PXD - Matador Resources: Strong Finances And Production Growth Make A Compelling Value

Summary

- Matador Resources Company is an independent E&P that mostly operates in the incredibly wealthy Permian Basin of West Texas.

- The company's reserves are okay, but they are less than peers so the company can stand some improvement here.

- Matador Resources is one of the few independents that is growing its production, which could help it overcome the impacts of near-term WTI declines.

- The company has improved its balance sheet considerably over the past two years, and it now boasts one of the strongest in the industry.

- Matador Resources Company is trading for a compelling valuation today.

Matador Resources Company ( MTDR ) is an independent crude oil and natural gas exploration and production company that operates in the wealthy Permian Basin of West Texas. The traditional energy sector in general was by far the best-performing one in 2022, but it has lost some of its shine in the face of the declining prices for energy that we have seen over the past month or two. With that said, though, Matador Resources is still up an impressive 40.00% over the past year, so it has outperformed many other things in the market.

Despite this stunning recent performance, the company still continues to have a very attractive valuation and as such may be worth buying today. Matador Resources has also been making a great deal of progress in reducing its debt, which was one of the biggest problems facing the company back during the pandemic. Matador Resources is also one of the few independent producers that are actually increasing its output, which should help offset some of the impacts of declining energy prices. The long-term fundamentals for crude oil and natural gas prices are still very positive, though, and when combined with Matador Resources’ very attractive valuation, the stock looks very much like a buy today.

About Matador Resources Company

As stated in the introduction, Matador Resources Company is an independent crude oil and natural gas exploration and production company that operates in the wealthy Permian Basin of West Texas. The company also has some operations in the surrounding basins. As of September 30, 2022, the company owned 124,800 net acres in the Permian Basin, 25,100 net acres in the Eagle Ford Shale, and 17,700 net acres in the Haynesville Shale:

{kind=link}

The Delaware Basin shown in the map above is one of the two major basins of the Permian Basin (the Midland is the other). This is an area that will undoubtedly be familiar to most readers that have been following the American energy industry for any period of time since it has been the focal point of America’s energy renaissance over the past decade. This is largely due to the fact that the Permian Basin is generally considered to be the second-largest hydrocarbon deposit in the world.

In fact, according to the U.S. Energy Information Administration , the Permian Basin contained proved reserves of five billion barrels of crude oil and nineteen trillion cubic feet of natural gas despite the fact that it has been exploited since the 1920s. That estimate was also of economically recoverable resources at 2018 prices, so we can assume that its reserves are even higher now since both crude oil and natural gas prices are significantly higher. The fact that this basin is the largest presence in Matador Resources’ portfolio provides the company with a few benefits.

One of the biggest benefits of this resource wealth is the incredible reserves that the company possesses. An energy company’s reserves are critically important, although they are frequently overlooked by investors. This is because the production of crude oil and natural gas is an extractive process. The companies in the energy industry literally obtain their products by pulling them out of reservoirs in the ground. As these reservoirs contain only a finite quantity of resources, companies must continually discover or otherwise acquire new sources of crude oil and natural gas or they will eventually run out of products to sell. As this is by no means guaranteed, the company’s reserves dictate how long it can continue to operate without success at this task.

As of December 31, 2021 (the most recent date for which data is currently available), Matador Resources had proved reserves of 323.4 million barrels of oil equivalents. During the most recent quarter, the company produced 105,200 barrels of oil equivalents per day so its reserves are sufficient to last for just under eight and a half years. This is a bit less than we really want to see as most of the majors have about ten years of reserve life and many of the best independents have twelve or more years. The company will likely release an updated summary of its reserves in about a month so we will want to examine that closely to see if Matador Resources is having any success at improving this figure.

One other advantage that the company’s reserves provide is the ability to grow production without needing to acquire new acreage. This is because the company simply has to drill more or drill more productively on the acreage that it already has. Matador Resources has been focused on this over the past few years. The company has guided to produce a total of 38 million barrels of oil equivalents in 2022, which is an increase over the levels that it had in previous years:

Matador Resources

As we can see, the company increased its production guidance during the most recent quarter. This is because its third-quarter production level came in 4% over guidance and the company expects to be able to maintain this higher performance over the remainder of the year. We will find out if it is successful when it announces its fourth quarter 2022 results, which should be in a few weeks.

