MTRN - Materion Corporation: Demand Is There And Investor Value Too

2023-06-05 04:20:49 ET

Summary

- Materion Corporation, a company in the advanced materials industry, has seen strong demand for its products and raised its guidance for 2023, with EPS expected to be between $5.6 and $6.

- The company has diverse end markets, with the semiconductor industry being the most significant, and is expected to outperform the market due to its ability to improve margins and establish partnerships.

- Materion's valuation appears fair, and its diversification across various industries offers investors a lower risk of volatile earnings results, making it a solid buy for diversified exposure to growing markets.

Investment Summary

Materion Corporation ( MTRN ) is a well-established company in the advanced materials industry. The company offers a diverse range of high-performance materials and services to cater to the needs of various industries. Their portfolio includes engineered materials, precision parts, thin film coatings, and beryllium products.

End Markets (Investor Presentation)

{kind=link}

With a large number of different end markets the company has seen strong demand so far for their products and the company even raised its guidance for 2023 which is impressive as we are still in a pretty difficult market environment. EPS is expected to come in between $5.6 and $6 for 2023. With a quite fair p/e of around 18 and solid FCF generated I see the company offering little risk here as an investment. With the semiconductor industry making up around 30% of the sales I see MTRN gaining a lot of momentum from this industry and keeping up the trend of growing sales in the double digits as they have for the last 9 quarters.

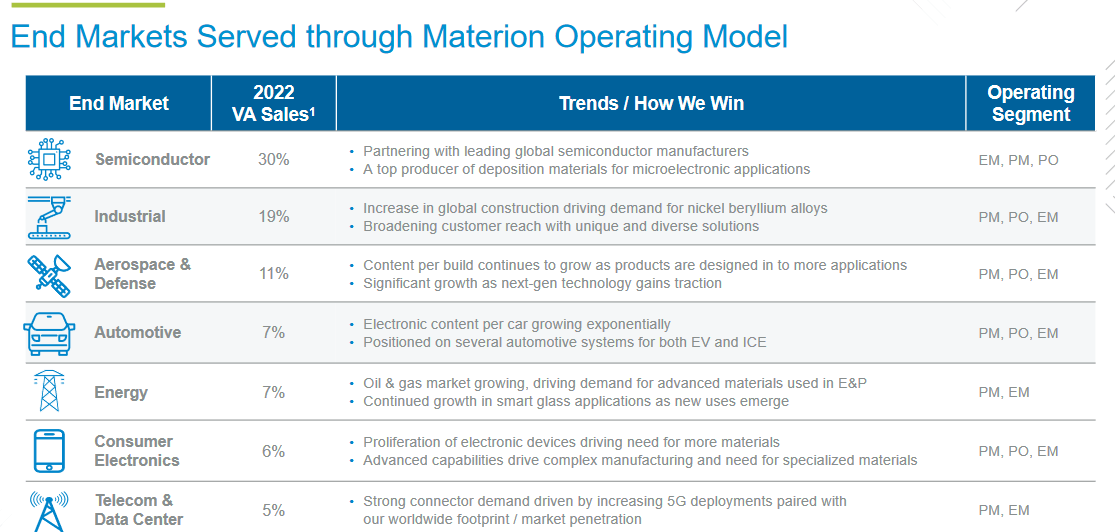

Diverse End Markets Create Demand

As I mentioned before, MTRN has a very diverse set of end markets that they are exposed to, but perhaps the most significant one is the semiconductor industry, where the company generates around 30% of its sales in 2022.

End Markets (Investor Presentation)

{kind=link}

The company has a history of entering into important partnerships to help boost its position in its selective markets. The semiconductor industry might have faced some short-term cyclical challenges but the outlook for that industry remains very strong. Demand for the semiconductor industry is expected to come from the automotive sector expected to be responsible for around 20% of the demand. This is a market that MTRN then has both direct and indirect exposure to. They serve the market directly as they supply material to manufacturers but also gain demand through the semiconductor industry too. I think this conclusion in MTRN has a very solid outlook and the ability to grow revenues like they have and also begin improving margins too.

