PXD - Matador Resources: Looks Like A Very Solid Buy After Q4 Earnings

Summary

- Matador Resources Company joined its peers in reporting very strong Q4 results.

- The company reported record production and strong reserve development.

- The acquisition of AEP sets it up very well to deliver 20%+ growth in 2023.

- The company has been using its high free cash flow to strengthen its balance sheet and now has one of the lowest leverage ratios in the industry.

- Matador Resources Company is trading at a very attractive price.

On Wednesday, February 21, 2023, Permian-based shale driller Matador Resources Company ( MTDR ) announced its fourth quarter 2022 earnings results. As was the case with most traditional energy companies that have reported their results so far, Matador Resources reported very solid results that showed year-over-year growth. This was at least partly due to crude oil prices, which remained higher than in the prior-year quarter despite the decline that we saw during the second half of the year. This is something that all investors should appreciate, as the long-term fundamentals for crude oil are quite positive and point to higher prices.

We will likely see some weakness in the near term due to recession fears and the Federal Reserve’s tightening monetary policy, though. That will provide an opportunity for accumulation if Matador Resources Company is not currently in your portfolio. Matador Resources saw its market price decline upon the release of this earnings report, so that could provide us with a buying opportunity.

Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Matador Resources’ fourth-quarter 2022 earnings report :

- Matador Resources brought in total revenues of $707.475 million in the fourth quarter of 2022. This represents a 24.92% increase over the $566.358 million that the company reported in the prior-year quarter.

- The company reported an operating income of $371.700 million in the reporting period. This compares quite favorably to the $325.121 million that the company reported in the year-ago quarter.

- Matador Resources produced an average of 111,735 barrels of oil equivalent per day during the most current quarter. This set a new record for the company and obviously beat the 87,288 barrels of oil equivalent per day that the company produced on average at this time last year.

- The company reported an adjusted free cash flow of $249.3 million in the period. This represents a 108.97% increase over the $119.3 million that the company reported in the corresponding quarter of last year.

- Matador Resources reported a net income of $253.8 million in the fourth quarter of 2022. This represents an 18.16% increase over the $214.8 million that it reported in the fourth quarter of 2021.

