MATV - Mativ Holdings: Not Quite A Buy Just Yet

2023-05-23 15:10:36 ET

Summary

- Mativ Holdings, Inc. has grown sales exponentially YoY as a result of a merger that happened last year.

- The first quarter of the year had Mativ Holdings, Inc. face many challenges, and I won't make an investment case for the company until there is more clarity, especially the margins.

- The long-term outlook for Mativ Holdings, Inc. does remain positive, however, which makes me want to still rate the shares a hold, as there is value to be had here eventually.

Investment Summary

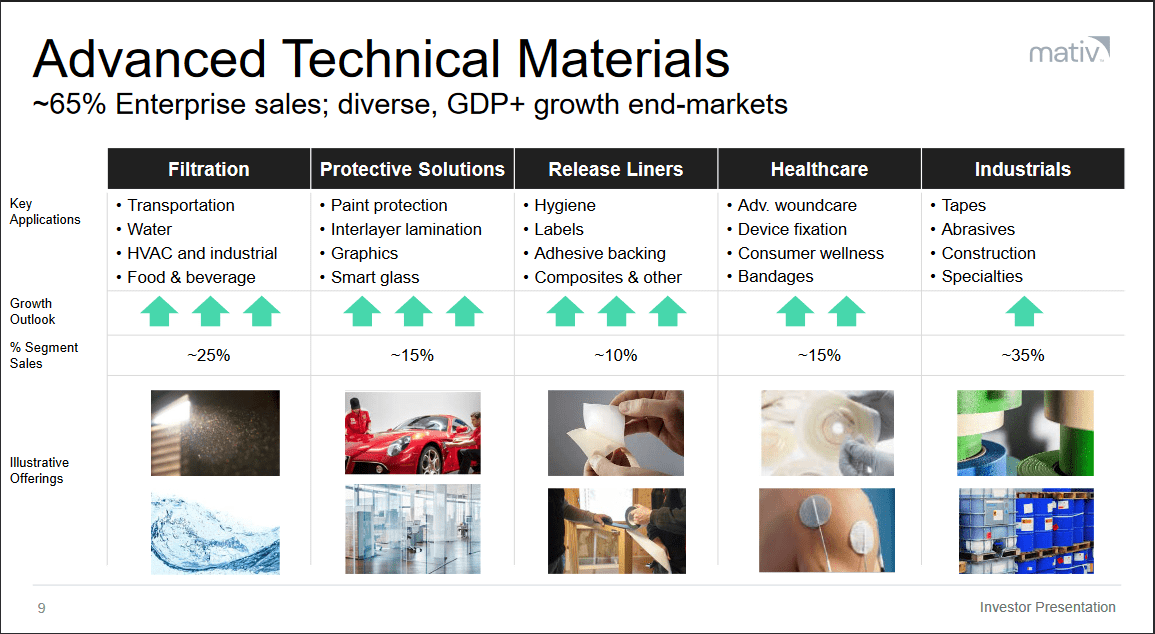

Mativ Holdings, Inc. ( MATV ) is a company specializing in performance materials. In the Advanced Technical Materials segment, the company focuses on producing and distributing a wide range of high-quality polymer, resin, and fiber-based substrates. These substrates serve as the foundation for various applications, including nets, films, adhesive tapes, and other innovative nonwovens.

{kind=link}

Looking at the last report from the company, they have managed to build up plenty of momentum. Sales grew at an impressive 66.9% YoY rate, reaching $679 million, a result of the merger that happened last year. Sales increased by about $680 million compared to the previous year pre-merger.

But besides this, Mativ Holdings, Inc. also noted it was highly able to make price increases to help offset the impacts of higher input costs, showcasing the moat and strong market position the company holds. But the margins still have a way to go before the company looks too good not to invest in given the low forward p/e of around 10. Until I see better margins across the business, I will rate MATV stock a hold.

