MCFT - MasterCraft Boat: Quality Little Business Facing A Revenue Collapse

2023-11-10 23:37:45 ET

Summary

- MCFT’s revenue has grown at a CAGR of +15% during the last decade, while EBITDA has exceeded this at +25%.

- The company has a strong market position, owing to its brand and reputation of high-quality products, alongside its proximity to customers.

- MCFT’s recent performance has materially slowed, with evidence to suggest FY24 will be an extremely problematic year, with a double-digit decline in revenue and margin erosion likely.

- MCFT performs extremely well relative to its peers, although is expected to suffer more greatly from the current macroeconomic environment.

- MCFT appears overvalued on a NTM basis, which factors in the difficulties the company faces during FY24F.

Investment thesis

Our current investment thesis is:

- MCFT is a good business that has scope for long-term growth and attractive margins. This said, the company is highly cyclical and is unable to benefit from its key competitive advantages. The industry will decline substantially in the coming year, with very little that can offset this impact.

- This is illustrated in MCFT’s valuation, which appears cheap from an LTM perspective but is expensive on a NTM basis. We believe this stock should be avoided until there is greater visibility over the near-term performance of the company.

Company description

MasterCraft Boat Holdings, Inc. ( MCFT ) is a leading manufacturer of premium performance sport boats. Based in the United States, the company operates through its MasterCraft, NauticStar, and Crest brands. MasterCraft boats are renowned for their innovation, quality, and performance, catering to water sports enthusiasts and professionals alike.

Share price

MCFT’s share price has performed moderately, particularly if distributions are also included, returning just under 100% to shareholders. This development is a reflection of its strong financial development but an underlying hesitancy among investors about the long-term trajectory of the company.