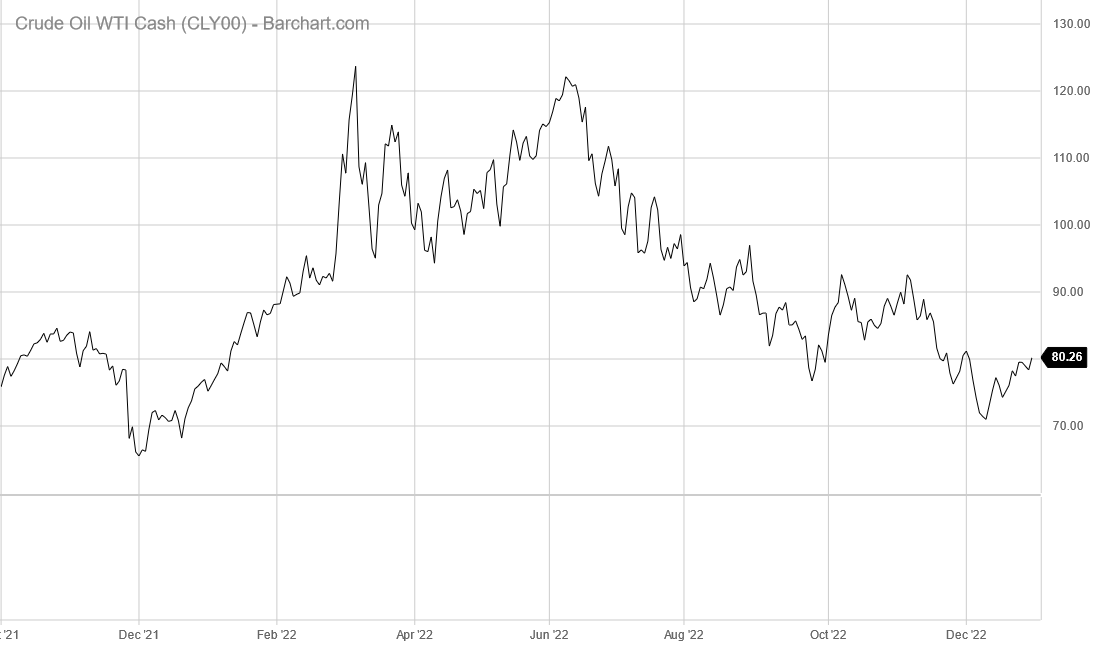

It seems essentially certain that the first thing that anyone reviewing these highlights will notice is that, basically, every measure of financial performance showed significant improvement compared to the prior-year quarter. This was largely expected as we have seen nearly every other traditional energy company show year-over-year financial improvements. One of the biggest reasons for this is that crude oil prices were higher during the fourth quarter of 2022 than they were during the fourth quarter of 2021:

{kind=link}

As we can see, the price of West Texas Intermediate crude oil declined significantly during the second half of 2022, but it still remained higher than it did during the same quarter of last year. It should be obvious why this would stimulate revenue growth. After all, Matador Resources received more money for each barrel of crude oil that it sold during the quarter than it did a year ago. All else being equal, that results in more money coming into the company. This means that it has more money available to cover its fixed expenses and ultimately makes its way down to the bottom-line net income and cash flow. We can see that Matador Resources benefited from the higher prices by looking at its realized sales prices:

| Q4 2022 |

| Q4 2021 |

| Crude Oil ($/bbl) |

| $82.39 |

| $60.96 |

| Natural Gas ($/mcf) |

| $5.32 |

| $6.64 |

We do see that Matador Resources had its natural gas realized sales price decline year-over-year. This does not contradict the statement that the company received higher amounts of money for its products than it received a year ago. This is because Matador Resources’ production is mostly weighted to crude oil. As we can see here, about 56% of its production is crude oil:

Matador Resources

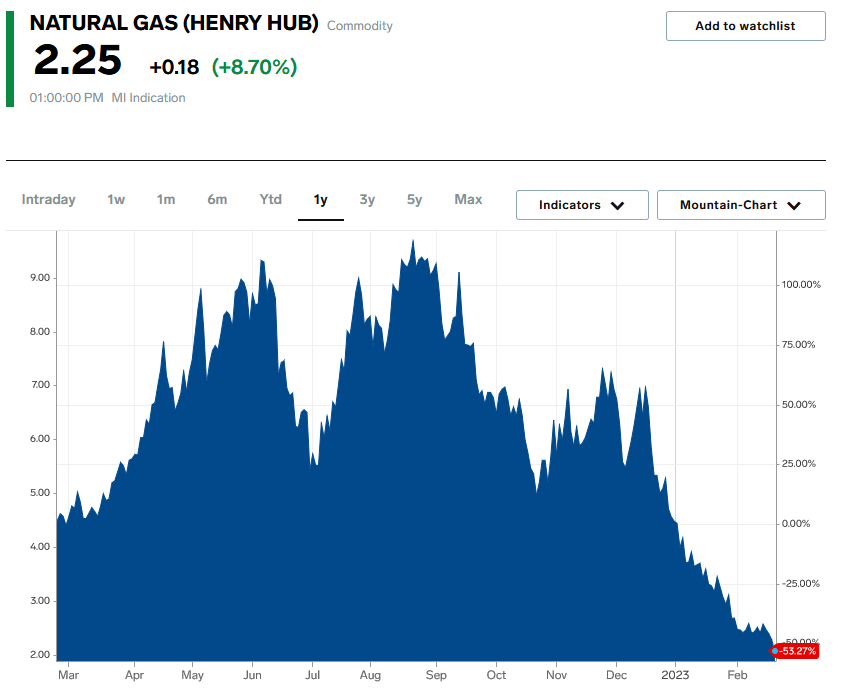

That is something that benefited it quite a bit this quarter. This is because natural gas prices have not been holding up as well as crude oil prices. We saw declines in both during the second half of 2022, but natural gas declined much more as the warm winter in both the United States and Europe reduced demand compared to previous years. Indeed, over the past year, natural gas at Henry Hub is down 53.27%:

{kind=link}

This compares to only a 16.15% decline for West Texas Intermediate crude oil over the same period. Thus, if Matador Resources had been more weighted to natural gas, its earnings would probably not have been as good as they were. With that said, though, the long-term fundamentals for natural gas are stronger than those for crude oil due to its use in the production of electricity, so it is nice to see that the company still has some exposure to that commodity.

