MTRX - Matrix Service Company: Too Early Until Proven Profitability Is Visible Once Again

2023-12-07 11:05:35 ET

Summary

- MTRX along with a lot of other construction companies are experiencing a difficult time right now.

- Higher interest rates are pushing the earnings down for the company.

- With a track record of lacking a positive bottom line, the company exhibits a risky investment right now, one where selling is the best choice.

Investment Rundown

The construction sector has been under a lot of pressure the last few quarters as the rise in interest rates has meant that financing projects are more expensive and the rise in several commodities and materials prices has also made it more tough to operate. One such company in the sector is Matrix Service Company ( MTRX ) which has seen its stock price increase rapidly over the last 12 months. It's still a relatively small company with a market cap of $275 million. Looking back at the top and bottom lines of the business, it has been quite poor. Since 2019 the revenue has been steadily declining and is close to 50% lower than that year. In terms of the bottom line, it doesn't look much better here, either. Since 2020 MTRX has consistently been unprofitable and this has led to shares steadily being issued to cover the TTM interest expenses of $2 million.

Without a profitable bottom line and no near-term catalyst that would indicate it might be achieved, this makes for quite a risky investment here, in my opinion. Should MTRX manage to achieve the net income it had in 2019 which was $28 million and the shares stay the same, we get an EPS of $1.03 and give that a 17x multiple which is the same as the industrial sector and MTRX might just offer a lot of upside as the target price reaches $17.5. However, I will reiterate that I don't see a quick turnaround for the company, and with a depleting cash position, I see further dilution ahead. To me, MTRX exhibits a sell right now as the risk to reward seems too high.

Company Segments

MTRX stands as a significant player in both the energy infrastructure and industrial markets. Their extensive range of services encompasses crucial aspects like engineering, fabrication, construction, and maintenance. Operating not only within the United States and Canada but also internationally, the company plays a vital role in supporting critical infrastructure needs on a global scale.

{kind=link}

Within its operations, MTRX is organized into three key segments, those being Utility and Power Infrastructure, Process and Industrial Facilities, and the Storage and Terminal Solutions segment. In the realm of utility and power infrastructure, the company contributes substantially to the power sector, providing essential services to enhance the development, maintenance, and efficiency of power infrastructure. This aligns with the growing demand for reliable and sustainable energy solutions on a global scale.

