MATV - Mativ Holdings Q2: Cutting Dividends But Not Ambitions

2023-08-24 13:19:29 ET

Summary

- Mativ Holdings reported $667 million in sales, but organic sales decreased by 8%.

- The release liner sector shows mid-single-digit growth in sales.

- Adjusted EBITDA increased by 33% compared to Q1, indicating cost-cutting and operational efficiency.

Thesis

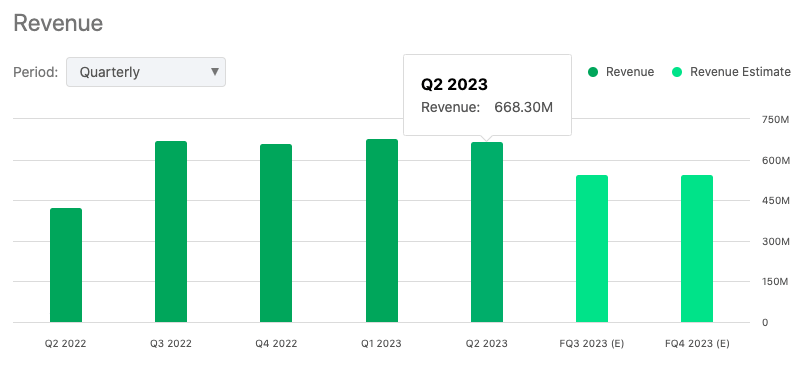

Mativ Holdings ( MATV ) has unveiled its Q2 2023 financials, posting a revenue of $668.3M and a non-GAAP EPS of $0.51.

{kind=link}

While the initial figures like the sales of $667 million may seem promising, a deeper dive reveals an 8% decline in organic sales. This analysis argues that, in spite of some commendable operational strides and strategic investments, Mativ's long-term performance and recent dividend cuts hint at underlying challenges that investors should approach with caution.

Company Profile

Mativ Holdings, Inc., founded in 1995 which some might recall as Schweitzer-Mauduit International, Inc., distinctly operates within two primary segments: Advanced Technical Materials and Fiber-Based Solutions.

{kind=link}

Examining the Advanced Technical Materials Segment :

- Product Lineup: This encompasses materials such as polymer, resin, fiber substrates, and a selection of nonwoven items.

- Market Implications: The segment primarily serves industries like filtration, protective solutions, and the healthcare sector, among others.

Turning our focus to the Fiber-Based Solutions Segment :

- Product Suite: The offerings here range from packaging and specialty papers to consumer-oriented paper products. Notably, this segment has ventured into the combustibles sector with various paper-based products.

- Market Orientation: The segment seems to primarily cater to cigarette and cigar manufacturers, as well as the commercial print industry.

From a geographical perspective, Mativ Holdings exhibits a notable global reach, distributing its products across diverse regions from the U.S. to Asia Pacific and beyond.

Mativ Holdings Q2 2023 Earnings Highlights

Mativ Holdings recently dropped their Q2 financials and reported sales of $667 million, which sounds great on the surface. But diving deeper, they faced an 8% hit in organic sales. However, credit goes to them for being agile and bumping up prices by 5%, which softened the blow from a 13% dip in volume and mix.

Looking at the sectors, the release liner was the star player, seeing a decent mid-single-digit growth in sales. Looking ahead, CEO Julie Schertell noted:

We've invested in new release liner capacity in Mexico, which is expected to come online in Q4 of this year, supporting greater growth in North and South America. Release line volume continues to lead in our portfolio, with a decade of consistent and strong growth.

And just a side note - the EP and healthcare sectors stayed consistent, showing no major hiccups.

Breaking down the earnings, the adjusted EBITDA went up by a solid 33% compared to Q1 of 2023. This should indicate to investors that Mativ has been on their A-game, cutting down costs and making the most of their operational synergies. Even with a 10% drop from Q2 2022's adjusted EBITDA, they managed to keep a 13.1% margin, which is commendable.

On the pricing front, there's a noticeable benefit of $40 million, and it seems like Mativ is keen on holding onto these price hikes.

Zooming out a bit, even with the whole inflation situation, which CFO Greg Weitzel said "continues to ease on most fronts", Mativ seems to be finding its footing. The input costs for this quarter are down just $14 million from last year.

Talking commodities, prices for NBSK pulp seem to be going down , which could be good news for Mativ. And with the market prices for polypropylene looking low (thanks to a lot of supply and, according to management, iffy demand), it feels like a win-win situation.

