MATX - Matson Shareholders: There IS An Alternative

2023-05-15 18:01:17 ET

Summary

- Although it's softer than this time last year, the business has improved dramatically over time. The capital structure, in particular, is much stronger now.

- The shares are slightly more expensive than they were when I last reviewed this name, and the dividend yield is a touch lower.

- The problem is that the world of TINA no longer exists. If you can earn 4.78% risk free, why would you buy this?

A few months ago, I wrote a cautious note about Matson, Inc. ( MATX ), and in that time the shares have returned a loss of about 0.27%, against a gain of about 2.6% for the S&P 500. The company has reported financials yet again, so I thought I’d check back in here to review those. Additionally, I thought I’d review the relative valuation here, given that it was the valuation that kept me away previously. A more tolerable person than me might write something like “at the risk of boring readers with yet another sermon about the fact that we’re seeking “risk adjusted returns” and not just “returns”.” I’m very comfortable with boring readers like you, so I’ll point out, yet again, that all of my investing decisions at the moment are in the context of a world where it’s possible to earn about 4.8% risk free. The world of “TINA” seems to no longer exist for investors, and all stocks should be viewed through that lens in my view.

My regular readers know that I am absolutely obsessed with making the lives of my readers as pleasant as possible. One of the ways I try to do that is by offering you the “gist” of my thinking relatively soon in an article. This allows you to decide whether or not you want to continue reading, or just take the highlights of my thinking and flee before you’re exposed to too much Doyle mojo. You’re welcome. Although the business is much improved when compared to the pre-pandemic era, the shares are still not cheap enough in my view. If the world were still offering risk free rates of less than 2%, I might think differently, but it isn’t, so I don’t. Although there’s room for the dividend to grow from current levels, it’s still a full 280 basis points below the risk free rate. So, investors are paying more in order to take on more risk. This makes no sense to me, and so I must continue to recommend eschewing these shares until something material changes. If the spread between the risk free rate and the dividend yield falls substantially, I’ll potentially get excited. If the business improves markedly, I’ll potentially get excited. In a world where you can earn 280 basis points more while taking on dramatically less risk, I’m not excited.