{kind=link}

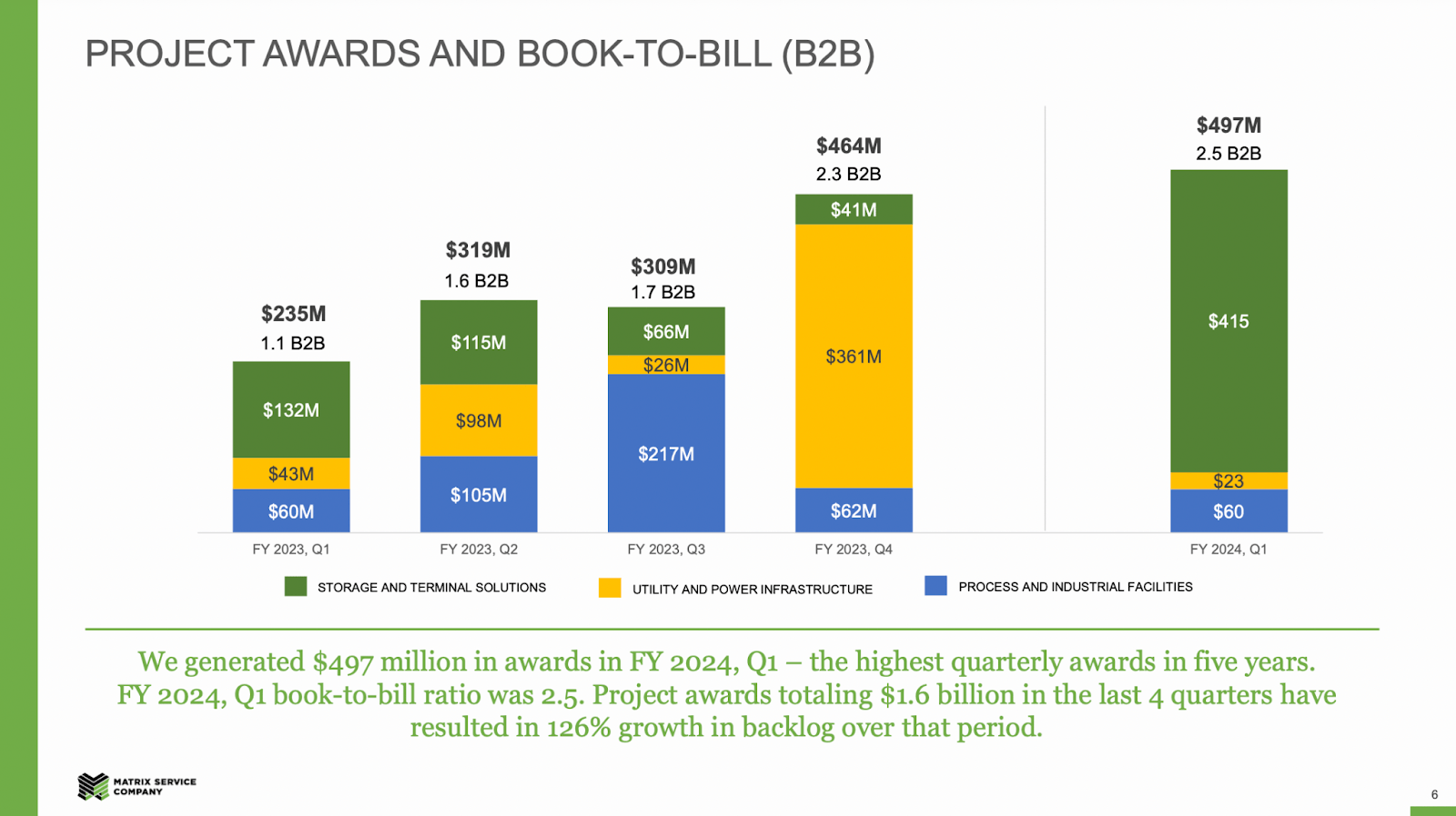

One of the key drivers behind the last 12 months' growth for the company's valuation has been the improved activity in the backlog part of the business. When rates were beginning to go higher, there seemed to have been a lot of worries in the markets that caused orders to be lower for MTRX. This seems to be on the reverse right now, and the FY2024 Q1 report showcased it climbing to $497 million in total.

