DVN - Matador Resources: Drilling For Dollars In New Mexico

2023-05-09 08:00:00 ET

Summary

- Matador Resources Company's price has been crushed in the last three weeks. We think this is overdone and presents a compelling opportunity at current prices.

- Matador Resources plans aggressive growth drilling with a boost in production that is not reflected in current prices.

- We think investors may find Matador Resources Company to be a good value proposition at current prices.

Introduction

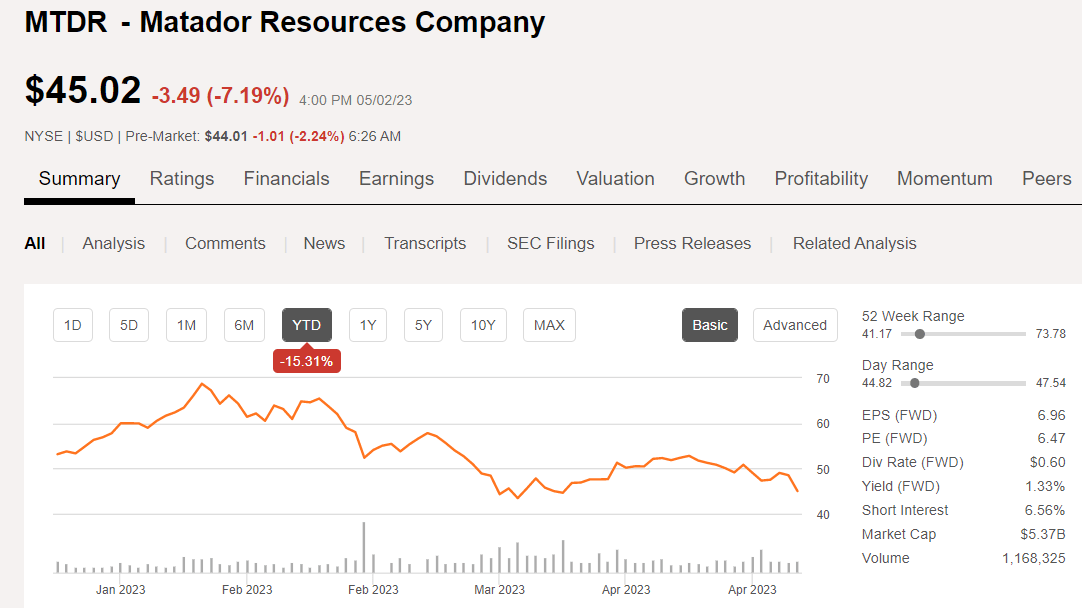

Matador Resources Company ( MTDR ) has been busy since we last wrote them up. Adding to reserves, increasing output, drilling wells that make a U-turn?!?!. None of that has mattered to its stock price in recent times, unsurprisingly. Since early February, MTDR has ridden the elevator down with the general WTI-based, shale driller cohort. It's been painful, but every cloud has a silver lining. Good companies like MTDR are getting cheaper, and may soon present very attractive entry points, certainly as compared with a few months ago.

{kind=link}

The company has been busy growing reserves, doubling the value of its acreage footprint through technology-I will discuss this later, and making strategic acquisitions. These factors are normally associated with success, and we think Matador belongs in that category. Analysts have viewed the company favorably , perhaps in part due to their habit of beating EPS estimates regularly. Price targets prior to the current rout have been substantially above recent highs in the low $50's, with a range of $61 to $81, and a median of $70.

Let's take a closer look at this company and come to our own conclusions about their near-term prospects.

A few thoughts on the macro picture first

The current rout in energy - everything energy it seems - is letting a lot of air out of the shale balloon. It's hard to pick a favorite in the current calamities making the rounds, really. Lackluster Chinese demand, or a regional bank implosion....take your pick. How about a U.S. debt default? We live in a time of extremes. One thing worth remembering is that, in times of inflation, panic, and even outright rebellion... assets have value. At the present, energy assets are undervalued in proportion to the benefits they bring. They have intrinsic value!