Market Outlook (PrecedenceResearch)

{kind=link}

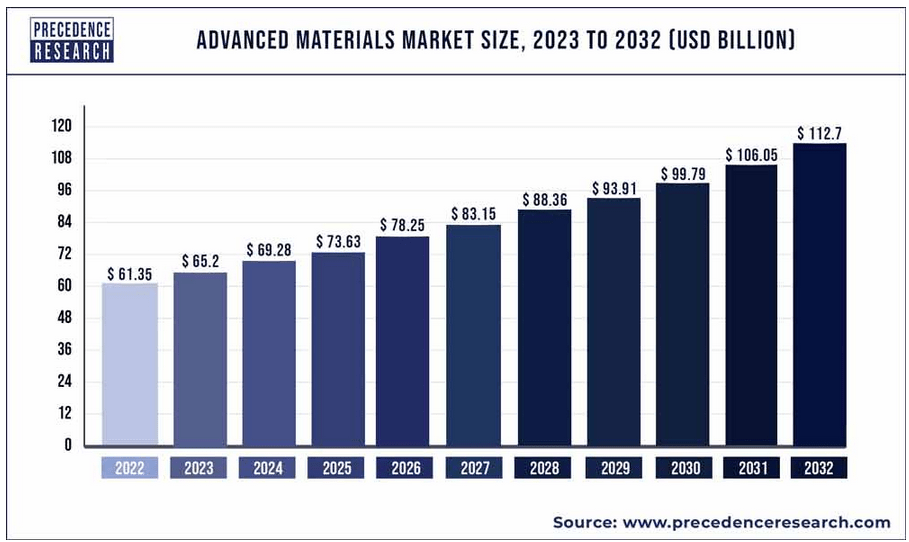

Looking at the advanced materials market size estimates are around a 6.27% CAGR from 2022 to 2032. I think MTRN will be able to outperform the market given their track record of doing so, but also because they have room to improve margins, which would greatly boost the EPS of the company in my view. Reasons for the increase in margins could be because of MTRN's ability to establish partnerships and secure deliveries, making inventories leaner and more efficient in the long run. History also shows the company has been able to raise the bottom line margins whilst growing revenues, and given the solid outlook I think it's reasonable to expect the margins to continue improving from here. Margin improvement may have happened during years of very high demand, but they seem robust and have stayed despite the short-term challenges the semiconductor industry faced which meant a softer pricing environment.