Markets They Are In

{kind=link}

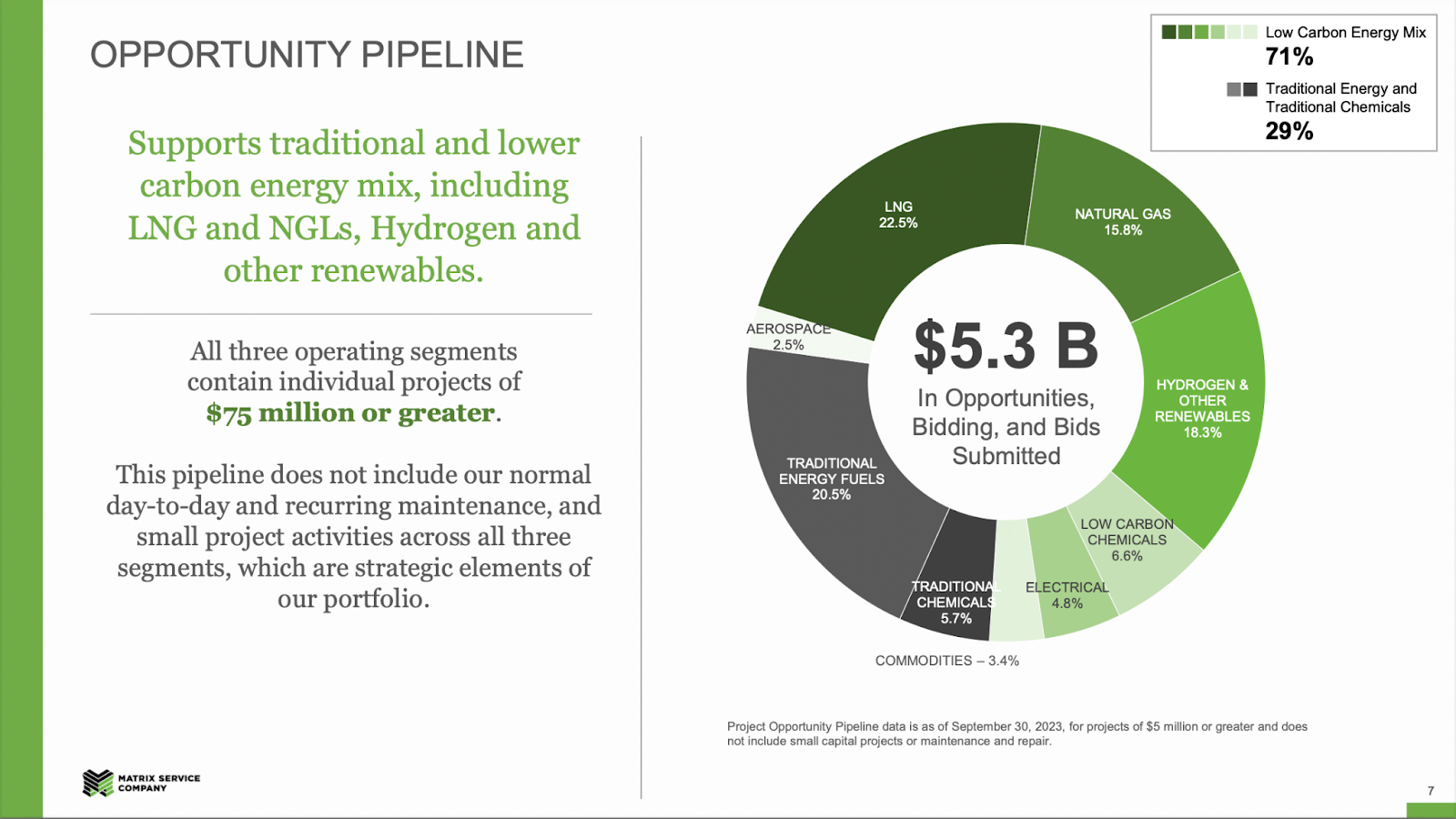

There are plenty of market trends right now appearing for MTRX which are on a large scale too. The clean energy transitions are positively supporting demand for MTRX as they offer construction and maintenance services to projects that include clean energy and other energy sources. The US Inflation Reduction Act was a major milestone for investments into both American infrastructure and green energy. These are major tailwinds that should support further project awards for MTRX, I think.

