MCFT - MasterCraft Boat Holdings: Likely To Continue To Sink With The Economy

2023-10-25 15:45:26 ET

Summary

- MasterCraft Boat Holdings, Inc., a manufacturer of recreational power boats, is currently trading at 52-week lows.

- Despite a rock-solid balance sheet, reasonable valuations, and recent buying by a beneficial owner, the stock faces additional, potential downside due to cyclical headwinds.

- A full investment analysis on MasterCraft Boat Holdings follows in the paragraphs below.

To reach a port we must set sail - Sail, not tie at anchor. Sail, not drift ."? Franklin D. Roosevelt.

Today, we look at a manufacturer whose stock is trading right at 52-week lows. The shares appear cheap on several metrics, but the company serves a cyclical industry. This manufacturing concern does have a rock-solid balance sheet and recent buying by a beneficial owner. Signs the stock is ready to rebound or further downside ahead? An analysis follows below.

{kind=link}

Company Overview:

MasterCraft Boat Holdings, Inc. ( MCFT ) is a Vonore, Tennessee-based manufacturer of recreational power boats, featuring three brands across three market segments. Specifically, through its MasterCraft, Crest, and Aviara marques, it is a leading maker of ski/wake boats, with a meaningful share of the pontoon and day boat markets. MasterCraft was founded in 1968 and went public in 2015, raising net proceeds of $82.1 million at $15 per share. The stock trades around $21.50 a share, translating to an approximate market capitalization of $370 million.

The company operates on a fiscal year ((FY)) ending June 30th. For the avoidance of doubt, FY23 refers to the twelve-month period ending June 30, 2023.

Segments

Management views its operations through its three brands: MasterCraft; Crest; and Aviara.

MasterCraft consists of 16 models of recreational sports craft typically used for water skiing and wake surfing, which are manufactured at the company's headquarters in Tennessee. Retail prices across the segment's portfolio range from ~$100,000 to $320,000. As the flagship brand, its boats have been offered since the company's inception and are well-known and well-regarded amongst powerboat enthusiasts. According to Statistical Surveys, the MasterCraft brand commanded a 20.8% of the domestic ski/wake category in calendar 2022, representing the number one market position. They are sold through 108 dealers across 158 locations in North America, as well as through 43 dealers internationally.

The segment generated FY23 operating income of $101.3 million on net sales of $468.7 million, reflecting the sale of 3,407 units at an average price of ~$138,000. The top line represented 71% of the company's total and a 0.6% increase over FY22.

Crest is MasterCraft's four lines of pontoon boats ranging from 20 to 27 feet in length and $35,000 to $220,000 in price, manufactured out of a facility in Owosso, Michigan. They are sold through 148 dealers in 185 locations in North America and two dealers internationally. The brand was founded in 1957 and acquired by MasterCraft in 2018. In calendar 2022, Crest held a 4.1% market share of the domestic aluminum pontoon category, ranking ninth. The segment accounted for FY23 operating income of $20.1 million on net sales of $141.2 million, reflecting sales of 2,836 units at an average price of ~$50,000. The top line represented 21% of FY23 total net sales and a 0.3% improvement over FY22.

Aviara is the company's four models of luxury recreational day boats, ranging from 28ft (starting in FY24) to 40ft in length and approximately $200,000 to $1.3 million in price. The European-style bowrider crafts were launched in-house in 2019. They are manufactured out of a plant in Meritt Island, Florida, and sold through one dealer with 57 locations in North America. Aviara commands a 6.3% share of the domestic 30-foot to 43-foot bowrider market, ranking it number seven. The segment produced an FY23 operating loss of $4.5 million on net sales of $52.1 million, representing sales of 134 units at an average price of ~$389,000. MasterCraft's newest segment was responsible for 8% of FY23's total net sales and a 50.2% increase over FY22.

MasterCraft's portfolio held a fourth brand, saltwater and deck boat unit NauticStar, which it exited in September 2022.

Although the MasterCraft and Crest brands have international dealers, the preponderance (95%) of the company's net sales is derived from North America. Revenue is recognized when boats are sold into dealers with ~40% to 50% of net sales occurring in FY4Q.

Recent Operating History and Stock Price Performance

The company's operating performance has largely been a function of the artificial economy since the advent of the pandemic. Using an apples-to-apples comparison of continuing operations, in FY19 (ending June 30, 2019), MasterCraft earned $2.61 a share (non-GAAP) and Adj. EBITDA of $73.4 million on net sales of $388.3 million. The pandemic significantly impacted FY20, with non-GAAP earnings falling to $1.43 a share and Adj. EBITDA dropped to $26.5 million on net sales of $308.1 million, representing a 20% decline at the top line.

Then, with the subsequent monetary and fiscal responses to the pandemic, MasterCraft benefitted immensely as lower borrowing rates combined with the work-from-home paradigm engendered significant demand for its boats. In FY21, a period still affected by lockdowns, net sales rebounded well above FY19 levels to $466.0 million. With Americans free to cheaply enjoy the outdoors in FY22, net sales soared 38% to a record $641.6 million while non-GAAP earnings ($5.01 a share) and Adj. EBITDA ($130.5 million) also reached all-time highs. Strong demand and supply chain issues conspired to bolster pricing and keep dealer inventory low.

