MCFT - MasterCraft: Small-Cap Stock With Strong Growth Potential

2023-07-07 06:04:59 ET

Summary

- MasterCraft Boat has delivered strong sales results, expanded its product line, and raised its guidance for a strong FY2023 end.

- MCFT has a low short interest at 7.08% and a forward price-to-earnings ratio of 5.96, which is below the consumer discretionary sector.

- Cautious of ongoing consumer discretionary headwinds and emission regulations that may influence boating designs in the long term.

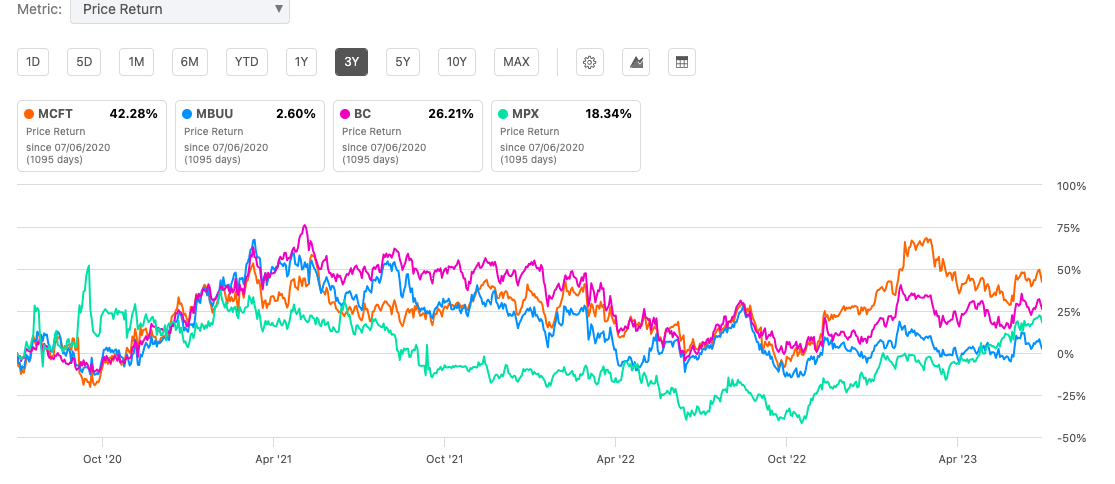

MasterCraft Boat Holdings, Inc. ( MCFT ), known for its wake surfing boats, has strengthened its top and bottom line fundamentals for three consecutive financial years. FY2023 is on its way to beating pre-pandemic results, with sales in Q3 2023 30% higher than in Q3 2019. Furthermore, the company has the inventory and innovations ready for a strong Q4; typically, 45% of annual powerboat retail sales occur in this period. Compared to some of its boating peers, MasterCraft has been a more rewarding stock to hold, with returns of 42.28% over the last three years.

Three year price return trend versus peers (SeekingAlpha.com)

{kind=link}

The stock has an attractive price-to-earnings ratio of 5.96 , generates positive and growing annual levered free cash flow and has a healthy balance sheet. The company has market-leading brands and recently released a new series of towboats . Although cautious of consumer discretionary headwinds, the company maintains strong sales, inventories are at optimal levels ahead of the Q4 summer selling season, and management has raised its guidance for FY2023 due to healthy demand in the previous quarters. Therefore, investors may want to take a bullish stance on this stock that is still trading well below its average price target of $35.40.

Company overview

MasterCraft is a builder, designer and seller of recreational powerboats. It has a diversified portfolio of brands, including MasterCraft, Crest and Aviara.

{kind=link}

It has grown through strategic acquisitions, organically and through internal band development. Its boats include ski-wake, fibreglass outboard, pontoon, and luxury day boats. The company has a strong reputation within the recreational boating industry and is known for its innovations. It has introduced various new upgrades, expanding its models over the last year, and most recently released a new model to its industry-leading wake and wave system boats lineup. Furthermore, dealer inventories have recovered with better availability to ensure healthy sales in the traditionally strong summer season.

The recreational boating industry in the US is expected to witness significant growth due to an increased demand for water sports in the area, expansion of water-related tourism and support from government initiatives. The North American market has an expected CAGR of 7% over the next five years to reach $15.1 billion by 2028.

{kind=link}

MasterCraft came into FY2023 cautious of the short-term headwinds regarding increasing inflation, high-interest rates and tightening of credit, all negatively impacting buying behaviour; however, over the last three quarters, sales have beaten pre-COVID numbers. Due to increased product availability and strong performance, the management team have raised their guidance for FY23 to sales of $656 million and adjusted EPS of $5.05.

Guidance FY2023 (Investor Presentation 2023)

Financials and valuation

MasterCraft has been increasing its sales and gross profit over the last five years if we ignore the COVID-19-influenced FY20. Sales have grown from $332.7 million in FY18 to $758.9 million TTM. The gross profit margin has decreased over the last five years from 27.31% in FY18 to 23.47% TTM. Net income was $57.8 million TTM and has been positive over the previous two financial years.

{kind=link}

As indicated below, MasterCraft has beaten annual EPS expectations for the last eight financial years.

{kind=link}

There is a positive levered free cash flow TTM of $104.2 million. Below we can see that cash flow has been positive over the last five years and above the $25 million mark, not including COVID-19-influenced FY20. This means that the company has cash to invest back into the company, reward investors or pay off debts. The company repurchased $7 million in common stock in the last quarter. It has spent over 80% of its $50 million authorised program since June 2021.

Annual levered free cash flow (SeekingAlpha.com)

If we look at the balance sheet, we can see that MasterCraft has total cash of $101.37 million TTM and total debt of $54.4 million TTM. MasterCraft has a current ratio of 1.81 and a quick ratio of 1.17, indicating that the company is sufficiently liquid to cover its short-term liabilities.

The small-cap stock has rewarded investors with returns of 39.04% over the last year and has a market cap of $527.31 million with relatively low short interest at 7.08%. It has a desirable FWD price-to-earnings ratio of 5.96, which is well below the consumer discretionary median of 14.60. Furthermore, we can see that the stock has outperformed some of its larger peers, Malibu Boats ( MBUU ) and Brunswick Corporation ( BC ) over the last three years regarding price returns. It is also trading under its peers, and its price-to-sales ratio is under one at 0.71, indicating that investors are paying less than a dollar for every dollar earned.

{kind=link}

{kind=link}

Risks

Investing in MasterCraft, a small-cap stock, can be profitable but risky due to its tendency to fluctuate faster than larger stocks. The company's products are discretionary, making it vulnerable to a weakening economy. Additionally, macroeconomic factors such as regulations could affect its performance, especially with new emissions regulations in the US potentially requiring costly technology updates. Despite economic challenges like inflation, higher interest rates, and tightening credit, MasterCraft has outperformed its original conservative guidance for FY23 and is confident in a strong finish.

Final thoughts

MasterCraft is a small-cap stock with a positive upward trending stock price over the last three years, outperforming larger peers in the recreational boating industry. Furthermore, it has been increasing its top and bottom line results while investing in the business through acquisitions and internal brand development. It has recently released a new line of boats, management has increased its FY2023 guidance, and the coming Q4 is historically a strong quarter. The stock is still trading well below its average price target. Therefore investors may want to take a bullish stance on this stock.

For further details see:

MasterCraft: Small-Cap Stock With Strong Growth Potential