MAT - Mattel: Negligible Upside Across All Investment Horizons Rate Hold

2024-01-16 16:00:00 ET

Summary

- It is better to avoid the discretionary/cyclical sector for the next 12 months due to weakened fundamentals.

- Mattel does not present a statistical advantage due to limited growth prospects in the midterm and poor capital efficiency in the long term.

- Net-net, a hold rating is supported for MAT across all investment horizons based on the arguments presented here today.

Investment briefing

Just as we have advocated ad infinitum towards industrials + basic materials for top down security selection in '24, we are advising to avoid industries within the consumer discretionary/cyclical sector for the coming 12 months. Investment return prospects for the sector are significantly weakened by a number of cyclical headwinds by best estimation.

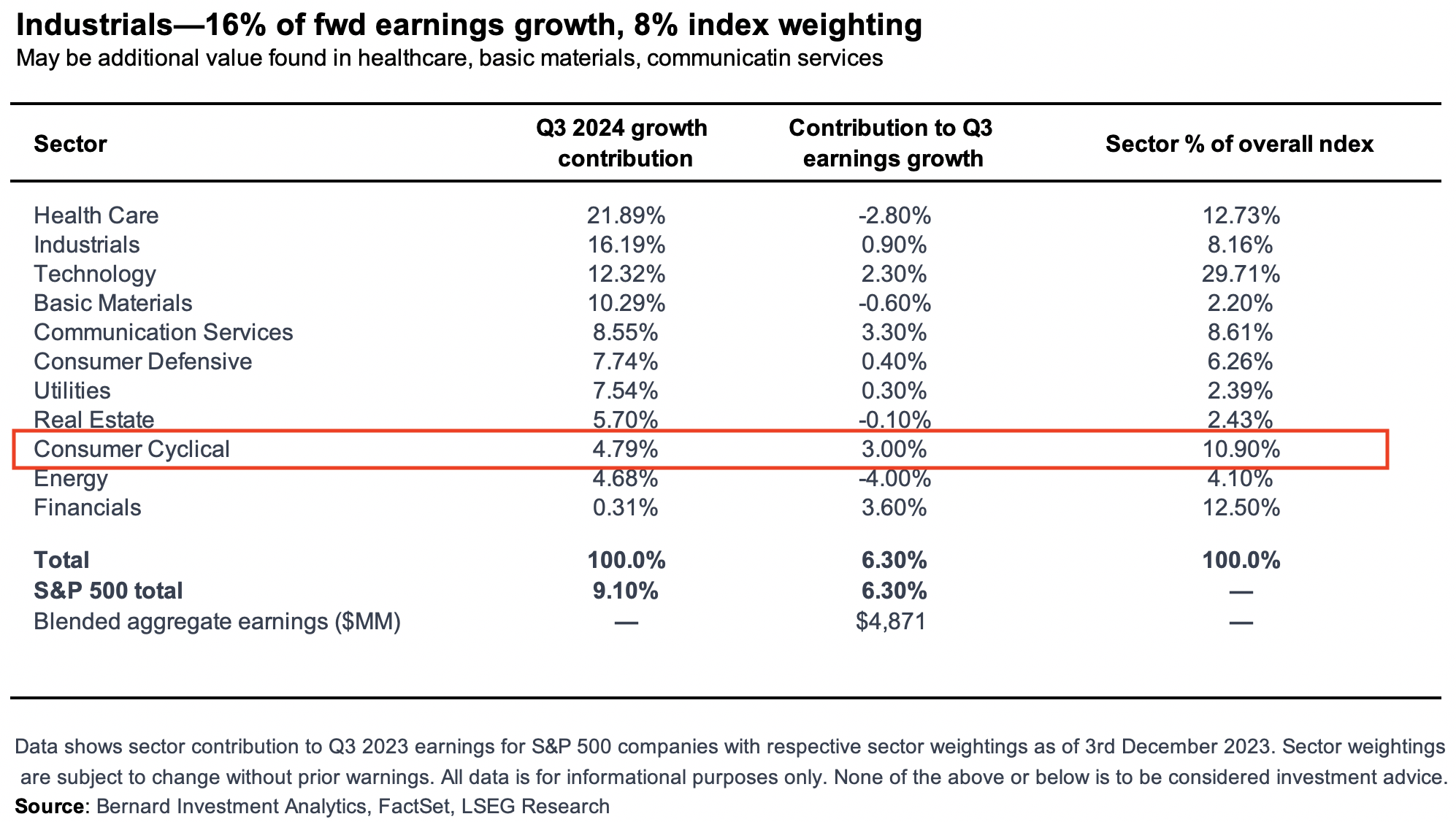

Readers of mine will have seen the data in Figure 1 repeated in our latest series of articles, from around October last year. It shows that healthcare, industrials and tech are all set to contribute heavily to the next 12 months of earnings growth. In fact basic materials, utilities and industrials offer the most compelling risk/reward calculus when put in a composite of value and growth, holding the lowest S&P 500 index weighting at the time.