Financial Snapshot

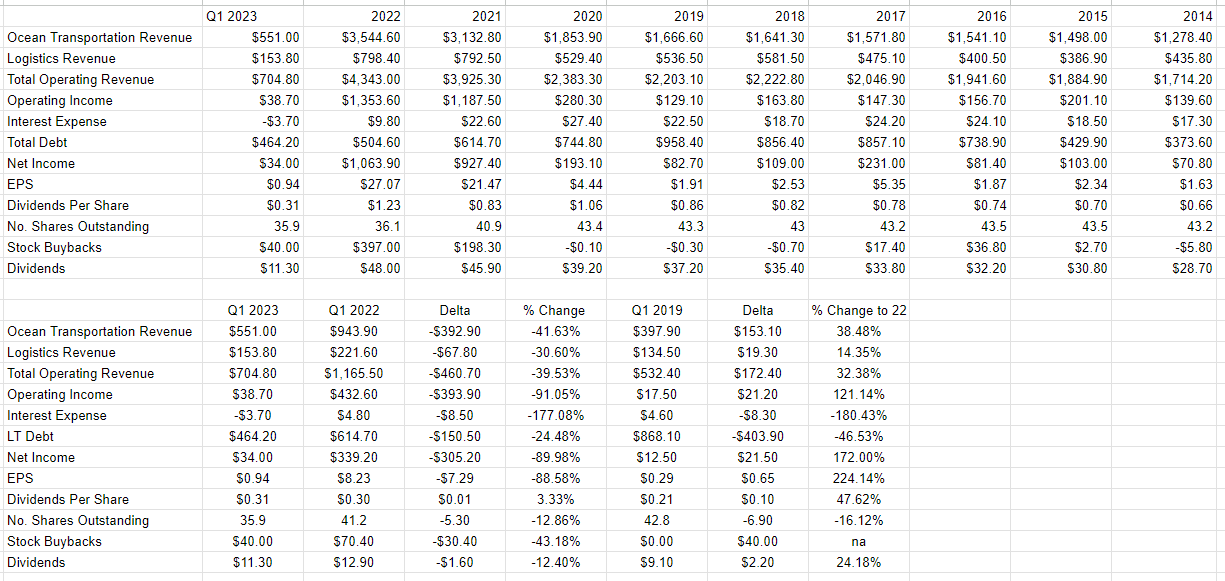

When compared to the previous year, the most recent quarter has been awful in many ways. It seems that the dynamics present in the market last year are no longer present. Things have returned to some kind of normal. As a result, total revenue is down about 39.5%, with the largest drop being seen in ocean transportation revenue, down about $392 million. In spite of this drop in the business, the dividend was raised yet again by about 3%. That written, in my previous piece on the name, I concluded that the annual dividend is relatively secure, and nothing has happened to change my view on that score.

Also, when we review what’s going on at Matson, I think it would be wise to put the most recent performance in a broader context. Although the business is much softer now than it was in 2022, that may say more about the latter than the former. For instance, when compared to the same period in 2019, revenue and net income are higher by about 32% and 172% respectively. Additionally, the capital structure has improved dramatically over the past year, with long term debt down about 25% compared to last year, and 47% compared to the pre-pandemic era.

I think the business is much improved in spite of the relative recent softness, and I think the dividend is well covered. For that reason, I’d be very happy to start to buy these shares at the right price.

{kind=link}

Matson Financials (Matson investor relations)

The Stock

One of the most important, and most painful, lessons I ever learned is that a company is different from the stock that supposedly represents it. A company can be growing revenue and earnings nicely, but if the stock is overpriced, the shares will tank. This relationship can work in the reverse, too. If a company has a fair bit of "hair" on it, and the market knows that, it may be a decent investment if the overall market is too pessimistic. I've come to the conclusion that the most important thing about stocks is the disconnect between market expectations and subsequent reality. If the expectations are too pessimistic, for instance, there may be profit to be made in even the most troubled business.

This is why I insist on only ever buying cheap stocks, because there's a strong relationship between "cheap" and "priced too pessimistically." This obviously doesn't always work out perfectly, but it's the approach that I try to take. When a stock is cheap, that's a clear sign that the market's not too optimistic about its future, so the stock is far less likely to hit the painful air pocket in the immediate future. So, in the case of Matson, it may be that the market is focusing on the recent deterioration, and failing to put the current financial performance in a broader historical context.

My regular readers know that I measure whether or not a stock is cheap in a few ways, ranging from the simple to the more complex. On the simple side, I look at the ratio of stock price to some measure of economic value, like earnings, free cash flow, and the like. Ideally, I want to see a stock trading at a discount to both the overall market and its own history. When I last reviewed Matson, the market was paying just over $0.53 for $1 of sales, and the dividend yield was about 1.95%, well below the risk free rate. Fast forward three months, and the shares are 21% more expensive on a price to sales basis, and the yield has dropped somewhat in spite of an uptick in the dividend payment per the following:

Source: YCharts

Source: YCharts

Although the shares are more expensive than they were in February, I think it fair to point out that the valuation is near the low side of the historical range. Additionally, although the dividend yield is lower than the risk free rate, there is certainly room for growth in this measure.

My regulars know that I think ratios can be instructive, but I want to confirm (or not) what they're "saying" by trying to work out what the market is "thinking" about a given investment. If you read my stuff regularly, you know that the way I do this is by turning to the work of Professor Stephen Penman and his book "Accounting for Value" for this. In this book, Penman walks investors through how they can apply some pretty basic math to a standard finance formula in order to work out what the market is "thinking" about a given company's future growth. This involves isolating the "g" (growth) variable in this formula. In case you find Penman's writing a bit opaque, you might want to try "Expectations Investing" by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and we can infer what the market is currently "expecting" about the future.

Applying this approach to Matson right now suggests the market is assuming that this company will grow earnings at a rate of ~9% in perpetuity. I consider that to be a very optimistic forecast given the volatility of Matson’s earnings. I would say of the current valuation that "cheaper" is certainly not the same thing as "cheap", and I would say that it makes sense to continue to avoid this name, especially in light of the fact that it's possible to earn a risk free of 4.78% at the moment.

For further details see:

Matson Shareholders: There IS An Alternative