I remind you of a point I made in the Exxon Mobil Corporation ( XOM ) article, They Don't Call It Black Gold For Nothing :

Something that often gets lost in discussions is XOM's product has intrinsic value . It's worth something. The value rises and falls according to market conditions, but at the end of the day we can't do without it. I bring this up because some authors are pointing to XOM's fairly paltry yield and recommending Treasuries at current rates. That case can be made, but do Treasuries have intrinsic value? Meaning can you put a T-bill in your gas tank and roll on down the road? Un-huh!

We think we are nearing a time when that situation may reverse, but we aren't there yet. I have no crystal ball and rely on logic and insight to form my opinions. Sometimes that works and other times you just have to roll with the market if you are long. That leaves us finding good companies that are becoming cheaper by the day, and I will suggest that Matador Resources is one such gem. And, when logic reasserts itself, Matador Resources Company could reward investors entering at current levels.

The thesis for Matador

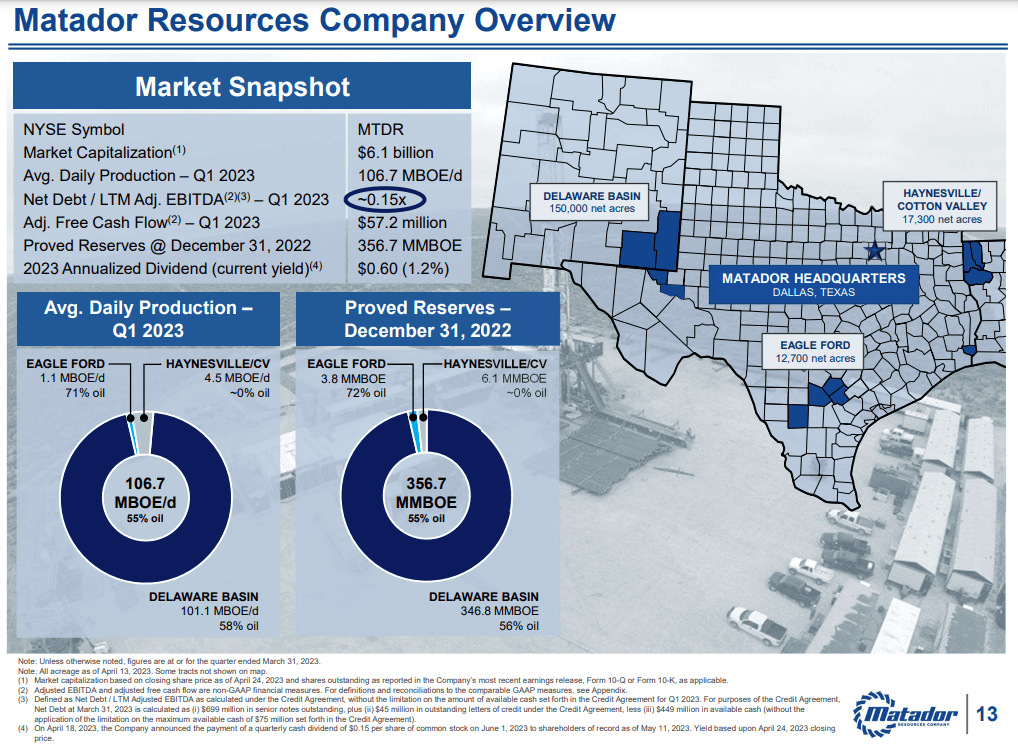

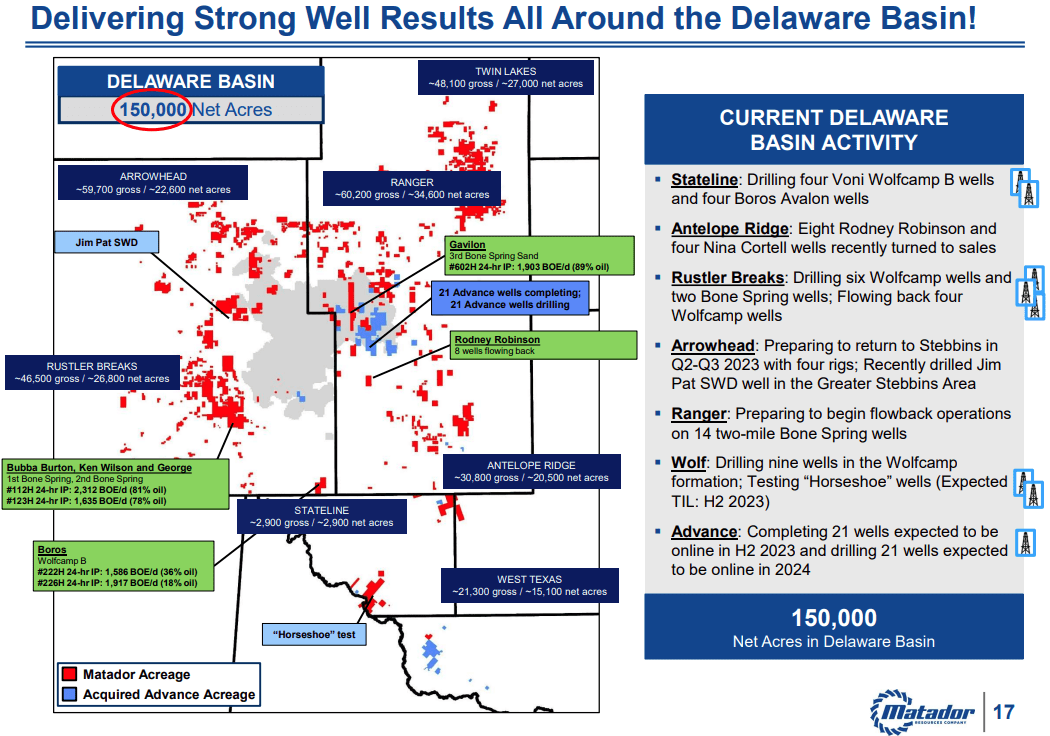

The company is focused primarily on the Delaware basin and has rapidly grown production, while cutting costs in direct and through technology. MTDR also has smaller acreage positions in the Eagle Ford and the Haynesville. In addition to its core E&P business, it operates a midstream company-San Mateo, that offers crude gathering, water transport, and disposal. The Advance deal brought new midstream optionality to MTDR's internally operated Pronto natural gas Midstream assets. The company has aggressive plans to take daily output from Q-4, 2022's, 111K BOEPD to 143K BOEPD, by Q-4, 2023. Oil percentage, thanks in large part will increase by 40%, as the company incorporates the Advance acreage near their Ranger drill unit in 2023 plans. Growth is a key to the thesis for MTDR, and they have a history of delivering it, while controlling costs.