Conversely, the consumer discretionary/consumer cyclical sector did not/does not currently offer a compelling risk/reward equation. As seen in Figure 1, the sector held 11% notional value of the market cap weighted S&P 500 index at the end of Q3 '23, but attribution wise, is tipped to provide just 4.8% of the next 12 months earnings growth.

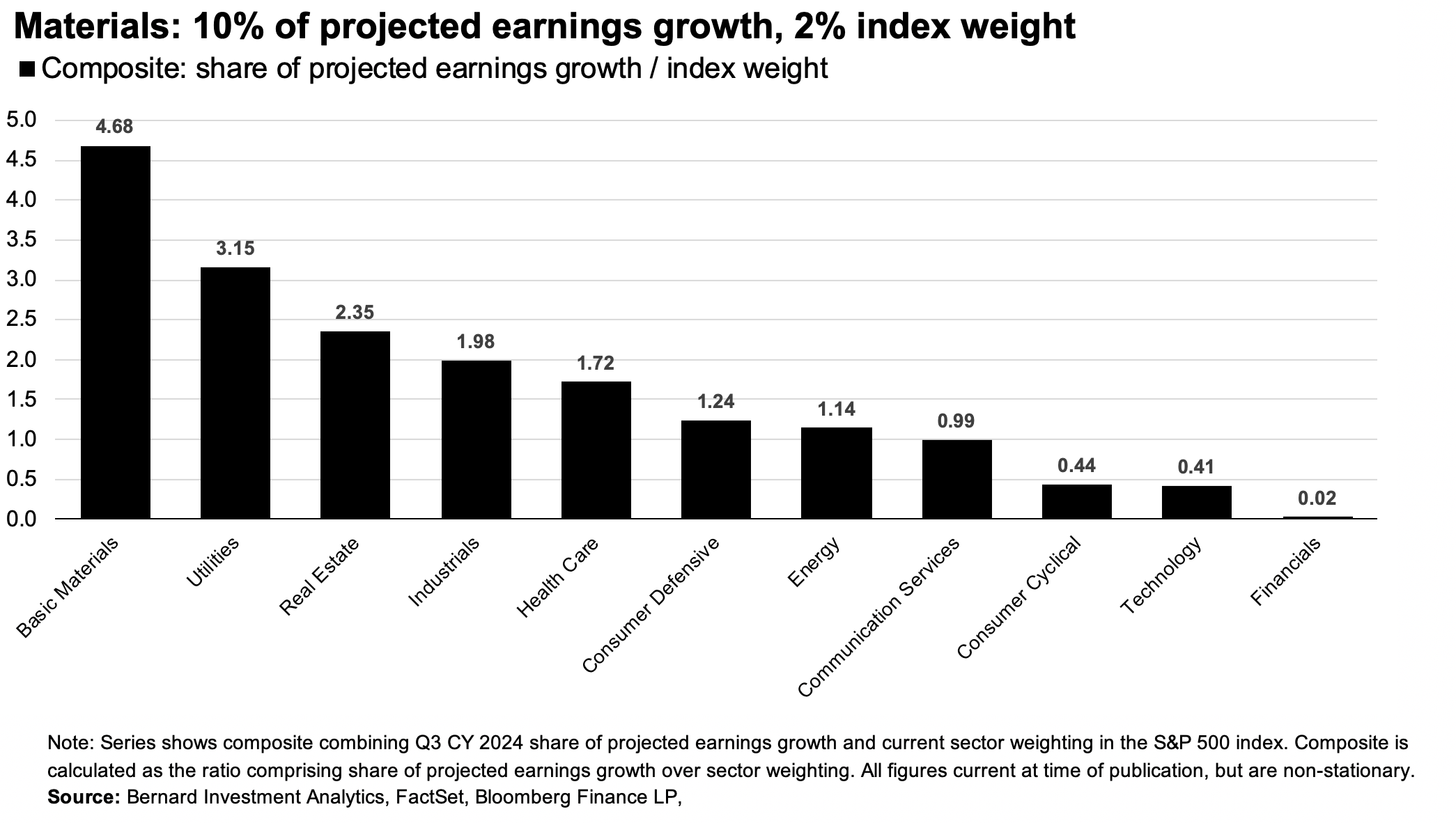

As far as the price/value axis is concerned, consumer cyclicals sit towards the end of the list, compared to their more defensive and 'old economy' counterparts (Figure 2).