Financial analysis

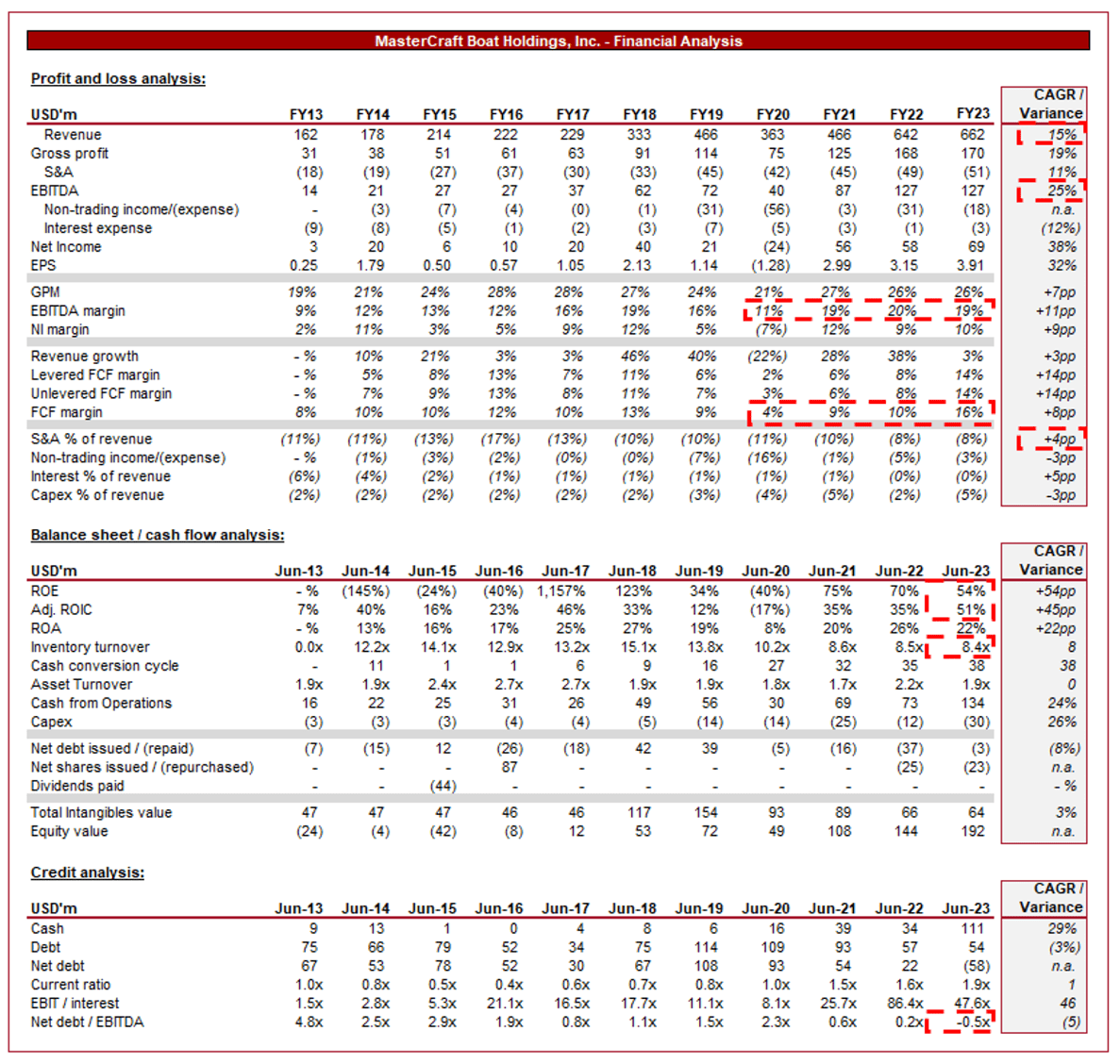

MasterCraft Boat financials (Capital IQ)

{kind=link}

Presented above are MCFT's financial results.

Revenue & Commercial Factors

MCFT’s revenue has grown impressively, with a CAGR of +15% in the last decade, while EBITDA has exceeded this at +25%. Revenue growth has been broadly consistent, with only a drawdown during the pandemic-hit year.

Business Model

MCFT specializes in premium, high-performance boats designed for wakeboarding, waterskiing, and other water sports. MCFT offers a diverse range of boat models, catering to different customer preferences, budgets, and needs. In addition to this, MCFT allows customers to customize their boats, from color schemes to basic and additional features. This level of personalization enhances customer satisfaction and the attractiveness of its product range, as buyers can tailor the boats to match their specific tastes and requirements.

It is focused on quality, innovation, and advanced technology, with the objective of differentiating itself from the wider market and attracting enthusiasts willing to invest in top-tier products.

Beyond its core offering of boats, the company also offers and prioritizes after-sales services, including warranty support, maintenance guidance, and customer support hotlines. A reliable after-sales experience enhances customer trust and loyalty, while reducing the friction associated with making such as purchase. This has been shown to encourage repeat business and a recurring revenue stream.

MCFT is known for its continuous innovation. It invests well in R&D, introducing cutting-edge features and designs in its boats. This commitment to innovation keeps its products attractive to consumers and ensures it can justify its premium brand and products.

One of the key benefits of the company is that it has a robust network of dealers and distributors. These partners play a vital role in marketing, sales, and after-sales services given the nature of the industry. This is an easily marketable service, let alone reaching consumers, and so global relationships through dealers and distributors are absolutely critical to easily reaching the end user.

MCFT maintains a strong online presence, utilizing social media, interactive websites, and mobile apps. Their digital strategy includes virtual boat tours, online configurators, and educational content, providing potential buyers with detailed information and engaging experiences.

We broadly consider the business model strong. The company has differentiated itself in a niche industry, with its product innovation, brand, and distribution network in particular allowing it to defend its position in our view.

We see scope for growth beyond broader economic development with:

- International Expansion - MCFT's expansion into international markets has broadened its customer base and brand image. As wealth shifts towards regions such as Asia, we see good scope for growth by pivoting its focus to specific international markets.