{kind=link}

Recent events for MTDR

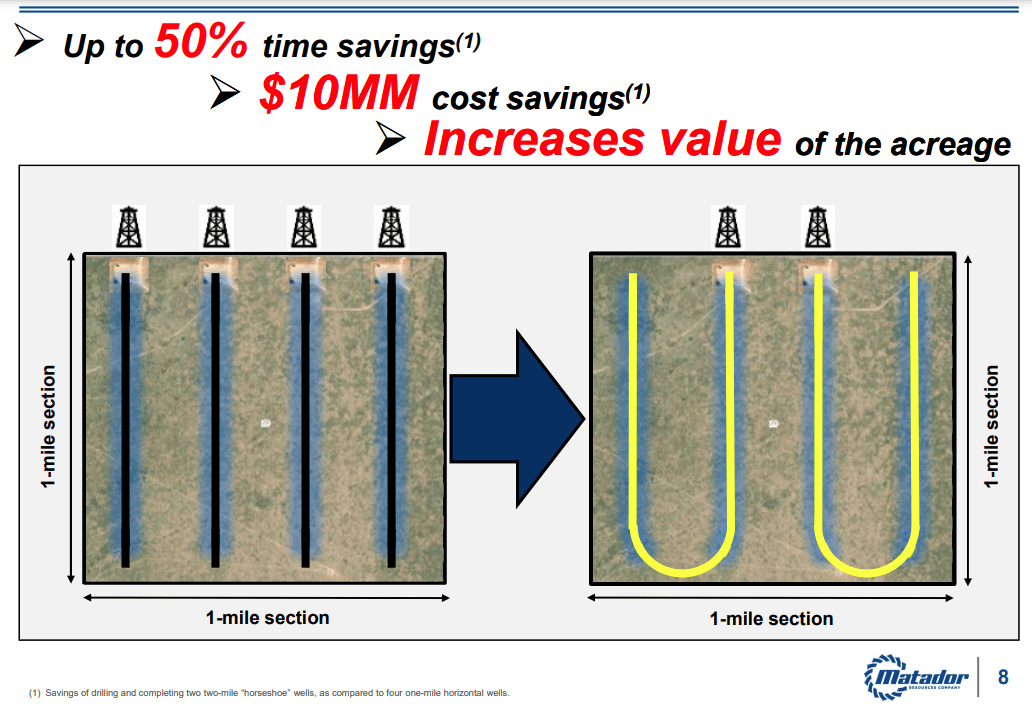

Often we extoll the virtues of big, blocky acreage that enables drilling 12-15K laterals much of the industry is moving toward. What if you don't have that blocky footprint that permits these wells? Simple, you make a U-Turn. Below you see an example of this innovation, that cuts costs and increases the value of the acreage. Glen Stetson, EVP-Production commented on the rationale for the U-turn wells in this acreage :

So this piece of acreage was unique in that the upper Wolf Camp, the Wolf Camp AXY was undeveloped, but in our section but that had been developed on every other side of this piece of acreage

It may seem like an out of the box approach, but if you think about it, it's done all the time. Deviating from vertical to horizontal involves a 90 degree build angle. Just flip the build angle on its side, drill the U-section, then build 90 degrees back in the other direction. A question that occurs to me is the contribution of the last foot in a well like this.

{kind=link}

It may seem like an out of the box approach, but if you think about it, it's done all the time. Deviating from vertical to horizontal involves a 90 degree build angle. Just flip the build angle on its side, drill the U-section, then build 90 degrees back in the other direction. Chris Calvert, Matador Resources Company COO, comments on the costs savings resulting from these U-bend wells :

We’ve documented it’s about $10 million in estimated savings that we’re going to realize, when you think about the amount of steel that’s needed to case a four string well, if you’re doing four single mile laterals versus two U-turn horseshoes, we’re actually saving about 10 miles of casing basically by reducing two vertical portions of these wells.

Makes sense.

