MTRN - Materion: New Advanced Materials Could Bring Significant FCF Growth

2023-09-10 05:02:53 ET

Summary

- Materion Corporation has a diversified business model and a strong track record in advanced engineered materials.

- The company is well-positioned in key markets such as semiconductors and industrial, with potential for significant net sales growth.

- Despite risks and competition, the stock appears undervalued and has potential for further growth.

Materion Corporation (MTRN) reports a strong track record and focus on advanced engineered materials. In addition, the business model is quite diversified. In my view, with more new innovative materials from R&D efforts and operating efficiency improvements, we may see further FCF growth in the coming years. Additionally, even considering risks from restructuring failures, the total amount of debt, or intense competition, the stock appears quite undervalued.

Materion Corporation: Diversified Business Model And 10% Expected 2023 EPS Growth

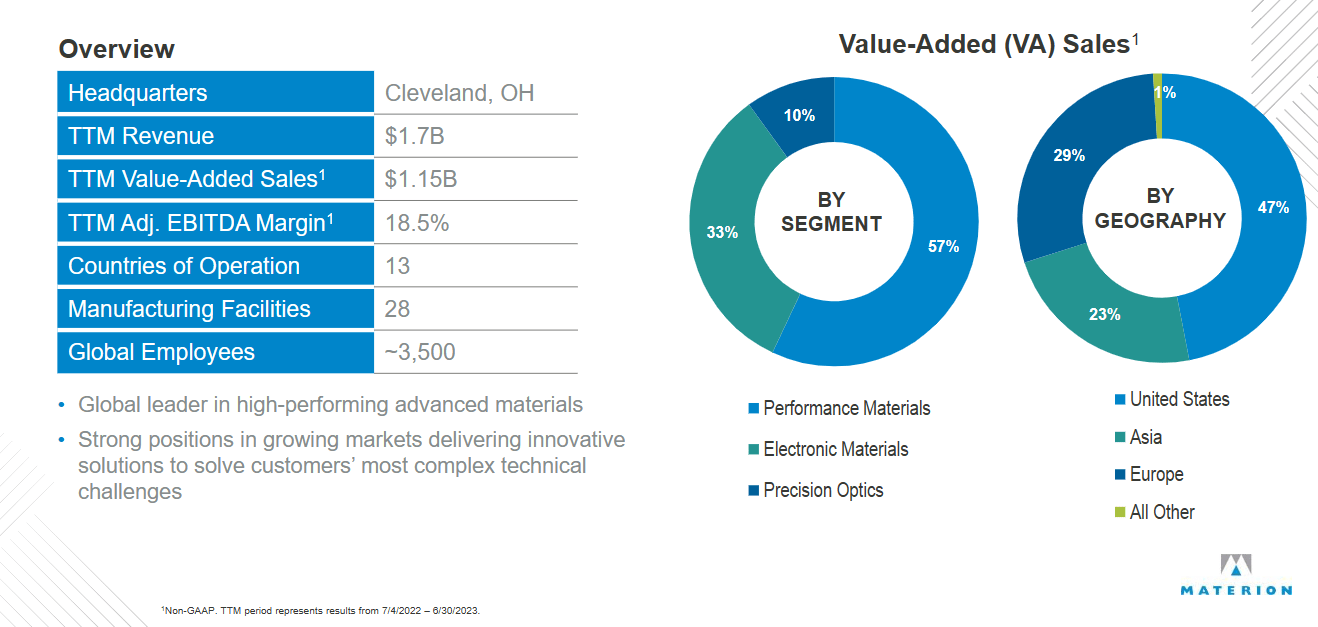

Materion Corporation, a leading advanced engineering materials company, has a strong track record since its founding in Ohio in 1931. It offers a broad range of high-performance products, spanning electrical, electronic, thermal, and structural products. Its end markets include semiconductors, industrial, aerospace, automotive, energy, consumer electronics, data centers, and telecommunications. Its continuous innovation and quality of products position it as a trusted choice for various industries, supporting technological progress and excellence at all times.

