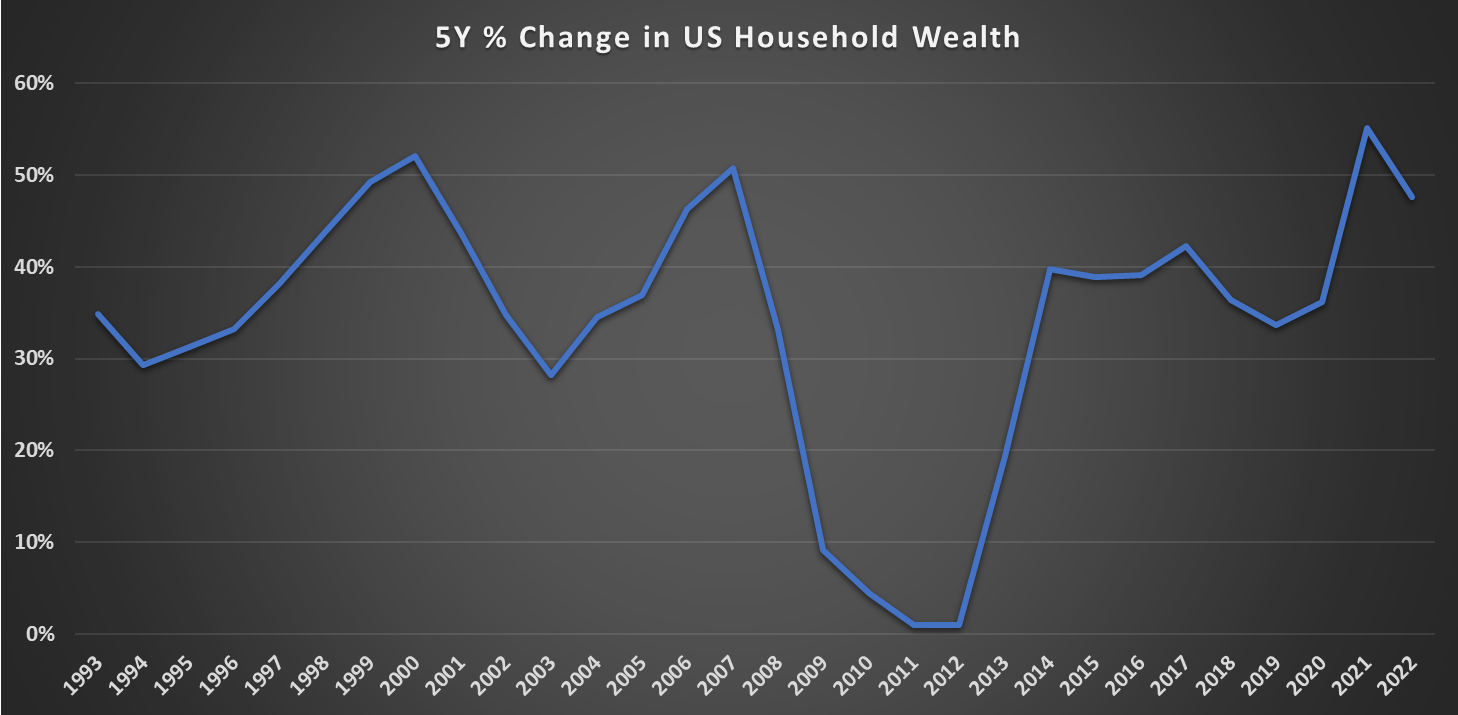

Even if we assume no growth in household wealth through the remainder of the decade, there would likely be an overall increase in recreational boat sales. As with an increasing number of registered boats comes the attendant replacement demand. Moreover, at least since the early 90s, there has never been a five-year period in which US household wealth declined, although it came close after the Global Financial Crisis ((GFC)).