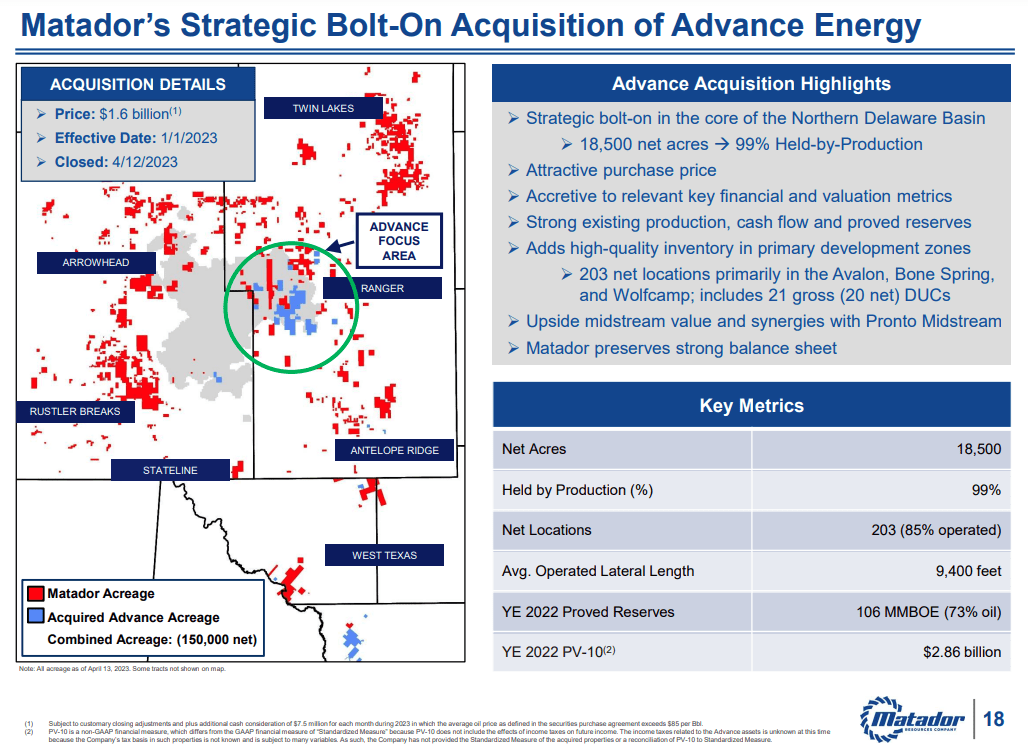

The Advance deal

This obviously looks like a nice pickup from an acreage utilization aspect. It works out to $88K per acre - they've paid more in the past. The market hasn't really clapped their hands about this so far, as they paid $1.6 bn in cash up front and entails further payments of $7.5 mm per month in 2023 when WTI is above $85 bbl. (That doesn't appear to be an issue right now!) The big upfront payment is at odds with a recent trend where companies swapped or printed stock to pay for transactions.

{kind=link}

It also comes with 24,500 BOEPD of high oil cut-74% production, which eases the pain from day-1, (01/01/2023), and 203 new drilling locations Tier I, Bonespring, Wolfcamp, and Avalon. There are also 21 DUC's ready to frac, so production could get a shot in the arm as these come on line.

One takeaway from this deal might be that people are recognizing that Tier I locations are getting scarcer, and they come with a cost. Cash and debt.

Geology and Technology delivering the goods

Matador is in some good dirt, clearly, with results like what they show in the slide below. The EIA DPR chronicles the decline in new well production over the last few years. The average in the Permian basin is just over 1,000 BOPD. MTDR is doing much better than that with many of these completions delivering 2,3K BOEPD.

{kind=link}

From a geological perspective, Tom Elsener, EVP Engr -commented on the quality of rock they are producing in the Lea County area of New Mexico:

We’re clearly very excited for all of the – all these wells that will be drilled and completed on the Advance properties. The bulk of it there is in Southern Ranger, Northern Antelope Bridge where we’ve drilled wells nearby, like the Mallon wells that have each produced a million barrels of oil each nearby some of our other Nina Cortell wells on the northern end of Antelope Bridge. And then we’ll, for the south where the Rodney Robinson wells are, this is an area that’s characterized by having very high oil cuts, typically 75% oil cut and also very low water cuts.

When you combine MTDR's great rock in the Delaware with the state of engineering for shale drilling and fracking these days, you get a winning combination that delivers these results.

Q-1 2023 results and guidance

Average production of 106,654 BOE per day (58,941 BOPD), this was a 14% organic increase in output from Q-1. Net cash provided by operating activities came to $339.5 million and Adjusted Free Cash Flow to $57.2 million. Net income came to $163.1 million, or $1.36 per diluted common share. Adjusted net income of $180.0 million, or adjusted earnings of $1.50 per diluted common share. Q-1 adjusted EBITDA came to $365.2 million, and San Mateo net income landed at $32.2 million, a reduction from Q-4, 2022's consolidated EBITDA of $504 mm. Primarily due to declines in realizations for the quarter.

{kind=link}

San Mateo Adjusted EBITDA of $48.7 million. Drilling, completion and equipping capital expenditures were $294.8 million, with midstream capital expenditures of $8.7 million.

Advance Acquisition Highlights

The deal closed on April 12, 2023 for an initial cash purchase price of $1.6 billion, subject to post-closing adjustments as previously discussed. Along with it came approximately 18,500 net acres (99% held by production) in the core of the northern Delaware Basin, most of which is strategically tucked in adjacent to Matador’s Ranger asset area in Lea County, New Mexico. A key feature of the deal was the 406 gross (203 net) horizontal locations identified for future drilling, including prospective targets throughout the Wolfcamp, Bone Spring and Avalon formations. Plans are to quickly monetize this new acreage. To do this they will be

- Completing 21 gross (20 net) wells that are expected to be turned to sales in the second half of 2023

- Drilling 21 gross (19 net) wells that are expected to be turned to sales in early 2024.

The PV-10 of the proved 100+ mm oil and natural gas reserves at December 31, 2022 of approximately $2.86 billion using the same unweighted arithmetic average first-day-of-the-month prices for the previous 12-month period that was used to value the Company’s reserves at December 31, 2022, which were $90.15 per barrel of oil and $6.36 per MMBtu of natural gas.

