MCFT - MasterCraft Boat: Acquisitions Creating Diversified Growth

2023-05-01 10:56:30 ET

Summary

- MasterCraft has been able to outperform the broader market in recent years displaying its ability to grow and succeed.

- I believe MasterCraft's targeted acquisitions will expand its customer base and increase its product offerings, creating future success.

- Based on my DCF assumptions, I believe that MasterCraft Boat is undervalued resulting in a buy rating.

MasterCraft ( MCFT ) has exemplified strong and consistent growth throughout the past few years. With strong integration of acquisitions and its current undervaluation, I rate this stock a buy due to its long-term growth potential.

Business Overview

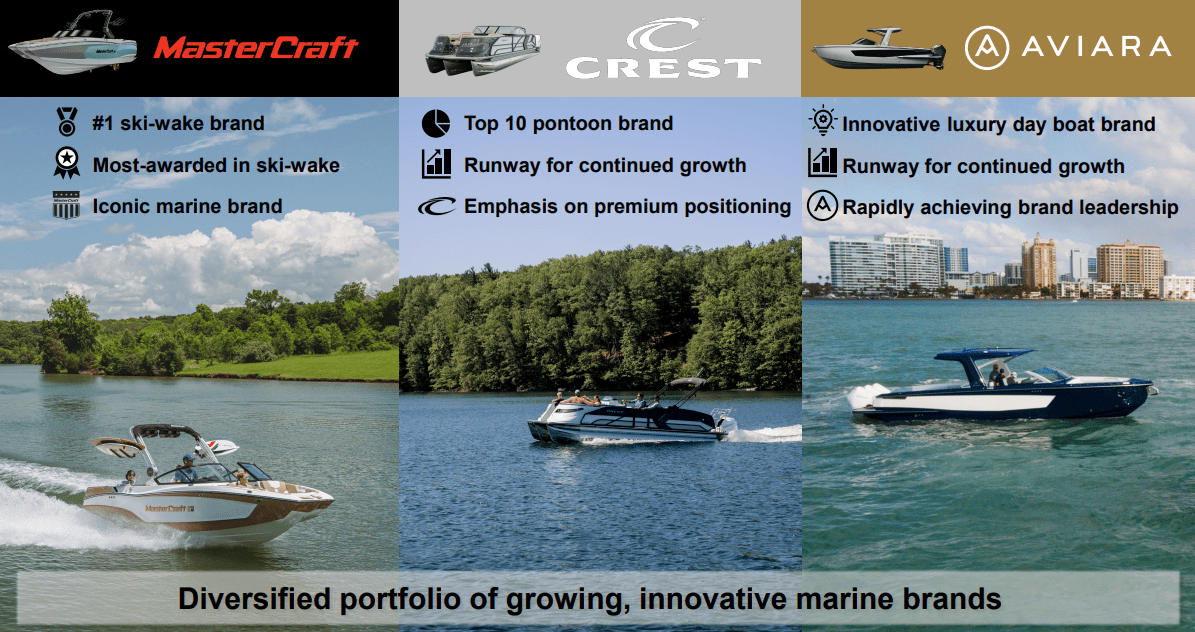

MasterCraft Boat Holdings, Inc. is a leading manufacturer of premium-performance sport boats. The company designs, manufactures, and markets boats that are known for their high quality, performance, and innovation. MasterCraft offers a wide range of boats, including towboats, pontoons, and luxury day boats, that cater to the needs of boating enthusiasts of all types.

The company has a strong track record of innovation and has been recognized for its industry-leading designs and technology. MasterCraft's boats are built with premium materials and feature advanced engineering and design features that provide superior performance and handling on the water.

MasterCraft has a strong presence in the North American boating market, with a network of dealerships and distributors across the United States and Canada. The company is also expanding its reach in international markets, including Europe, Asia, and Australia.

In addition to its core boat manufacturing business, MasterCraft also offers a range of aftermarket products and accessories, including audio systems, towers, covers, and other boating accessories. The company is committed to providing its customers with a superior boating experience and offers a range of services, including financing, warranties, and customer support.