Author's calculations, Federal Reserve data

{kind=link}

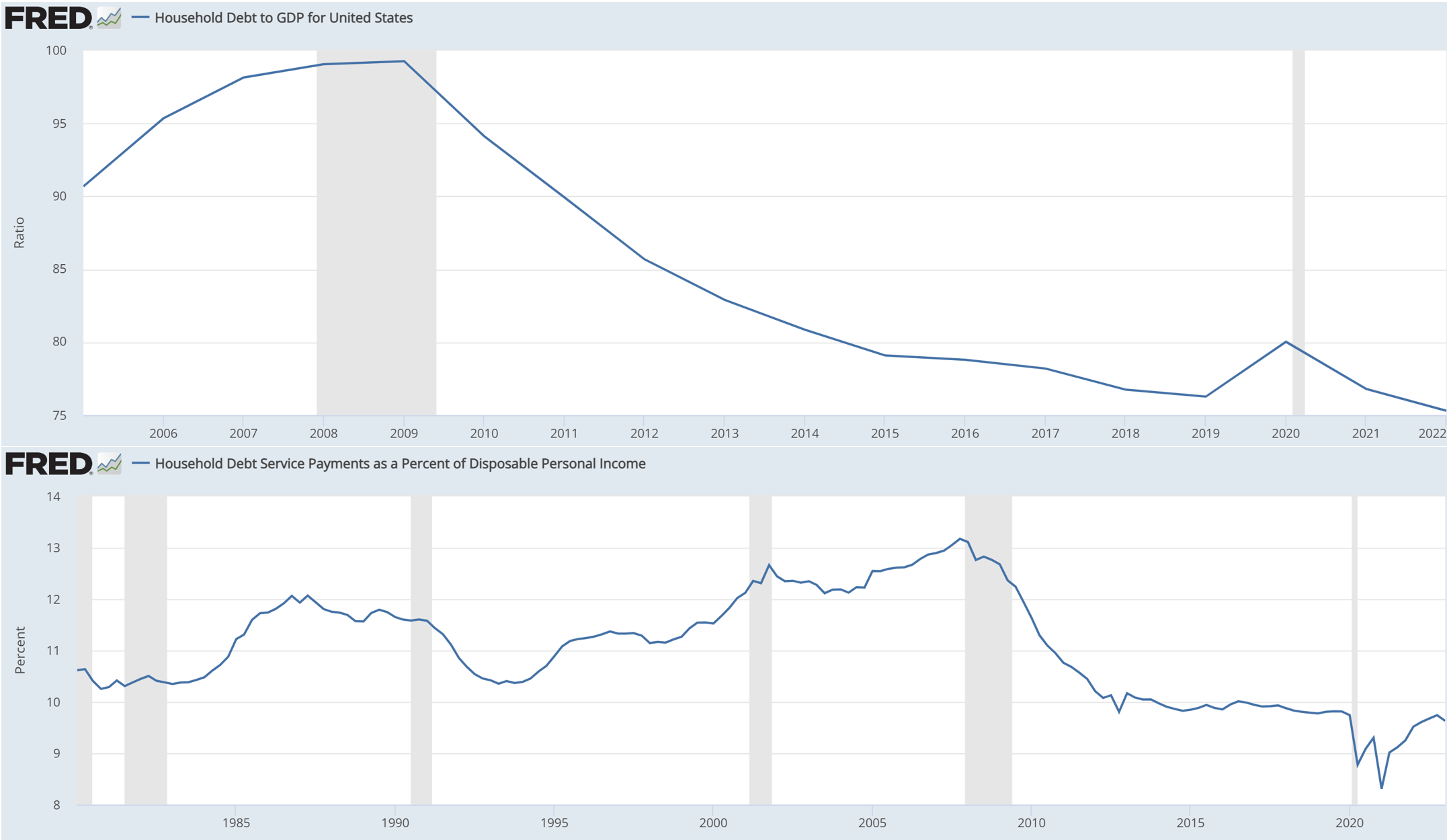

But the current environment has little resemblance to the GFC, with household debt to GDP at a multi-decade low. And even with higher rates pushing up debt servicing costs, they too are at a multi-decade low.

{kind=link}

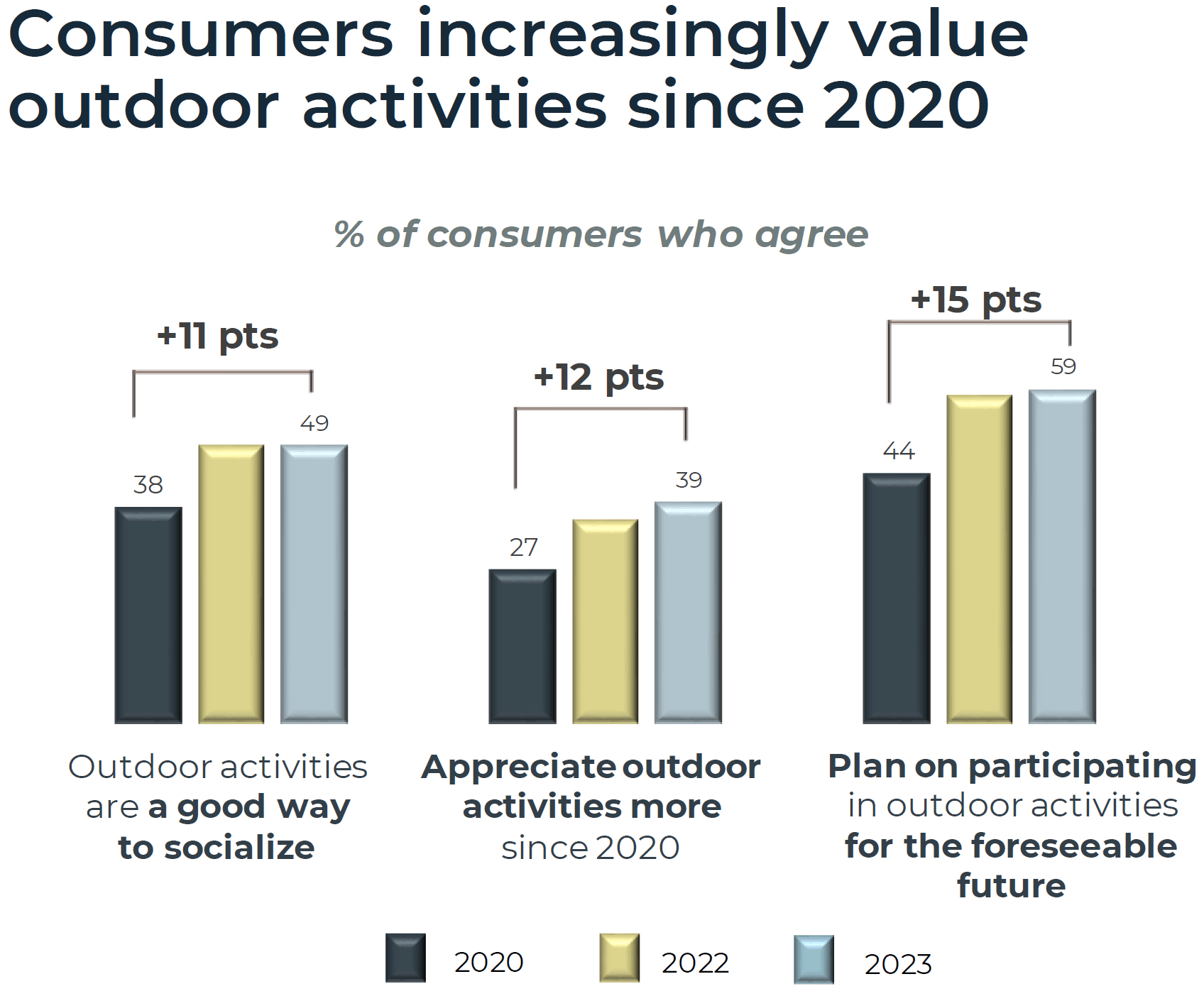

Moreover, consumer behavior patterns appear to be shifting favorably for the industry.