The Advance deal along with other acreage bolt-on acquisitions in 2023, brought MTDR to 150,000 net acres in the Delaware Basin, with a significant increase in the total proved oil and natural gas reserves to approximately 465 million BOE. These reserves are estimated to have a PV-10 value of approximately $12 billion.

Debt

MTDR funded the Advance acquisition with a combination of cash on hand, free cash flow and borrowings under their reserves-based lending-RBL, credit agreement. The borrowing base under the RBL credit agreement is $1.25 billion and does not yet include any reserves for the assets that were acquired in the Advance acquisition. On March 31, 2023, we successfully increased the elected commitment under the RBL credit agreement from $775 million to $1.25 billion, of which only $625 million is currently drawn.

The company successfully launched a private offering of $400 million of senior unsecured notes due 2028, which was oversubscribed by $3 billion. The high demand for these bonds led to an increase in the size of the offering from $400 million to $500 million and issued the 6.875% senior unsecured notes at a price of 98.96% of their face value.

Following the bond offering that included an increase in their borrowing base to $2.2 bn, MTDR had over $600 million in liquidity. The company intends to use their free cash flow for the remainder of the year primarily to repay debt under the RBL credit agreement, as shown in the slide below. Growth capex will also be funded, as will the fixed dividend while continuing to opportunistically pursue strategic bolt-on acquisitions and midstream opportunities that may arise, are the next priorities.

{kind=link}

Guidance for Q-2 and 2023

Matador anticipates its average daily oil equivalent production should increase 19% from 106,654 BOE per day in the first quarter of 2023 to approximately 126,500 BOE per day in the second quarter of 2023. This significant sequential increase is primarily attributable to the closing of the Advance acquisition in April 2023. Matador expects to turn to sales 27 gross (20.8 net) operated horizontal wells in the Delaware Basin during the second quarter of 2023.

The Company expects D/C/E capital expenditures for the second quarter of 2023 will be approximately $358 million and midstream capital expenditures to be approximately $41 million.

{kind=link}

Risks

Current pricing has MTDR, some 20% below prices of three weeks ago, so I would say the bottom is in, absent further oil price declines. There is some optimism built into the Advance deal basing valuations at Dec, 22 WTI prices. $90 crude is in the rear view for the foreseeable future, and cash flow generation may not allow repayment of the RBL as quickly as they anticipate.

The company is unhedged anticipating higher oil and gas prices as we go through the year. Joe Foran, Chmn comments on MTDR's hedging philosophy:

The upside is limited so that if you have a somewhat reversal in the top price, the sailing you don’t have much room and you could be quickly paying money out rather than receiving the benefit of higher oil prices. So that’s where we think it is. We think it’s, oil prices currently are a little less and that the middle ground is somewhat higher above the price you can hedge. So we would think we’d be losing money on the outset or undertaking too much risk on having to not getting that benefit of higher prices should they turn around some.

Can't argue with that, but it does present a risk if oil prices tank completely.

Your takeaway

As I noted in the thesis statement, the driver for Matador Resources Company is growth. They have been hitting targets, so let's do them the courtesy of assuming they will continue to do so.

On that basis, assuming $75 WTI to be conservative, loose math suggests, they will generate revenues of ~$3.60 bn, less capex of ~$1.2 bn, less costs of revenue at ~$400 mm, dividends of $71 mm, and debt repayments of ~$300 mm, resulting in~$1.7-$1.9 bn of EBITDA in 2023 with average production of 130K BOEPD.

On that basis, Matador Resources Company is trading at a high side EBITDA of $1.9 bn of 3.3X EV. That's not excessive by any means. For reference, one of our favorites, Devon Energy Corporation ( DVN ), is selling at 3.6X EV/EBITDA, at today's depressed prices. On a flowing barrel basis using their YE 2023 exit rate, Matador Resources Company sells for $42K per bbl. Pretty cheap compared with some companies we have seen recently.

Matador Resources Company pays a modest dividend of $0.60 per share, but should be considered primarily a growth proposition levered by controlled costs, and expanding production.

For further details see:

Matador Resources: Drilling For Dollars In New Mexico