{kind=link}

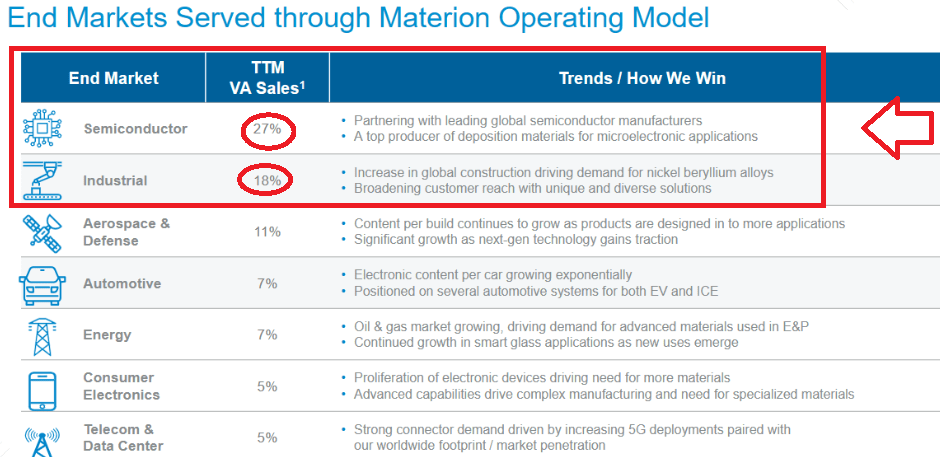

In my view, it is quite impressive that Materion Corporation successfully adapts its products to the latest technological trends, maintaining its position as a leader in key markets. With that, in this regard, I believe that the most relevant markets are the semiconductor market and industrial market. In these particular target markets, Materion Corporation could receive significant net sales growth from new partnerships with semiconductor manufacturers and the increase in global construction driving demand for nickel alloys.

{kind=link}

The recent information reported in the last quarterly report about an incoming market recovery driven by strong organic pipeline is worth noting. Besides, management noted that it has identified several growth opportunities, 2023 capital expenditures of about $95 million with an effective tax rate of 17%-18%, and optimistic 2023 EPS growth of about 10%. I included some of these figures in my models.

Source: Quarterly Presentation Source: Quarterly Presentation

Balance Sheet

In June 2023, Materion Corporation reported cash and cash equivalents worth $16 million, with accounts receivable close to $189 million, inventories of $455 million, and prepaid and other current assets of about $37 million. Total current assets stood at $697 million, and the current ratio is larger than 1x. Thus, I am not really concerned about the total amount of liquidity. With net property, plant, and equipment worth $493 million and intangible assets worth $137 million, goodwill stood at $320 million with total assets of about $1.737 billion.

Source: 10-Q

I believe that the list of liabilities may be studied in detail as the total amount of debt is not small. The company noted short-term debt worth $27 million, with accounts payable of about $123 million, salaries and wages close to $21 million, and total current liabilities of close to $233 million. Besides, with finance lease liabilities of $13 million and retirement and post-employment benefits worth $20 million, long-term debt stood at $412 million. The asset/liability ratio is larger than 1x, so I would say that the balance sheet is stable.

Source: 10-Q

Contractual Obligations Do Not Seem Worrying, But Investors May Want To Have A Look At Them

In 2021, Materion Corporation made modifications to its credit agreement, expanding its revolving credit facility from $375 million to $675 million, including a $300 million delayed draw loan facility. The term of the agreement was extended to 2026, and an uncommitted incremental credit facility of up to $150 million was allowed.

In November 2021, the company used $300 million to acquire HCS-Electronic Materials. In January 2023, it switched from LIBOR to SOFR, and increased the limit on its precious metal lines to $615 million. The company pays a variable commitment fee based on the unborrowed amounts of the line of credit. With regards to future payments, the most relevant payment is expected to be around 2026. Hence, I do not think that investors may have to worry in 2024 and 2025 about negotiations with debt holders.