All is not equal when it comes to energy companies like Matador Resources, however. As noted in the highlights, the company benefited from its highest production level in history. The company produced an average of 111,735 barrels of oil equivalents per day, which is a 28.01% increase over the prior-year quarter:

Matador Resources

This higher production also had a positive impact on the company’s financial performance. It should be obvious why this would be the case. After all, a higher level of production means that the company had more products that it could sell for money. This helps to offset some of the impact of the fact that crude oil prices are not as high as they were back in June 2022, and more importantly some of the impact of the natural gas price decline over the past year. It did not fully offset it, though, and Matador Resources’ adjusted EBITDA still came in lower for the fourth quarter than it did earlier in the year:

Matador Resources

That is disappointing, particularly considering that adjusted EBITDA is essentially a proxy for pre-tax cash flow, and as investors, we are mostly interested in cash flow. With that said though, Matador Resources did report a record adjusted free cash flow of $1.217817 billion over the course of 2022. That had a positive impact on the company’s balance sheet, which we will discuss later in this article. Overall, there is little to be disappointed with, even though these results were a bit weaker than the company’s performance in the second or third quarters of 2022.

Whenever an energy company releases its fourth quarter results, it typically includes a summary of its reserves. This is something that we want to keep an eye on because of the importance of reserves to an oil and gas company. Investors frequently overlook this, however, which is a big mistake. This is because the production of crude oil and natural gas is by its nature an extractive process.

Matador Resources literally obtains its products by pulling them out of reservoirs in the ground. As these reservoirs only contain a finite quantity of resources, the company must continually discover or otherwise acquire new sources of resources or it will eventually run out of products to sell. As of December 31, 2022, Matador Resources had total proved reserves of 356.722 million barrels of oil equivalent compared to 323.397 million barrels of oil equivalent that it had on December 31, 2021.

That is nice to see because it shows that the company not only managed to replace all the resources that it pulled out of the ground but was able to do that and still grow its reserve base. This is exactly the kind of thing that we like to see to ensure long-term sustainability. At its fourth-quarter production level, the company’s proven reserves are sufficient to last for 8.75 years. That is not as good as the ten-year life that many of the company’s peers have but it is reasonably acceptable. It would be nice to see Matador Resources acquire some new resources to boost its effective reserve life, though.