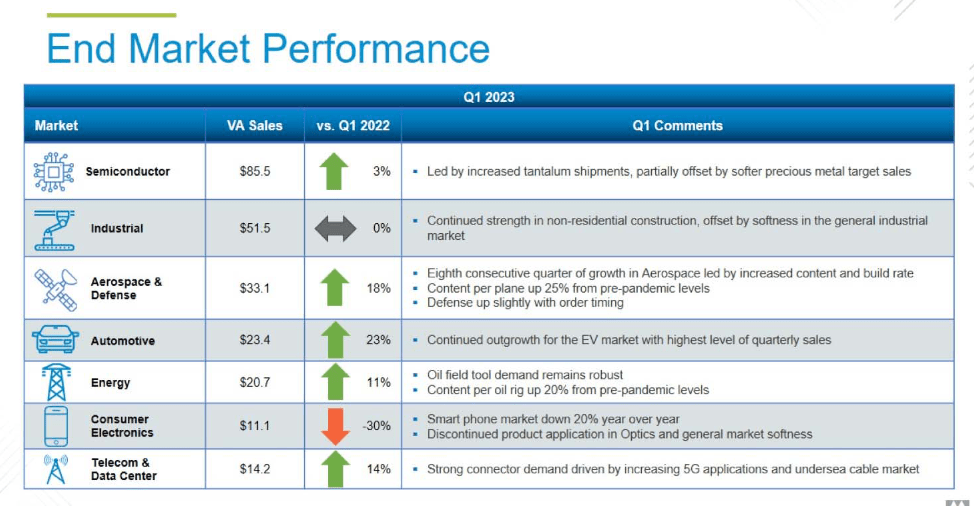

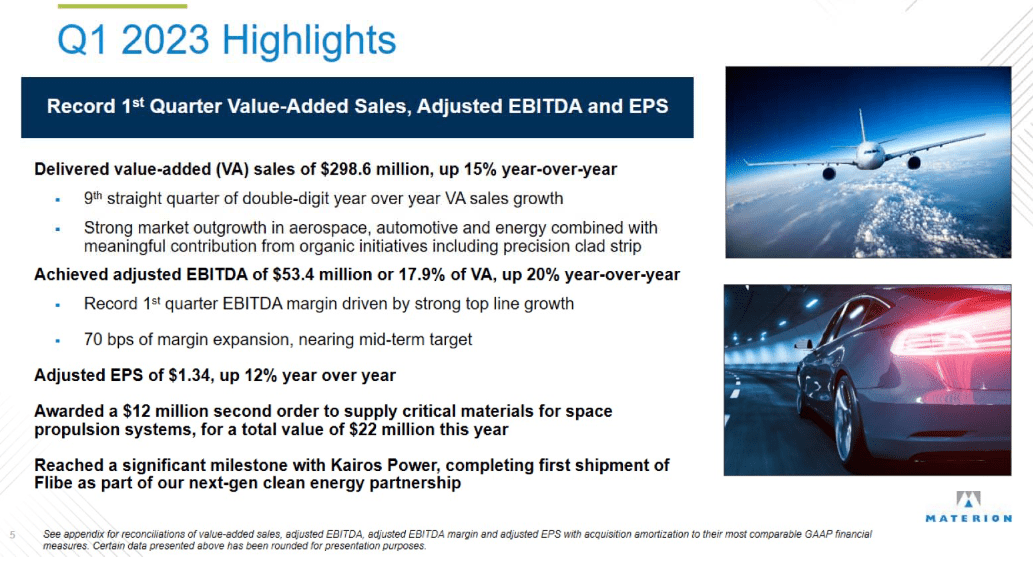

Quarterly Result

Looking at the first quarter of 2023 for the company they had another solid result in my opinion. This view seems to have been shared with the CEO Jugal Vijayvargiya too saying the following, "Despite a challenging end-market environment, we delivered a ninth consecutive quarter of double-digit organic growth, demonstrating the continued power of our outgrowth initiatives". This solid performance does justify the valuation the company is trading at in my opinion. Having the ability to grow margins despite challenges and make significant partnerships I think creates the buy case around this company. The partnership with Kairos Power and MTRN completing the first shipment to is great news.

{kind=link}

The partnership is an exciting opportunity as MTRN now gets exposure to the nuclear sector, a market I think will prove vital in our adoption towards renewables.

Looking at the bottom line however for the company they continued to impress. MTRN achieved their mid target of a 70 bps improvement in margin expansion and this helped them achieve an EPS of $1.34 for the quarter. Going into the coming quarters looking at the margins and the improvements of them will be key in my opinion. The company noted they are taking cost-cutting measures to help counter the softer demand some markets are facing. Seeing whether or not these measures have any impact I think will be interesting. It would help indicate whether or not the full-year EPS of $5.6 - $6 is achievable or not.