{kind=link}

High-quality Products And Further Diversification Will Most Likely Lead to Lower Net Sales Volatility

I believe that Materion Corporation stands out as an industry leader, committed to delivering high-quality products and innovative solutions that drive technological progress for its customers. Its extensive portfolio ranges from precious and non-precious metals to powders, inorganic chemicals, specialty coatings, beryllium and copper alloys, beryllium compounds, ceramics, and coated metal systems. In my view, further diversification of the products offered will most likely reduce net sales volatility.

I Assumed That Restructuring Initiatives Would Not Fail

I usually dislike investing in companies that are conducting restructuring activities because you do not really know how it is going to turn. With that, Materion Corporation has significant expertise, and has run activities for many decades. I trust that management will likely enhance operational efficiency. As a result, we may see FCF improvements.

During 2023, the Company implemented various restructuring initiatives across the Performance Materials, Electronic Materials and Precision Optics segments to improve operational efficiency. This resulted in severance and related costs of approximately $1.5 million and $2.1 million during the three months and six months ended June 30, 2023, respectively. Source: 10-Q

In the first six months of 2022, Company recorded a combined total of $1.1 million of restructuring charges in our Precision Optics, Electronic Materials and Other segments as a result of cost reduction actions taken in order to reduce our fixed cost structure. Source: 10-Q

Inflation Reduction Act of 2022 And Other Tax Rules Could Have Further Beneficial Effect On Future FCF Growth

I would also expect further benefits from the Inflation Reduction Act of 2022, which management mentioned in the last quarter report. In my view, if management identifies further production credit from the Internal Revenue Service and U.S. Treasury Department, more investors will most likely have a look at the FCF expectations of Materion Corporation.

The IRA affords the Company eligibility to a production credit beginning in 2023, for which the Company expects to recognize cash savings. The issuance of guidance and interpretation as to the eligibility for, calculation of, and methods for claiming the production credit remain pending. We will continue to monitor developments related to the production credit from the Internal Revenue Service and U.S. Treasury Department and evaluate the potential impact to the Company’s production credit. Source: 10-Q

Product Innovation May Also Bring Further Net Sales Growth

Materion Corporation invests close to 3% of value-added sales in research and development. These initiatives include evaluation and testing of new products as well as new high performing advanced materials. Considering the total amount of dollars invested in research and development, I believe that we may see new innovations, which may lead to further demand for advanced materials.

R&D expense accounted for 3% of value-added sales in the first half of both 2023 and 2022. Source: 10-Q

Cash Flow Expectations

Considering previous net income growth reported in the past, I assumed an average net income close to 16% and median net income growth of about 13%. I believe that my numbers are conservative.