Figure 1.

{kind=link}

Figure 2.

{kind=link}

Naturally, this is the kind of place we'd start looking, to observe (i) any industry outliers from the sector, and (ii) selective opportunities within the space. Perhaps the most cyclical consumer industry there is the leisure products industry, currently priced at median 13x forward earnings and 1.6x book value. That is, priced cheaply, because there's been little value creation above the cost of equity.

Within the industry, our systems were immediately drawn to the investment debate of Mattel ( MAT ). MAT is name behind some of the greatest entertainment products of our generation, ranging from labels such as HotWheels, MatchBox, Bob The Builder, UNO, and perhaps its most iconic label, Barbie. The Barbie movie's release in early 2023 was a short-term catalyst for MAT, its stock having rated from 16x trailing earnings just prior to 77x trailing P/E at the time of publication. Wall St analysts have also revised EPS targets on MAT to the upside 12 times within the last 3 months, indication of a growth period ahead.

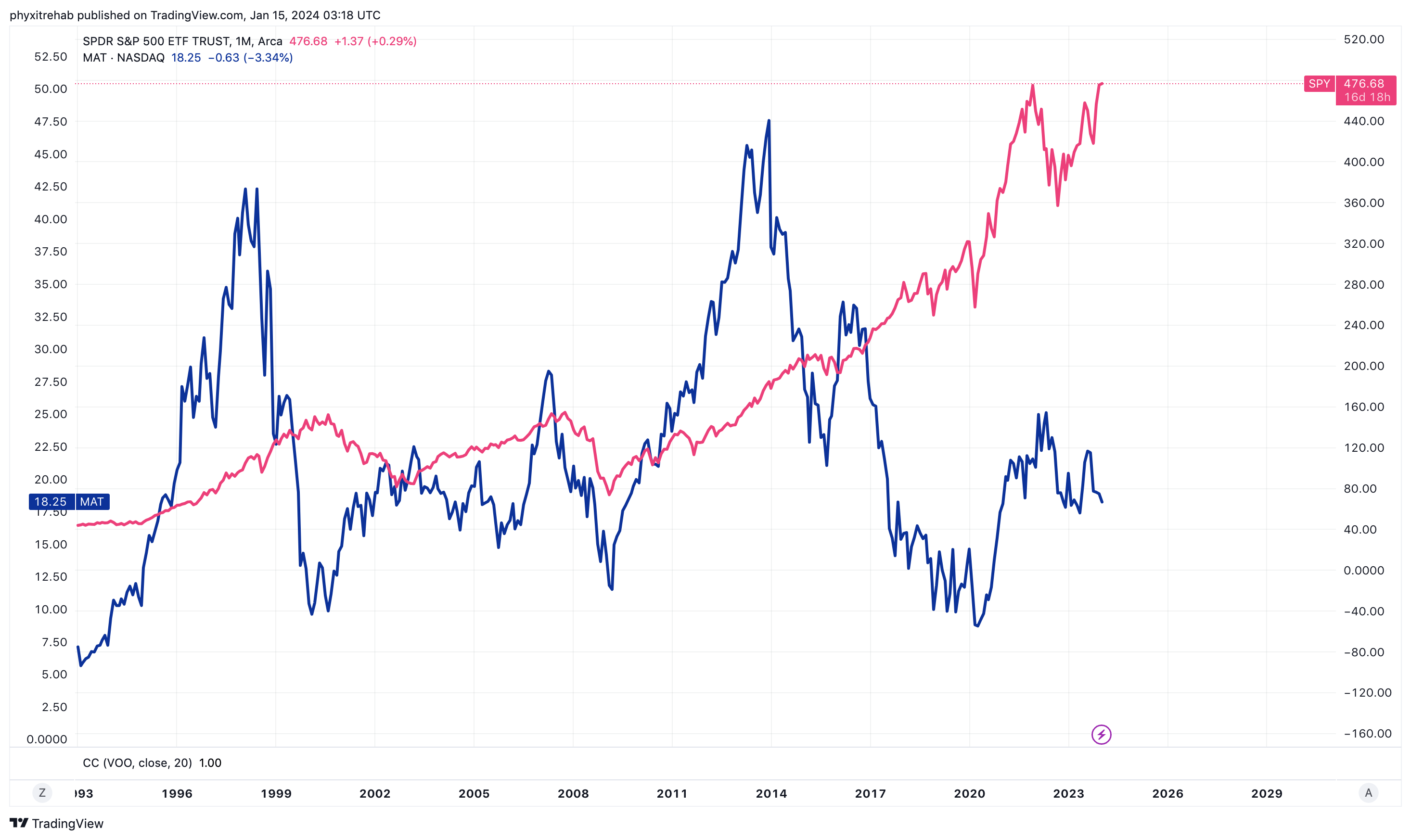

The question is exactly what lies on the horizon for MAT shareholders, current and prospective. This is a company that has substantially underperformed the benchmark indices in the last 10-years or so (Figure 3), now diverging further from the broad market. The case for a reversal is yet to be seen in our view.

This report will cover all of the moving parts in the MAT investment debate, providing investors with the most informed investment reasoning possible. We rate MAT a hold on valuation, fundamentals, and economics at $15-$16/share. Net-net, rate hold.

Figure 3.

{kind=link}

Critical investment facts

In response to the question, " What is your view on investment X or Y", the immediate response should be, " What is your time horizon?". Naturally, there is a case for owning an asset over various holding periods, based on exogenous factors. I have outlined our views on MAT across all 3 investment horizons in the arguments below.

- Short-term investment returns (1-12 months)

Outcomes from the buying and selling of investment securities within the first 12 months are heavily dependent on the starting valuations paid. Cheaper starting multiples offer a statistical advantage to the upside.

MAT currently sells at 14.4x forward earnings and >77x trailing earnings. Both are well above industry averages. The issue here is, that, adjusted for growth forecasts, you're still paying 1.5x earnings, or $1.50 for every $1 of future growth. The market has also valued the firm at around 3x the net assets employed in the company, at a 7% cash flow yield as I write.

The question is what's on offer at these prices.