Winnebago Industries Spotlight Survey 2020-2023

{kind=link}

Earlier, I highlighted that the ski-wake category was back in line with the pre-pandemic trend on a cumulative basis. During that time, the Bank Prime Loan Rate was between 3.5% and 5.5% . With Prime now at 8.5%, it’s unclear what the short-to-medium-term trend will look like, but I’ll try unpacking it.

During the first six months of 2023 (FQ3/Q4), the busiest retail season, Prime averaged 7.92% compared to 3.61% in the prior year period. MasterCraft delivered 6,377 units in F2023, down 6.9% y/y. If we adjust for the ~900 additional units of above-optimal dealer inventory, units were down 21.6%. This seems to align with management’s F2024 forecast if we assume slightly lower ASPs due to customers mixing down.

With debt servicing costs up ~120% and units down ~22%, we can see the ratio was above 5:1. It would be nice if we could extrapolate this ratio to any future rate change, but the real world isn’t so simple. As previously noted, F2023 was coming off the back of two of the strongest years the industry has seen. So, we must assume that some replacement demand was brought forward and was, therefore, understated in F2023. For this reason, I think the “natural demand” is slightly higher than guidance implies, all else equal.

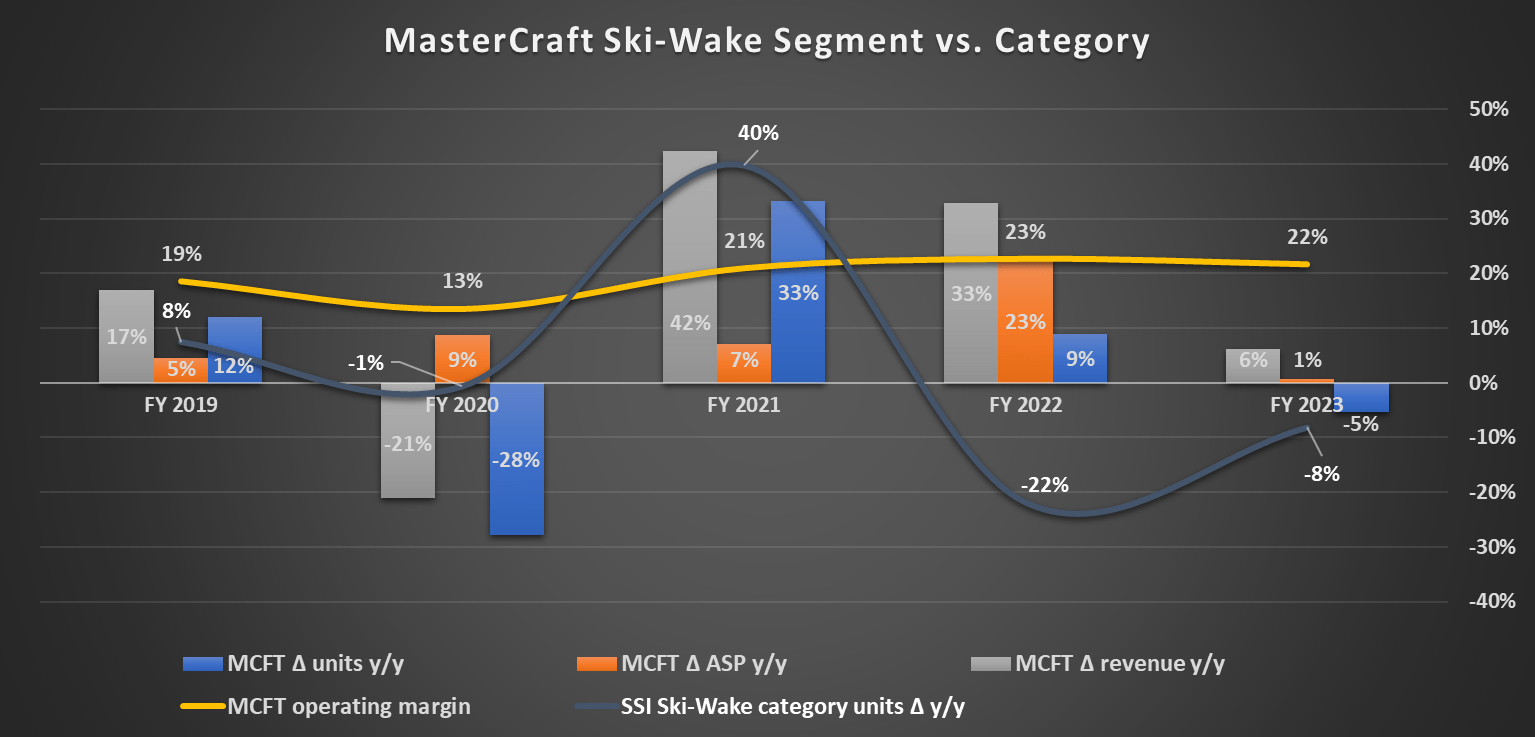

MasterCraft and Industry Cyclicality

The chart below is not a perfect comparison, as it compares wholesale to (estimated) retail, but still a useful one. As you all know, the surge in demand during the pandemic coincided with disrupted supply chains, which caused retail to exceed wholesale in 2020 and 2021.