Source: YCharts

{kind=link}

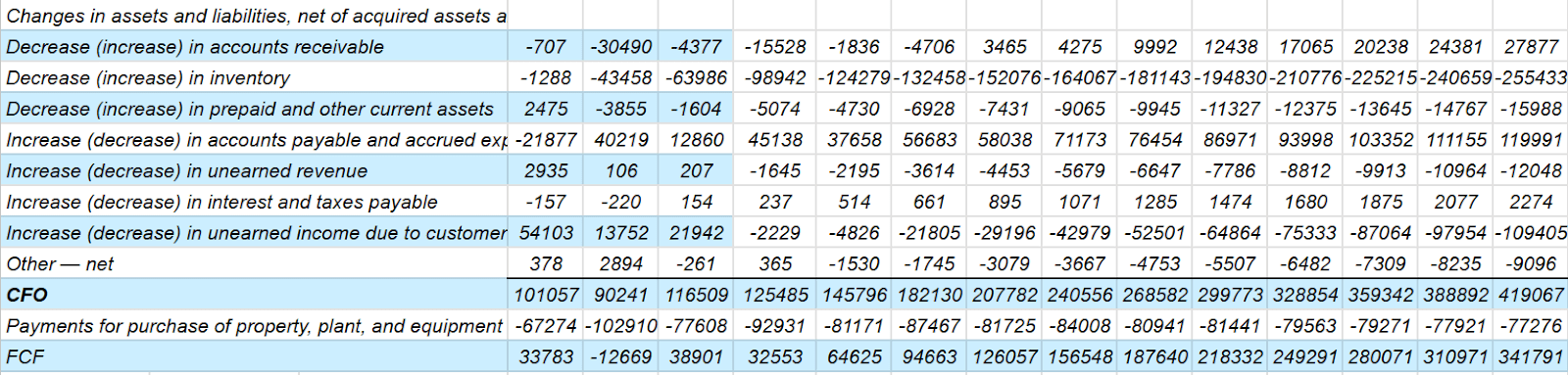

Considering the previous assumptions, I included 2033 net income of about $433 million with the following adjustments to reconcile net income to net cash provided by operating activities. I assumed depreciation, depletion, and amortization of about $121 million, amortization of deferred financing costs in interest expense close to $7 million, stock-based compensation expense of about $28 million, and amortization of pension and post-retirement costs of close to -$2 million.

{kind=link}

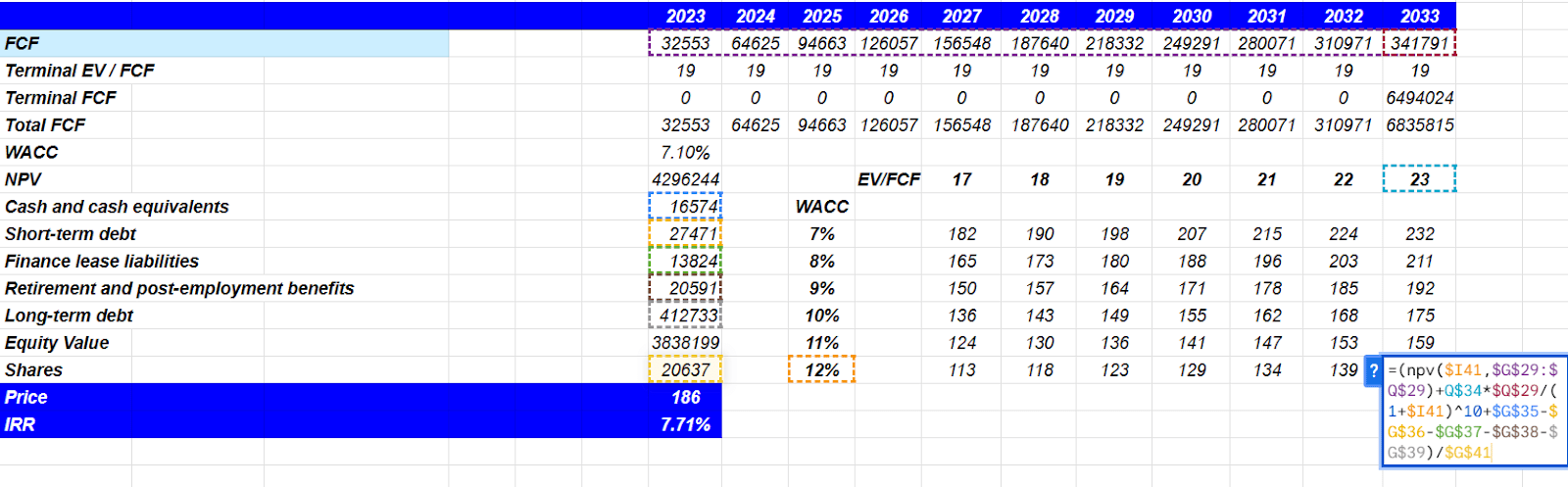

Changes in assets and liabilities, net of acquired assets and liabilities included accounts receivable of about $27 million, with decrease in inventory worth -$256 million and changes in prepaid and other current assets of close to -$16 million. Besides, with accounts payable and accrued expenses of about $119 million and changes in unearned revenue of close to -$13 million, I obtained CFO worth $419 million. Finally, taking into account payments for purchase of property, plant, and equipment of about -$78 million, 2033 FCF would be close to $341 million.