Quarterly Result

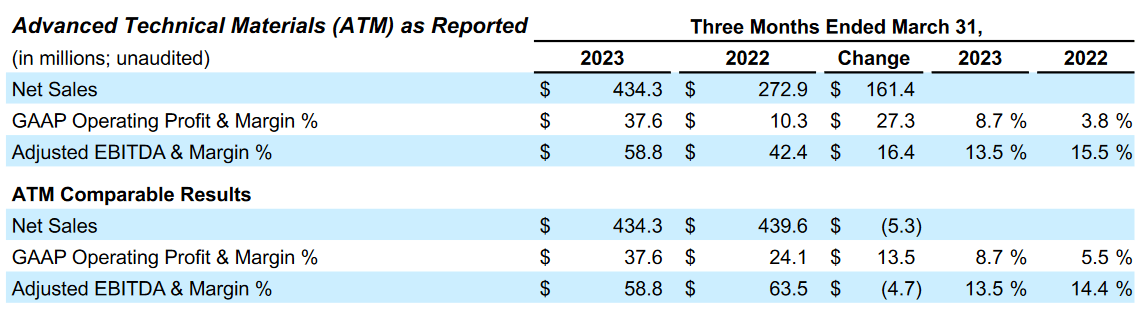

Looking at the last quarter , the company managed to increase sales substantially as a result of the merger that happened last year. Total sales came in at $679 million, and the ATM segment was responsible for a majority of those sales, reaching $434 million. What is slightly worrying, though, with this segment is that the EBITDA margins did take a hit on a YoY basis, going from 14.4% in 2022 to 13.5% in the first quarter of 2023. Perhaps the pricing power the management noted did help to offset some of this loss in margins, but if we experience a softer market, then I fear the margins might dip further as pricing power might be useless in a soft market environment. It should be noted that the result of the ATM segment is a comparison of the results after the merger and before the merger, so 2022 numbers are based on legacy SWM results. But nonetheless, it will be vital to see the development of the margins in this segment.

Earnings Highlights (Earnings Report)

{kind=link}

Looking at the cash flows of the quarter, they were a negative $20.7 million from operating activities. Taking the capital spending and software costs into account, the free cash flows were a negative $39.9 million. The company did say they expect to see stronger cash flows for the remainder of the year, as this result was caused by seasonality. Nonetheless, I fear it could help drive dilution in the coming quarters until MATV manages to get a strong cash flow base to operate with.

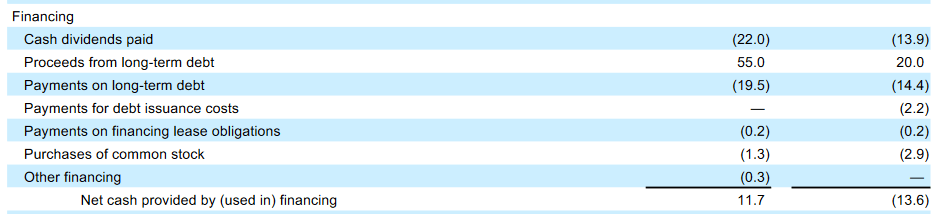

With only $97 million in cash and $1.7 billion in long-term debts, Mativ Holdings, Inc. has a narrow line to walk on financially. But these negative cash flows didn't stop the company from issuing a dividend of $0.4 per share in the last report. I would have much preferred to see this skipped and instead have the management focus on actually building up their margins and having the dividend be funded by cash flows and not what seems to be from the cash position.

Company Outlook (Earnings Report)

{kind=link}

A comment from the CEO Julie Schertell highlights some of the reasons the company might be trading at the valuation it does:

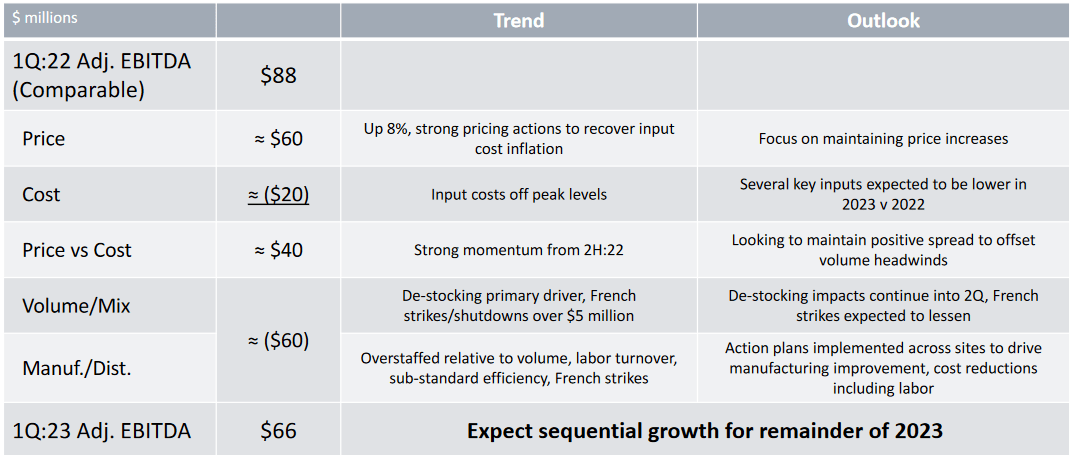

"We continue to navigate an uncertain macro environment, focusing our efforts on internal actions we can control and working to mitigate external factors. While the first quarter was particularly difficult, we anticipate delivering significantly improved sequential EBITDA for the remainder of the year."

There is uncertainty about the margins, and thus you do not get a premium valuation for the company. I think the coming quarters will be crucial in the way EBITDA develops. If Mativ Holdings, Inc. fails on its projection here that the next few quarters will bring better results, a drop and correction in the multiple might very well happen.

Risks

Looking at some of the risks within Mativ Holdings, Inc. I have already mentioned one of them, the cash flows . They remain negative, but management still issued a dividend , which I find irresponsible. In my view, a dividend should only be funded by cash flows when they are positive and strong. That seems to be the case later, not now, with MATV. Moves like this make me concerned that the dilution of shares will start to happen as a result of needing to raise capital.

Mativ Holdings, Inc. did also note they are in a challenging macro environment but did manage to pass on some costs to consumers, resulting in perhaps better margins than what otherwise would have been. The valuation might be lower than the sectors, but I find that MATV might deserve a valuation as such because of the uncertainty about some of the coming quarters we have. A negative surprise could very well result in a significant drop in the Mativ Holdings, Inc. share price to reflect lower-than-anticipated EPS or continued negative cash flows.