Mativ's been making some solid moves operationally, especially in their commercial and manufacturing areas, which is great for their bottom line.

Regarding the sale of Engineered Papers that's expected to close in Q4 2023, and if that goes through, they're looking at a business value of around $2.2 billion in sales and a 13% adjusted EBITDA margin.

In terms of managing their debt, once the EP sale wraps up, they're planning to reduce their leverage by 0.3 turns. Their aim? To get their leverage to sit comfortably between 2.5 to 3.5 times by end of next year.

Wrapping the highlights up, their operating cash flow for Q2 is a decent $40 million, showing a nice bounce back from Q1.

Performance

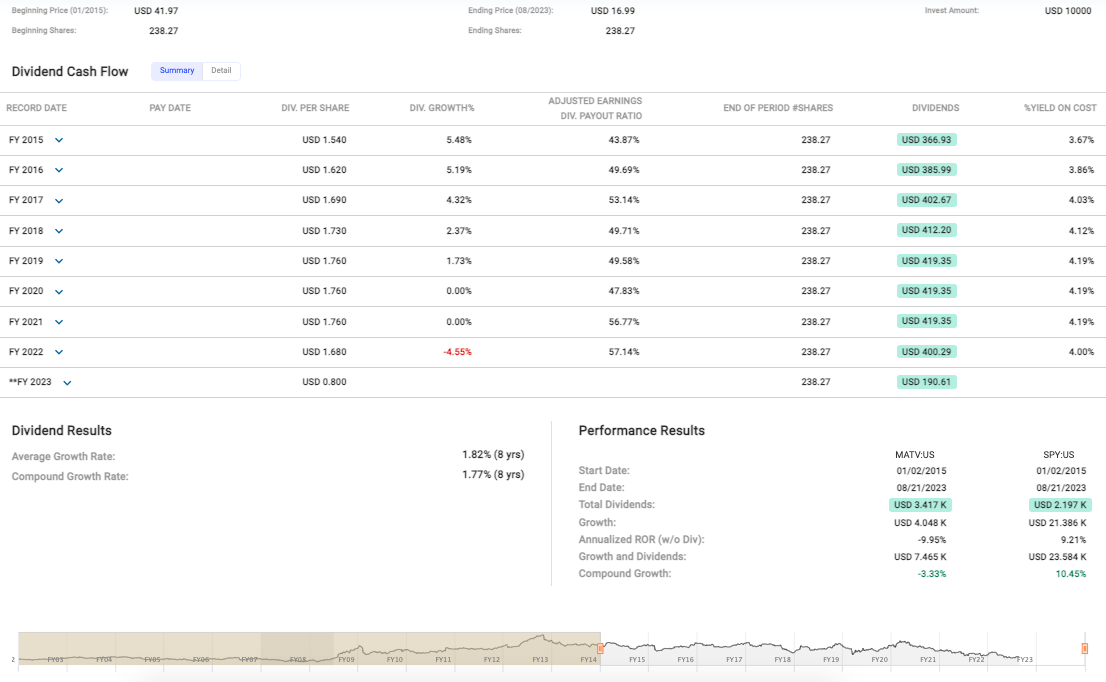

Over a medium-term time frame (see data below), Mativ's share price has eroded from a starting figure of $41.97 in 2015 down to $16.99 in 2023. This significant decline has resulted in an annualized rate of return (without dividends) of -9.95%. In a market where the S&P 500 Index has offered a 9.21% return over the same period, Mativ has been a marked underperformer.

{kind=link}

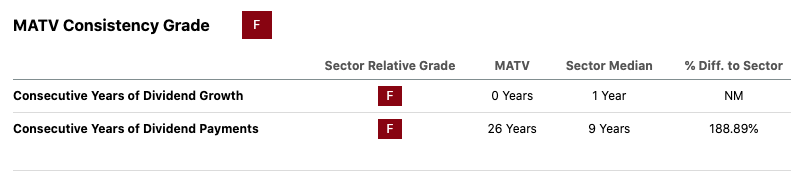

A deeper look at the dividend track record (which gets an " F " rating from Seeking Alpha Quant) shows that dividends have grown at a feeble average of 1.82% over 8 years, with compound growth at 1.77%.

{kind=link}

For an optimist, this might seem as moderately respectable until you consider that in the most recent fiscal year, 2023, there was a drastic cut with dividends plummeting to $0.800 per share from the prior year's $1.680. Generally, such a significant cut is rarely a good omen for income investors, often reflecting deeper underlying financial distress or strategic shifts. However, CEO Schertell explained that "debt reduction remains [Mativ's] priority use of cash in the near term."