- Expanding Product Range - Diversifying its product line to include electric boats, other sustainable solutions, and other potential products has the potential to drive growth going forward. This could be achieved through M&A.

Margins

{kind=link}

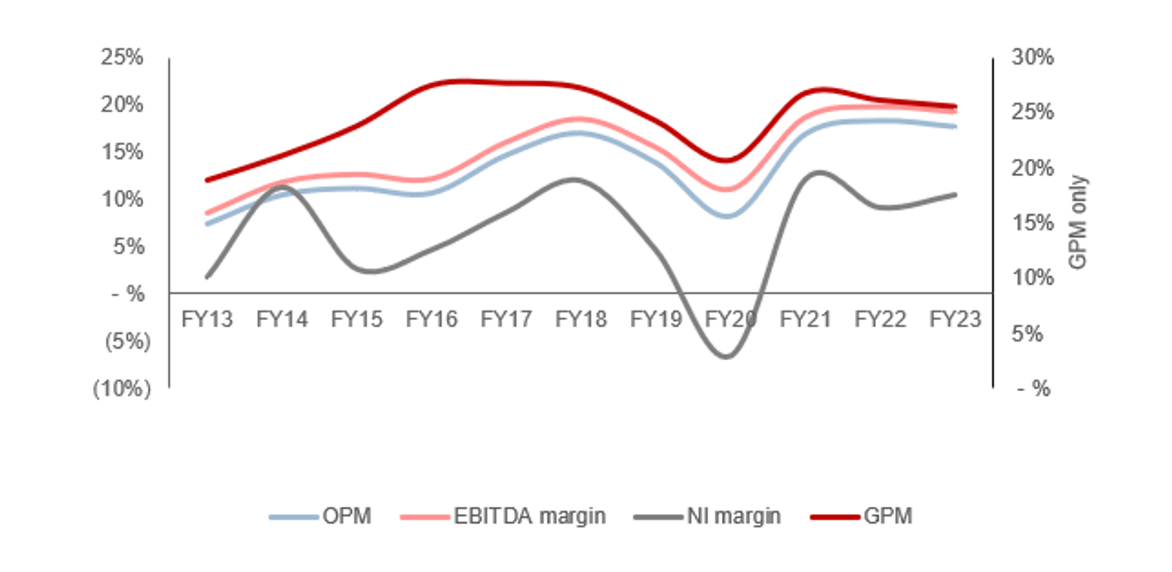

MCFT’s margins have developed well during the last decade, although the pandemic contributed to a stagnation of this, with the company broadly in line with its FY18 level.

Its margin improvement is due to a combination of numerous factors. Firstly, economies of scale in production as the business has grown, as evidenced by its incremental GPM improvement. Further, operating cost leverage, with S&A spending diluting to 8% of revenue. Finally, a product mix shift toward higher-value boats.

This said, the business has seen volatility, which is expected given the discretionary nature of its products. Margins will be highly tethered to the level of demand, which will dictate the amount of discounting required to achieve revenue.

Quarterly results

MCFT’s financial performance has slowed materially in recent quarters, with top-line revenue growth of +29.7%, +10.2%, (1.5)%, and (15.5)% in its last four quarters. In conjunction with this, margins have remained (impressively) flat, with EBITDA-M in excess of 19% in three of these four quarters.

The decline in revenue growth is a reflection of the current macroeconomic environment. With elevated interest rates and inflation, consumer spending on discretionary products has declined. Although MCFT targets more affluent customers, there has inevitably been a slowdown. Many of its products will be used for recreational activities and thus are inherently linked to the wider market.

We expect conditions to remain difficult until macroeconomic conditions improve and expansionary policy returns. This will likely be mid-to-late 2024 at the earliest, although does not necessarily mean MCFT’s revenue will continuously decline till then. This said, we do suspect the bottom is ahead.