Author's calculations, company disclosures, SSI data

{kind=link}

Nevertheless, this chart demonstrates that MasterCraft—particularly its ski-wake division—has a highly variable, low fixed-cost structure, combined with laudable operational execution from its management team.

Results were remarkably impressive in F2020 when facilities were closed for 6-8 weeks . Revenue and unit volume contracted by 21% and 28%, yet the division still generated a healthy operating profit. This should give investors confidence in MasterCraft’s ability to navigate economic downturns.

On this note, Malibu’s CEO remarked , “In a 30% down market, we can still be above 15% [EBITDA] margins. We can still be very profitable even in a prolonged downturn.”

Crest’s units sold fell 10% in F2023, but its operating margin was flat y/y at 14.2%.

Ski-Wake Market Position

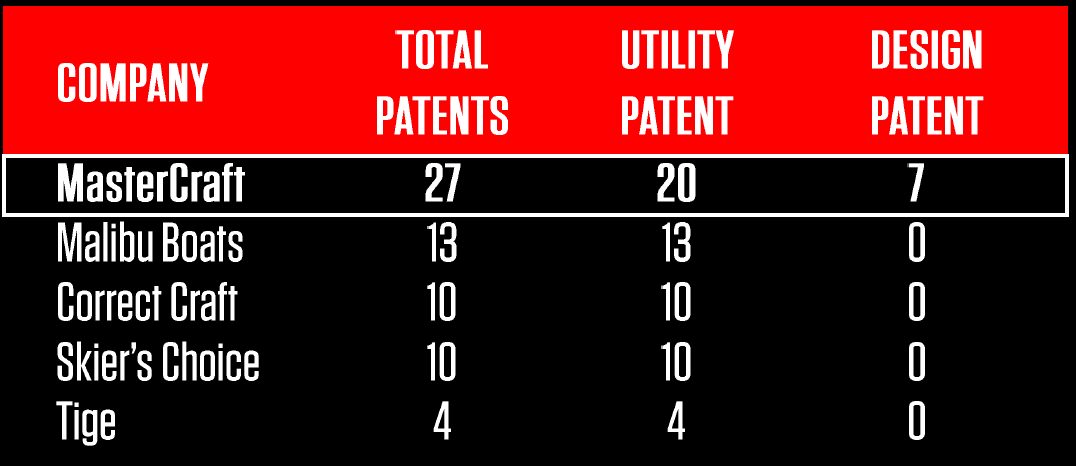

You cannot measure the economic value of a company’s intellectual property by patent count alone, but it is generally a helpful measure. Between 2014 and 2019, MasterCraft was awarded more patents than the next two competitors combined.

MasterCraft Investor Day, September 2019

{kind=link}

Between 2019 and 2023, the number of patents awarded grew from 35 to more than 50 — which also coincided with a doubling of their engineering and product development team to 60 from 29.

That said, I am not claiming that MasterCraft has more valuable IP than Malibu or any other competitor. My point is that innovation is deeply embedded in the company’s culture. And that it will continue, I believe, is a safe assumption.

MasterCraft Vs. Malibu

I spent a lot of time comparing the two brands, trying to gain an informational edge as to which is more likely to gain share over the other over the long term. My first draft of this article had over 1,000 words, breaking down the similarities and differences between them by factors most influential in the purchasing decision.

What I came to realize, however, was that this endeavor was folly. Even if there were a “right answer” as to which had the greatest value proposition, this would not necessarily translate into market share gains, as this would assume perfectly rational purchasing behavior. But we know that such decisions are driven by emotion more than reason.

Generalizing about whether one brand does something better than the other is a contentious issue, as I discovered when speaking to dealers and owners. It was rare for one to concede that the other was doing something better, but there were recurring themes for which they would praise the other brand.

Historically, MasterCraft has dominated the 22-foot category with its X22 . Likewise, Malibu has dominated the 23-foot category with its 23LSV , the best-selling wake boat ever. Rather than one being objectively or ostensibly superior, however, the purchasing decision often hinges on personal preferences and practical decisions like the size of one’s boathouse.

MasterCraft's base models tend to be more expensive, but they also include some features that are optional upgrades on Malibu’s. When adjusted for options, the two are priced very competitively. Over the years, the trend has generally been that when one company introduces an impressive new feature, the other finds a way to close the gap, such that differences between them are marginal in any given year.

For example, Malibu introduced stern thruster controls to its throttle in 2021, with two buttons to spin the boat in either direction. MasterCraft followed suit by adding a rotating knob to its throttle. Likewise, MasterCraft had a distinct advantage with its patented transom seats , which is less significant now with Malibu's recently updated seats. There are plenty of walkthrough videos from the companies and their dealers, which I encourage you to check out.

Operations and Financials: MasterCraft Vs. Peers

For this analysis, I’ll compare MasterCraft against its two most directly listed peers, Malibu and Marine Products (MPX). Before any comparisons are made, I should state that I think both are great companies; I simply believe that the discount at which MasterCraft trades is unjustifiable, particularly in reference to the latter.