{kind=link}

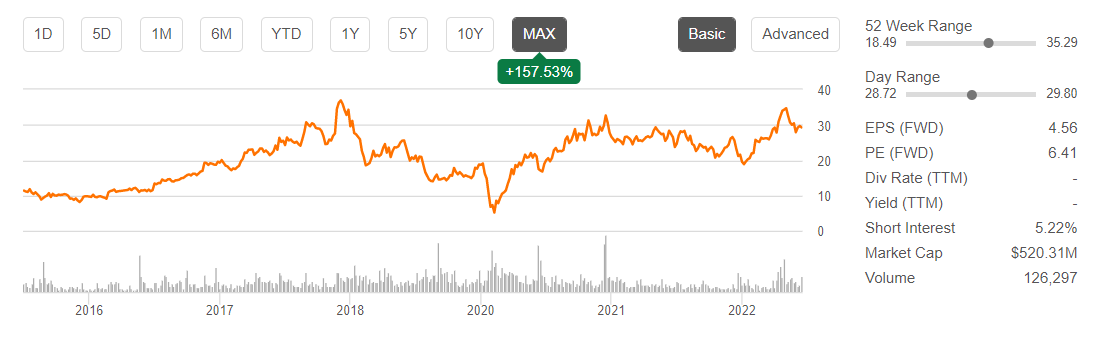

MasterCraft is currently priced at $29.27, with a market capitalization of $520.312 million, an impressive ROIC of 39%, and a 6.41 P/E ratio. While its stock price is lower than its 52-week high of $35.29, it presents potential value for a long-term investment in my view.

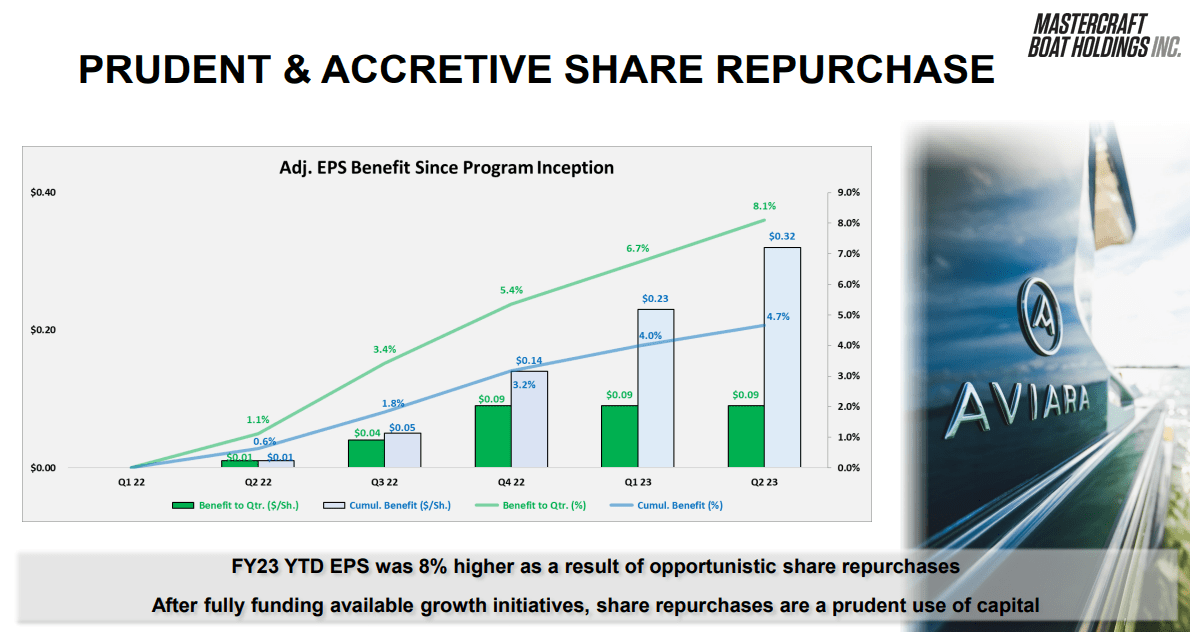

MasterCraft has also committed to repurchasing shares over the upcoming years which I remain positive about as I believe that the company is currently undervalued, thus this action should create shareholder wealth.