Key takeaways from its most recent quarter are:

- This was the most profitable fiscal year in the Company's history, illustrating a period of strong growth and secular trends.

- Management acknowledges retail sales growth slowing significantly and is behind expectations. Inventory response was not sufficient, contributing to dealer inventories currently that are higher than Management considers optimal. This will likely contribute to difficulties in the near term.

- Management is turning focus to controllable actions, laying the foundation for long-term growth through investing in targeted initiatives that will allow the business to exploit industry growth.

- Management is seeking to achieve value creation through product line expansion, technological innovation, and an improvement in the customer experience.

Balance sheet & Cash Flows

MCFT is conservatively financed, with a ND/EBITDA ratio of (0.5)x. This gives Management the optionality of raising debt for growth if required, while also maximizing cash returns. These cash returns have been strong, with a FCF margin double-digits for the majority of the decade.

Despite this, however, distributions to shareholders have been minimal, with deleveraging and M&A preferred. We would like to see consistent buybacks/dividends if Management is not going to regularly acquire businesses. The cost of debt thus far has been minimal and so there has been no requirement to rapidly deleverage.

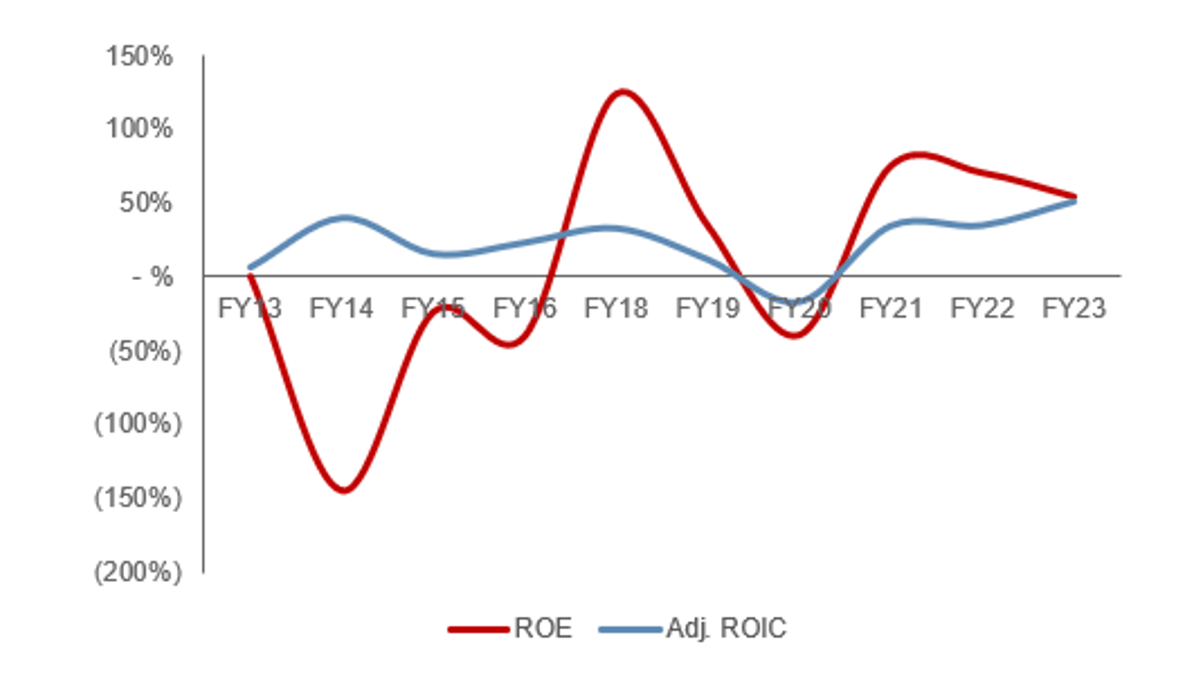

ROE has been broadly strong, with only a blip during the pandemic. Its ability to quickly shift inventory is critical to remaining asset-light despite its production nature, de-risking, and maximizing returns.