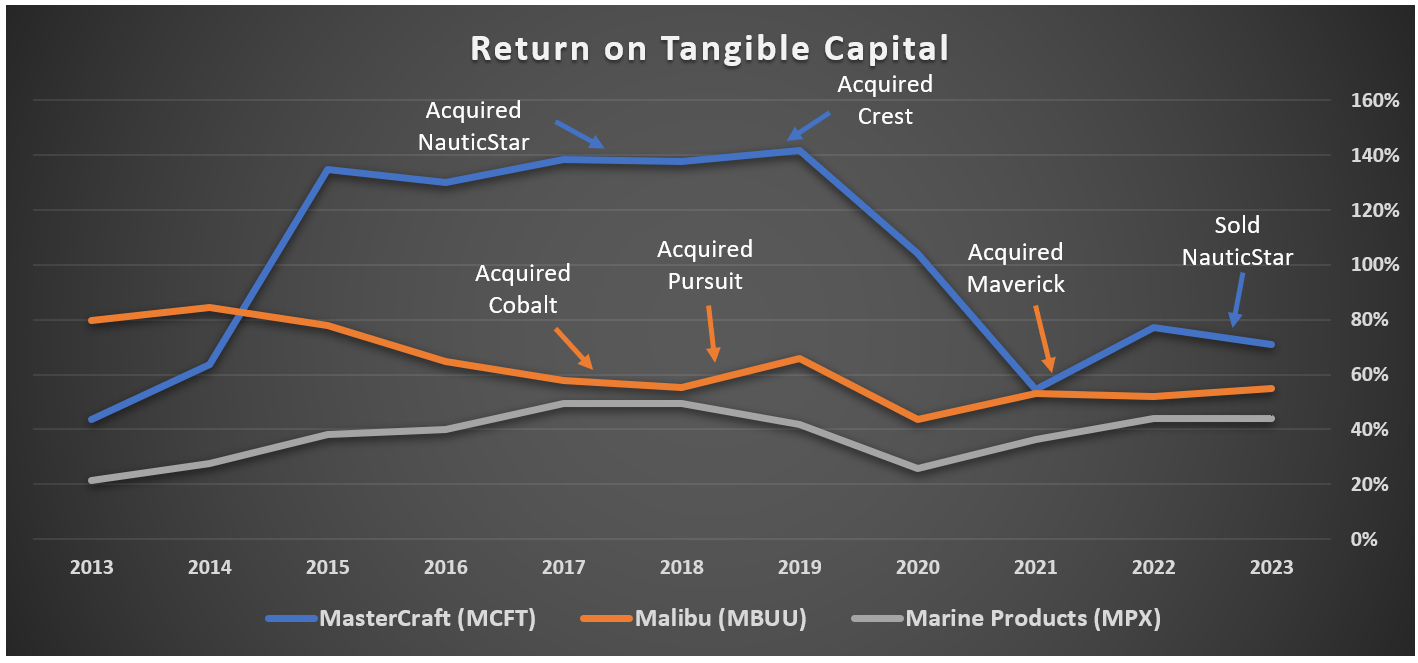

Let’s begin by comparing the three companies using the return on tangible capital ((ROTC)) metric. I believe this is the most useful financial metric, as it measures the profits a business generates from operations relative to the capital required to produce those profits.

I use operating earnings in the numerator as a proxy for “return,” as it simplifies comparisons by excluding differences in capital structure and tax rates (driven by international revenue). That said, the three are very similar in both respects. I’ve adjusted operating earnings for non-recurring expenses and amortization, which I don’t view as an actual economic expense for these companies. I have not excluded share-based compensation.

Tangible capital is calculated as net working capital plus net fixed assets. Given how the industry landscape was shifting in the spring, I’ve adjusted working capital to reflect my estimate of each company’s average requirements for 2023. The most significant adjustment was for MasterCraft, which had the largest cash surplus measured by short-term investments and interest income.

Finally, it must be noted that the chart below is not a perfect comparison, as Marine Products' fiscal year does not align with the other two companies. As Marine Products is a less direct comparison to MasterCraft, I have only adjusted its fiscal year from 2019 through 2023.

Author's calculations, company disclosures

{kind=link}

On the M&A front, it’s worth mentioning for those unfamiliar that Crest’s results have improved considerably on virtually every metric since it was acquired, as is the case with Malibu’s acquisitions. NauticStar, on the other hand, suffered operating losses for several years before it was sold.

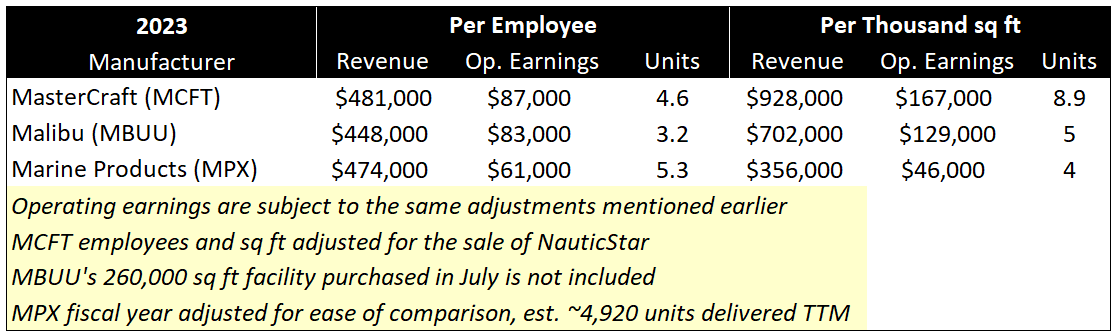

Unhindered by NauticStar’s losses, Crest’s early inefficiencies, and Aviara’s startup costs, the above chart conveys that MasterCraft has tremendous economic goodwill, capital efficiency, operating efficiency, or some combination. The table below, I believe, suggests that it is the latter.