Seeking Alpha Investor Presentation

{kind=link}

{kind=link}

MasterCraft reported strong financial results for the second quarter of fiscal 2023, with sales of $159.2 million, a 10.2% increase from the prior-year quarter which marks the highest net sales, diluted adjusted earnings per share and adjusted EBITDA that MasterCraft has ever posted for a second quarter. Record net income from continuing operations was $20.1 million, or $1.12 per diluted share, up 11.9% and 19.1%, respectively, from the prior-year period. Diluted adjusted net income per share was $1.20, up 18.8% from the previous year. However, the gross profit margin decreased 120 basis points to 24%, compared to 25.2% in the second quarter of 2022, mainly due to inflation, changes in the model mix, higher dealer incentives, and increased warranty costs.

I believe the robust growth in boat purchases is likely to decrease in the short term but stabilize and grow over the long term, as the surge in demand that began during the Covid pandemic has created a whole new customer base. This increase in demand has been driven, in part, by the retirement boom that occurred at the onset of the pandemic. MasterCraft has been able to take advantage of this trend by targeting first-time buyers, retaining existing customers, and expanding its supplementary product offerings generating stable annual cash flows.

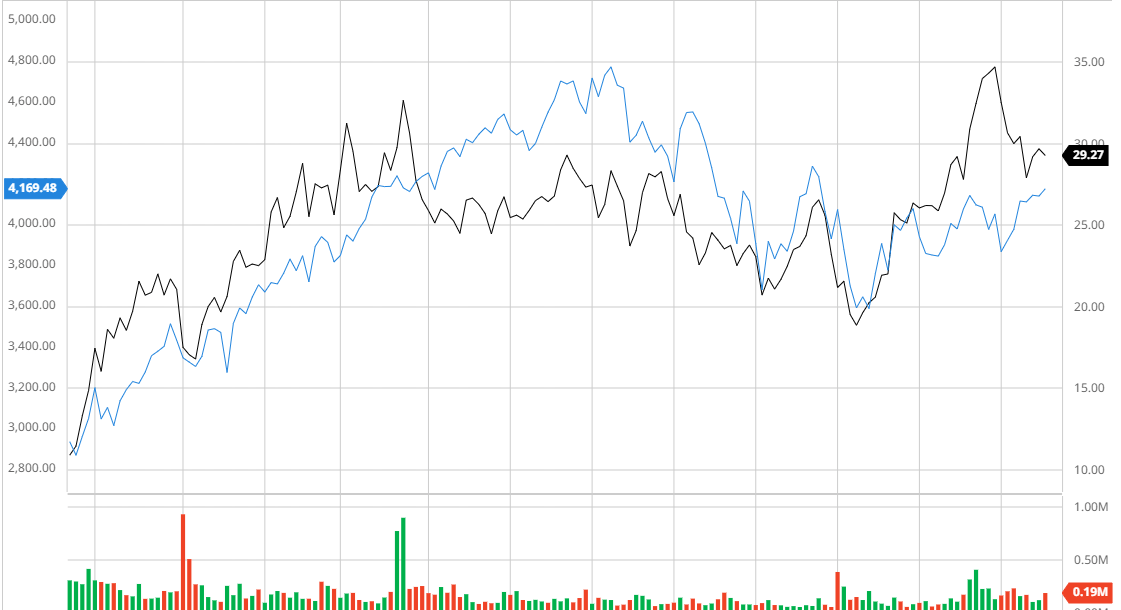

Outperforming the Broader Market

Over the past three years, MasterCraft has demonstrated its ability to innovate its core business model to expand its customer base and create support through acquisitions and new product lines, outperforming the broader market in the process.