{kind=link}

Outlook

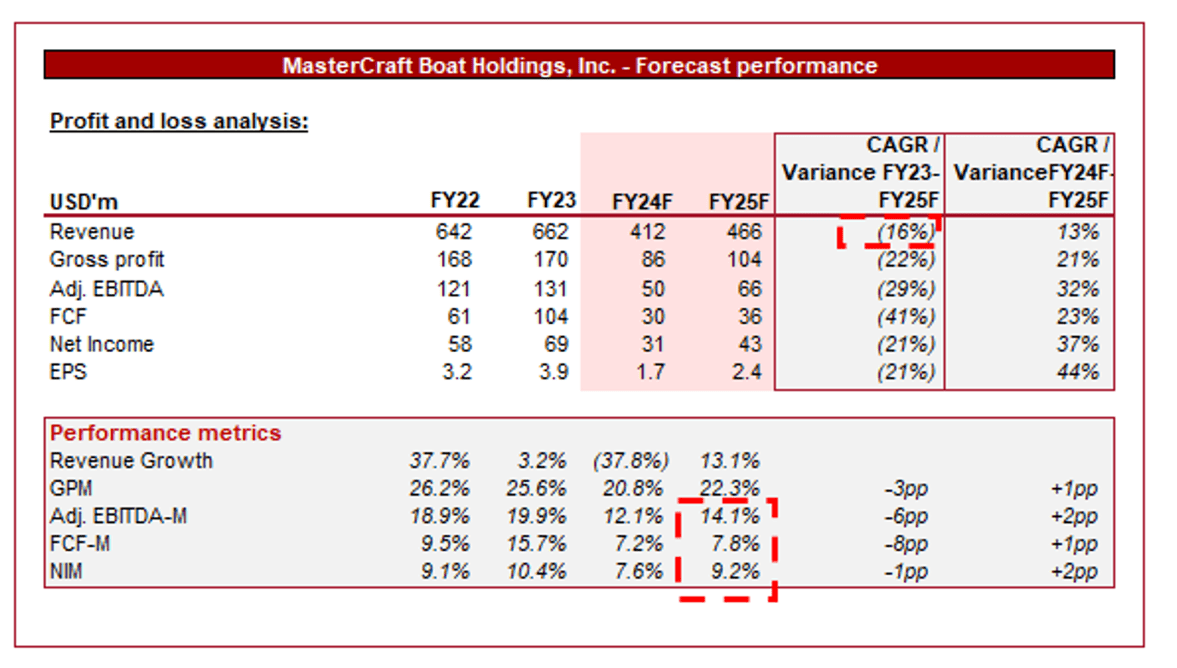

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a substantial step-down in revenue growth during FY24F, alongside a significant decline in margins.

These appear to be quite extreme assumptions given the limited outlook on FY24F. This said, we do see reason to consider the FY24F level to be reasonable. Firstly, the decline in revenue was progressively worsening, with macroeconomic conditions following suit. Further, with retailers stocking up on inventory, the level of initial demand will likely be abnormally low.

Considering the margin strength in the final two quarters, we believe there is significantly more uncertainty associated with where this lands. Analysts are likely assuming MCFT foregoes unit economics to protect revenue, which is not a bad assumption.