Author's calculations, company disclosures

{kind=link}

It’s worth noting that MasterCraft reduced its workforce by about 300 across its MasterCraft and Crest facilities, first reported on June 30, 2023. Thus, I have used their employee count from 2022 for the above calculations. To produce comparable unit volumes in the future will require increasing its workforce by a similar amount, as the manufacturing process does not lend itself well to automation. In contrast, Malibu’s workforce increased slightly y/y from 3,015 to 3,095.

However, we cannot ignore that 2023 was a strong year, and 2024 will be comparatively soft. At the mid-point, my math suggests that operating earnings will fall to $35,000 and $53,000 per employee for MasterCraft and Malibu, or $52,000 and $74,000 per thousand sq ft. Operating leverage works in both directions.

Valuation

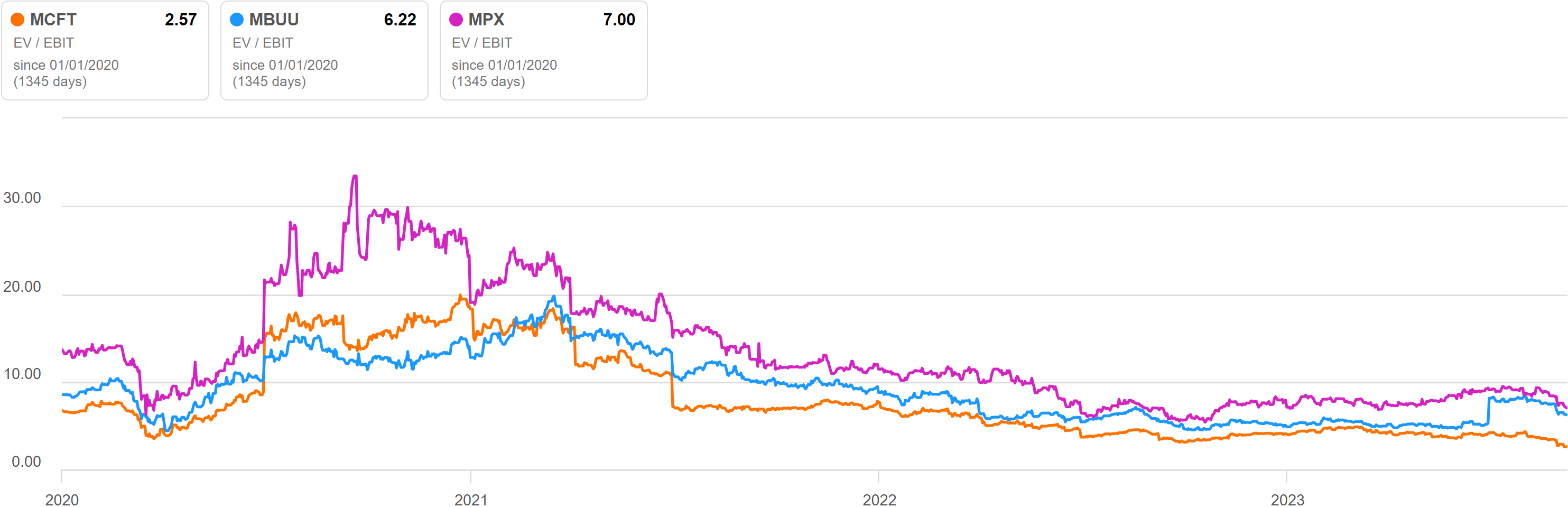

Despite its spectacular financial and operating performance over the long term, MasterCraft's valuation almost invariably falls short of the others, sometimes by a lot. However, the gap isn't as wide as the chart currently suggests, as Malibu's EBIT is not adjusted for the $100m liability settlement (3.7x modified)