{kind=link}

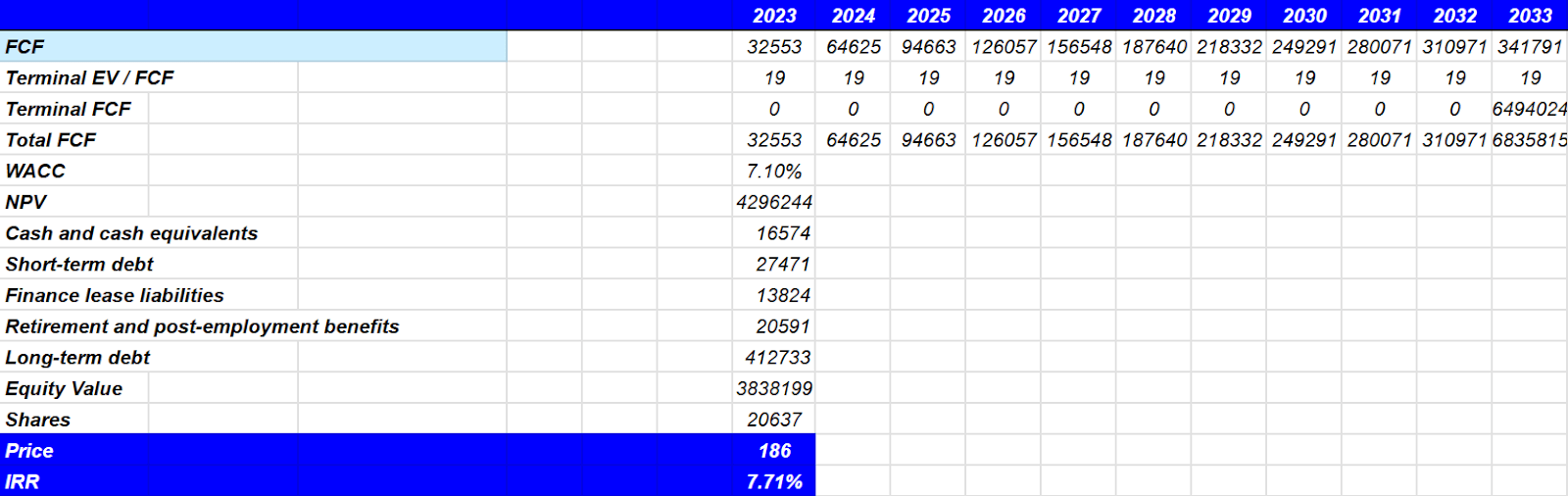

If we assume a terminal EV/FCF of about 19x, the terminal FCF would be about $6494 million. Note that MTRN reports an EV/10 Years Median FCF close to 21x, so my EV/FCF multiple appears reasonable.

Source: YCharts

Besides, with a WACC of 7%, the implied NPV of future FCF would be $4.296 billion. If we also add cash and cash equivalents worth $16 million, and subtract short-term debt of $27 million, finance lease liabilities close to $13 million, retirement and post-employment benefits close to $20 million, and long-term debt worth $412 million, the implied forecasted equity value would stand at $3.838 billion. Finally, the forecasted price would stand at $186 with an IRR of 7%.