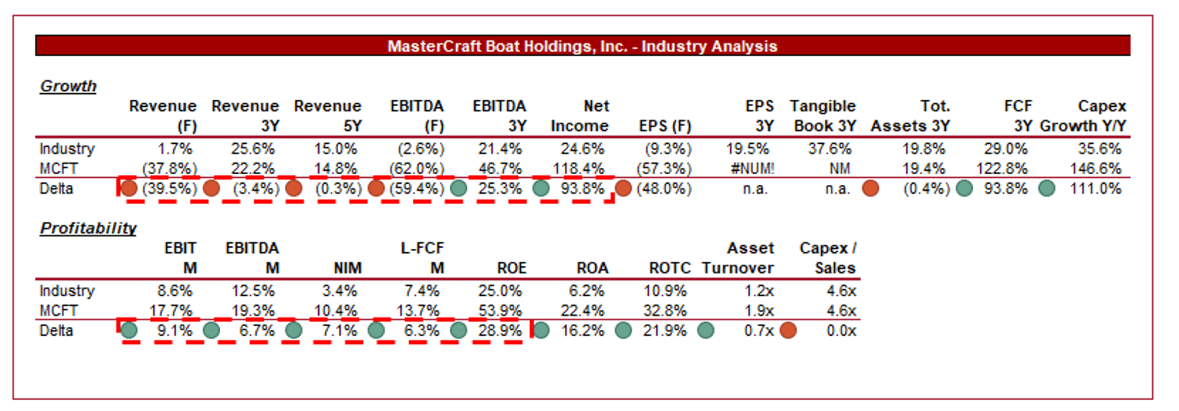

Industry analysis

Leisure Products Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of MCFT's growth and profitability to the average of its industry, as defined by Seeking Alpha (22 companies).

MCFT performs well relative to its peers. The company has lagged behind in revenue growth, but only marginally so. On an absolute basis, its performance is still strong. This reflects the uptick in demand for boats and MCFT’s ability to ride this wave.

Further, MCFT’s margins are significantly better, allowing for a superior LFCF margin and ROE. Even if the company sees a near-term contraction, it will potentially remain above average. High margins are a reflection of the nature of its products, with its niche and target audience allowing for premium pricing.

