MATX - Matson And Its Real Value

2023-08-02 15:19:07 ET

Summary

- Matson, Inc. has seen a decline in shipped volume over the past year, most likely due to customer product purchase decreases.

- The pandemic-era shipping boom drove Matson fundamentals much higher than previously normal levels before Covid.

- Global instability and trade wars could pose a potential threat to Matson shipping lanes and volume in the future.

- This article focuses on the fundamentals, the real value versus the current share price, and discusses whether Matson Inc is currently worth investing in.

Matson, Inc. ( MATX ) saw a shipping boom during the pandemic due to increased customer product demand as well as a surge in shipping prices from supply chain bottlenecks. While shipping prices have fallen since record highs, they still sit well above previous pre-pandemic levels. This has supported Matson's skyrocketing fundamentals in the last three years.

As prices begin to fall, Matson will need to accommodate shipping larger volumes to maintain its current outlook. That could prove difficult with food prices rising and customer purchases for non-essential products decreasing. Another potential headwind for Matson is the global instability worsening, which could cause difficulties in continuing to increase shipping volumes for certain products from specific countries. Matson will need to mitigate these headwinds to continue to maintain its higher stock valuation.

During the most recent guidance, Matson saw declines across all its fundamentals in its financial statements. Stating many of the headwinds we have highlighted above. The company does believe in a return to normal shipping volumes and geopolitical stability in the second half of 2023. Additionally, Matson is focusing on sustainability projects to maintain its climate responsibilities. This will require investment in technology developed for efficiency to meet its carbon goals. Matson's environmental, social and governance ((ESG)) initiative does help with its bottom line by reducing fuel costs, which have been rising since the war in Ukraine, during the transportation of goods. Overall, Matson does have competing dynamics that can dictate the stock's performance in the near and long term.

When considering these current stories about Matson Inc, we need to determine which news topics will have a long-term and ongoing effect on the company and its share price. Shipping trends continue to show decreases from the geopolitical environment as well as customer demand reductions. Matson still thrives on increased shipping prices compared to pre-pandemic levels giving it excess cash reserves. The continued investment in improved technology that reduces costs indicates that Matson is preparing for more sustainability to withstand future potential downturns.

Due to potential declines in fundamentals in the short term, there is concern about a stock correction. The downside risk of Matson is relatively low due to its stability in a global free trade environment. While stability is good, there is worry about its growth potential after record highs during the pandemic. Matson seems to present two potential paths, one of some downside risk and the other resurgence from customer demand as well as reduced costs.

While current news stories, good or bad can sway our opinion about investing in a company, it's good to analyze the fundamentals of the company and to see where it's been in the past and in which direction it's heading.

This article will focus on the long-term fundamentals of the company, which tend to give us a better picture of the company as a viable investment. I also analyze the value of the company versus the price and help you to determine if Matson Inc is currently trading at a bargain price. I provide various situations which help estimate the company's future returns. In closing, I will tell you my personal opinion about whether I'm interested in taking a position in this company and why.

Snapshot of the Company

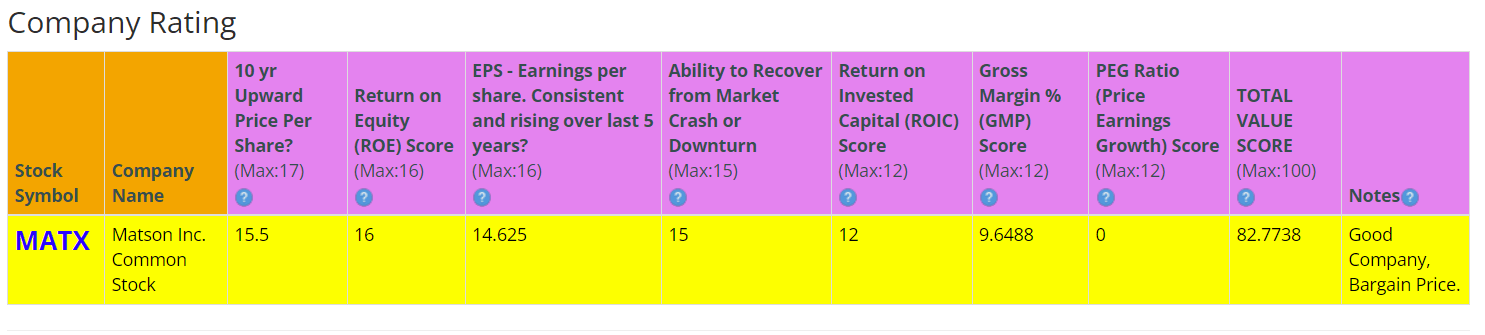

A fast way for me to get an overall understanding of the condition of the business is to use the BTMA Stock Analyzer's company rating score. Matson Inc shows a strong rating score of 82.7 out of 100. In summary, Matson could still see stock rises in the future due to having strong fundamentals.