MasterCraft Compared to the S&P 500 (Created by author using Bar Charts)

{kind=link}

MasterCraft's Targeted Acquisitions to Expand Customer Base and Product Offerings

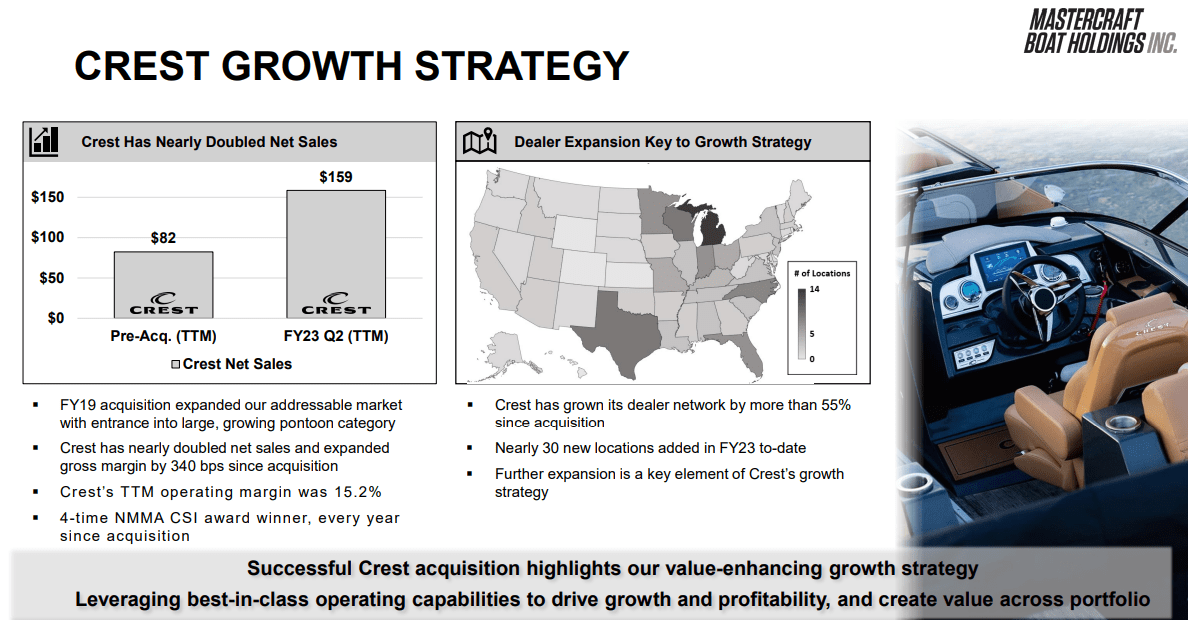

MasterCraft's adeptness at integrating new acquisitions and innovations into its core business model has enabled the company to achieve scale while driving its FCF forward. This increase in FCF has given the company the freedom to invest in new avenues and leverage technological advancements to its advantage. One of its successful acquisitions that highlights the expansion of its customer base is Crest Marine, a leading producer of innovative, high-quality pontoon boats ranging from 20 to 29 feet. Since the acquisition in October 2018 for $80 million, Crest has nearly doubled its net sales, and its gross margin has expanded by 340 bps. MasterCraft has also leveraged its extensive dealer network to benefit Crest, which has seen a 55% increase in its dealer network since the acquisition. This remarkable growth from Crest, along with its future prospects, is a testament to MasterCraft's ability to acquire companies with tremendous potential and integrate them into its core business, thus adding new products to its portfolio with profitable recurring cash flow.