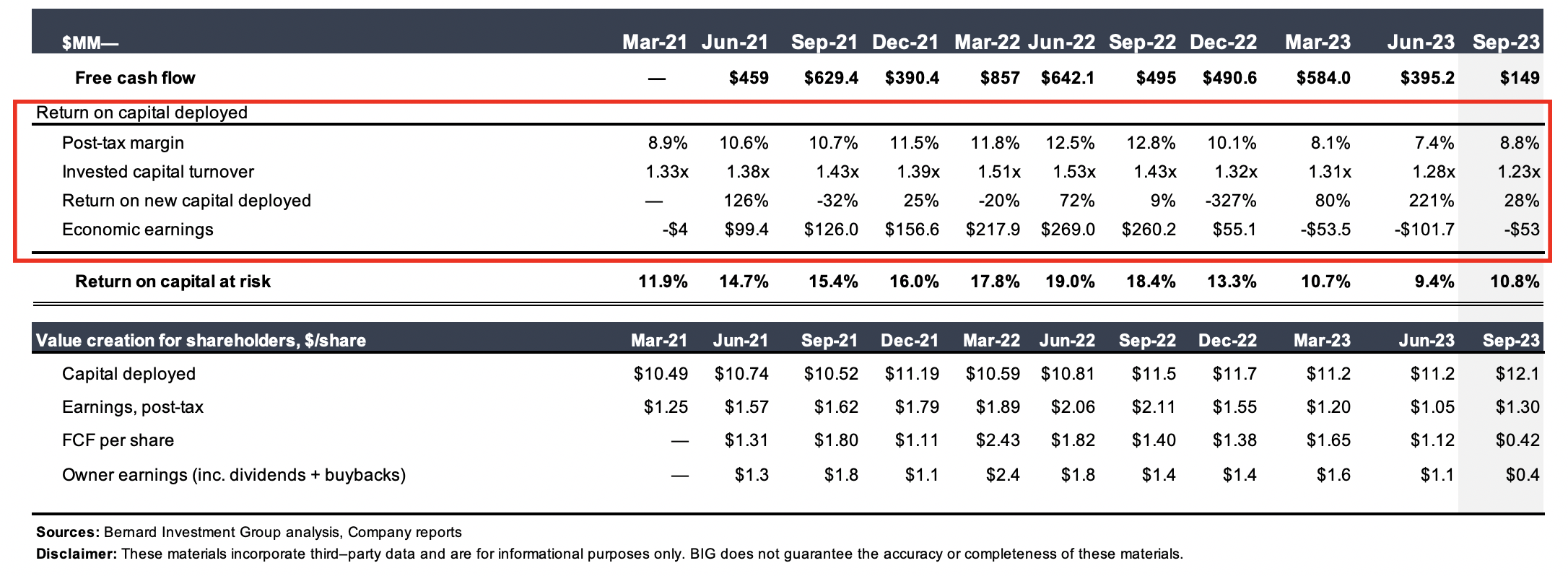

MAT produced a return of 4.16% on the equity capital in the business in the last 12 months, adjusting to 1.3% when paying 3.17x book value:

- Net equity capital of $2.03Bn or $5.76/share against earnings of $83mm or $0.23/share in the last 12 months, otherwise 4% ROE.

- Pay ~3x book value of equity = 3.17 x $5.76 = $18.25/share.

- Investor ROE = $0.23 / $18.25 = 1.3%.

As such, the scope for a re-rating due to a statistical discount is not apparent in our estimation, sporting the notion of a hold on MAT.

- Mid-term investment returns (1-3 years)

The return of any corporate security over a 1-3 year window is intrinsically dependent on the fundamentals of the corporation, i.e. sales and earnings growth.

MAT is a mature-phase company, with limited reinvestment opportunities given its size and market share. External factors-such as the Barbie movie, for instance-are typically the catalysts for price change in such a business.

Historically speaking, it has compounded sales at 2-3% since 2018, but earnings have decreased at about 8% per year on average since then. It has, however, compounded FCF methodically in that time, but thanks to asset disposals and use of leverage to finance asset sales rather than returns on capital invested. For reference, on MAT's balance sheet, $2Bn of equity is holding up $6.2Bn of assets, illustrating the firm's 3x multiplier on equity from use of debt.