Before jumping to conclusions, we'll have to look closer into individual categories to see what's going on.

{kind=link}

Fundamentals

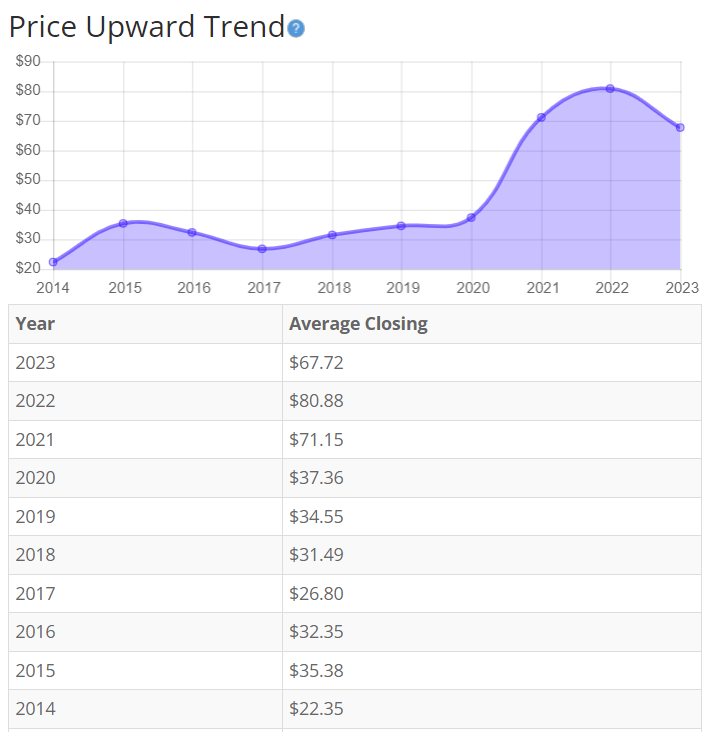

The share price has seen a large rise since pre-pandemic levels. The recent fall is most likely due to reduced guidance from the company on macroeconomic factors and global instability. Customer demand for products has declined as necessities like food have seen price rises. This has impacted Matson's shipping volume from previous pandemic highs when people were buying more online. The stock price still sits double compared to pre-pandemic levels due to higher shipping costs and increased volume. Online shopping should continue to increase which could drive shipping volume to return to higher levels in the coming years.

Matson has also seen an impact from global trade wars, with a 30% reduction in trade volume in China. Matson still holds the fastest joining between China and California which gives some barrier to entry for competition. Overall, the share price average has grown by about 203% over the past 10 years, or a Compound Annual Growth Rate of 13.1%.

{kind=link}

Earnings

Earnings shot up during the pandemic and have continued to rise. Part of this could be related to Matson's efforts to reduce the costs of fuel on its bottom line. Another potential explanation is the impact of the headwinds has not been seen on its EPS yet. Matson also repurchased shares in the recent year, which would have improved EPS without any direct business growth. Overall, it seems obvious that the pandemic greatly benefited the company earnings to go from 4.44 to 21.47 in a single year. A significant reduction in EPS in the next year seems to be likely.

BTMA Stock Analyzer

Since earnings and price per share don't always give the whole picture, it's good to look at other factors like the gross margins, return on equity, and return on invested capital.

Return on Equity

Because of the exaggerated increase in earnings during the pandemic, the ROE also experienced a similar surge. With the current headwinds faced by the company and reduced guidance in the recent quarter I would expect to see a continued reduction in ROE. However, it's likely that the return on equity will plateau above previous pandemic levels due to increased customer online demand and global tension decreases.

For return on equity ((ROE)), I look for a 5-year average of 16% or more. Matson does meet my requirements, but the ROE average would be much less if we removed the current pandemic level highs.

BTMA Stock Analyzer

Let's compare the ROE of this company to its industry. The average ROE of 8 Shipbuilding and Marine companies is 35.29%.

Therefore, Matson's 5-year average of 34.38% is within its industry peers.

Return on Invested Capital

The return on invested capital again looks to match the ROE trend. Capital expenditure seems to have been reduced compared to previous levels in 2021. Most likely this is because of the reduced need for additional shipping, which forced Matson to invest in additional freighters and containers to meet demand during the pandemic. Since this has subsided due to falling customer purchases, it would make sense to see a reduction in capital expenses. Other capital expenses are likely related to its commitment to improving technology for emissions reductions. The declining trend of ROIC is expected to continue at least in the short term. For return on invested capital ((ROIC)), I also look for a 5-year average of 16% or more.