Valuation

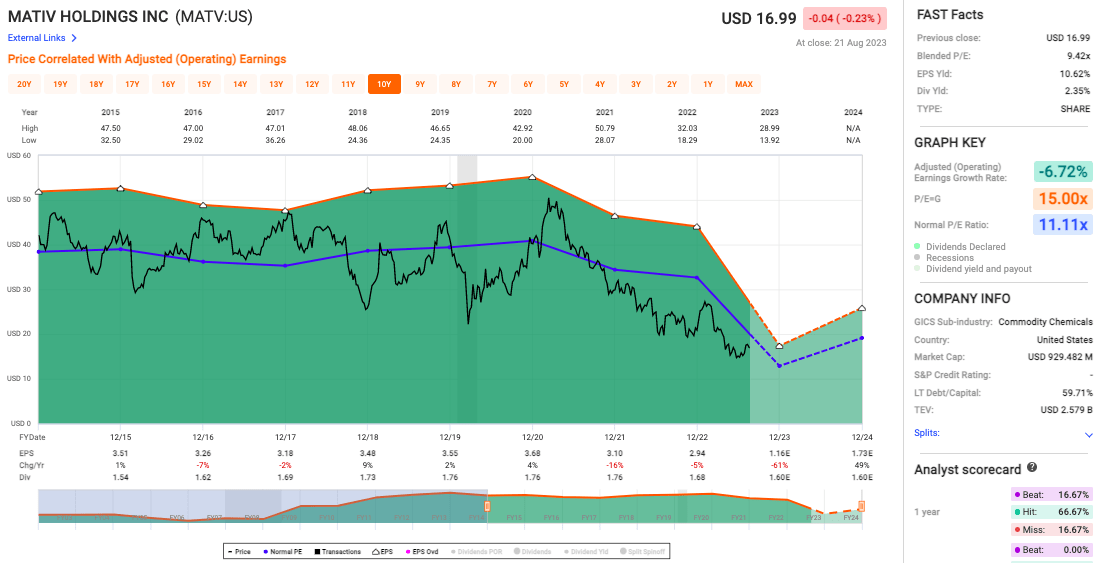

Mativ's chart (see below) isn't showing a flattering trajectory, given that the adjusted operating earnings growth rate is at a concerning -6.72%. This indicates that, at least operationally, Mativ is on a declining path, or at best, a plateau.

{kind=link}

Mativ's blended P/E stands at 9.42x, quite a bit lower than the P/E=G rate of 15.00x. The "normal" P/E ratio, historically speaking, for Mativ is 11.11x. What this means is Mativ is currently undervalued compared to its historical standards. But is this justified? Given the negative growth rate in its operating earnings, it might be.

Risks & Headwinds

Mativ's organic sales took an 8% dip. A big chunk of this seems to come from the aforementioned 13% slide in volume and mix, likely due to customers cutting back and some shaky economic momentum out there.

Jumping back to last year, when we compare Q2 2023 with the brighter days of Q2 2022, there's a noticeable 10% drop in the adjusted EBITDA. Especially worth noting is the ATM (Advanced Technical Materials) segment. They've faced an 18% hit in adjusted EBITDA from last year, which is nearly a $14 million drop. On top of that, they're dealing with a margin drop of 130 basis points.

Zooming out a bit, there are several things impacting EBITDA. According to management, they're talking about changes in volume, shifts in manufacturing, and some added costs. All these elements came together, resulting in a $35 million dent in the adjusted EBITDA when you compare it with last year.

Given all this and with the planned sale of Engineered Papers on the horizon, Mativ has adjusted their goals a bit. Initially, they aimed to hit an EBITDA of $100 million each quarter, but now they're looking more at the $70 million mark.

Rating: Hold

While Mativ Holdings has made notable operational improvements and investments that might bolster future growth, especially with their release liner capacity in Mexico and potential from the Engineered Papers sale, there are undeniable concerns. The company's long-term stock performance is lackluster, with a significant decline over the years. Moreover, the recent drastic dividend cut, although aimed at debt reduction, is worrisome. Combined with an observed dip in organic sales and adjusted EBITDA from the previous year, it suggests caution is warranted. However, the company's current undervaluation and potential upside from strategic shifts and operational synergies provide enough reason to hold for now in my opinion.

For further details see:

Mativ Holdings Q2: Cutting Dividends, But Not Ambitions