Financials

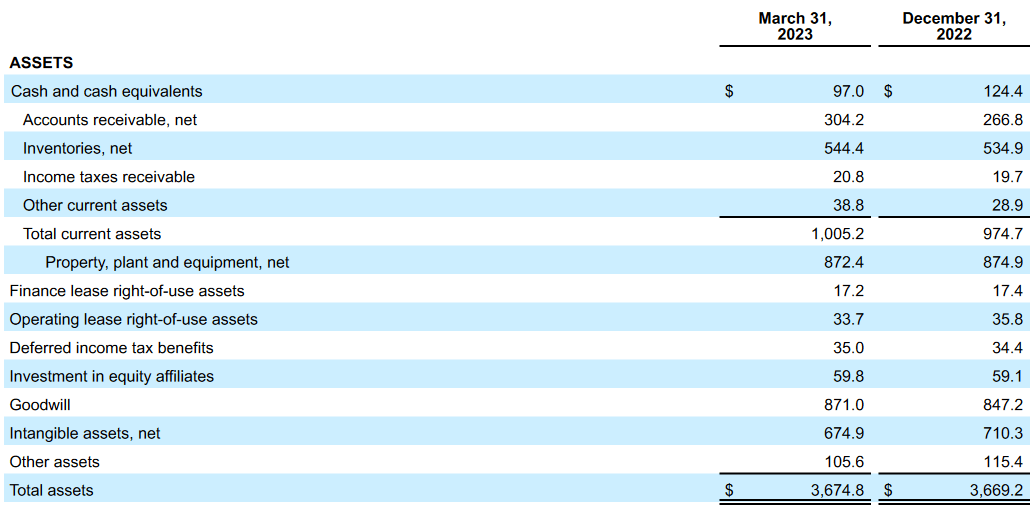

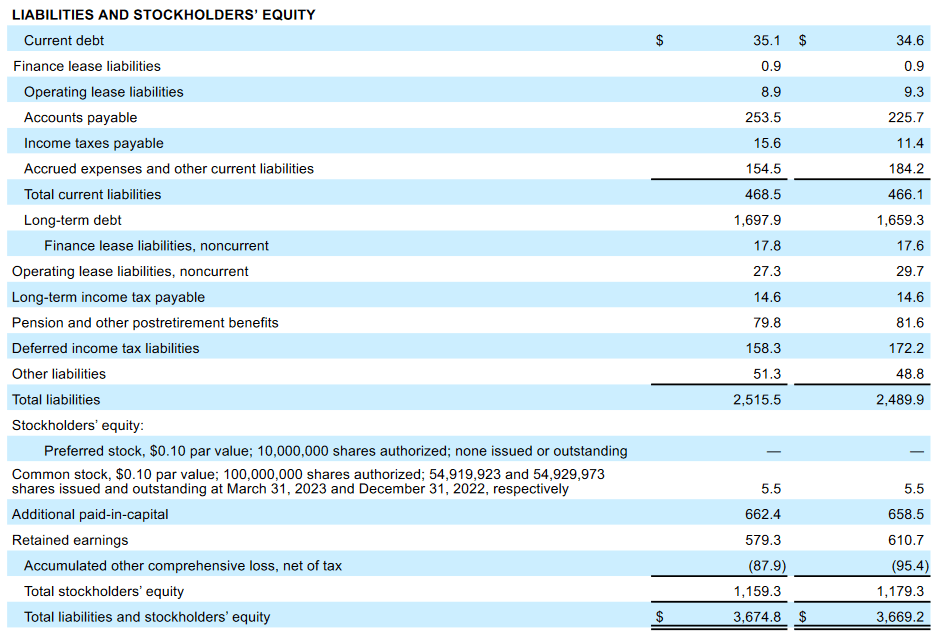

Moving over to the financials, Mativ Holdings, Inc. has seen a QoQ decline in the cash position by around 25%, ending up with under $100 million in cash. Not a move I like to see, especially when the company has issued a dividend recently, too. The cash flows are negative as mentioned, so I do not see a scenario in the near term where an increase in the cash position might be possible unless funded by share dilution, which also is not ideal. Comparing the cash position to the debts, there is a big discrepancy. Unfortunately, the $97 million in cash won't too much for their $1.7 billion in long-term debts.

Company Assets (Earnings Report) Liabilities(Earnings Report)

{kind=link}

{kind=link}

What worries me more regarding the financial state of the company is the net debt/EBITDA ratio, which is sitting quite high at 6.89. That is far above my comfort level of 3. There is a high probability that there will be a dilution of shares because of this, in my opinion, as the EBITDA could possibly not be sufficient to cover debts. This would, of course, hurt an investment in the company and open up too much downside risk.

Company Financing (Earnings Report)

{kind=link}

All in all, I find there to be several improvements necessary before I can say the company looks to be in a strong financial position. The cash position needs to increase to bring more flexibility and financial freedom for the company to make strategic investments and help fuel potential growth. But in order for that to happen, MATV needs to increase its margins, especially the free cash flow margins. Stopping the dividend could be a good start to help further stabilize the financial state they are in. It's not necessary to issue one when cash flows are negative.

Valuation & Wrap Up

Mativ Holdings, Inc. is a promising play if you want to get exposure to the materials industry and some of the end markets that the company serves. But there are improvements I'd like to see before I could comfortably say MATV is a buy. Some of the arguments the company has regarding future growth are that they are well positioned to benefit from megatrends. These include the demand for cleaner air through filtration by industrials as companies seek alternative building solutions and practices. Looking at the margins, there might be a catalyst, as the company is seeing increased growth and faster growth, too, in higher-margin products.

Company Markets (Investor Presentation)

{kind=link}

One of the main issues I had when reviewing the Mativ Holdings, Inc. financials was the cash flows being negative. The management mentioned this might be seasonal, so the coming quarters will reveal whether this is true or not. Until and unless cash flows improve, I think there is a high probability of shares being diluted, hurting an investment. For the moment, however, I will rate Mativ Holdings, Inc. stock a hold, as I do see potential in the merger that happened last year. In the long term, the outlook for Mativ Holdings, Inc. does remain positive, but it will be hard to find a strong buy point until the improvements I mentioned have happened.

For further details see:

Mativ Holdings: Not Quite A Buy Just Yet