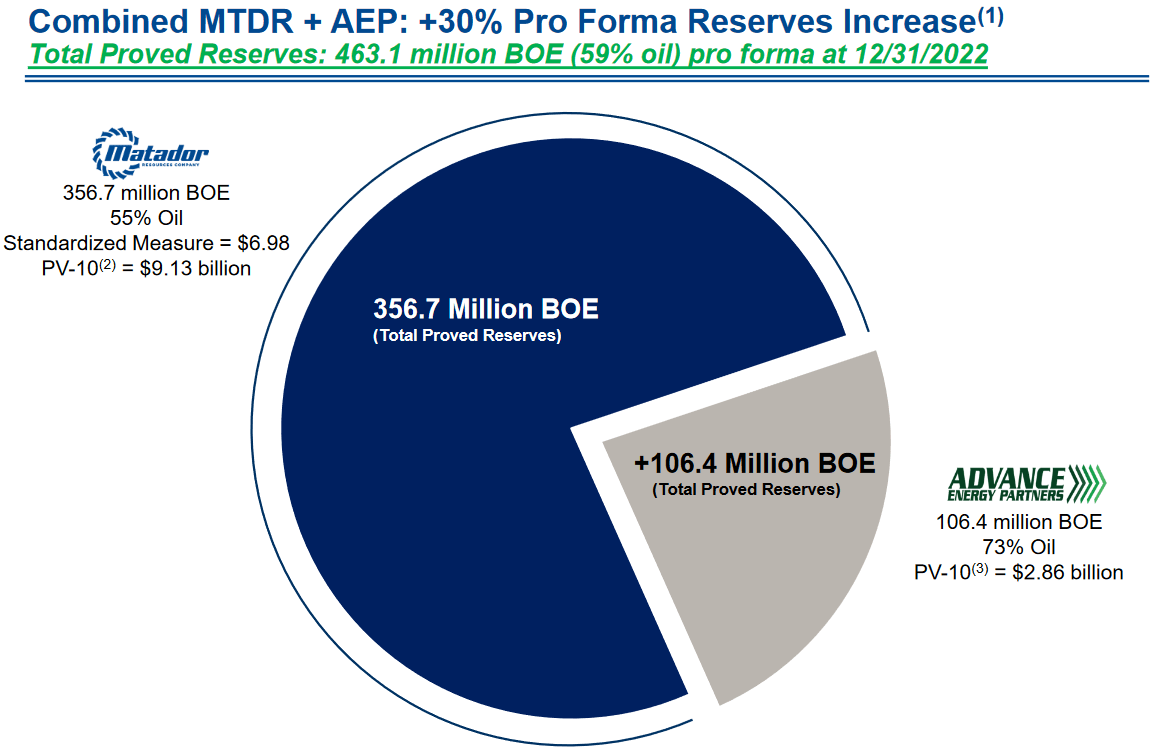

Fortunately, the company is doing exactly that. Last month, Matador Resources agreed to acquire Advance Energy Partners Holdings for $1.6 billion. That makes this the largest acquisition in the company’s history. Advance Energy Partners has estimated proved reserves of 106.4 million barrels of oil equivalents as of December 31, 2022, which would become directly accretive to Matador Resources’ total once the acquisition closes:

{kind=link}

This acquisition is expected to close early in the second quarter of 2023, but it has an effective date of January 1, 2023, so we can assume that this is a done deal at this point.

In addition to boosting Matador Resources’ reserves, the deal will also increase its EBITDA and profits. After all, the land that it will be acquiring through this deal is producing oil and natural gas. The company expects that it will increase its adjusted EBITDA by $475 million to $525 million annually if oil prices stay around their present level. Matador Resources had a full-year 2022 adjusted EBITDA of $2.224158 billion so that would be a 21.36% to 23.60% increase over the company’s 2022 figures. That is not exactly a bad year-over-year cash flow boost, particularly considering that this acquisition will pay for itself in about 3.2 years.

Financial Considerations

It is always important to look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the money to repay the maturing debt, which can cause a company’s interest expenses to increase depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. This is something that can be a very real risk for a company like Matador Resources due to the volatile nature of commodity prices.