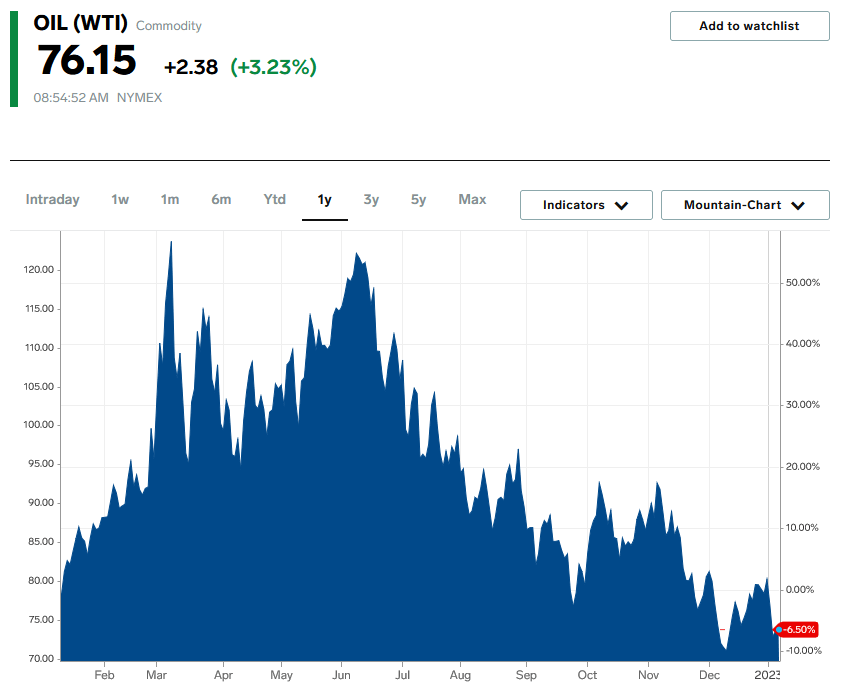

The fact that the company is increasing its production sets it apart from some of its peers such as Diamondback Energy ( FANG ) and Pioneer Natural Resources ( PXD ), as both of those companies are generally holding production steady. The fact that the company is growing its production is somewhat nice to see though as this is one of the only ways that an energy company can grow its cash flows. After all, higher production translates into more products to sell and thus generate revenue. This can be attractive because energy prices do not always move in a favorable direction for these companies. As we can see here, West Texas Intermediate crude oil has generally been declining since June and is actually down 6.05% over the trailing twelve-month period:

{kind=link}

The higher revenue that Matador Resources will generate from a greater production level partially offsets some of the impacts of the fact that it has fewer products to sell. With that said, Matador Resources does enjoy some protection against energy price declines due to its hedging strategy. It is hardly alone in this as most energy companies utilize some form of a hedging strategy. In effect, what the company is doing is using derivatives such as forward and futures contracts to lock in a selling price for the crude oil and natural gas that it produces.

Matador Resources does not actually disclose exactly how its hedges are structured but it sold its oil at an average price of $91.69 per barrel due to its hedges in the third quarter of 2022 so we can assume that the selling price under them is likely in the $80-$90 range since that $91.69 per barrel is actually a bit less than the $94.36 per barrel price that the company would have received in the absence of the hedges. Thus, we can conclude that the recent decline in crude oil prices will not have a significant impact on the company’s cash flow in the near term, although it might if the price decline lasts for more than a few quarters. That is a very possible scenario if the country enters into a recession, which is widely expected to occur in 2023.

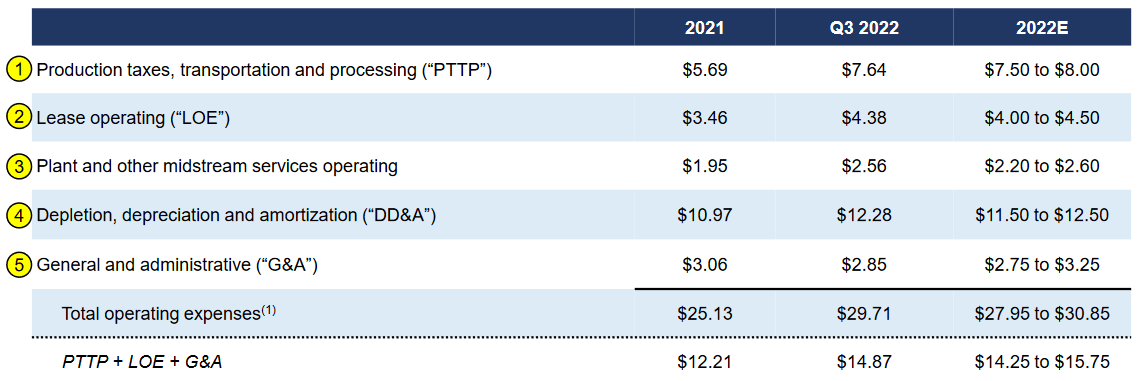

Fortunately, Matador Resources will be able to remain profitable even if energy prices decline further from today’s levels. This is because the high quality of the company’s acreage allows it to produce very cheaply. As we can see here, the company’s breakeven production costs were $14.87 per barrel in the third quarter of 2022:

{kind=link}

This is up a bit from 2021 but that is not exactly surprising. Energy companies were affected by inflation during 2022 just like everybody else. In particular, the price of both steel and diesel fuel was higher than in the previous year and both of these components are necessary for drilling a well. The takeaway though is that energy prices can decline substantially and Matador Resources will still be able to generate cash flow. This is very nice to see and should provide a great deal of comfort to investors, particularly as energy prices usually decline during a recession.