{kind=link}

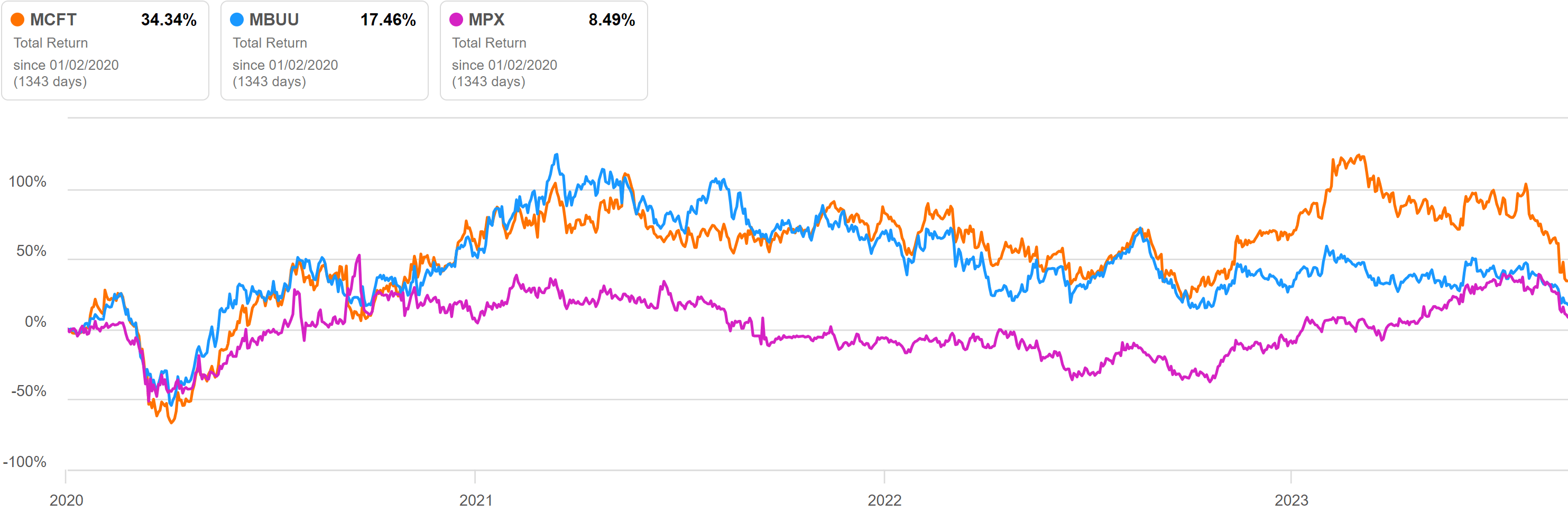

Despite the discount and being down nearly twice as much from its 52-week high, MasterCraft still outperformed.

{kind=link}

So, why the discount? MasterCraft’s ski-wake revenue concentration (~70%) is the primary reason. Malibu, in contrast, has greater portfolio diversification ( ~50% ski-wake ). Likewise, Marine Products’ lineup is targeted toward recreational and coastal fishing categories, which are expected to be less economically sensitive than the ski-wake category. Moreover, it pays a sizable and well-covered dividend (48% 2Y average payout ratio). However, if it isn't cut, I’d expect that to climb closer to the 2019/20 average of 70% over the next 12-24 months.

The above differences are captured in MasterCraft’s beta of 1.8 (5Y monthly), compared to 1.6 and 1.2 for Malibu and Marine Products. However, as indicated below, these differences might not be as substantial as valuations suggest.

Author's calculations, company disclosures

{kind=link}

Marine Products closed its facilities for five weeks in 2020 , compared to the 6-8 weeks mentioned earlier for MasterCraft. Granted, the purchasing activity in 2020 was not representative of the patterns likely to transpire during future downturns. But I hope this illustrates that Marine Products might not be as well insulated as implied by its valuation.

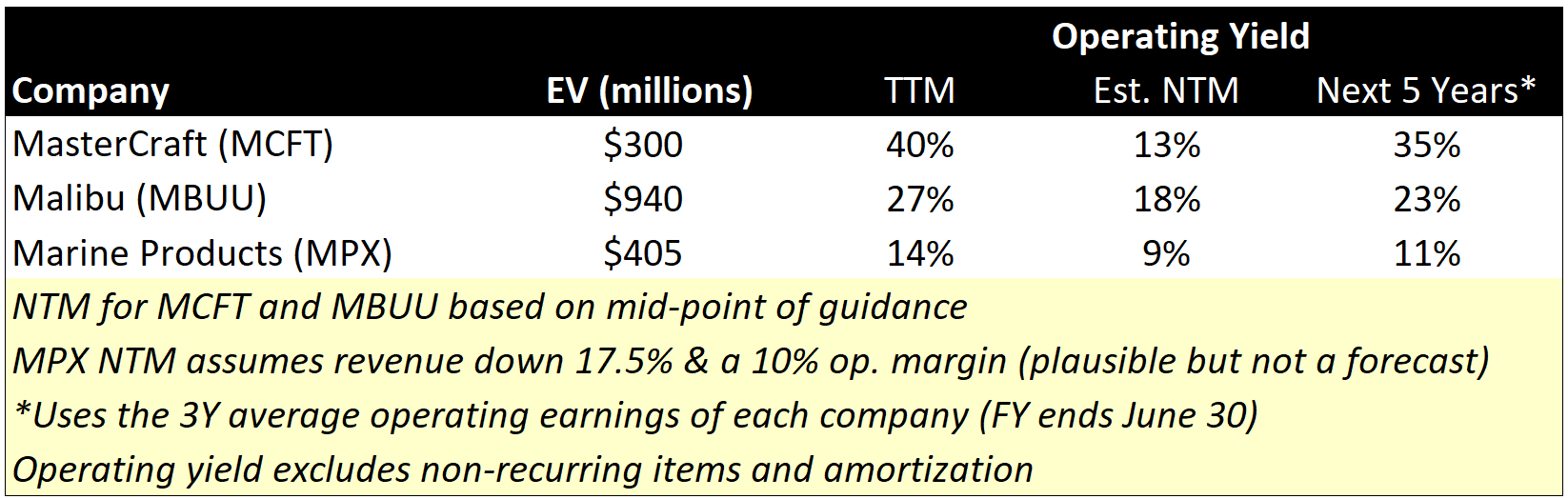

Warren Buffett encourages a thought exercise for investors, which is to think of a stock as a bond. “Warren views the earnings yield of a stock the same as he would a bond's yield.” He refers to this as an “equity bond.” With an equity bond, you know the price, but you don’t know what the coupons will be, and it’s your job to figure it out.

Author's calculations, company disclosures

{kind=link}

Although MasterCraft is likely to be the worst affected in 2024, the price of its equity bond more than reflects that. Even if its average coupons fall below the 3Y average by 25%, the 5Y yield would still be an impressive 27%. With a 13% NTM yield, this would require ~$90m on average in the subsequent four years. In contrast, its coupons were $119.3 and $118.9 in 2022 and 2023.