{kind=link}

Analyst Consensus

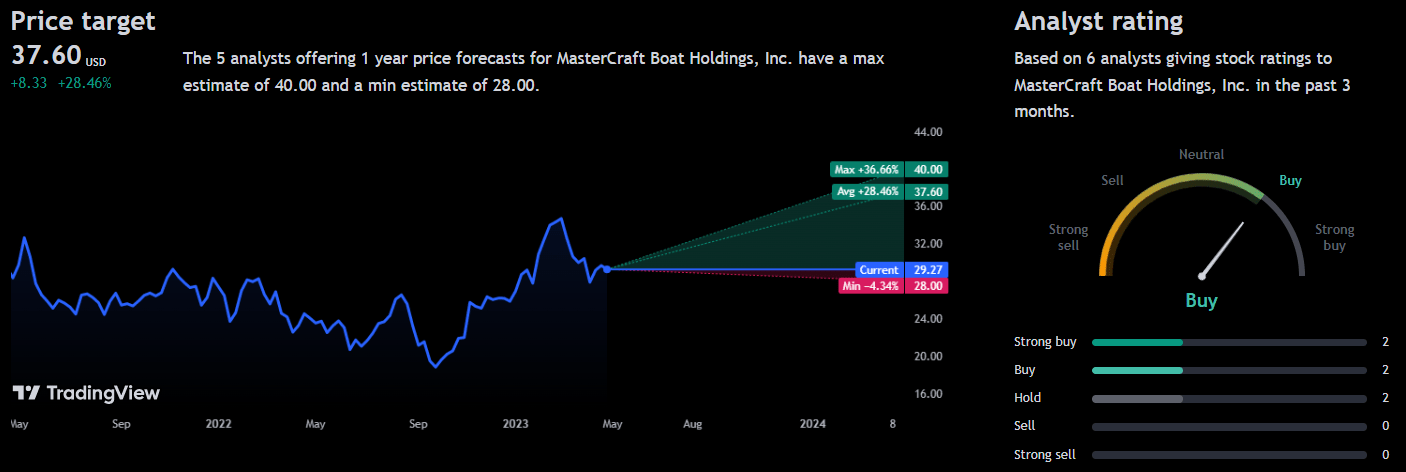

Analyst consensus rates MasterCraft as a "buy", recognizing MasterCraft's growth potential organically and through acquisitions. With an average 1Y price of $37.60, there is a potential upside of 28.46%.

{kind=link}

Valuation

Before creating my assumptions and calculating my DCF, I will calculate the Cost of Equity and WACC for MasterCraft using the Capital Asset Pricing Model. Factoring in a risk-free rate of 3.43%, I was able to conclude that the Cost of Equity was 7.45% as displayed below.

Created by author using Alpha Spread

Assuming this Cost of Equity value, I was able to calculate the WACC to be 6.87% as shown below, which is under the industry average of 7.98%.