Matson passed this test, but only because the pandemic boosted these numbers, as well. However, I will be more conservative and use the pre-pandemic numbers, which would show that Matson would not pass this test in a normal situation.

BTMA Stock Analyzer

Gross Margin Percent

The gross margin percentage ((GMP)) has continued to rise since pandemic levels. Matson Inc has seen revenue growth decline compared to the previous 2021 and the majority of 2022 levels but has still managed to keep its gross margin steady. This is a good indicator that Matson is resilient to downturns from current headwinds. It also means that a decline is to be expected in its quarterly and yearly earnings for 2023. The last quarter of 2022 showed revenue decline outpacing cost reduction. I typically look for companies with gross margin percent consistently above 30%. So, Matson does not make the cut.

BTMA Stock Analyzer

Financial Stability

Looking at other fundamentals involving the balance sheet , we can see that the debt-to-equity is less than 1. This is a positive indicator, telling us that the company can afford its obligations.

Matson's Current Ratio of 1.05 is satisfactory, indicating it can pay off short-term debt with its current assets. Matson did recently announce a stock repurchase which would have had an impact on its current ratio.

Ideally, we'd want to see a Current Ratio of more than 1, so Matson exceeds this amount.

Matson is in great financial health with still a large amount of cash on hand. The steady reduction in its debt with the continued increase in its cash reserves over the last 3 years shows a stable, resilient company. The company does seem to issue large amounts of debt for operations, most likely due to large capital costs to run the business. The company does routinely continue to pay off its obligations yearly.

Matson Inc does pay a regular dividend.

{kind=link}

This analysis wouldn't be complete without considering the value of the company vs. share price.

Value Vs. Price

The company's Price-Earnings Ratio of 4.2 indicates that Matson might be underpriced when comparing Matson's P/E Ratio to a long-term market average P/E Ratio of 15.

The 10-year and 5-year average P/E Ratio of MATX has typically been 14.2 and 11.3, respectively. This indicates that MATX could be currently trading at a low price when comparing to its average historical P/E Ratio range.

{kind=link}

The Estimated Value of the Stock is $132.25, versus the current stock price of $91.34. This indicates that Matson Inc is currently selling below potential value.

For more detailed valuation purposes, I will be using a diluted EPS of 19.74. I've used various past averages of growth rates and P/E Ratios to calculate different scenarios of valuation ranges from low to average values. The valuations compare growth rates of EPS, Book Value, and Total Equity.

In the table below, you can see the different scenarios, and in the chart, you will see vertical valuation lines that correspond to the table valuation ranges. The dots on the lines represent the current stock price. If the dot is towards the bottom of the valuation range, this would indicate that the stock is undervalued. If the dot is near the top of the valuation line, this would show an overvalued stock.

BTMA Wealth Builders Club

BTMA Wealth Builders Club

According to the valuation analysis based on forward growth, MATX is overpriced.

In my opinion, it's more important to focus on the forward growth valuation of MATX because negative earnings growth of around -71% to -77% is being forecast between now and the end of the year. In addition, earnings will likely gravitate back to normalized levels since the COVID surge has subsided and shipping revenues are reducing.

In summary, this forward growth analysis shows an average valuation range of around $21 to $63 per share versus its current price of about $93, this would indicate that MATX is overpriced.

Summarizing the Fundamentals

After analyzing the fundamentals for Matson, I feel a need to be very cautious. The company seems to have seen unprecedented growth during covid but is starting to see reductions due to contracting consumer spending. Global uncertainty in the next few years also urges strong apprehension that the stock price will continue to rise. Shipping and logistics do tend to remain relatively stable, and consumers will continue to order more items online than in previous years as more eCommerce companies grow. However, the company's highs seen during the pandemic may not be seen again for many years making the short-term prospects of this company very difficult to recommend.

In terms of Gross Margin, the company has continued capital investment into technology to reduce fuel costs that continue to rise because of the war in Ukraine. I see this not only as a natural investment that helps the company's bottom line but also positive community perception, which has intangible benefits. Gross margin is expected to decline in the next year, I believe these cost reductions may mitigate some of that drop. Reductions in ROIC, ROE, and EPS will likely happen due to decreased customer shopping demand and lowered shipping requirements. Short term this will have a significant impact. The stock price is already above the current average of 61 seen in the previous chart.

In terms of valuation, my analysis shows that the stock is overpriced.