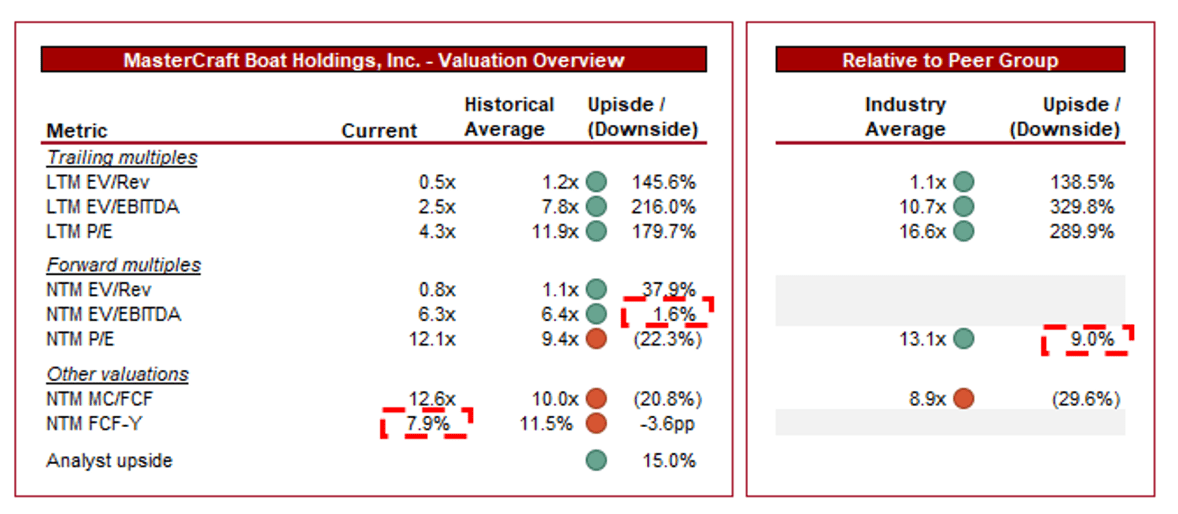

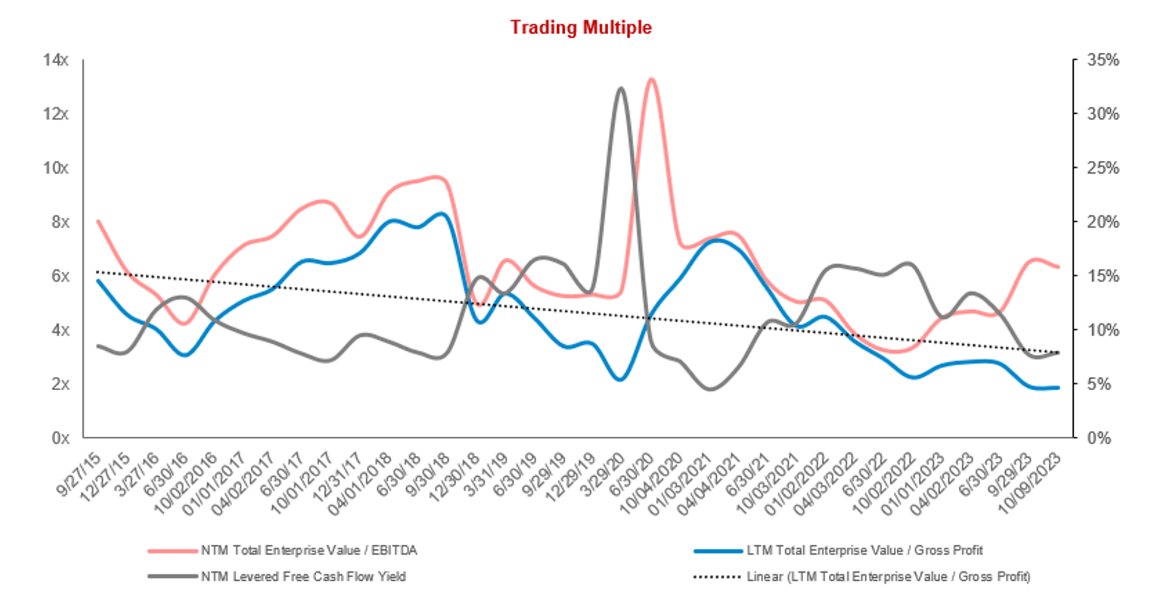

Valuation

{kind=link}

MCFT is currently trading at 2.5x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, primarily due to the near-term outlook, creating uncertainty about its 3Y trajectory. We do believe the development of its business model is an offsetting factor. The discount on an LTM basis appears unreasonably large, however, when taking into consideration the NTM forecast, its valuation appears overvalued.

Further, MCFT is trading at a substantial discount to its peer group, although again a much smaller amount on a NTM basis. on a normalized basis, we see good scope for a premium, owing to its strong margins. However, as the above illustrates, MCFT is expected to be far more impacted by the current conditions, with substantial margin risk. For this reason, a discount is reasonable. On a NTM basis, we believe the discount is slightly lacking, as we would suggest closer to ~20%.

Based on these factors, we believe the stock is likely overvalued by ~10%, not sufficient to imply a sell rating. We see the stock struggling in the coming quarters, although investors appear to be pricing in difficulties already.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Successful introduction of innovative products that contribute to improved demand.

- M&A to offset the potential decline in revenue growth

- Expanding market share through aggressive customer acquisition during this period of difficulty.

- Share price bounce on outperformance given the depressing outlook in FY24F.

Final thoughts

MCFT is a good-quality business. The company has developed a reasonable market position through scale, allowing its brand awareness and reputation to grow well, alongside its proximity to customers through its distribution network. Although simple, we believe these factors will allow it to defend its position against competition, allowing for good margins in the long term.

We are very concerned about the upcoming year, however, with a substantial decline in revenue ahead and margin uncertainty. We do not believe an investment today would be a good decision until there is greater visibility.

For further details see:

MasterCraft Boat: Quality Little Business Facing A Revenue Collapse