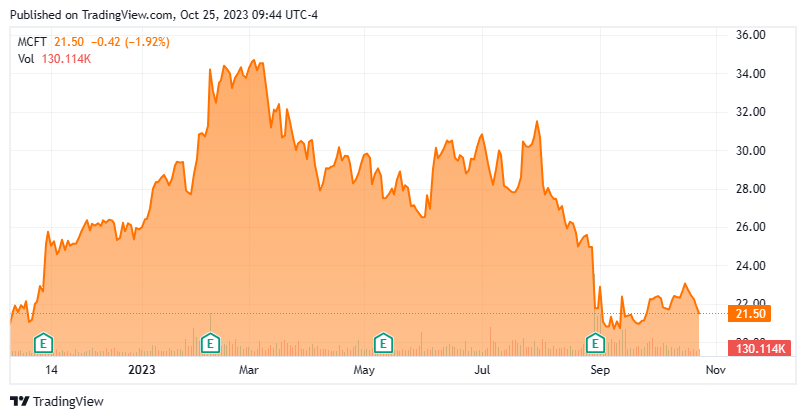

During this goldilocks period, the stock rebounded sharply off its pandemic-selloff low of $4.90 a share, ultimately reaching a four-and-a-half-year high of $35.39 in March 2023 - still below its all-time high of $39.50 a share set in 2018.

Q4 FY23 Financials and FY24 Outlook

However, higher borrowing costs stalled the momentum as FY23 progressed, which, owing to the restocking of its dealers' inventories, looked like FY22 on some financial metrics. Non-GAAP earnings were up 7% to $5.35 a share, while Adj. EBITDA increased 1% to $131.5 million and net sales rose 3% to $662.0 million. However, the extent of the momentum loss was revealed in MasterCraft's 4QFY23 financials, reported on August 30, 2023. The company posted 4QFY23 earnings of $1.37 a share (non-GAAP) and Adj. EBITDA of $32.7 million on net sales of $166.6 million versus $1.92 a share (non-GAAP) and Adj. EBITDA of $47.6 million on net sales of $197.2 million, representing declines of 29%, 31%, and 16%, respectively.

Even though these numbers were off significantly from the prior year period, the bottom line was $0.30 better than Street estimates while the top line amounted to a $4.5 million beat, somewhat indicative of the skepticism the market had placed on the company's ability to deliver strong results in a high interest rate environment.

August Company Presentation

Either way, with wholesale unit sales significantly exceeding retail unit sales in FY23, the company's dealer inventories ramped from meaningfully understocked to slightly overstocked, removing an in-built tailwind the company enjoyed as it entered FY23. As such, MasterCraft's FY24 outlook, which reflected this dynamic, was abysmal versus expectations.

Citing cyclical headwinds (higher borrowing costs and lending standards) eating into consumer demand, management guided to earnings of $1.67 a share (non-GAAP) and Adj. EBITDA of $47 million on net sales of $405 million (based on range midpoints) against Street expectations of $3.83 a share (non-GAAP) and Adj. EBITDA of $102 million on net sales of $569 million. Already down 29% from their 52-week high entering the report, shares of MCFT fell 13% in the subsequent trading session, closing at $21.76. The stock remains stuck near these trading levels since then.

August Company Presentation

Balance Sheet & Analyst Commentary:

The good news for MasterCraft is that its balance sheet is in excellent shape after generating record cash from operation activities of $136.8 million, providing it capital allocation flexibility while it weathers the challenging macro environment. As of June 30, 2023, it held cash and securities of $111.4 million versus debt of $53.7 million with access to an additional $100 million of liquidity. Some of that cash looks earmarked for share buybacks after the company announced in July 2023 that its board had approved a new $50 million stock repurchase program, adding to the $1.6 million remaining on its prior $50 million authorization. MasterCraft does not pay a dividend.

August Company Presentation

The pessimistic outlook prompted one downgrade (B. Riley) and six reduced price targets, making four hold ratings against two buys and one outperform. Analysts' median twelve-month price objective fell from $38.50 to $24. On average, they are slightly more optimistic than MasterCraft's management, expecting the company to earn $1.80 a share (non-GAAP) on net sales of $411.8 million in FY24, followed by $2.54 a share (non-GAAP) on net sales of $465.8 million in FY25.

Beneficial owner Coliseum Capital Management used the 52-week lows as an opportunity to cost average, adding 279,437 shares at an average price of $21.68 on September 26th - 28th. It currently owns 12% of MasterCraft.

Verdict:

An investment decision regarding MasterCraft Boat Holdings, Inc. stock is largely a function of where one believes the U.S. economy is currently situated in the economic cycle. If a would-be investor believes the economy is currently at or near the bottom of the cycle - i.e., consumer borrowing costs have reached a high and borrowing availability has bottomed - then shares of MCFT represent reasonable value at a forward P/E of just under 12, a forward EV/FY24E Adj. EBITDA below 7 and a price-to-FY24E sales of .8.

However, the bet here is that the U.S. economy has another significant leg down that is currently not priced into the market (or MasterCraft stock). Furthermore, the historically low interest rate period post-pandemic pulled significant demand into FY21 and FY22 - the effects of which will be felt for many years thereafter. As such, this cyclical play - albeit a well-run business - is to be avoided.

It takes just one wave to capsize a boat, and one more to take it down ."? Federico Chini.

For further details see:

MasterCraft Boat Holdings: Likely To Continue To Sink With The Economy