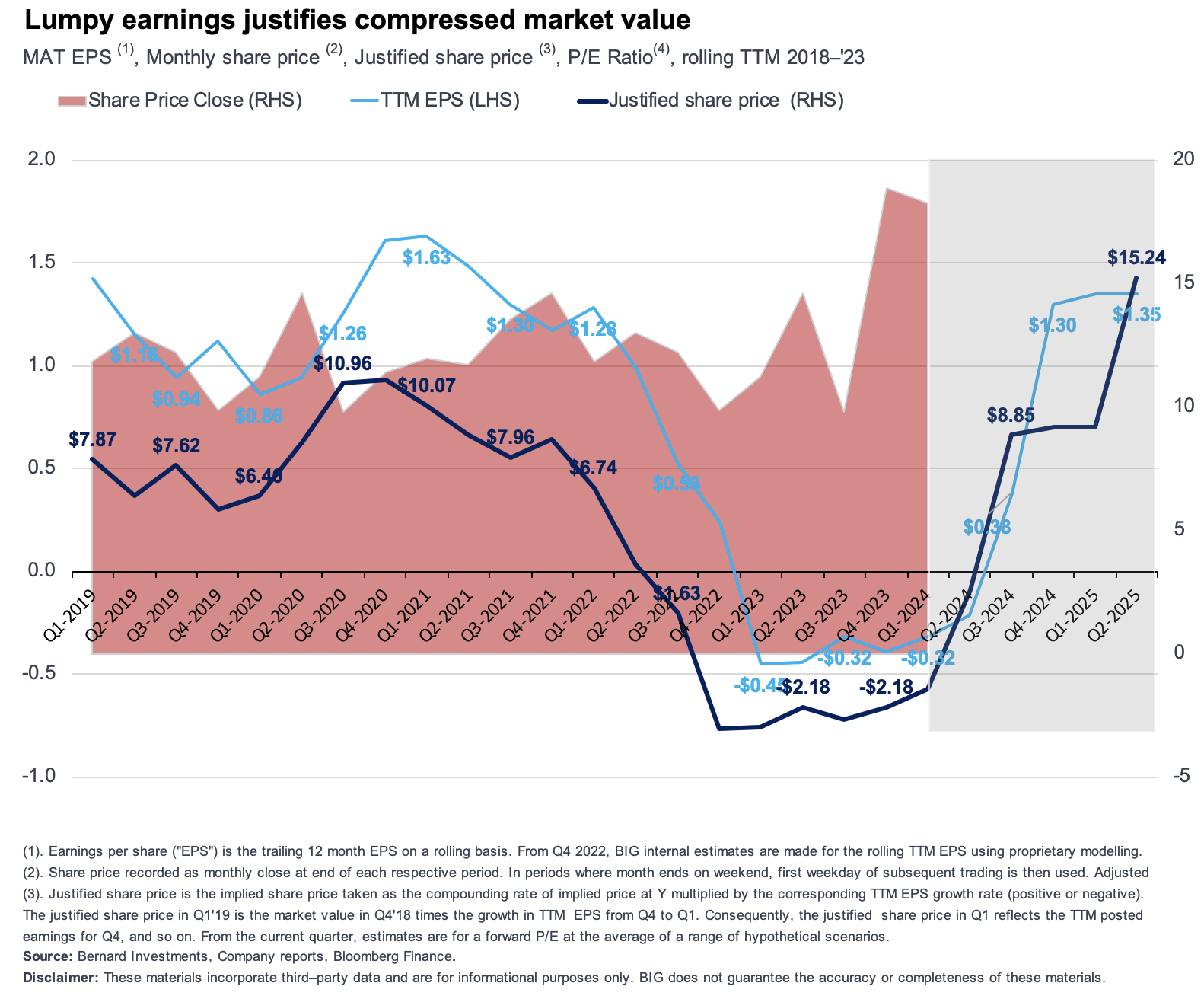

Moreover, both historical earnings and projected earnings assumptions out to FY'25 support MAT trading below $20/share in my estimation. As seen in Figure 4, the company is worth around $15-$16/share under our forward growth assumptions, around 20% below the current cost. In that vein, the rating off MAT's 2023 lows was supported in the data.

Consequently, a buy rating for those investors holding stocks for 1-3 years minimum is not well supported based on these findings. With sales + earnings growth clamped, and no dislocation in price-value, investment returns are soft, especially compared to the raft of selective opportunities available elsewhere in more valuable industries.

Figure 4.

{kind=link}

- Long-term investment returns

Judgement on a company's long-term investment prospects should ideally centre around a discussion on business economics. How much capital (cash from investors) has the company consumed, what level of profits against this capital does it produce. The lower and higher the better, respectively.

The case for owning MAT over any extended duration falls apart when analysing in these terms.

Critically:

- MAT had $12.10/share of capital invested into the business as of Q3 '23

- It produced $1.30/share in trailing post-tax earnings on this, a 10.8% return on investment.

- From 2020-2023, it invested another $1.57/share of capital to maintain its competitive position. It produced an additional $0.05/share in NOPAT on this, just 3% incremental return on investment.