{kind=link}

Sensitivity Analysis

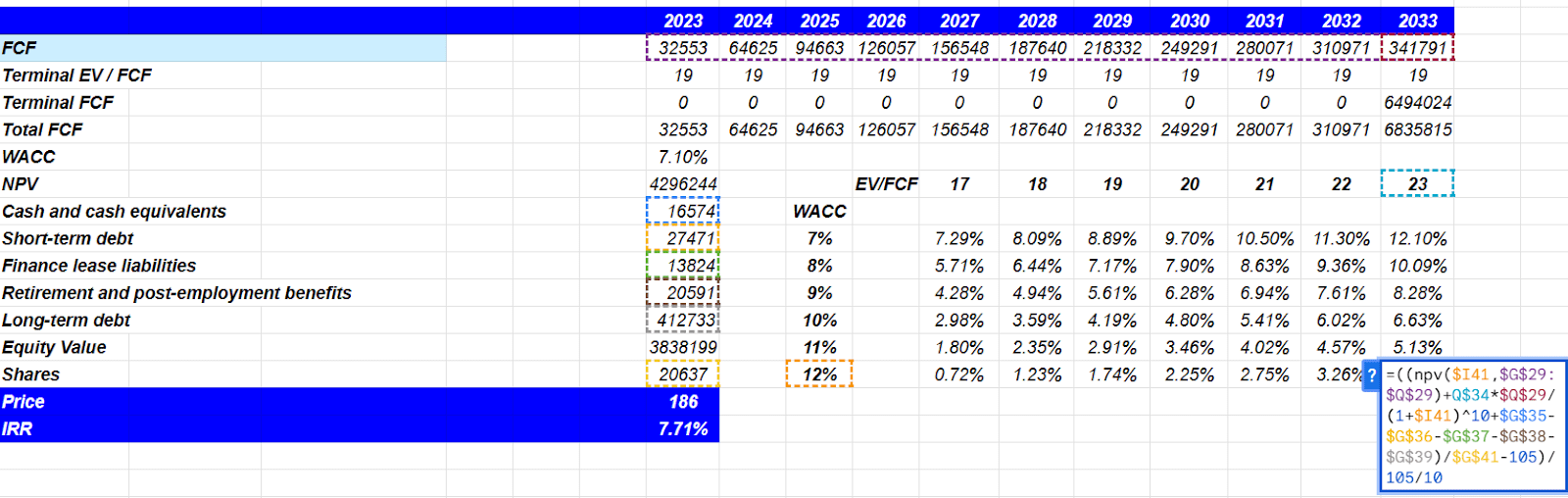

In my view, the results obtained in my model do not seem to change dramatically after changes in the EV/FCF and the WACC. Using a WACC of 7%-12% and EV/FCF of 17x-23x, I obtained a forecast price of close to $113-$232 and positive IRR of 0.72%-12%. With these figures in mind, I think that Materion could trade at a larger stock valuation.

{kind=link}

{kind=link}

Risks And Competitors

Materion Corporation faces significant risks due to the cyclical nature of its end markets. These risks include sensitivity to economic changes, inflation, interest rates, fluctuations in the US dollar, and the health of key industries. Also, in periods of slowdown, customers may temporarily adjust their inventories, negatively impacting Materion. The company must be proactive in managing these risks, and maintain the flexibility to adapt to changing conditions in its end markets to maintain its sustainable success.

The company competes with peers like Honeywell International (HON), Praxair, Solar Applied Materials, Ametek (AME), and others. Besides, Precision Optics (POCI), headquartered in Westford, Massachusetts, manufactures thin film coatings and optical filters, distributing globally. It faces competition from Viavi (VIAV), Coherent (COHR ), MKS Newport Optics, Alluxa, and other providers. Although the company develops new markets and applications, rapid technological evolution and competition can result in the occasional loss of existing applications and customers. Adapting to these challenges is crucial in its highly competitive environment.

My Opinion

In my opinion, Materion Corporation, with a strong track record and focus on advanced engineered materials, appears to be well positioned to meet challenges and seize opportunities in its various end markets. I believe that further diversification of the products offered, new innovative materials from R&D efforts, and further improvement of operating efficiency will most likely accelerate net sales growth. Even taking into account the fact that competition in the industry is intense or risks from the total amount of debt, I believe that there is significant room for stock price improvement.

For further details see:

Materion: New Advanced Materials Could Bring Significant FCF Growth