MATV - Mativ Holdings: Don't Get Your Hopes Up

2023-08-31 11:53:03 ET

Summary

- MATV remains a hold due to negative cash flows and challenged volume levels.

- Investors seeking value should look elsewhere.

- The company's margins have improved, but FCF growth and volume growth are needed for an upgraded rating.

Investment Summary

Back in May, I wrote an article about Mativ Holdings Inc (MATV) as well where I concluded that the price wasn't very fair to pay given the performance of the business and some of the challenges they have faced so far. This view remains and I won't be upgrading my rating for the company either. It remains a hold in my opinion as long as some of the fundamentals of the business are the way they are, like negative cash flows and challenged volume levels as customers continue to destock.

Investors seeking a value play should be looking elsewhere rather than MATV right now. Where MATV may start to look appealing would be when the earnings multiple reflects a discount of around 10 - 15% against the sector. That would in my opinion be considered adequate to make the risk/reward profile reasonable enough for an upgraded rating. In the meantime, I stand by my hold rating for MATV.

A Brief Overview

The company operates in the chemicals industry where it focuses on manufacturing and selling polymer, resin, and fiber-based substrates. The company has divided its operations into two primary segments which are Advanced Technical Materials and Fiber-Based Solutions.

Segment Results (Investor Presentation)

As of the last report, the clear majority of sales is coming from the first segment at around 80%, which has been driven by a diverse set of end market demand through the years and a strong market position in primary products like deep polymer, resin, and various coatings.

Margin Growth (Investor Presentation)

Right now, the priority should be on getting back margins and reclaiming the FCF margin for the business. It has in recent years slipped up on this front a bit and that has me worried. Without proper FCF the company cannot efficiently invest in new pipelines of growth and expansions which mutes girth prospects and in turn the valuation as well, at least in my opinion it should.

Quarterly Result

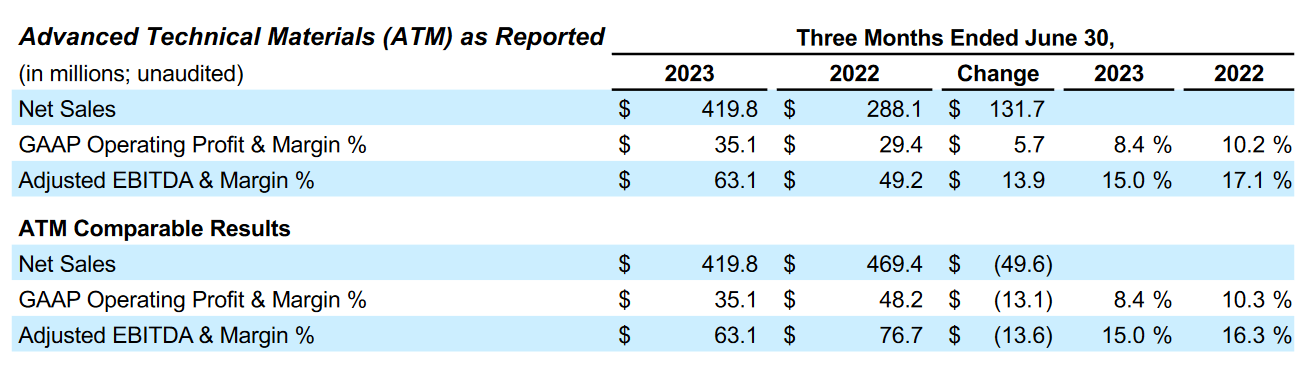

The last quarter, they showcased a solid 56% growth in sales, which came inorganically as the company completed a merger. Looking at the organic sales growth instead, it was far lower at 8% YoY instead. The quarter had some positives and negatives for investors to look at, but unfortunately, not enough incentives to make MATV anything but hold right now. The volumes remained challenged as the management noted customers are continuing to destock investors and that makes demand softer.

{kind=link}

Where there were some shining lights though was the margins for the business. EBITDA margins grew rapidly on a YoY basis to 63.1%, up from 49.2% the year prior. This shift reflects the management's ability to perform well despite higher interest rates and materials expenses increasing.

Risks

Delving into the various risk factors within the company, one of the foremost concerns I've already highlighted is the trajectory of cash flows. A distinct feature that raises eyebrows is the persistently negative cash flows, which are at odds with the management's decision to issue dividends. This approach, in my estimation, appears rather imprudent, as dividends should ideally be sustained by robust and positive cash flows. This fiscal decision potentially raises questions about the company's financial stability and the viability of sustaining dividends in the long run. Such a scenario could pave the way for potential dilution of shares if capital raising becomes necessary.

FCF (Seeking Alpha)

It's crucial to know the backdrop of the broader macroeconomic environment. A key observation is that MATV has acknowledged operating in a challenging macro landscape. Despite this hurdle, the company has exhibited a degree of resilience by deftly passing on some of the cost burdens to consumers. This strategic maneuvering likely played a role in bolstering the company's margins beyond what could have been anticipated otherwise. This implies a degree of adaptability and strategic acumen on the part of the management. As of the last report for example, there was a showcase of sequentially higher margins for the company, despite the low demand and volumes the quarter otherwise had to offer. Margin retention and improvement despite these challenges may be why MATV is rewarded with the valuation it gets, but that isn't to say it makes for a good buy yet.

Financials

The balance sheet of MATV though continues to be a highlight, even though volumes are declining. The cash position sits at over $100 million and is sufficient to cover the current debts of $34 million a few times over.

Liabilities (Earnings Report)

As for the long-term debt, though, this is where the situation does get a little tricky. If MATV isn't able to get back cash flows to where they used to be, I think that paying back debt will be more difficult and leave less capital over for expansions. Back in 2019, the FCF was over $100 million and that left the company with no issues in paying back debts. It seems as though the company is resorting to diluting shares to raise capital now, which of course hurts investors and diminishes the buy case significantly.

Valuation & Wrap-Up

I think that MATV has done somewhat well in the last report, and I have to admit my view on the company is slightly more positive than when I wrote my last article. Nonetheless, I don't think investors should be getting their hopes up too much as FCF remains negative and the dilution of shares continues. Even if the margins are expanding, we need volume growth before MATV could be considered anything else than hold. If MATV can lean more heavily into its smaller segment and drive FCF growth that way, then perhaps we will see the share price rise as a result, but I remain doubtful.

{kind=link}

Without an ample discount rate either, I find the buy case nonexistent currently and that leads me to stay with my hold rating for MATV as previously issued.

For further details see:

Mativ Holdings: Don't Get Your Hopes Up