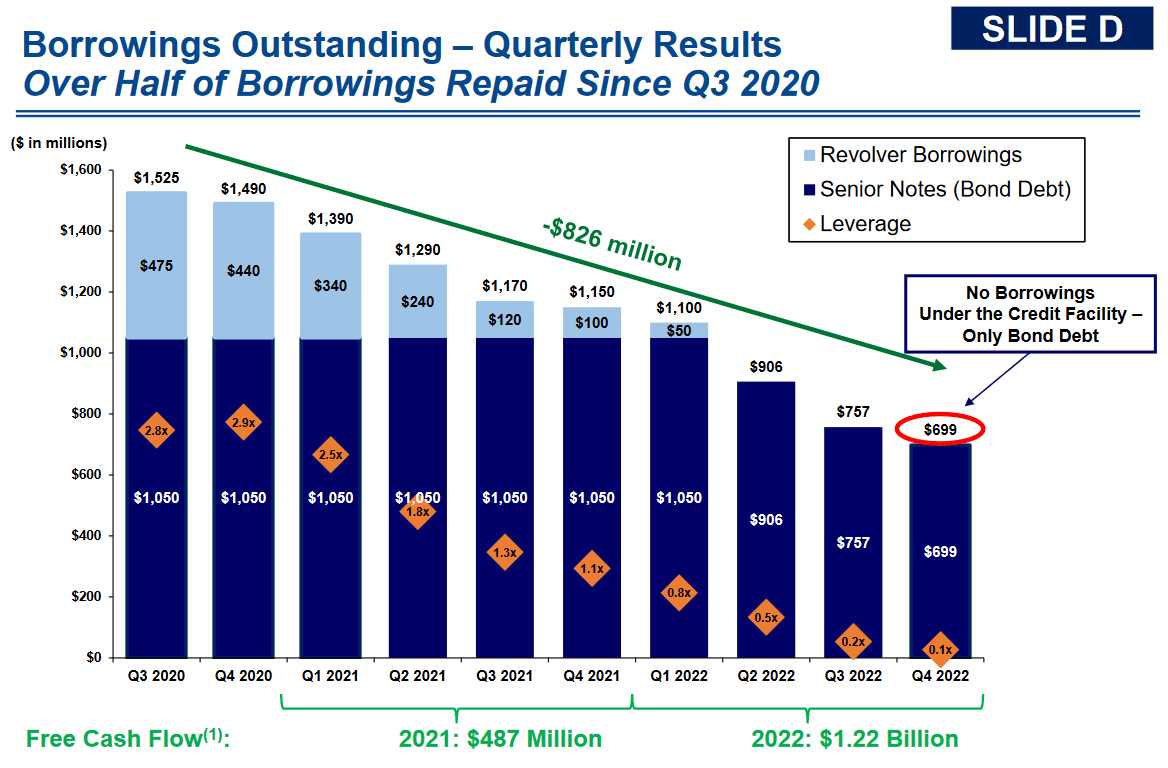

One metric that we can use to judge an exploration and production company’s ability to carry its debt is its leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to this task. As of December 31, 2022, Matador Resources had a leverage ratio of 0.1x based on its trailing twelve-month adjusted EBITDA. This is an incredibly low ratio that is directly linked to the company’s focus on maximizing its free cash flow in the two years since the outbreak of the COVID-19 pandemic:

{kind=link}

As we can see, Matador Resources has been using its cash flow to pay down its debt. This is one of the reasons why the company has so far not rewarded us with a huge dividend like Pioneer Natural Resources ( PXD ) or Devon Energy ( DVN ). The fact that the company now has almost no net debt though is a very good thing. One major reason for this is that the market continues to be somewhat hostile to traditional oil and gas companies.

We have even seen a few banks refuse to lend to companies in the industry. Thus, the company will ideally not want to depend on outside capital. It is hardly alone in this as we have seen many energy companies spend the past two years focusing on strengthening their balance sheets and achieving independence from the capital markets. It is very nice to see that Matador Resources has now accomplished this goal. Investors have nothing to worry about regarding the company’s debt.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of an independent exploration and production company like Matador Resources, one method that we can use to value it is to look at the forward price-to-earnings ratio. This is similar to the commonly reported price-to-earnings ratio except that it incorporates analysts’ estimates of the company’s earnings per share over the next year. The ratio essentially tells us how much we are paying today for each dollar of earnings that the company is expected to generate over the next year.

According to Zacks Investment Research , Matador Resources currently has a forward price-to-earnings ratio of 6.08 based on estimates of its forward earnings per share. That is substantially lower than the 20.81 forward price-to-earnings ratio of the S&P 500 Index ( SP500 ):

{kind=link}

Matador Resources looks incredibly cheap by this measure. However, as I have pointed out in the past, pretty much everything in the traditional energy industry is substantially undervalued based on earnings. Thus, it may make sense to see how Matador Resources compares to some of its peers in order to determine which company currently offers the most attractive current valuation. Here is a summary:

| Company |

| Forward P/E |

| Matador Resources |

| 6.08 |

| Diamondback Energy ( FANG ) |

| 5.67 |

| Pioneer Natural Resources |

| 8.70 |

| Devon Energy |

| 6.98 |

| APA Corporation ( APA ) |

| 5.37 |

As we can see here, Matador Resources is not the cheapest company in the industry. However, it does generally compare well to its peers. As the price per dollar of earnings is substantially lower than anything outside of the traditional energy sector, it might make sense to buy the stock today, especially since the share price fell significantly following the release of this earnings report.

Conclusion

In conclusion, Matador Resources Company continued the string of strong earnings releases that we have been seeing across the energy sector. In particular, the fact that Matador Resources Company achieved record free cash flow in 2022 is quite nice, as is the fact that it achieved positive reserve development. When we consider the boost that is likely to come to the company in 2023 due to the Advance Energy acquisition and its affordable valuation, Matador Resources looks like a very solid buy today. The strong balance sheet is simply a bonus.

For further details see:

Matador Resources: Looks Like A Very Solid Buy After Q4 Earnings