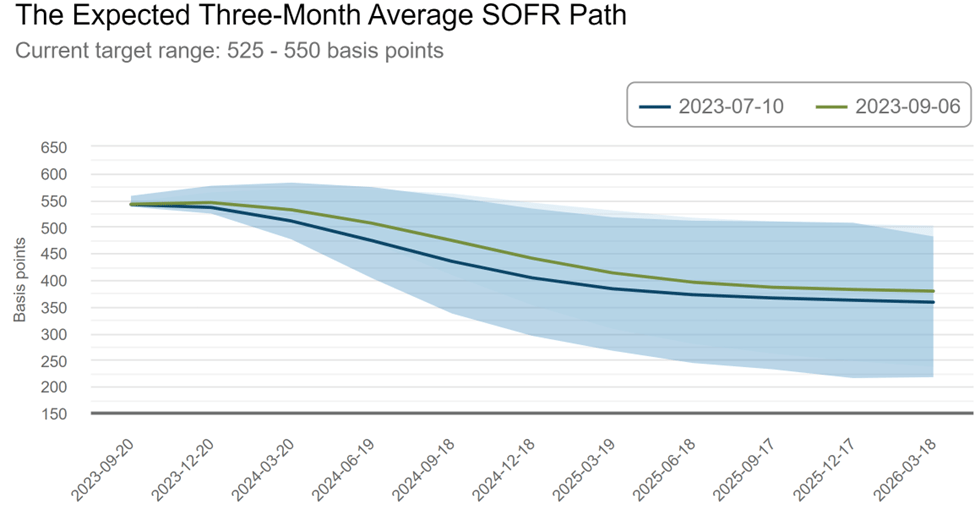

Although the market expects rates to remain higher for longer than just a few months ago, if they approximate the current forecasted path, MasterCraft has a good shot at achieving this.

{kind=link}

On the other hand, it is incredibly difficult to envision a scenario in which Marine Products' equity bond generates a 27% yield over the next five years—particularly with its current payout ratio—which would demand unprecedented returns on retained earnings. This would require an average coupon of $109m, compared to the 3Y average of $46m. However, that Malibu’s equity bond would generate that yield is very conceivable.

It would seem then that Marine Products is priced for a magnificent future, and MasterCraft is priced for the antithesis. This scenario strikes me as highly implausible. I'm not claiming that Marine Products is overvalued on an absolute basis, but it is difficult to conclude that it isn't overvalued on a relative basis. MasterCraft, however, strikes me as patently undervalued on an absolute and relative basis.

Downside Protection

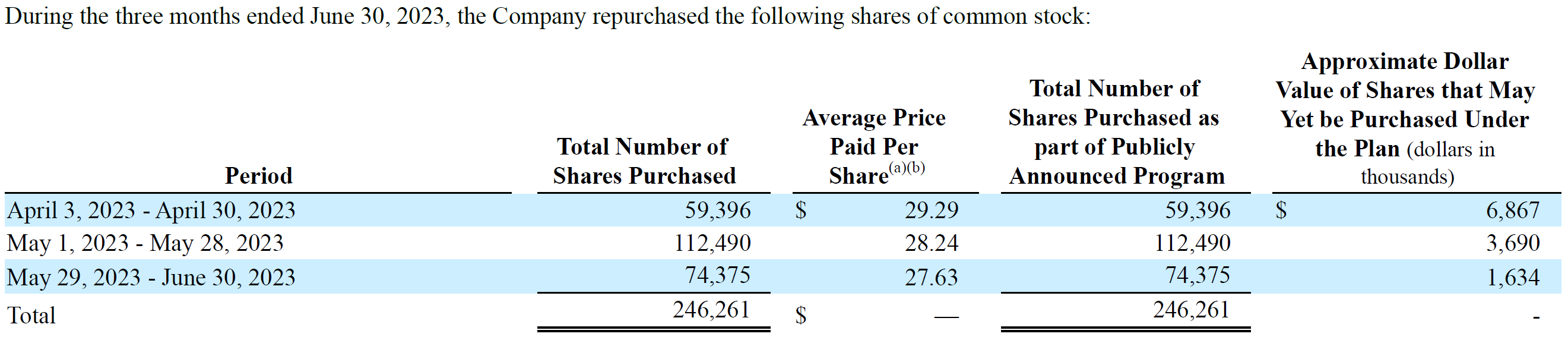

Adding downside support to MasterCraft’s equity bond price is that the board of directors authorized a new repurchase program on July 24, 2023, under which the company can repurchase up to $50m of its outstanding shares. This becomes effective upon expiry of the existing repurchase program, which had $1.6m remaining as of June 30, 2023.

{kind=link}

That the company was repurchasing shares in the high 20s in the spring and has a record cash surplus suggests that it will be buying as many shares in the low 20s as it pragmatically can.

As far as I can tell, using the entirety of the plan would add more value to existing shareholders than any acquisition could, as the latter would require a company to sell itself for much less than its worth, which doesn’t occur very often.

Risks

- Interest rates remain higher than what is priced-in (Fed Funds aren’t expected to return to the F2023 average of ~3.84% until the first half of 2025 )

- A prolonged and severe economic downturn

- Significant market share loss

- Sterndrives capture a sizable percentage of entry-level ski-wake customers

Conclusion

If you like the company’s prospects long-term, as I do, you can (1) buy now knowing that a better entry may arise, (2) wait for a better entry that may not arise, or (3) wait for a clear signal that things are getting better before buying.

On the surface, the latter option is the most appealing. But it isn't an option at all, not if you wish to capture most of the upside. When there are clear signs that tomorrow will be better than today, the improvement in outlook is already reflected in the price. This will not be lost on most of you, but reminders of this kind often help us make wise investment decisions.

For further details see:

MasterCraft: A Tale Of Cyclical Headwinds And Secular Tailwinds