Fundamentals Of Crude Oil And Natural Gas

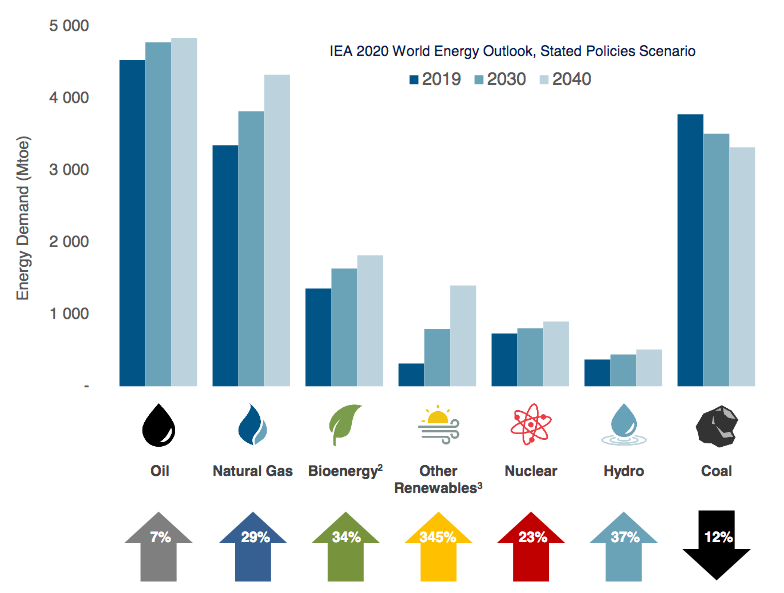

As I have mentioned a few times over the course of this article, the long-term fundamentals for both crude oil and natural gas point to higher prices, although each of these resources will likely see a decline should the economy enter into a recession during 2023. The biggest reason for the long-term price increase is that demand for both resources is likely to rise more than their supply. This is something that may prove surprising to many readers considering that politicians have been promoting the idea that fossil fuels will soon be going the way of the dinosaurs. However, according to the International Energy Agency, the global demand for crude oil will increase by 7% and the global demand for natural gas will increase by 29% over the next twenty years:

{kind=link}

Perhaps surprisingly, it is environmental concerns that will drive the growth in natural gas demand. As everyone reading this is no doubt well aware, concerns about climate change have led governments all around the world to impose a variety of incentives and mandates that are intended to reduce the carbon emissions of their respective nations. One of the most common strategies being employed is to encourage utilities to retire old coal-fired power plants and replace them with renewables. However, renewables suffer from a lack of reliability. After all, solar power does not work when the sun is not shining and wind power does not work when the air is still, or ironically when it is blowing too quickly.

A common solution to this problem is to supplement renewables with natural gas generation capacity since natural gas is reliable enough to ensure the “always-on” capacity that people expect from a modern electric grid and burns cleaner than any other fossil fuel. This is one reason why natural gas is frequently referred to as a “transitional fuel,” as it provides a means to maintain modern life while reducing carbon emissions until such time as we have better technology.

The demand growth for crude oil is likely to be somewhat more difficult to understand. After all, governments in many developed nations have been actively attempting to reduce the consumption of crude oil within their borders. However, it is a very different story in the various emerging markets around the world. These nations are expected to see tremendous economic growth during the projection period, which will naturally have the effect of lifting the citizens of those nations out of poverty and putting them securely into the middle class.

These newly middle-class people will naturally begin to desire a lifestyle that is much closer to that of the developed nations than their lifestyles today. This will require the growing consumption of energy, including energy derived from crude oil. As the populations of these nations substantially exceed those of the developed nations, the growing crude oil consumption from these nations will more than offset the stagnant-to-declining production in the world’s developed markets.

Unfortunately, it does not appear that energy production will grow sufficiently to keep up with this demand growth. One reason for this is that upstream oil and gas producers have been underinvesting in capacity since the energy price crisis of 2015. This is one reason why the offshore drilling industry never recovered from that event. According to Moody’s , the energy industry must immediately increase upstream spending by $542 billion in order to avoid a supply shock.