- Investors could have literally just bought the index over this time, endured the drawdown of 2022, and still be positioned at multiples above MAT's equity line.

This is all good info-but it's already happened. We need understanding of what the expectations are ahead.

I would draw investors to the following datapoints:

- In this new age, MAT's products are undifferentiated and there is no additional brand value above the other toy and play retailers. This is evidenced by the fact it draws in 8-10% margins post-tax on $5.2Bn of TTM sales, meaning it possesses no consumer advantages that allow it to price its offerings above peers. Again, its offerings are largely undifferentiated.

- Normally, you'd expect such a firm to make up the slack in turnover, producing >$1 of sales for $1 of invested capital. MAT exhibits this form but not at a magnitude high enough to overcome the thin margins. It routinely does 10-12% return on capital, in-line with long-term market averages, precisely the reason for its flat equity line in the past 10 years by our estimation.

As a positive, it has compounded FCF per share methodically across 2023, scoring $1.30/share in Q3 vs. $0.53 in Q1 (TTM values). This is also higher than what was seen across 2020-'21.

On face value, this is constructive, except that:

(i). The firm also has ~$180mm in maintenance CapEx charge - 2.25x higher than its last 12 months earnings. It must invest the $180mm each rolling TTM period to remain competitive.

(ii). It employs no growth capital to expand the business, and is not mining the M&A pipeline at all.

(iii). It is not returning cash to shareholders via dividends or buybacks.

Where is the excess cash going?