Created by author using Alpha Spread

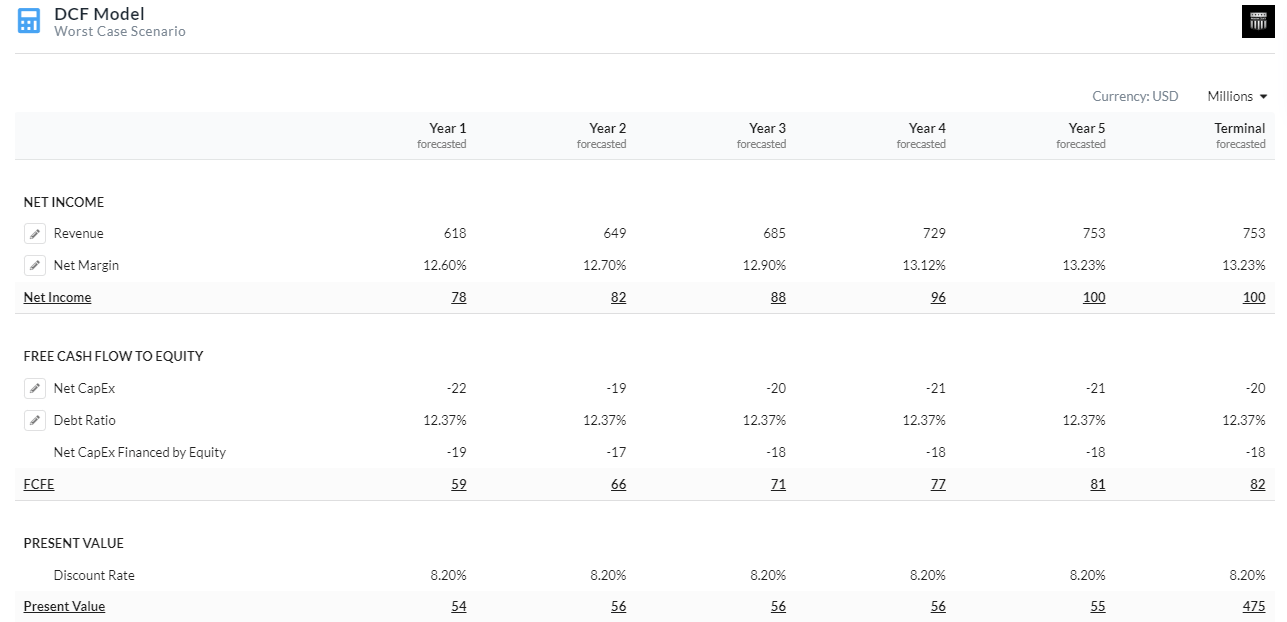

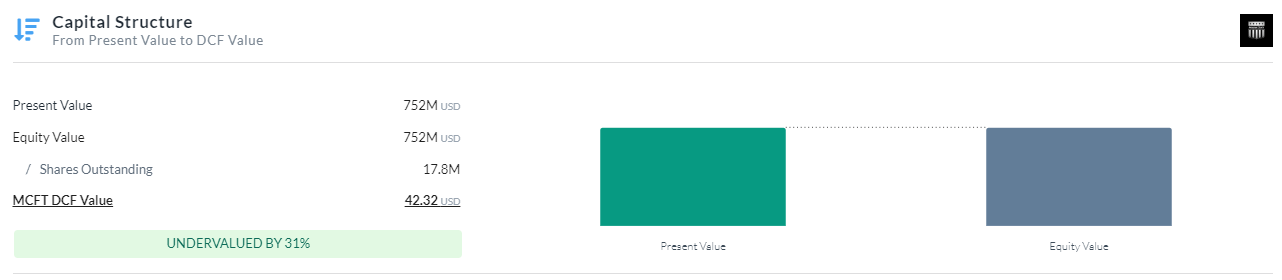

After performing an Equity Model DCF analysis utilizing FCFE, it has been determined that MasterCraft is currently undervalued by 31% with a fair value of approximately $42.32. The analysis was conducted using a discount rate of 8.2% for a 5-year duration. To account for potential macroeconomic headwinds that could impact discretionary spending on leisure boats, a 1.33% risk premium was added. The analysis also assumed a mid-single-digit revenue growth rate beyond 2023, in line with pre-pandemic growth rates for MasterCraft. It is predicted that the company will continue to pursue innovative technologies and acquire more efficient assets, resulting in an increased operating margin over time. The DCF analysis provides a clear indication that MasterCraft is currently undervalued and has significant potential for future growth.

DCF 5Y Assumptions (Created by author using Alpha Spread) MasterCraft Capital Structure (Created by author using Alpha Spread)

{kind=link}

{kind=link}

Risks

Rivalry: The leisure boating industry is seeing swift technological advancements, which could lead to other brands seizing MasterCraft's market share, resulting in a decline in customers. This is mainly due to new boat designs gaining popularity, new GPS and safety systems being introduced, and the potential arrival of electric/hybrid boats in the near future.

Failure to Integrate Acquisitions: Because of the recent nature of MasterCraft's strategic acquisitions, it is uncertain whether the company can smoothly integrate these new segments, which may lead to stagnant growth and potential issues with free cash flow.

Macroeconomic Headwinds: Poor macroeconomic headwinds will hurt MasterCraft boats as it is a discretionary purchase. In times of economic uncertainty, consumers may be more cautious with their spending, opting to hold off on big-ticket items like boats. Additionally, if the cost of raw materials or other inputs increases due to inflation or supply chain disruptions, this could also impact the profitability of MasterCraft's business. This will hurt MasterCraft's overall ability to acquire new companies and stagnate its expansion into new markets.

Conclusion

In summary, I believe MasterCraft is a buy based on its impressive track record of integrating and expanding through acquisitions, coupled with its undervaluation. The company's diversified range of high-quality products and strong ROIC make it an attractive investment for those seeking long-term growth.

For further details see:

MasterCraft Boat: Acquisitions Creating Diversified Growth