Earnings Highlights

{kind=link}

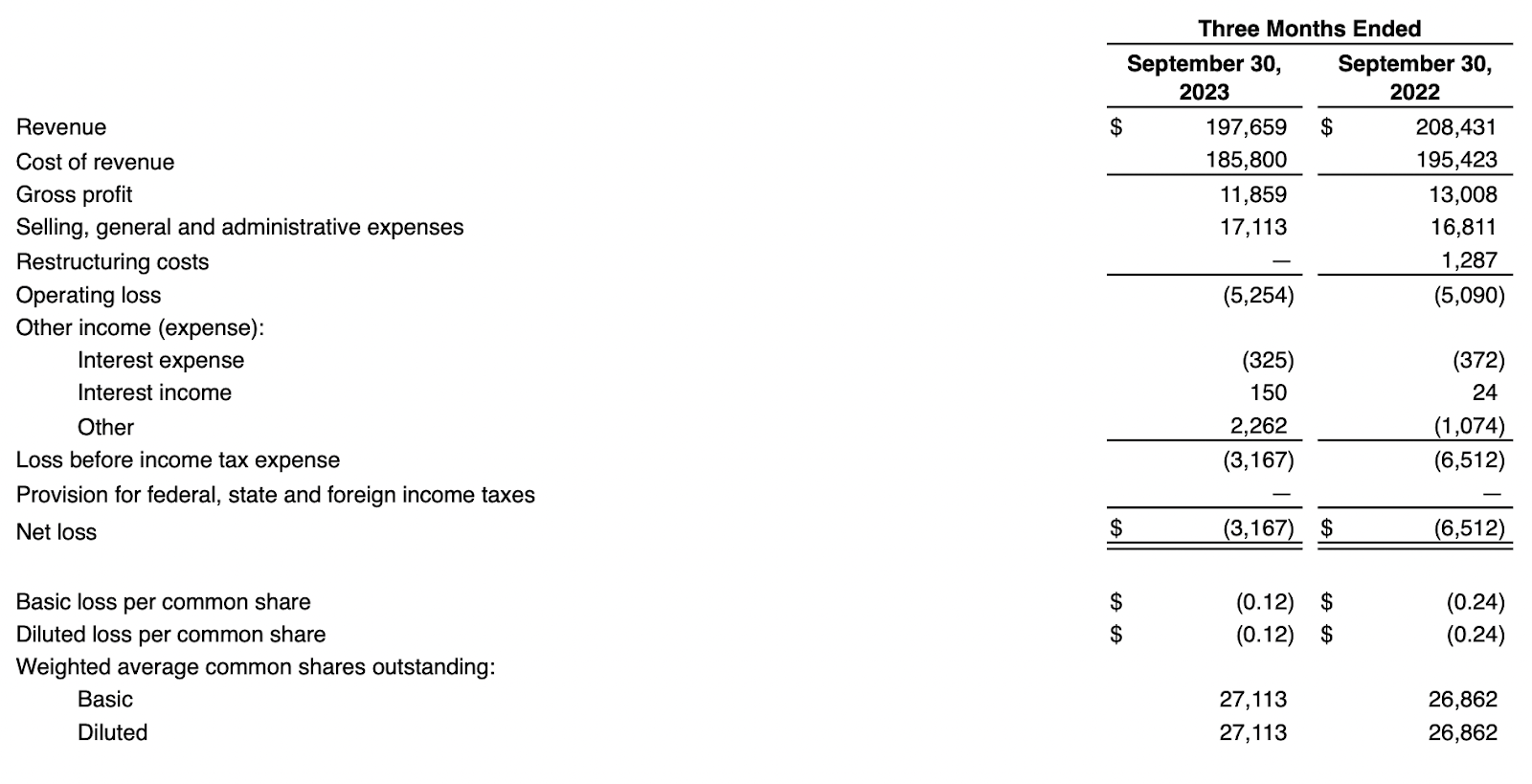

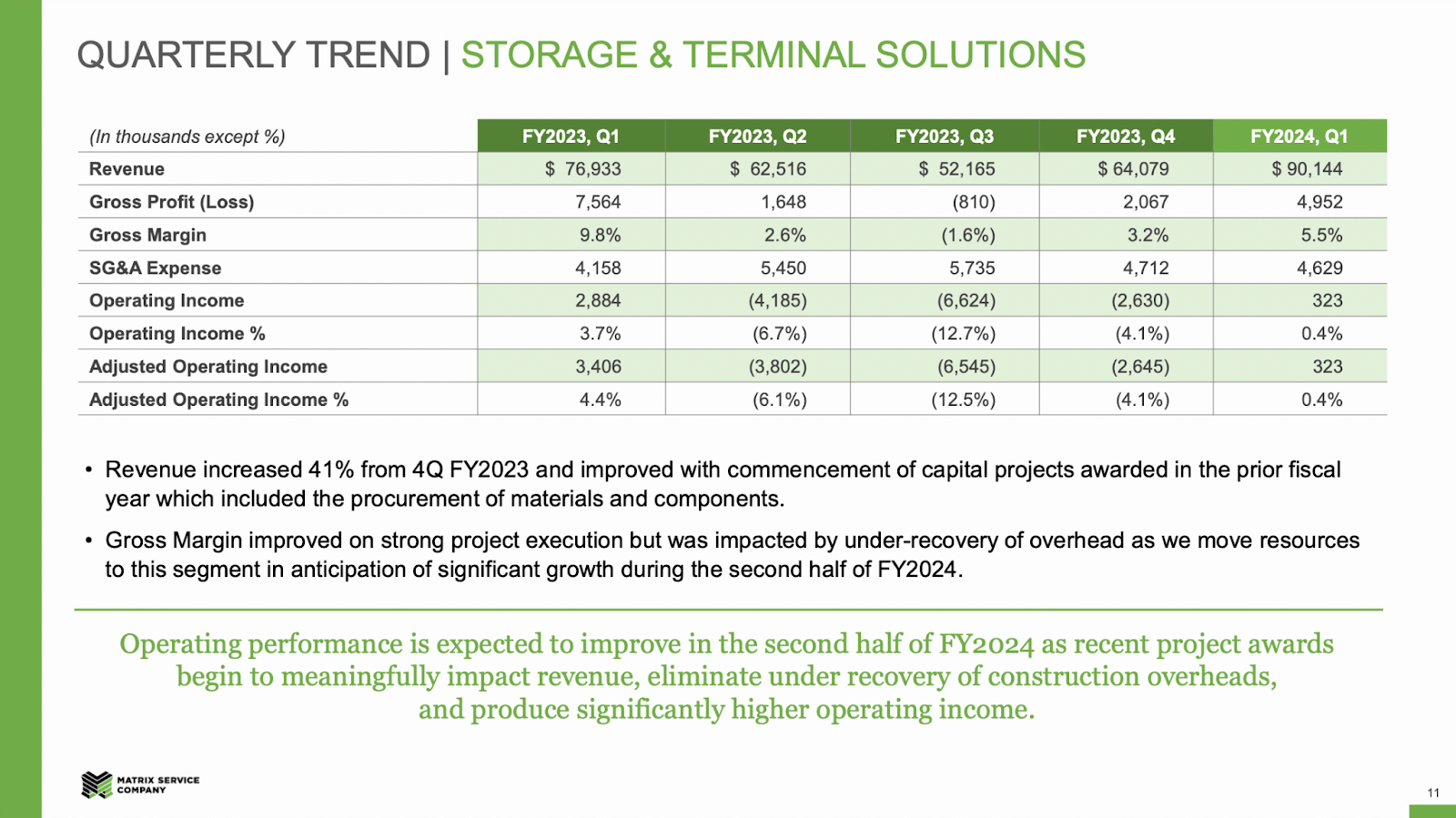

Looking at the last earnings report from MTRX that being the FY2024 Q1 released on November 8 there was a lack of top-line growth but some improvements in the bottom line. As mentioned earlier, there were a total of $497 million of total awards for MTRX in the last quarter, totaling $1.4 billion right now. This was further highlighted as it brought MTRX to a book-to-bill ratio of 2.5. The segment that saw the largest amounts of awards last quarter was Storage and Terminal Solutions, topping at $414 million. What I also want to highlight is the fact that MTRX is also continuing its trend of dilution YoY now sitting at 27.1 million outstanding shares, up from 26.8 million.

{kind=link}

Looking at the Storage and Terminal Solutions segments specifically, some noticeable trends are appearing here right now. YoY the gross margins have fallen quite a bit down to 5.5%, from 9.8% a year earlier. This move is the result of a lack of revenues and sticky prices. But I think it also showcases some of the lacking capabilities that MTRX has right now in raising prices for its customers and charging more. That is a clear sign of lacking a moat in my opinion, and something that might and perhaps even should be resulting in a lower valuation for the business.

Going into the coming few reports from the company, I find it crucial that we see strong margin expansion across the board, across all segments of the business but also that dilution halts. Right now investors are losing value from the dilution and the lack of profitability makes for a risky case here. I believe the coming quarters will be very difficult for the business and failing to meet expectations is currently on the table, resulting in me issuing a sell rating here.

Risks

A substantial portion of MTRX revenue is derived from contracts awarded on a project-by-project basis. The nature of these contracts introduces inherent uncertainties due to the prolonged and intricate bidding and selection processes. Various factors, such as fluctuations in the actual or anticipated market conditions, the financial accessibility of customers, changes in governmental rules, permitting requirements, and environmental considerations, collectively contribute to the complexity of predicting the timing and likelihood of securing new contracts.