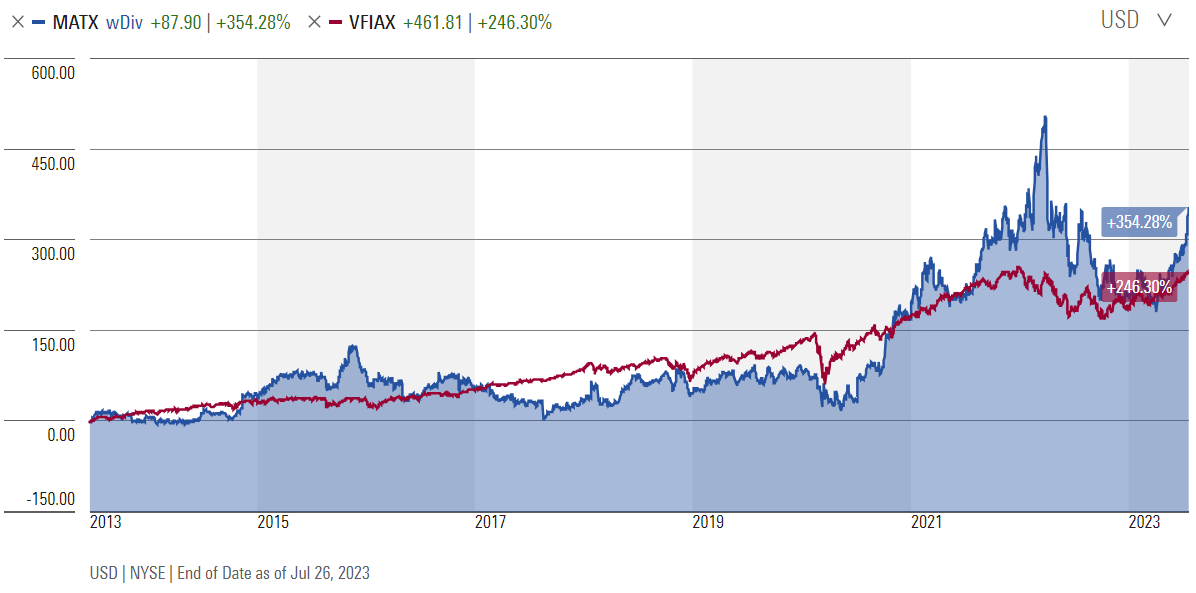

Matson Inc Vs. The S&P 500

Now, let's see how Matson Inc compares versus the U.S. stock market benchmark S&P 500 (SP500) over the past 10 years. From the chart below, we can see that the S&P 500 has outperformed MATX for most of this time period. Matson has outperformed the S&P through the COVID years. During the supply chain bottleneck, shipping prices rose and customers were buying a lot of products online causing higher returns launching it above the S&P after 2021. But this surge is temporary, and Matson will eventually normalize and performance will be hindered.

{kind=link}

Forward-Looking Conclusion

Over the next five years, the analysts that follow this company are expecting it to grow earnings at an average annual rate of 15%.

For the next quarter, analysts are forecasting -71.30% growth. For the current year, growth is expected to be -77.20%.

The Expected Annual Compounding Rate of Return is 19.68%.

Does Matson Inc Pass My Checklist?

- Company Rating 70+ out of 100? Yes (82.8).

- Share Price Compound Annual Growth Rate > 12%? Yes (13.1%).

- Earnings history consistently increasing? No.

- ROE (5-year average 16% or greater)? Yes (34.4%).

- ROIC (5-year average 16% or greater)? Yes (20.1%).

- Gross Margin % (5-year average > 30%)? No (24.1%).

- Debt-to-Equity (less than 1)? Yes.

- Current Ratio (greater than 1)? Yes.

- Outperformed S&P 500 during most of the past 10 years? No.

- Do I think this company will continue to successfully sell their same main product/service for the next 10 years? Yes.

Matson Inc scored 7/10 or 70%. On the surface, Matson seems like a viable prospect, however, if removing the outlier effects of COVID, the fundamentals would not be nearly as impressive.

Is Matson Inc currently selling at a bargain price?

- Price Earnings less than 16? Yes (4.2).

- Is MATX's Value greater than Current Stock Price? NO (Value $21 to $63 < $93 Stock Price).

Overall metrics show that Matson Inc is financially stable, and most fundamentals look satisfactory at surface level. But when we dug deeper, we realized that the positive effects of increased shipping during COVID, have greatly exaggerated the fundamentals. It's realistic to foresee the earnings and fundamentals returning back down to normal levels.

My biggest concern is the current Matson, Inc. stock price being inflated from previous pandemic highs that could take many years to beat. Global instability, increased fuel prices, inflation, and customer demand reduction all may make shipping volume reduce in the next few years. Recent guidance from the company also states an expected reduction in the year 2023 with an optimistic view of returning closer to pandemic norms in the second half. I find this to be overly optimistic and could foresee a stock dip before a rise.

I'm passing on Matson because I see more downside than upside potential.

For further details see:

Matson And Its Real Value