It seems highly unlikely that the industry will increase its spending by anywhere close to this figure. After all, the industry currently has to deal with politicians and activists demanding that it improve the sustainability of its operations. In addition, investors have been demanding higher returns from these companies. There is even an effort being driven by certain asset managers and banks to deprive the industry of capital investment due to it not meeting certain “environmental” credentials.

I have already pointed out that several companies in the industry are opting to forgo any production increase and simply return capital to their investors. This all points to a situation in which the demand for energy is likely to grow much more than the supply. The laws of economics tell us that such a scenario should result in rising prices. It should be fairly easy to see how rising energy prices should benefit Matador Resources and its stockholders going forward.

Financial Considerations

It is always important to look at the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This repayment is usually accomplished by issuing new debt to pay off the maturing debt, which can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market.

In addition, a company needs to make regular payments on its debt if it is to remain solvent. Thus, an event that causes a decline in cash flow can push a company into financial distress if it has too much debt. This second point can be an especially big concern in the upstream energy space due to the impact that volatile crude oil and gas prices can have on a company’s cash flow.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. In addition, it tells us how well a company’s equity can cover its debt obligations in the event of a liquidation or bankruptcy event, which is arguably more important.

As of September 30, 2022, Matador Resources had a net debt of $807.8 million compared to $3.0656 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 0.26, which is fairly reasonable. Here is how that compares to the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| Matador Resources Company |

| 0.26 |

| Pioneer Natural Resources |

| 0.16 |

| Diamondback Energy |

| 0.38 |

| Coterra Energy ( CTRA ) |

| 0.15 |

| Devon Energy ( DVN ) |

| 0.51 |

As we can see, Matador Resources’ financial structure is generally in line with its major independent peers. This is a sign that the company is not likely relying on too much debt to finance its operations and as such, its leverage should not pose any outsized risk.

Ultimately, though, a company’s ability to carry its debt is more important than its financial structure. The usual way that we judge a company’s ability to carry its debt is by looking at its leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us the number of years that it would take the company to completely repay its debt if it were to devote all of its pre-tax income to that task.

During the third quarter of 2022, Matador Resources reported an adjusted EBITDA of $539.7 million, which works out to $2.1516 billion on an annualized basis. This gives the company a leverage ratio of 0.38, which is very reasonable. This is also far below the 2.8x leverage ratio that Matador Resources had back in the third quarter of 2020 so we can clearly see that the company has been making a great deal of progress in reducing its debt. As I have pointed out in numerous previous articles, most of the best-financed independents have a leverage ratio of less than 1.0x so Matador Resources clearly fits into this category. Overall, the company should have minimal trouble with its debt. This is not something that investors really have to worry about.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a sub-optimal return on that asset. In the case of an independent exploration and production company like Matador Resources, one metric that we can use to value it is the forward price-to-earnings ratio. This ratio tells us how much we have to pay today for each dollar of earnings that the company is expected to generate over the next year. As such, a lower ratio generally indicates a better value.

According to Zacks Investment Resources , Matador Resources has a forward price-to-earnings ratio of 5.88 based on the company’s forward earnings estimates. This is substantially lower than the 18.93 forward price-to-earnings ratio of the S&P 500 Index ( SP500 ). However, as I have pointed out in many previous articles, the entire energy sector has looked incredibly undervalued for quite some time now. Therefore, it makes some sense to compare Matador Resources’ ratio to its peers:

| Company |

| Forward P/E |

| Matador Resources |

| 5.88 |

| Pioneer Natural Resources |

| 9.01 |

| Diamondback Energy |

| 5.53 |

| Coterra Energy |

| 5.71 |

| Devon Energy |

| 6.94 |

As we can see, Matador Resources is generally in line with its peers so it is not really presenting an especially attractive valuation relative to its energy sector peers. However, the company is clearly very attractive relative to pretty much anything else in the S&P 500 Index and the stock’s valuation is still very reasonable. The reason why it does not appear especially compelling in this comparison is simply that the entire sector is ridiculously undervalued. Matador Resources looks very much like a buy today.

Conclusion

In conclusion, there are a lot of reasons to like Matador Resources Company today. It is one of the few independent energy companies that is actively growing its production, which should help it offset some of the impacts of the recent decline in energy prices. Matador Resources has also significantly improved its balance sheet over the past two years and it now has one of the most attractive financial positions in the industry. Matador Resources Company is also offering a very compelling valuation relative to the S&P 500 Index, so it could certainly be worth buying today.

For further details see:

Matador Resources: Strong Finances And Production Growth Make A Compelling Value