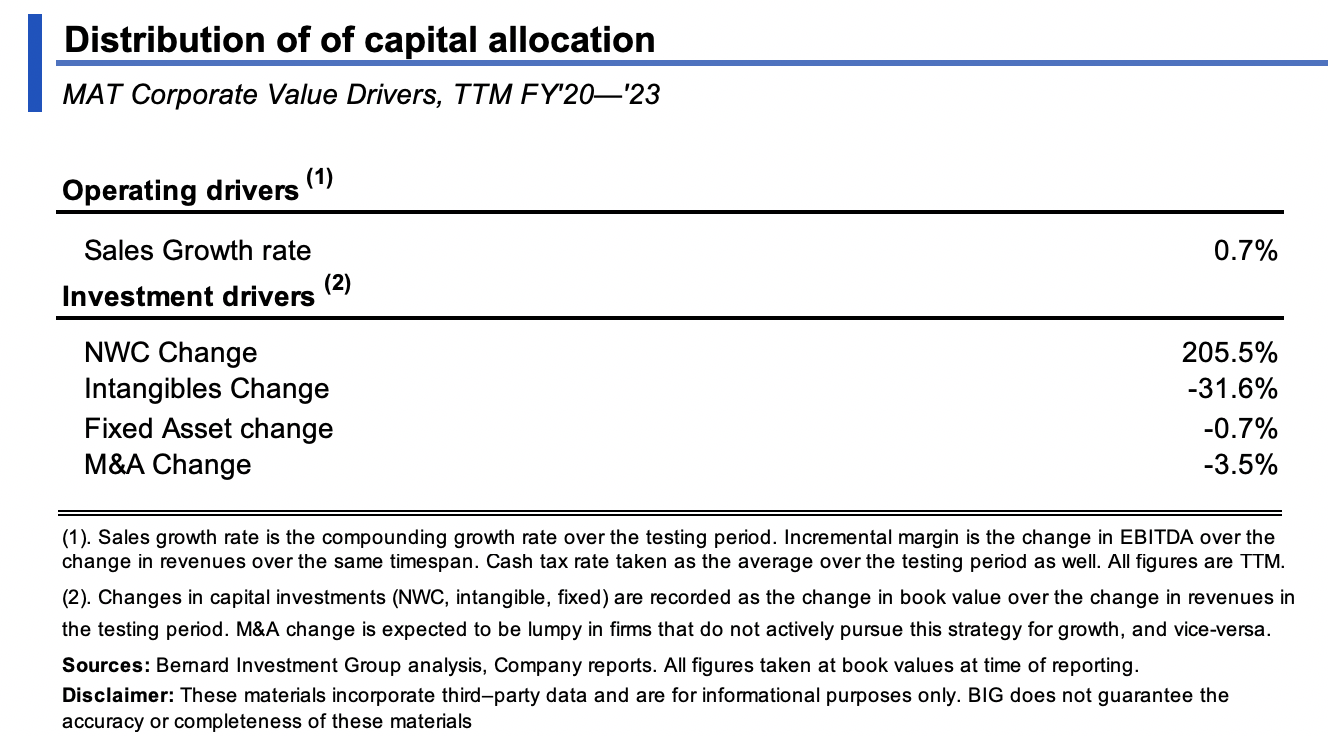

Quite simply, it is all consumed in MAT's capital-hungry working capital cycle. For instance, in the last 3 years, it has compounded sales a 30bps per period. To engender this growth, it took $2.05 investment to working capital for each new $1 in sales growth.

As such, basically all of MAT's cash flow is tied up in working capital, and it requires at least $2 of net working capital to produce $1 of sales.

That is where the cash is going.

From 2020-date, total receivables increased from $680mm to >$1.5Bn, inventories from $610mm to $790mm (30% change vs. just 7% sales growth), and total current assets up from $2Bn to $3.04Bn, on current liabilities of c.$1.3Bn.

As far as the economics of growth are concerned, this is not it. In that vein, the evidence supports a hold on MAT long term as well.

Figure 5.

{kind=link}

Figure 8.

{kind=link}

Discussion Summary

After factoring in all of the moving parts, a hold rating is supported for MAT across all investment horizons in our opinion. There is little statistical advantage provided in the short term from valuations, in the midterm from fundamentals + growth, or long-term from business returns or capital efficiency. Net-net, we estimate the stock is worth $15-$16/share, small downside from today's market price. Net-net, rate hold.

For further details see:

Mattel: Negligible Upside Across All Investment Horizons, Rate Hold