{kind=link}

Another notable risk currently associated with MTRX is its ongoing lack of profitability. The company has struggled to return to the positive bottom line it enjoyed a few years ago. The absence of sustained profitability raises concerns, particularly if upcoming quarters reveal additional losses in this area. Continued financial downturns could potentially trigger a significant correction in the company's share price in the short term. The company seemed to be quite positive about the future and the coming years, especially when addressing the margins. The CEO John R. Hewitt said in the last report that, thanks to a lot of large project awards, the company will likely see further revenue climb in the second half of FY2024. These additional revenue streams will also impact margins in a supportive way, according to the CEO. However, the 5-year average for the company in terms of net margins has been negative 4.38%. The TTM is at negative 6.25% which means MTRX has a lot of work to do right now to make those future margin assumptions a reality. Back in 2019, the net margin was 1.9% which right now with the TTM revenues would mean $15.5 million in earnings. With a 17x multiple, that leaves us with a price target of $9.7 right now, roughly 7% lower than today's prices. This further underlines why I don't see a buy case here, and why investors are better off selling and staying on the sidelines until MTRX can prove consistent positive earnings are achievable.

Final Words

MTRX operates in the construction industry where there have been a lot of difficulties over the last few quarters following a rapid rise in interest rates which has made issuing and funding new infrastructure projects far more costly. For MTRX this has seemed to be the case for quite a bit and since 2019 the revenues have been falling and the bottom line is consistently unprofitable. Even with the same net margins as in 2019 applied now would mean with a 17x multiple we get a target price lower than today's stock price. This to me further underscores the lack of incentive to be buying here. I want to see positive earnings for the better part of 2024 before considering a higher rating here, to be frank.

For further details see:

Matrix Service Company: Too Early Until Proven Profitability Is Visible Once Again