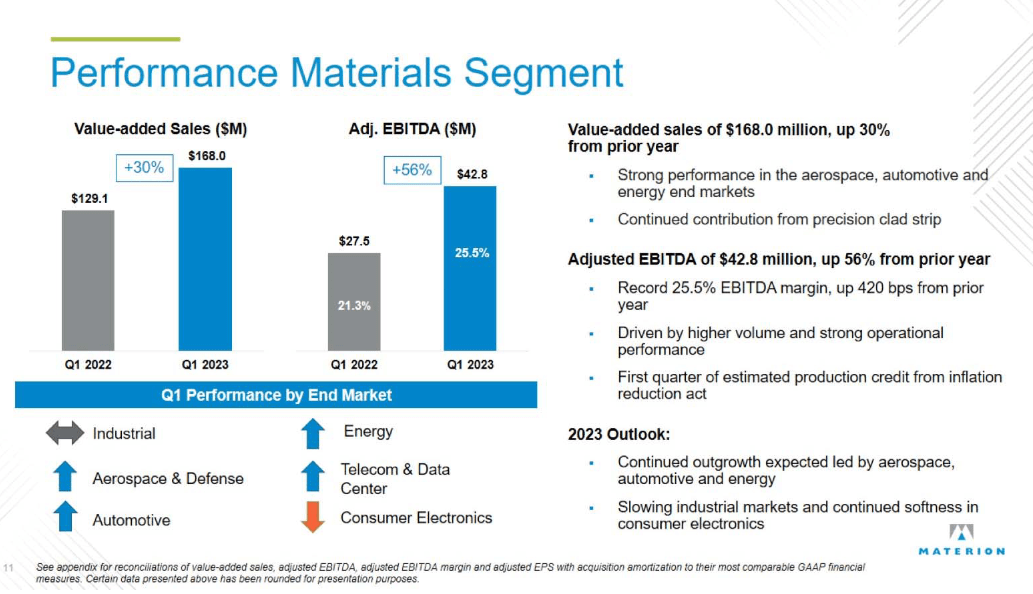

Performance Segment (Q1 Report)

{kind=link}

One of the fastest growing segments of the business is the Performance Materials segment seeing a large jump in the margins, reaching a record 25.5%, up 420 bps from the year prior. Being the largest segment of the company this is where a lot of my attention will be for the next report. I would like to see a further improvement in margins which hopefully should be possible as the company noted several end markets showing demand here, like the automotive and energy industries for example.

Risks

One of the slight risks of the company is perhaps the debt they hold. The net debt/EBITDA ratio comes out at around 2.2 right now and if there is a slowdown or a softer pricing environment in the industries that MTRN sells to, then I can see this number increasing as EBITDA would likely dip down. This would increase the likelihood of MTRN starting to dilute shares in order to raise capital. In the past, they have done this to a small extent.

{kind=link}

So far though the company is able to pay off its long-term debt and in the TTM they paid off about $31 million. 2 years ago I would have been worried about the margins in the company, but they have come a long way and are still seeming to climb. They aren't fantastic with the gross margins being around 21% right now, below the sector. I think the cost-cutting measures the company is taking should hopefully have some form of impact on them to the upside, but if not then I would be concerned.

Valuation & Wrap Up

Looking at the valuation of MTRN right now they seem to be quite fairly valued in my opinion around 18x forward warnings. As a company able to grow sales double digits consistently they have proven themselves worthy or trading above the sector's average I think. The company does have a small dividend yield right now of around 0.48% and I think they will be able to maintain this with their current levered FCF of $67 million , which have grown exceptionally over the last few years as a result of MTRN growing sales and improving their margins.

{kind=link}

Right now I think MTRN offers investors a great opportunity to get exposure to a variety of different end markets and benefit from the demand they are seeing as opposed to making a pure investment into any of them. This vast diversification of markets also places less risk of volatile earnings results in my opinion. Even though semiconductor industry sales make up around 30%, a decrease here is backed up by stability in industries like energy or automotive instead. I think MTRN is on a solid path to bring value to investors right now. They have a solid balance sheet where the debts are manageable by the cash flows they are generating and the coming quarters should bring further margin improvements as MTRN implements their cost-cutting measures. For now, MTRN will be a buy from me and a great way to get diversified exposure to many growing markets.

For further details see:

Materion Corporation: Demand Is There And Investor Value Too